Neurofeedback Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

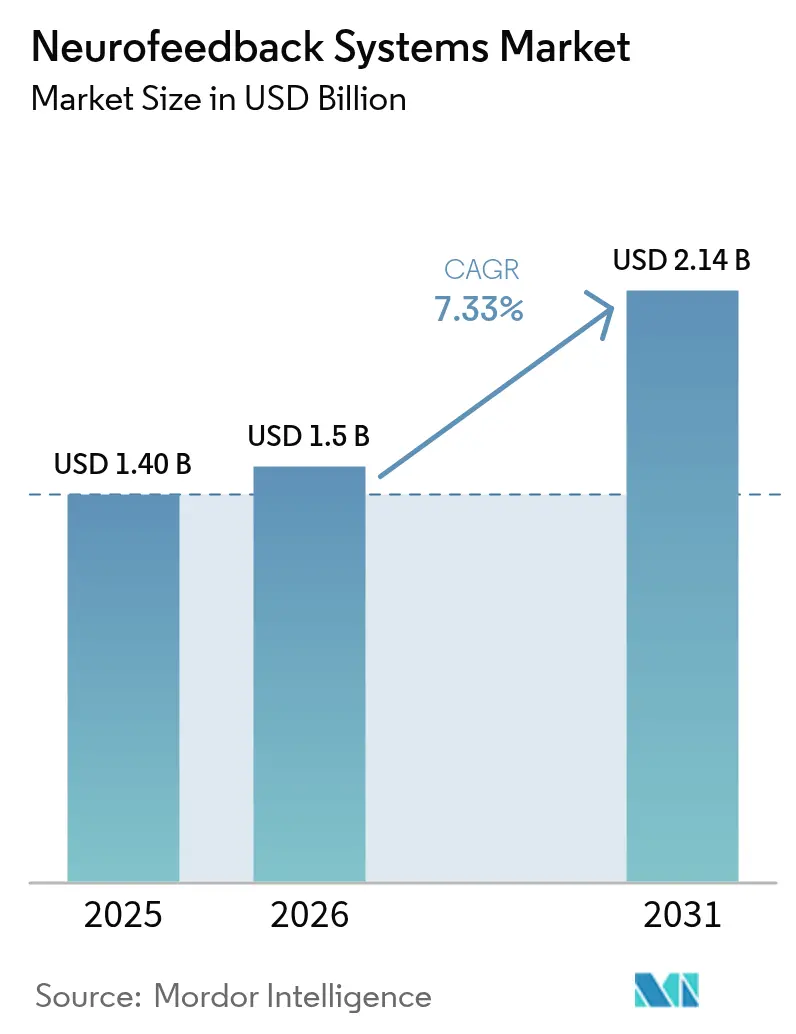

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurofeedback Systems Market Analysis by Mordor Intelligence

Neurofeedback systems market size in 2026 is estimated at USD 1.5 billion, growing from 2025 value of USD 1.40 billion with 2031 projections showing USD 2.14 billion, growing at 7.33% CAGR over 2026-2031. Clinical validation across multiple indications, wider regulatory acceptance, and the emergence of subscription-based business models have created favorable conditions for the sustained expansion of the neurofeedback systems market. FDA clearances for wearable ADHD systems, rising consumer interest in home-based cognitive wellness, and increasing pilot insurance coverage continue to strengthen the commercial case for non-pharmacological neurofeedback interventions. Portable and tele-enabled platforms now account for almost half of installed systems, showing how digital health infrastructures accelerate the neurofeedback systems market. At the same time, elite sports programs and military research units are adopting neurofeedback to optimize cognition, creating specialty demand pockets that reinforce overall revenue momentum.

Key Report Takeaways

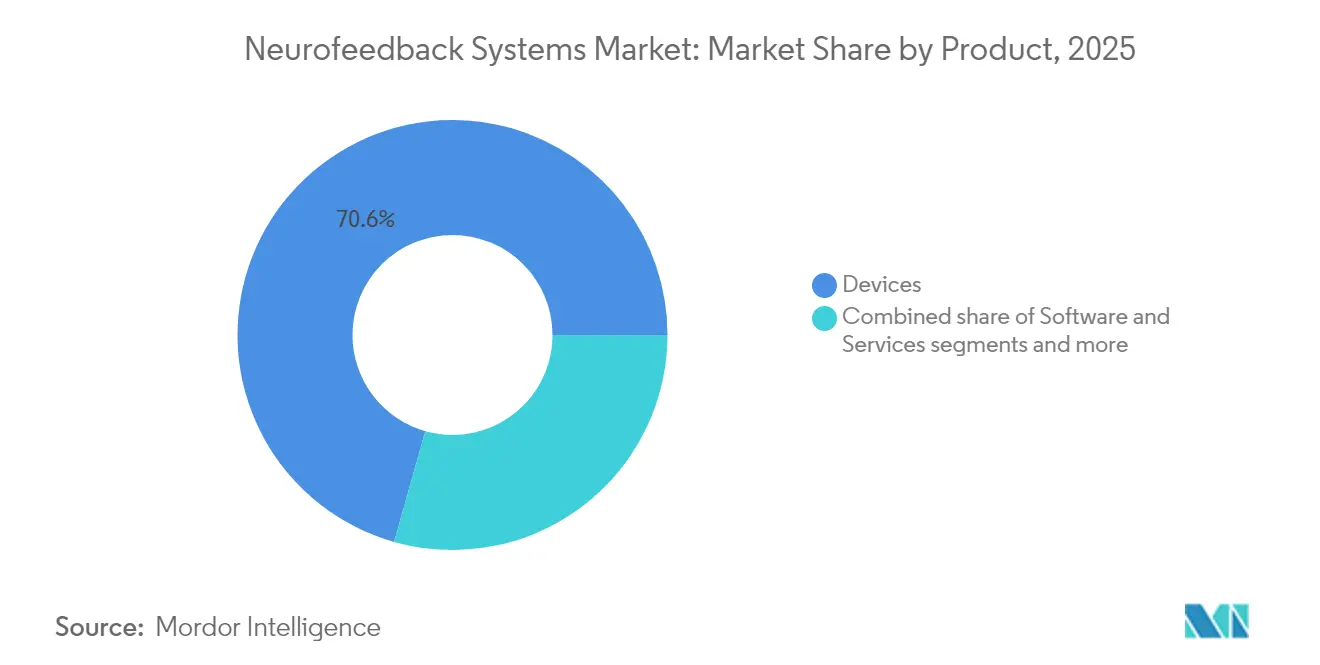

- By product type, devices accounted for 70.62% of the neurofeedback systems market share in 2025. Software and services are anticipated to expand at a 7.68% CAGR through 2031, the fastest pace within the ecosystem.

- By application, ADHD accounted for 31.45% of the neurofeedback systems market size in 2025, maintaining its leading position. Cognitive performance enhancement is projected to advance at an 8.01% CAGR to 2031, outpacing all other use cases.

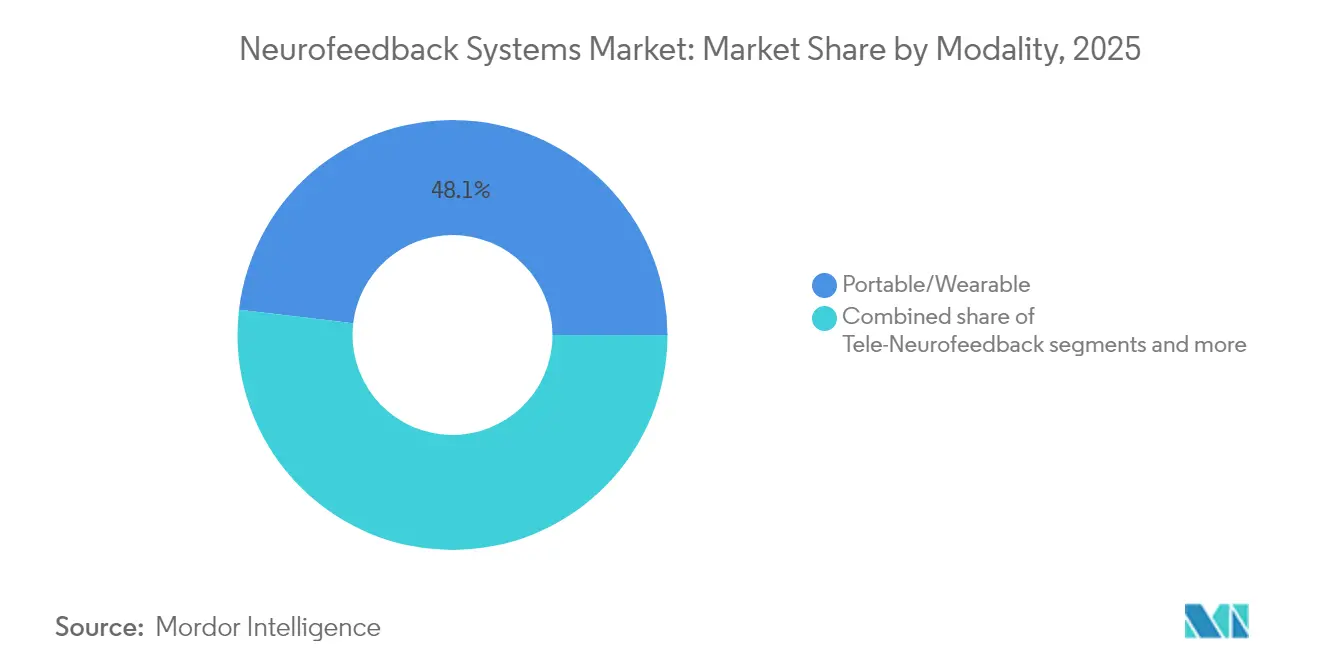

- By modality, portable/wearable systems captured 48.12% of revenue in 2025, underscoring user preferences for mobility. Tele-neurofeedback platforms are set to post the fastest 7.88% CAGR during 2026-2031 as remote care expands.

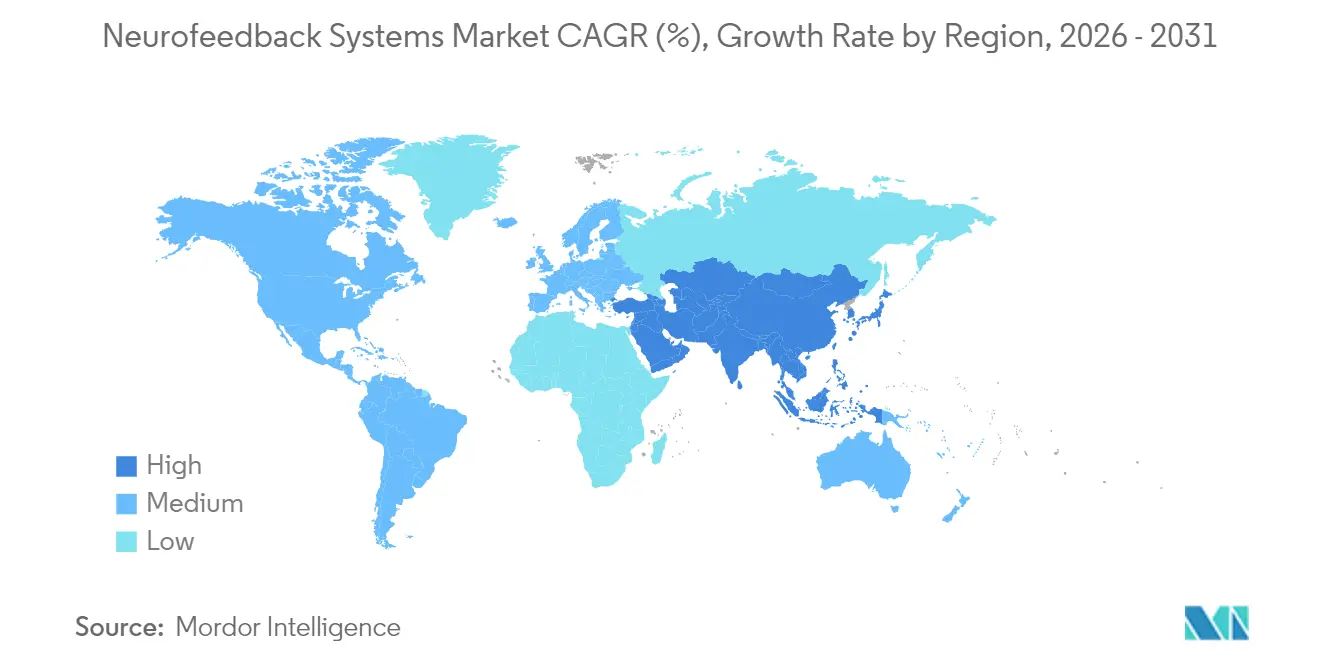

- By geography, North America led with 39.10% revenue share in 2025, thanks to mature reimbursement pilots and concentrated clinical research funding. The Asia-Pacific region is predicted to record an 8.07% CAGR through 2031, driven by rapid digital health rollouts and heightened mental health awareness.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurofeedback Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ADHD diagnoses driving clinical adoption | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Integration with wearables for at-home mental-wellness programs | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Increasing insurance coverage pilots for neurofeedback therapy | +1.2% | North America core, spill-over to Europe | Medium term (2-4 years) |

| Rise of elite-sports demand for cognitive performance training | +0.9% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| AI-enhanced signal processing improving treatment outcomes | +1.1% | Global, led by technology hubs | Long term (≥ 4 years) |

| Expansion of tele-neurofeedback platforms in rural care | +0.8% | APAC, Latin America, rural North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in ADHD diagnoses driving clinical adoption

Global ADHD prevalence climbed sharply post-pandemic, pressing caregivers to seek effective non-drug therapies. Randomized controlled trials show that mobile neurofeedback delivers significant gains in attention and response inhibition among children aged 8-15, with benefits sustained three months post-training. The FDA reclassification of digital ADHD therapy devices into Class II during September 2024 established special controls and simplified the 510(k) pathway[1]Source: U.S. Food and Drug Administration, “Classification of the Digital Therapy Device for ADHD,” federalregister.gov . Clinics subsequently integrated neurofeedback into first-line behavioral programs, which lifted utilization rates across theneurofeedback systems market. Commercial payers have responded by running limited reimbursement pilots, creating a virtuous cycle that accelerates equipment demand. Collectively, these factors add measurable growth momentum through 2028.

Integration with wearables for at-home mental-wellness programs

Consumer EEG modules embedded in earbuds and headbands now stream brain-state data to smartphone apps, enabling continuous stress management and mindfulness coaching. Meta-analyses confirm that combining consumer-grade neurofeedback with guided meditation reduces psychological distress, albeit with small effect sizes, but on an unparalleled scale. Corporate wellness programs have begun subsidizing these devices, expanding the neurofeedback systems market beyond clinical settings. Device makers leverage cloud analytics to refine algorithms automatically, improving usability over time. Because wearables bypass clinic visits, they are well-suited for longitudinal mental-wellness initiatives, ensuring long-term demand.

Increasing insurance coverage pilots for neurofeedback therapy

Select U.S. payers now reimburse neurofeedback for childhood ADHD under defined protocols. Early outcome data show decreased stimulant dosage and improved academic performance, which lowers overall care costs. Legislators in several states have proposed parity mandates covering evidence-based digital therapeutics, increasing pressure on national insurers. Europe follows a similar trajectory through health-technology assessment frameworks that evaluate digital devices in a centralized manner. Stable reimbursement fosters equipment purchases by clinics, reinforcing the neurofeedback systems market.

Rise of elite-sports demand for cognitive performance training

Professional teams apply neurofeedback to shorten reaction times and sharpen decision-making under stress. Field studies in basketball and marksmanship show measurable gains after eight training sessions, prompting Olympic committees to fund larger trials. The military community mirrors this focus, exploring neurofeedback to enhance situational awareness during complex missions. Although volumes remain niche, high purchasing power boosts average selling prices and offers strong margins for vendors operating in the Neurofeedback devices industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited long-term clinical evidence for certain indications | -1.4% | Global, particularly in emerging markets | Medium term (2-4 years) |

| High device costs and capital-budget constraints in clinics | -1.1% | Developing economies, rural healthcare systems | Short term (≤ 2 years) |

| Lack of standardized training protocols for practitioners | -0.8% | Global, with variations in regulatory frameworks | Long term (≥ 4 years) |

| Data-privacy concerns in cloud-based home-use systems | -0.6% | Europe (GDPR), North America, privacy-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited long-term clinical evidence for certain indications

While short-term trials show efficacy in PTSD, chronic pain, and insomnia, meta-analyses caution that long-term durability of benefit remains under-documented. Major insurers therefore classify most neurofeedback procedures as investigational outside a narrow ADHD definition. Academic groups initiated multi-year studies to close this gap, yet results will not influence coverage decisions until after 2027. This evidence deficit slows uptake in indications where reimbursement is essential, tempering growth in the neurofeedback systems market.

High device costs and capital-budget constraints in clinics

A whole 24-channel clinical EEG neurofeedback rig can exceed USD 30,000, and a standard treatment cycle costs USD 2,000-8,000 per patient, significantly higher than cognitive behavioral therapy alternatives. Small community practices and rural hospitals often defer purchases, relying on referral networks instead. Vendors are now piloting subscription pricing and equipment-as-a-service models that amortize upfront costs, but acceptance remains uneven. Until financing models mature, hardware investment barriers will cap adoption, particularly in emerging markets, restraining the neurofeedback systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Maintain Leadership While Software Accelerates

Devices dominated revenue with a 70.62% share in 2025, underscoring the hardware-centric entry point of the neurofeedback systems market. EEG-based systems remain the workhorse for clinical ADHD and epilepsy protocols, while premium fMRI and fNIRS rigs cater to research centers focusing on emotion regulation and depression. Software and services, although smaller, are on track for a 7.68% CAGR through 2031, driven by demand for AI-driven analytics that fine-tune thresholds in real-time. Subscription dashboards create ongoing revenue streams that cushion suppliers from equipment replacement cycles.

The fNIRS subsegment is gaining visibility as recent ventrolateral prefrontal cortex training studies report marked reductions in negative affect among high-efficiency learners. Concurrently, fMRI-guided feedback shows clinically meaningful modulation of depression-related neural networks. Legacy platforms such as HEG and SCP/LENS occupy niche therapeutic corridors, especially within concussion management, adding specialized breadth to the neurofeedback systems market.

By Application: ADHD Maintains Lead as Performance Enhancement Gains Speed

ADHD accounted for 31.45% of the neurofeedback systems market size in 2025, solidifying decades of clinical research and strong demand from caregivers. Treatment outcomes include sustained attentional improvements, which reinforce confidence among pediatric neurologists. Cognitive performance enhancement, however, is advancing at an 8.01% CAGR, targeting professional athletes, pilots, and e-sports participants with non-invasive cognitive optimization protocols.

Anxiety and depression protocols benefit from amygdala-focused fMRI studies that demonstrate sizeable symptom reductions, while epilepsy programs retain consistent reimbursement due to established efficacy. PTSD interventions that leverage amygdala-derived EEG-fMRI patterns achieve 66.7% responder rates, indicating breakthrough potential in treatment-resistant populations. Sleep disorder solutions, including alpha-training regimens, demonstrate how the neurofeedback systems market continues to diversify to meet various patient needs.

By Modality: Portability Captures Nearly Half of Deployments

Portable and wearable platforms accounted for 48.12% of shipments in 2025, as patients and clinicians favored flexibility and lower total cost of ownership. Miniaturization advances ensure clinical-grade signal quality despite the use of fewer electrodes. Dense-sampling wearable fNIRS modules now enable the visualization of cortical oxygenation in real-world settings, opening new avenues for personalized mental health interventions.

Tele-neurofeedback services are expected to be the fastest-growing modality with an 7.88% CAGR to 2031, driven by favorable telehealth regulation and broadband expansion. In-clinic fixed installations remain indispensable for complex protocols such as deep-brain network mapping and multi-modal co-registration studies, maintaining a stable core within the neurofeedback systems market.

Geography Analysis

North America generated 39.10% of 2025 revenue, reflecting early FDA approvals, strong venture funding, and pilot reimbursement programs that span ADHD and stroke rehabilitation. Academic-industry collaborations drive technology refinement, evidenced by the BEAM™ platform developed with more than USD 40 million in federal research grants. Nevertheless, broad payer coverage remains limited, compelling clinics to blend cash payments with emerging insurance pilots.

Europe holds a solid second position, aided by the European Union’s joint health-technology assessment regulation that streamlines device evaluation across member states. National digital-health agencies in Germany, France, and Belgium expedite market access once clinical benefit is proven, and local payers have begun conditionally reimbursing digital neurofeedback for ADHD. Research institutes across the continent are exploring fNIRS and fMRI feedback for mood disorders, adding scientific gravitas to the regional neurofeedback systems market.

Asia-Pacific registers the fastest growth with an 8.07% CAGR projected through 2031. Governments in Japan and South Korea fund AI-enabled medical devices, accelerating regulatory approvals that favor domestic suppliers. China and India, with vast patient pools and growing telehealth ecosystems, are piloting low-cost portable EEG kits to bridge mental-health care gaps. The combination of policy support, technology manufacturing capability, and rising public health awareness propels Asia-Pacific to the forefront of neurofeedback systems market expansion.

Competitive Landscape

The neurofeedback systems market shows moderate fragmentation. No single vendor controls more than one-tenth of global revenue, yet leading players retain competitive advantages through patented algorithms and broad regulatory clearances. Companies such as NeuroSigma, Advanced Brain Monitoring, and Emotiv differentiate via AI-driven analytics that personalize feedback loops and shorten training cycles.

Strategic partnerships amplify innovation velocity. Emotiv’s 2025 investment in MYndspan integrates MEG biomarkers, such as Functional Brain Age, with consumer EEG, enriching multimodal brain-health profiling. Cognixion’s alliance with Blackrock Neurotech extends research access to non-invasive BCI architectures, fostering an open innovation culture. These collaborations signal a shift in the industry toward holistic neurotechnology ecosystems that integrate hardware with cloud analytics.

Cost-reduction initiatives also influence market dynamics. Open-source projects such as OpenNIRScap demonstrate that a functional NIRS cap can be assembled for under USD 1,000, challenging established suppliers to justify premium pricing with superior accuracy and supportive clinical data. Vendors respond by bundling turnkey training curricula and outcome reporting to preserve value. Overall, competition centers on clinical efficacy, ease of use, and total cost of ownership rather than on hardware alone.

Neurofeedback Systems Industry Leaders

Brainmaster Technologies, Inc

Mind Media

NeuroCare Group GmbH

Neurobit Systems

BEE Medic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in neurofeedback systems are increasingly tied to clearer pathways for clinical commercialization and evidence generation. In the United States, neurofeedback products commonly move through the FDA Class II framework for biofeedback devices, and multiple 510(k) clearances for neurofeedback software systems (for example, GrayMatters Health Ltd. Prism and IASIS Technologies IASIS i2) point to an active route for adjunctive-use indications such as symptom management in PTSD. That combination creates scope for vendors to package outcomes reporting, practitioner training, and protocol standardization into their software and services layer, especially as portable and tele-enabled platforms broaden access beyond specialty centers.

In the near term, go-to-market headroom is more about standardization, interoperability, and payer-facing proof than adding new hardware channels. As of May 2026, the FDA maintained recognized consensus standards relevant to EEG biofeedback systems and software, which supports vendor investment in compliant signal-processing pipelines and quality systems that reduce friction during updates and new configurations. On the demand side, research translation programs and workshops led by bodies such as the National Institute of Mental Health (NIMH) reinforce a shift toward trial designs and validation packages that can support broader clinical uptake, while subscription and equipment-as-a-service models help address capital barriers tied to higher-end clinical EEG neurofeedback rigs.

Recent Industry Developments

- May 2026: NeuroCare Group AG received regulatory approval to market its TMS devices in Saudi Arabia, extending its Middle East footprint in regulated neurotherapy markets. The approval complements the companys broader platform approach that combines clinic delivery with digital therapy tooling.

- September 2025: BrainMaster Technologies Inc. was awarded a U.S. Marine Corps purchase order (H9225725PE055) for BrainMaster equipment. Government procurement supports installed-base visibility and can accelerate follow-on demand for training, accessories, and compatible software across military and performance-focused use cases.

- July 2024: NeuroCare Group AG acquired Smart TMS in the UK, expanding its clinic presence across the UK and Ireland and enabling wider deployment of its Digital Therapy Platform across the acquired network. Consolidation at the provider level can increase utilization of neurofeedback-adjacent systems through standardized protocols and centralized technology adoption across multiple sites.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the neurofeedback systems market is defined as the revenue generated from equipment and related software used to record brainwave signals and provide feedback that helps users train or regulate those signals in clinical, research, and supervised wellness settings.

Scope exclusions: We exclude general EEG diagnostic-only systems that are not configured or sold for neurofeedback training, along with non-device services that are not tied to a neurofeedback system sale or license.

Segmentation Overview

- By Application

- Attention Deficit Hyperactivity Disorder (ADHD)

- Pain Management

- Insomnia

- Anxiety Disorder

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the base structure of the market, we start with public sources that explain disease burden, care pathways, and where neurofeedback is actually being used. Useful inputs come from sources such as the US FDA device databases, the US National Library of Medicine (ClinicalTrials.gov), PubMed-indexed clinical papers, and CDC mental health related statistics that help validate demand-side context.

We also review non-paywalled materials such as university hospital websites, association publications on neurotherapy and behavioral health, and company filings and investor presentations for product positioning and broad revenue disclosures. Pricing references are cross-checked using publicly visible catalogs and reimbursement or coverage commentary where available, and patent databases help track how sensing, signal processing, and training software are evolving. These desk sources are supported by paid subscriptions used for company financials and intelligence, news and financials, and selective patent analytics. The list mentioned here is not exhaustive, because many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to translate the desk-based view into realistic adoption and pricing assumptions, by speaking with clinic operators, hospital department stakeholders, researchers, and channel-side participants who can describe ordering patterns and usage frequency. Because this is a global market, we also ensure respondent inputs are collected across major regions, so device placement and software licensing, as well as any home-use momentum, are not overstated from a single geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 40% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 15% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where the demand pool is reconstructed from treated and trainable cohorts, typical care settings that offer neurofeedback, and the expected rate of system placement per site. We then convert those placements into annual revenue using pricing and replacement cycles.

Once the broad totals are formed, we corroborate them with selective bottom-up checks, such as sample roll-ups of supplier activity, channel checks on unit movement, and a volume times average selling price logic applied to device and software components.

Inputs that matter in this market include clinic and hospital adoption rates for neurofeedback programs, the split between device sales and software licensing, average sessions supported per system per week, refresh and upgrade cycles for amplifiers and sensors, and the pace of regulatory clearances that expand addressable use. Since the system mix is shifting toward portable and tele-enabled formats, we also adjust assumptions for home-use share and subscription duration where evidence supports it.

For forecasting, we apply scenario analysis so growth is not forced into one line. The scenarios are anchored to interview consensus on adoption speed, pricing progression, and regional expansion. Where bottom-up signals are thin in smaller countries, we handle gaps using proxy indicators like the count of operating neurotherapy providers and relative healthcare spending, and then we review those assumptions again during validation.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with internal consistency tests across regions and applications, then comparing implied volumes against independent signals such as site counts, typical utilization ranges, and observed pricing bands. When an outlier appears, we re-open the related assumptions, re-check the supporting desk evidence, and, if needed, revisit primary contacts to confirm whether the deviation is temporary.

Before sign-off, a second analyst review is completed to ensure formula logic, unit conversions, and year alignment are consistent across the model. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory actions, reimbursement shifts, or notable technology launches. Right before delivery, a final pass is done so the latest public updates and any newly received expert inputs are reflected.

Mordor Intelligence's Neurofeedback Systems Market Size Versus Other Published Estimates

Published market sizes for neurofeedback systems can vary even when the topic appears identical, because authors do not always count the same revenue streams, time frames, or buyer settings. Differences also come from how prices are treated over time and whether adoption is tied to real site deployment signals or to broader mental health spending.

Some published figures fold in adjacent neurofeedback related services and wider neurotechnology solutions, then project forward using a single growth curve. In Mordor Intelligence, the total is limited to neurofeedback devices and associated software revenues that are directly linked to neurofeedback training use, with country-level scaling checked against provider presence and regional adoption patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.40 B (2025) | |

| Global Research Outlet A | USD 1.45 B (2025) | Often presents a broader basket that can blend devices with a wider set of software and service elements across neurofeedback related offerings, which can lift the counted revenue in the same year. |

| Industry Publisher B | USD 1.48 B (2024) | Uses a different base year and typically relies on category level growth rates, which can shift totals when currency timing, inflation, and price progression are not re-validated against observed system placement and licensing duration. |

The spread is mainly explained by scope and base-year alignment, and then by how pricing and adoption are carried through the forecast. By keeping the revenue definition tied to system and software sales that can be traced back to where neurofeedback is delivered, the estimate stays easier to reproduce and simpler to audit over time.

Key Questions Answered in the Report

How fast is the neurofeedback systems market expected to grow between 2026 and 2031?

The market is projected to expand at a 7.33% CAGR, climbing from USD 1.5 billion in 2026 to USD 2.14 billion by 2031.

Which application currently generates the highest revenue?

ADHD holds the leading position with 31.45% of 2025 revenue due to extensive clinical validation and early payer engagement.

What segment is likely to grow the quickest over the next five years?

Cognitive performance enhancement is forecast to post the fastest 8.01% CAGR as elite sports and defense sectors adopt neurofeedback for mental optimization.

Why are portable systems gaining traction so rapidly?

Wearable platforms deliver clinical-grade EEG quality in a compact form, enabling home-based protocols that align with rising telehealth preferences.

Which region offers the strongest expansion opportunity?

Asia-Pacific is projected to record an 8.07% CAGR through 2031 on the back of supportive digital-health policy and sizable unmet mental-health demand.

How are vendors addressing high upfront equipment costs?

Manufacturers are introducing subscription and equipment-as-a-service models that spread capital expenditure over time, making neurofeedback more accessible to smaller clinics.

Page last updated on: