Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

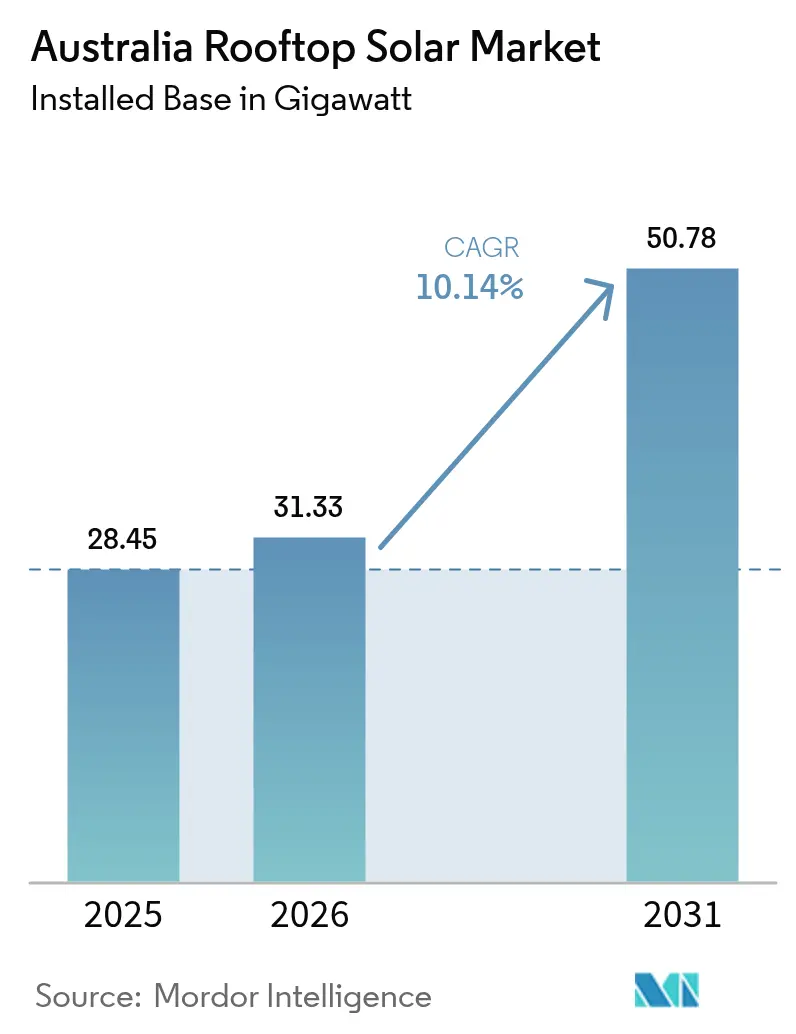

| Base Year Market Size (2025) | 28.45 gigawatt |

| Market Volume (2026) | 31.33 gigawatt |

| Market Volume (2031) | 50.78 gigawatt |

| Growth Rate (2026 - 2031) | 10.14% CAGR |

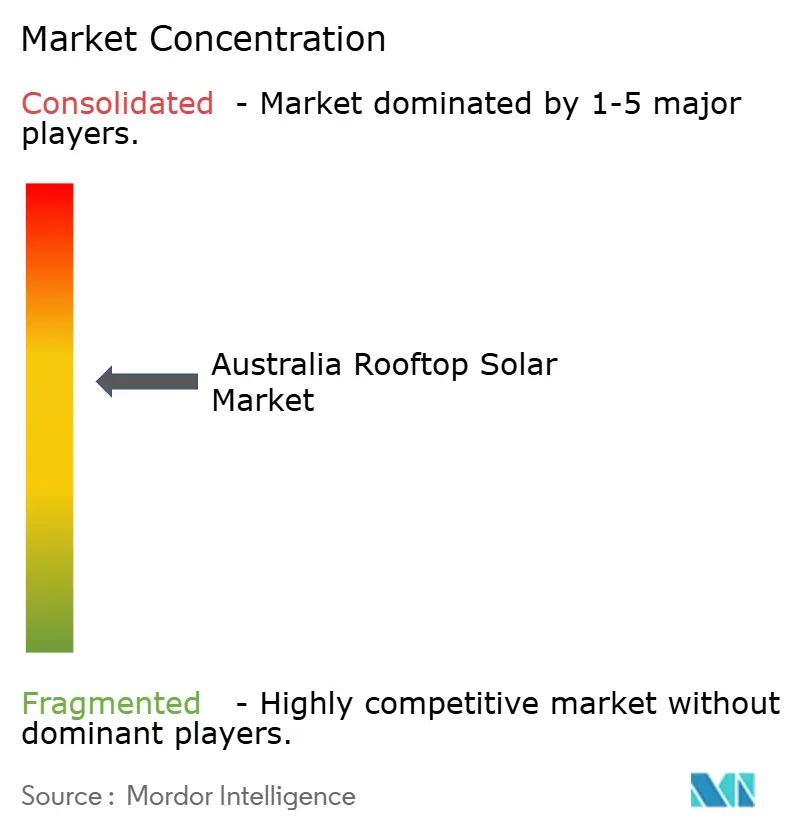

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Rooftop Solar Market Analysis by Mordor Intelligence

Australia Rooftop Solar Market size in 2026 is estimated at 31.33 gigawatt, growing from 2025 value of 28.45 gigawatt with 2031 projections showing 50.78 gigawatt, growing at 10.14% CAGR over 2026-2031.

This expansion elevates distributed generation from a helpful supplement into a key pillar of national electricity supply, already contributing more than 12% of grid power in 2025. Growth is propelled by a progressive policy mix, lower equipment costs, battery uptake, and rapid technological advances, while the federal Solar Sunshot program steers supply-chain localisation. Network operators are transitioning from static to dynamic operating envelopes, which raise export ceilings and enable higher rooftop penetration, notably in South Australia, where the 10 kW export limit is being addressed. Commercial momentum, expanding virtual power plant participation, and larger average system sizes indicate an accelerating shift from residential dominance toward diversified, service-oriented business models across the Australian rooftop solar market.

Key Report Takeaways

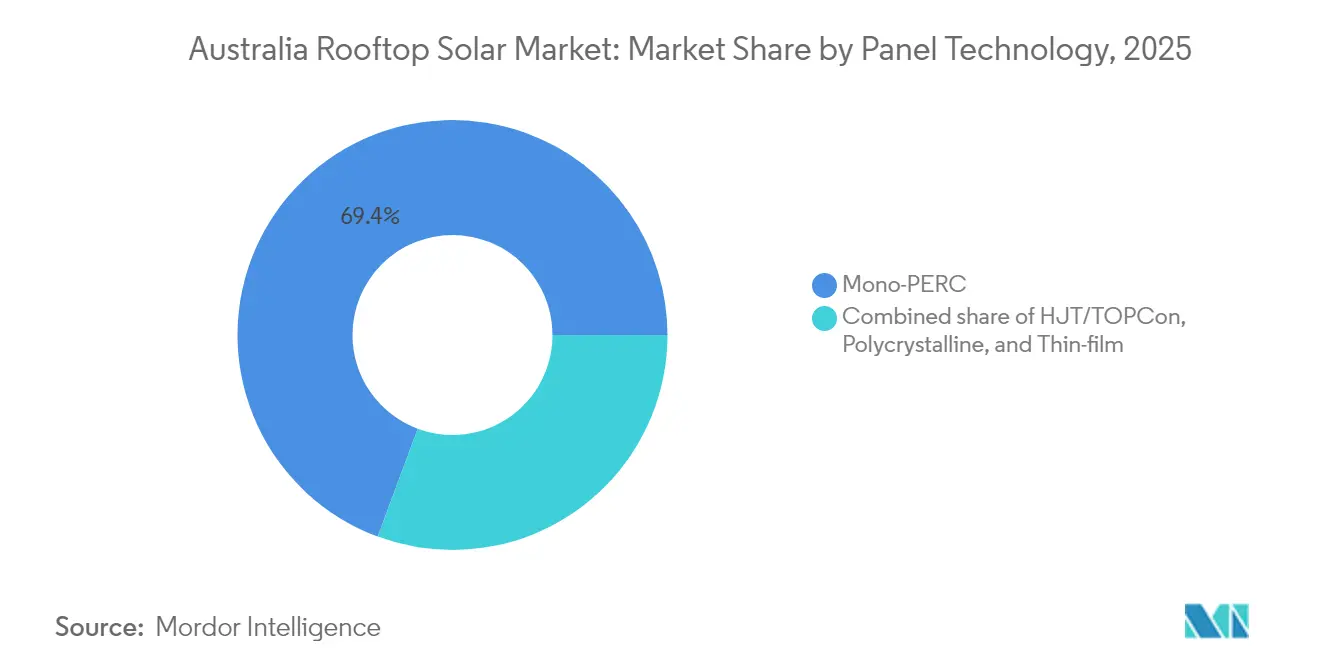

- By panel technology, mono-PERC panels commanded a 69.35% revenue share of the Australian rooftop solar market in 2025, whereas heterojunction and TOPCon are forecasted to grow at a 16.3% CAGR to 2031.

- By system size, the 5 to 10 kW range captured 44.20% of Australia's rooftop solar market size in 2025; the 30 to 100 kW band is projected to expand at a 13.9% CAGR between 2026-2031.

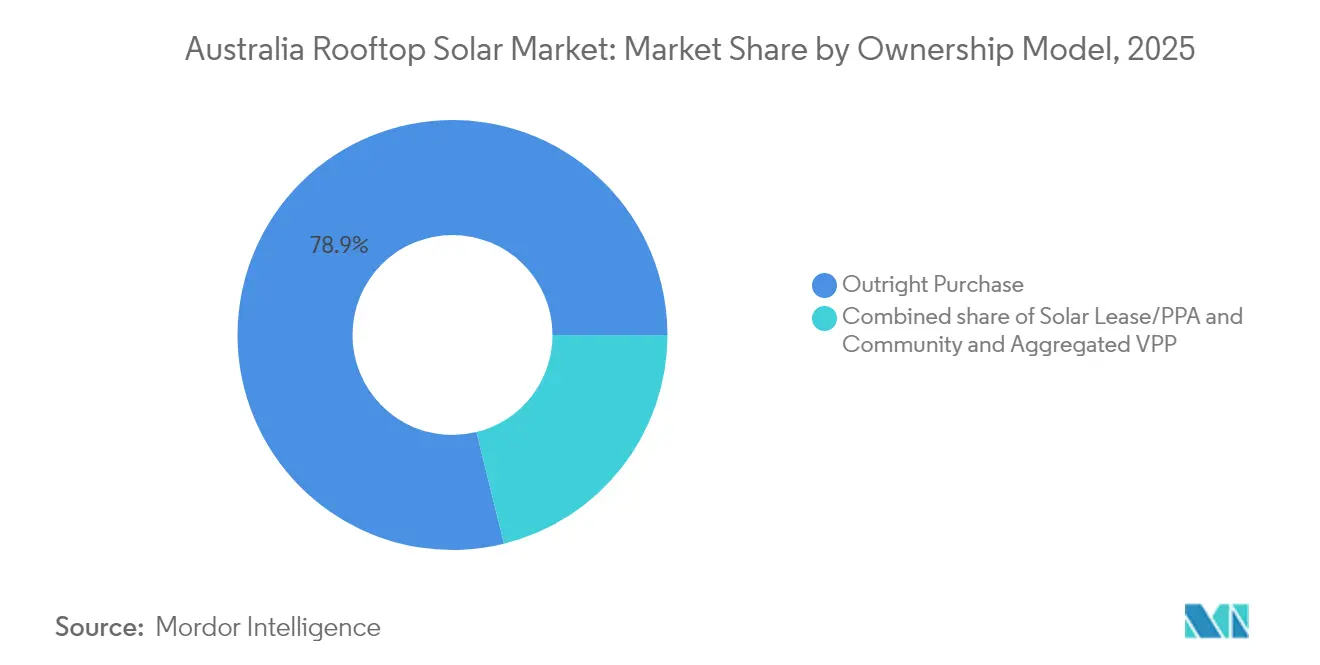

- By ownership model, outright purchase held 78.85% of Australia's rooftop solar market share in 2025; however, community solar and VPP aggregation are expected to grow fastest at a 19.1% CAGR to 2031.

- By end user, the residential segment accounted for 67.10% of Australia's rooftop solar market share in 2025, while commercial and industrial installations are set to post the fastest growth at 12.05% CAGR through 2031.

- Queensland led in total installations with more than 1 million systems in 2024, but South Australia delivered the highest penetration at 10.7% of the state's electricity demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Rooftop Solar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining PV & battery costs | +2.8% | National, with early gains in Queensland, NSW, Victoria | Medium term (2-4 years) |

| SRES & state-level rebates continuity | +2.1% | National, enhanced in Victoria, NSW, ACT | Short term (≤ 2 years) |

| Rising retail tariffs shortening payback | +1.9% | National, most pronounced in SA, Victoria | Short term (≤ 2 years) |

| Virtual-power-plant (VPP) program uptake | +1.4% | SA leading, expanding to Victoria, NSW | Medium term (2-4 years) |

| Mandatory climate-reporting for C&I roofs | +1.2% | National, concentrated in major cities | Long term (≥ 4 years) |

| Solar Sunshot Program & local mfg push | +0.8% | National, focused on NSW Hunter Valley, SA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining PV & Battery Costs

Combined module and storage prices continue falling. The average home solar payback period dropped below five years in 2024, while battery packs approached AUD 10,000, encouraging paired installations. CSIRO’s perovskite research achieved 11% efficiency on printed cells, signalling future cost declines via roll-to-roll manufacturing.[1]CSIRO, “Printed flexible solar cell milestone,” csiro.au Price deflation coincides with rising retail tariffs, thereby accelerating the adoption of both products across households and businesses. With virtual power plant revenue stacking, batteries now generate grid services income that further shortens returns. Cost trends, therefore, underpin a self-reinforcing adoption loop in the Australian rooftop solar market.

SRES & State-Level Rebates Continuity

The federal Small-scale Renewable Energy Scheme remains in force to 2030, underwriting certificate income that de-risks purchases. Victoria’s battery rebate and NSW’s Empowering Homes package add upfront discounts that sway system sizing decisions. These layered incentives lift installation volumes, stabilise installer pipelines, and steer buyers toward larger arrays that future-proof consumption. Consistent rebate rules across jurisdictions reduce stop-start cycles and sustain installer employment, anchoring growth in the Australian rooftop solar market.

Rising Retail Tariffs Shortening Payback

Wholesale electricity costs rose 83% in 2024, following coal retirements and increased peak-demand volatility. Concurrently, feed-in tariffs slid to 3 c/kWh, shifting value from export to self-consumption. The tariff gap makes rooftop solar the cheapest retail supply option, particularly for businesses exposed to demand charges. Enterprises therefore pursue solar-plus-storage to cap exposure to high spot prices, reinforcing the commercial growth runway across the Australian rooftop solar market.

Virtual-Power-Plant (VPP) Program Uptake

South Australia’s VPP demonstrates aggregated value, pooling more than 1 MW of home batteries for frequency response services. Victoria has 700,000 eligible rooftops, providing the critical mass for statewide orchestration. Participation generates new revenue streams that boost residential economies and opens up merchant models for aggregators. Expansion into small businesses broadens capacity under management, tapping idle battery assets during work hours and boosting resilience to blackouts nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid export limits & congestion | -1.8% | SA, Victoria leading, spreading to Queensland, NSW | Short term (≤ 2 years) |

| Import-linked supply-chain volatility | -1.2% | National, affecting all segments equally | Medium term (2-4 years) |

| Ageing early systems needing retrofits | -0.9% | National, concentrated in early adoption areas | Medium term (2-4 years) |

| Tougher fire-safety / building codes | -0.6% | National, with stricter enforcement in Victoria, NSW | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Export Limits & Congestion

High-penetration feeders experience voltage rise and thermal constraints that compel dynamic export caps. South Australian trials across 2,835 inverters verified software limits that safeguard stability while returning AUD 250 annually to a 10 kW system. AEMO earmarked AUD 16 billion for transmission upgrades to absorb renewable peaks.[2]Australian Energy Market Operator, “2025 Integrated System Plan,” aemo.com.au Until these lines are built, rooftop export ceilings limit revenue, prompting households to opt for batteries and curbing unconstrained growth in the Australian rooftop solar market.

Import-Linked Supply-Chain Volatility

Rooftop panels remain 99% import-dependent, leaving installers vulnerable to freight hikes and geopolitical shocks. The AUD 1 billion Solar Sunshot initiative aims to localise module assembly in the Hunter Valley and South Australia, with SunDrive trialling copper-based cells at pilot scale. Yet domestic polysilicon and glass facilities are years away, so currency swings and shipping delays can inflate costs and elongate project cycles, tempering the otherwise strong demand trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Panel Technology: Next-Generation Efficiency Disrupts Mono-PERC Leadership

Mono-PERC cells delivered 69.35% of system shipments in 2025, maintaining a price-performance sweet spot. Yet, heterojunction and TOPCon lines are scaling swiftly, registering a 16.3% CAGR to 2031 and edging towards parity on a $/W installed basis. Lifespans above 30 years and temperature coefficients below 0.3% per °C drive commercial site preference for these higher-efficiency modules. Polycrystalline shares continue to contract due to lower efficiency, while thin-film technology positions itself in weight-constrained structures.

SunDrive’s copper-plated heterojunction cell has reached commercial pilot runs with Trina, opening a local high-efficiency supply. CSIRO’s printed flexible cell roadmap targets building-integrated photovoltaic cladding that could revolutionise supermarkets and warehouses. Maxeon’s 24.1% IBC module offering launched in Q3 2024 anchors the premium residential segment. Technology choices, therefore, revolve around space constraints, degradation rates, and embodied-carbon goals, steering differentiation within the Australian rooftop solar market.

By System Size: Mid-Range Dominance Faces Commercial Scaling

Systems between 5 kW and 10 kW secured 44.20% of Australia's rooftop solar market share in 2025, reflecting typical suburban roof space and electricity use. Average installs hit 9.9 kW that year as households future-proofed for electric vehicles. Simultaneously, the 30 to 100 kW commercial class is forecast to register the fastest growth, with a 13.9% CAGR, fueling capacity uplift among warehouses, schools, and shopping centers. The up to 5 kW tier is being phased out as small-scale tariffs decline, while the 10 to 30 kW tier suits boutique commercial premises and larger homes.

Large roofs above 100 kW, though a smaller count, yield outsized megawatt additions. Smart inverters in this bracket participate in frequency markets, monetising otherwise curtailed energy. Businesses cluster charging stations under solar canopies, coupling daytime photovoltaic output with fleet electrification strategies. Module efficiencies near 24% reduce the surface area for a given wattage, allowing tighter footprints to accommodate higher ratings and enhancing the mid-range class's appeal. Thus, size dynamics continue to diversify as the Australian rooftop solar market matures.

By Ownership Model: Community Solar Disrupts Traditional Purchase Patterns

Outright purchase retained a 78.85% share of the Australian rooftop solar market in 2025, underpinned by rebate frameworks that reward owner-operators. Yet community projects, leases, and PPAs are chipping away at this dominance. Community and VPP aggregation shows a 19.1% CAGR, granting apartment tenants and renters access to shared arrays. Leases eliminate upfront costs, and PPAs provide cheaper power than the grid without requiring a capital outlay.

RACV’s commercial VPP product bundles battery hardware, grid services, and maintenance into a single bill, illustrating the shift in service. Developers of build-to-rent housing add communal rooftop arrays with transparent allocation of kilowatt-hours to tenants. As retail margins tighten, electricity retailers are integrating solar hardware bundles into their tariff plans, creating stickier relationships and generating data-rich customer insights. These models collectively reduce inequality in solar access and diversify revenue streams across the Australian rooftop solar market.

By End User: Commercial Momentum Challenges Residential Dominance

Residential rooftops accounted for 67.10% of installed capacity and revenues in 2025, driven by accessible financing and widespread installer networks. However, mandatory climate-reporting rules drive corporations to publicise scope-2 emissions cuts, spurring a 12.05% CAGR for commercial and industrial arrays through 2031. Commercial projects benefit from daytime load alignment and demand charge avoidance, generating superior internal rates of return compared to households. Retrofit activity is rising among 2010-era homes that require inverter swaps or size expansions, opening a secondary market. Companies are layering batteries onto solar to sell frequency response, deepening the value proposition and tilting the Australian rooftop solar market toward business-led deployments.

Commercial estates also unlock bundled energy-management contracts that combine solar, storage, and efficiency retrofits. Supermarket groups, breweries, and cold-storage operators are prime adopters, aligning rooftop output with refrigeration loads to hedge volatile wholesale power. Leasing and power-purchase agreements shift capital off balance sheets, allowing firms to claim decarbonization without upfront cash. This convergence of disclosure pressure, tariff arbitrage, and finance innovation accelerates the commercial share of capacity additions in the Australian rooftop solar market.

Geography Analysis

Queensland counted more than 1 million rooftop systems and 3.8 GW of capacity in 2024, maintaining numerical leadership on the back of abundant irradiance and business-friendly feed-in structures. Brisbane’s suburban sprawl provides ample roof surface, while regional councils streamline permitting. New South Wales added 970 MW during 2024 as Sydney households and inland agribusinesses chase hedge value amid volatile wholesale prices. Victoria, an early adopter state, is now pivoting to battery incentives that boost self-consumption ratios and trigger two-stage retrofits on mature homes.

South Australia leads the way in penetration, at 10.7% of overall consumption, thanks to its strong solar resource and early policy support, making the state a live laboratory for dynamic export limit trials. Western Australia’s isolated South West Interconnected System necessitates a more nuanced balancing of rooftop generation with limited interconnection, prompting the development of battery and demand-response schemes. Tasmania’s hydro dominance reduces solar urgency, yet niche off-grid communities adopt hybrid diesel-PV-battery microgrids to reduce fuel logistics costs.

AEMO’s integrated system plan earmarks AUD 16 billion for new inter-state lines that lift rooftop hosting capacity and strengthen east-to-west power flows. Queensland commissioned the country’s first commercial solar panel recycling plant in October 2024, tackling looming waste streams and retaining valuable materials such as silver and silicon. The Solar Sunshot program clusters pilot module lines in NSW’s Hunter Valley, leveraging existing materials know-how, while South Australia nurtures inverter and battery assembly. These geographic nuances shape policy, infrastructure, and industry development vectors within the Australian rooftop solar market.

Competitive Landscape

Competition remains fragmented among thousands of accredited installers, resulting in tight margins for simple residential systems. Chinese module giants Trina, Jinko, and LONGi dominate the supply, yet product differentiation arises from warranty lengths, degradation guarantees, and smart inverter integration. Premium niche vendors such as Maxeon and REC capture high-efficiency demand segments. Origin Energy is vertically integrating by co-investing with SunDrive in heterojunction pilot fabrication, creating a home-grown technology pathway.

Retail energy incumbents bundle rooftop packages with electricity tariffs to defend customer bases. AGL repurposes land at retired coal plants into recycling hubs, differentiating on circular-economy credentials. Specialized EPCs focusing on commercial rooftops deploy energy-management software that taps demand-response revenue, raising the bar for integrated offerings across the Australian rooftop solar market.

Virtual power plant operators represent an emerging competitor category. RACV leverages its automotive club membership to cross-sell solar-battery bundles, while Amber Electric’s spot-price-linked retail plan dynamically manages customer batteries to capture arbitrage opportunities. Installers who can couple hardware with software and finance now win tenders from corporates seeking turnkey decarbonization. The ongoing tightening of AS/NZS 4777.2 inverter standards favors technically adept players, gradually weeding out small-scale installers and inching the market toward moderate consolidation.

Australia Rooftop Solar Industry Leaders

Trina Solar

JinkoSolar

LONGi Green Energy

Maxeon (SunPower)

Canadian Solar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Australia's Solar Energy Industries Association (SEIA) has urged the nation's climate change and energy minister to "urgently intervene" on a rule change that poses a risk to the adoption of rooftop solar PV. The new rule, set to take effect on 1 July 2025, coincides with the federal government's launch of its AUD 2.3 billion (USD 1.49 billion) Cheaper Home Batteries Program. Under this rule, certain accredited solar and energy storage specialists will be barred from collaborating with licensed electricians.

- June 2025: Wesfarmers secured a AUD100 million loan from the Clean Energy Finance Corporation, aiming to power Bunnings and Officeworks sites with 100% renewable electricity by the end of 2025. The funds will be allocated for solar installations, battery setups, and EV charging stations.

- November 2024: Australia proudly marks its 4 millionth rooftop solar installation, achieving a total capacity of 25 GW, with 3.15 GW added in 2023 alone. The Australian Federal Minister for Climate Change and Energy hailed this 4 millionth installation as a significant milestone for the nation.

- October 2024: Trina Solar and SunDrive have formed a joint venture in Australia, aiming to accelerate the production of high-efficiency heterojunction solar cells. This majority Australian-owned venture combines SunDrive's cutting-edge solar technology with Trina Solar's global manufacturing expertise.

Australia Rooftop Solar Market Report Scope

The Australian Rooftop Solar Energy market report includes:

By Panel Technology

| Mono-PERC |

| HJT/TOPCon |

| Polycrystalline |

| Thin-film (CdTe/Perovskite) |

By System Size

| Up to 5 kW |

| 5 to 10 kW |

| 10 to 30 kW |

| 30 to 100 kW |

| 100 to 1 MW |

By Ownership Model

| Outright Purchase |

| Solar Lease/PPA |

| Community and Aggregated VPP |

By End User

| Residential |

| Commercial and Industrial |

| By Panel Technology | Mono-PERC |

| HJT/TOPCon | |

| Polycrystalline | |

| Thin-film (CdTe/Perovskite) | |

| By System Size | Up to 5 kW |

| 5 to 10 kW | |

| 10 to 30 kW | |

| 30 to 100 kW | |

| 100 to 1 MW | |

| By Ownership Model | Outright Purchase |

| Solar Lease/PPA | |

| Community and Aggregated VPP | |

| By End User | Residential |

| Commercial and Industrial |

Key Questions Answered in the Report

What is the current capacity of the Australia rooftop solar market?

Installed rooftop capacity reached 31.33 GW in 2026 and is forecast to climb to 50.78 GW by 2031.

How fast is the commercial segment growing compared with residential?

Commercial and industrial rooftops are projected to expand at a 12.05% CAGR, outpacing the overall market’s 10.14% growth.

Which system size dominates new installations?

Arrays between 5 kW and 10 kW hold 44.20% of 2025 installations, but 30 to 100 kW systems show the fastest growth.

What technologies are overtaking mono-PERC panels?

Heterojunction and TOPCon modules are gaining share at a 16.3% CAGR thanks to higher efficiencies.

How important are virtual-power-plants to future growth?

VPP participation adds revenue from grid services, raising battery returns and supporting widespread adoption, especially in South Australia and Victoria.

Is local manufacturing expected to reduce supply-chain risk?

Yes, the AUD 1 billion Solar Sunshot scheme and partnerships such as SunDrive-Trina aim to establish domestic module lines and lessen import dependency over the next five years.

Page last updated on: