Network Emulator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

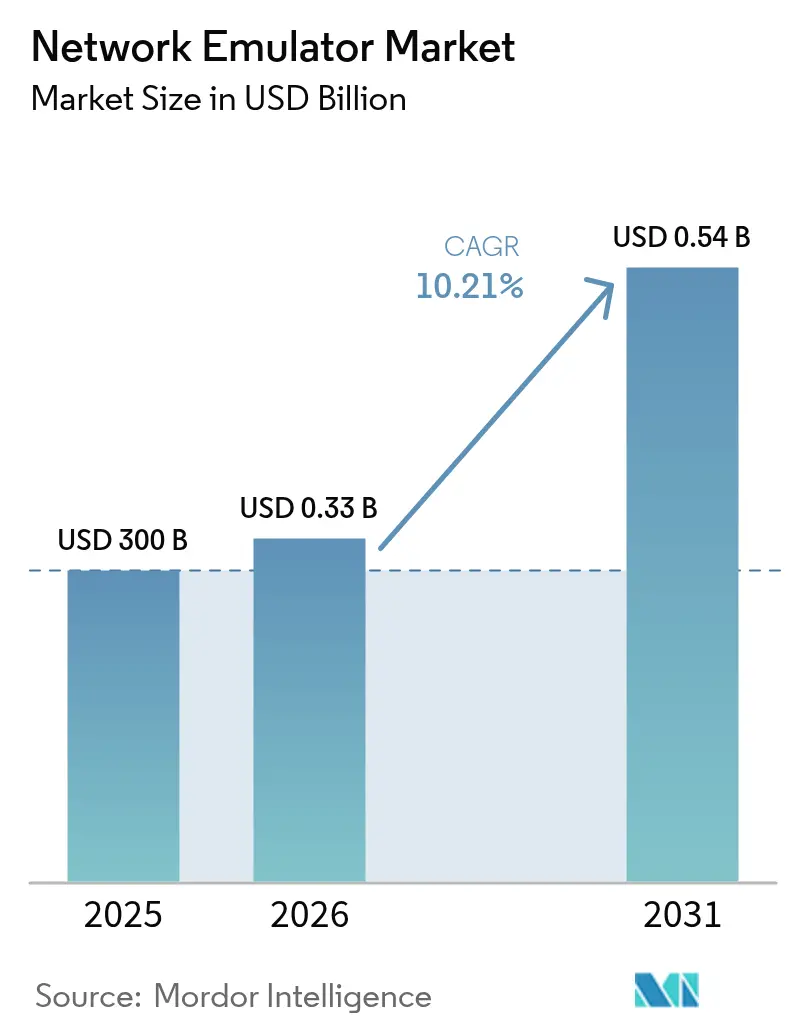

| Market Size (2026) | USD 0.33 Billion |

| Market Size (2031) | USD 0.54 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

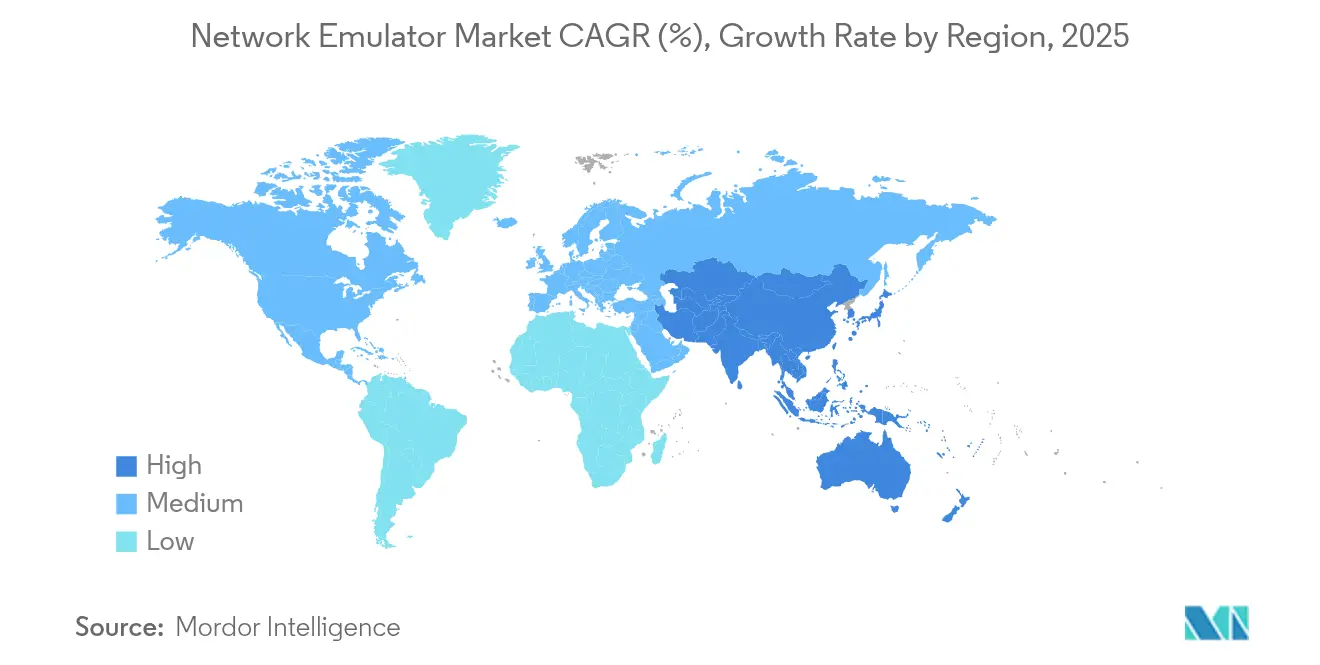

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

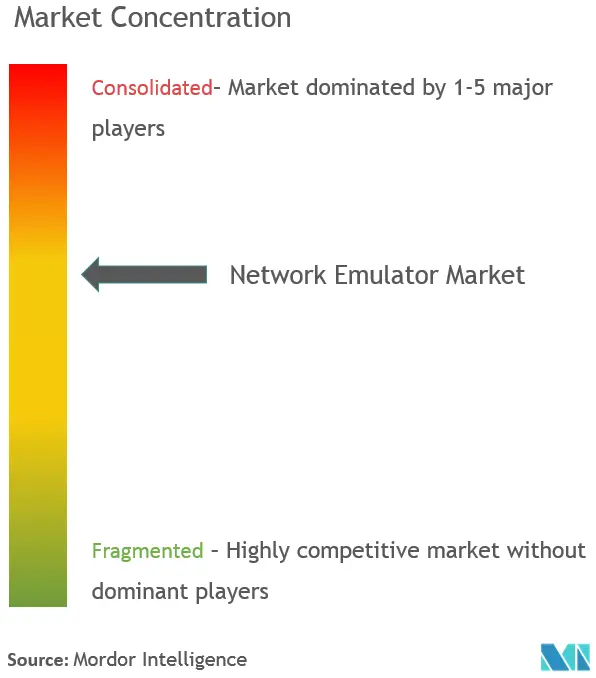

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Emulator Market Analysis by Mordor Intelligence

The network emulator market size was valued at USD 300 million in 2025 and estimated to grow from USD 330.63 million in 2026 to reach USD 538.1 million by 2031, at a CAGR of 10.21% during the forecast period (2026-2031). Momentum comes from 5G standalone upgrades, AI-centric data-center traffic, and regulatory scrutiny that requires nanosecond-level performance validation across critical infrastructure. Vendors are pivoting toward cloud-native, software-defined testing frameworks to keep pace with service-based 5G cores, LEO satellite backhaul, and automotive Ethernet traffic. Industry consolidation—typified by VIAVI Solutions’ USD 1.27 billion purchase of Spirent Communications—signals a strategic race to unify hardware, software, and assurance assets in one portfolio.[1]VIAVI Solutions, “VIAVI to Acquire Spirent for USD 1.27 Billion,” investors.viavisolutions.comKeysight Technologies’ parallel deal structure, which divested Spirent’s high-speed Ethernet and security lines to VIAVI for USD 410 million, underlines how leading players are reshaping competitive boundaries while satisfying antitrust regulators.

Key Report Takeaways

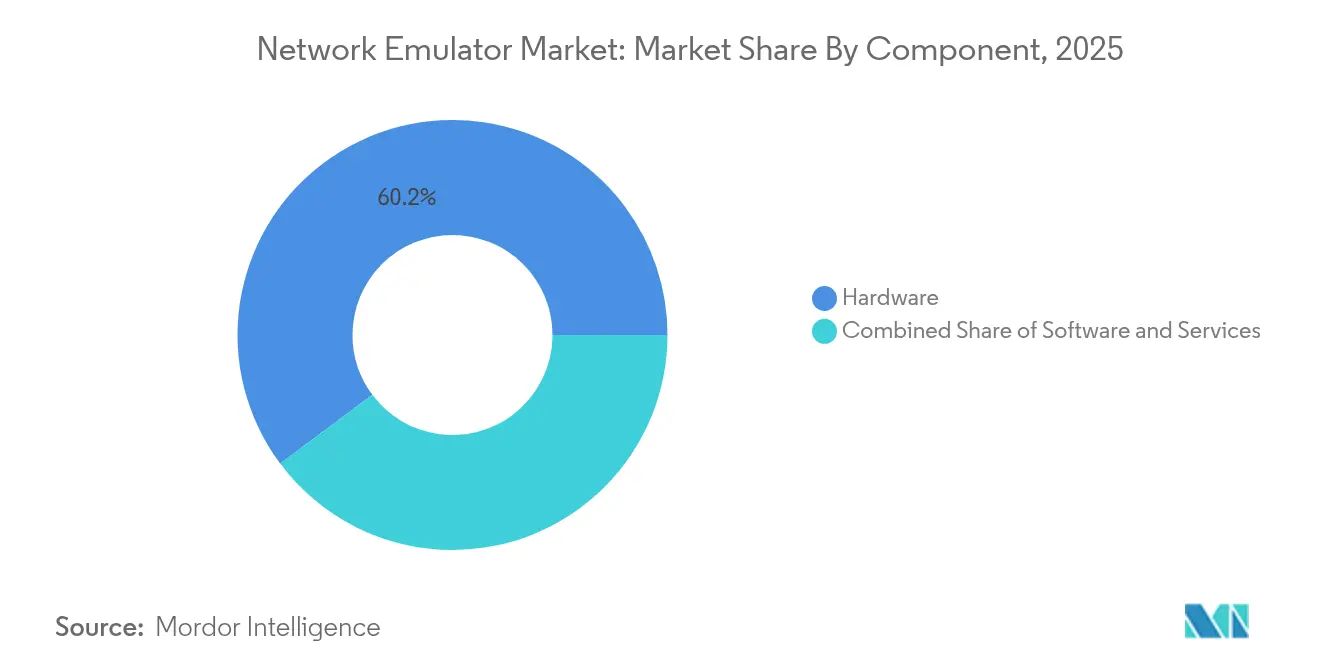

- By component, hardware commanded 60.20% of 2025 revenue, while the services segment is projected to grow the quickest at a 13.89% CAGR through 2031.

- By application, SD-WAN and SASE held 31.12% of 2025 revenue, whereas 5G RAN and Core testing is forecast to register the fastest 13.12% CAGR through 2031.

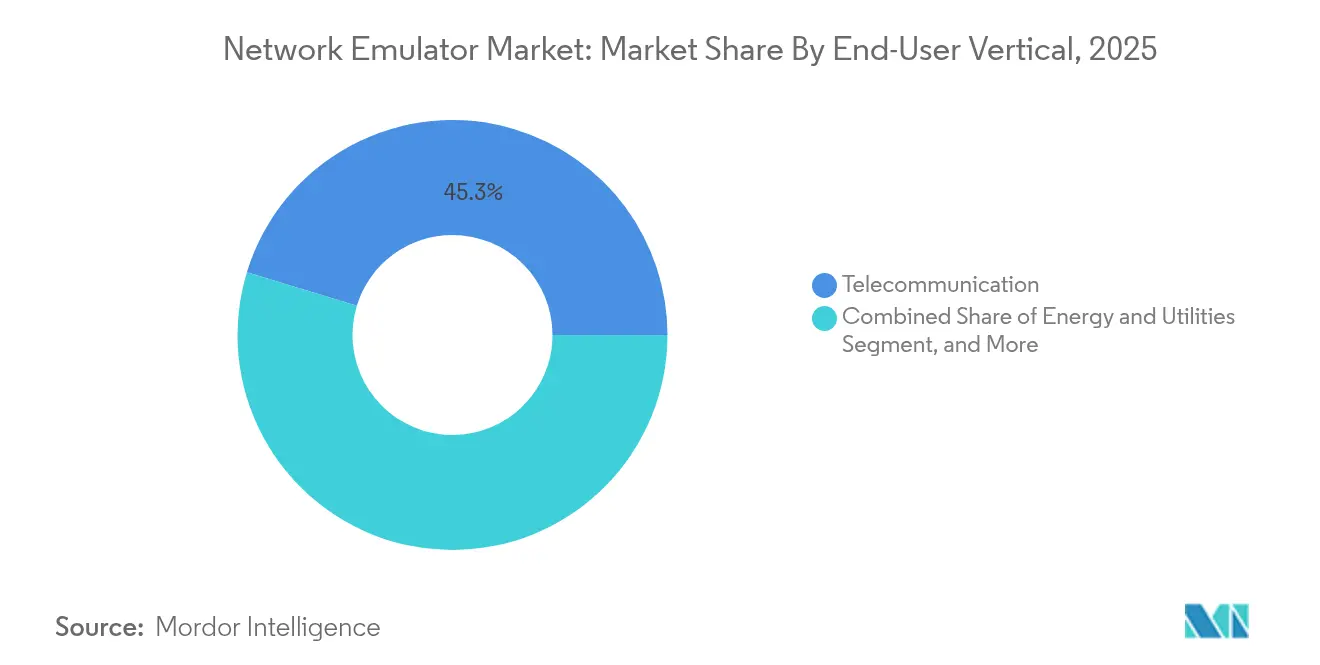

- By end-user vertical, telecommunications service providers accounted for 45.28% of 2025 revenue, but automotive and transportation is expected to expand at a 12.44% CAGR through 2031.

- By network type, 5G/LTE networks delivered both the largest 38.05% revenue share in 2025 and the quickest 13.4% CAGR outlook through 2031.

- By geography, North America led with a 37.35% revenue share in 2025, while Asia-Pacific is set to post the highest regional CAGR of 13.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Network Emulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G stand-alone core roll-outs accelerating real-time test demand | +2.1% | Global; North America, China, South Korea lead | Medium term (2–4 years) |

| Surge in SD-WAN and SASE enterprise deployments | +1.8% | North America and EU; APAC gaining | Short term (≤ 2 years) |

| Adoption of cloud-native network digital twins for DevSecOps | +1.4% | Global; hyperscale data-center operators | Medium term (2–4 years) |

| Growing regulatory focus on critical-infrastructure resiliency testing | +1.2% | North America and EU; emerging in APAC | Long term (≥ 4 years) |

| Proliferation of LEO‐satellite broadband driving multi-link emulation | +0.9% | Global, with early adoption in rural North America and emerging markets | Long term (≥ 4 years) |

| Automotive software-defined vehicle (SDV) validation requirements | +1.6% | Global, concentrated in automotive manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Stand-Alone Core Roll-outs Accelerating Real-Time Test Demand

Standalone 5G subscriptions reached 1.2 billion in 2024, with China and India adding the largest absolute numbers.[2]Ericsson Mobility Report Team, “November 2024 Mobility Report,” ericsson.com Operators must now validate service-based interfaces, network slicing, and microsecond synchronization without LTE anchors. NTT DoCoMo’s lab work with Keysight illustrates how tier-1 carriers rely on emulation to replicate beamforming and URLLC scenarios before field deployment. Precision requirements spill over into automotive V2X and industrial automation, elevating demand for network emulators that deliver deterministic timing.

Surge in SD-WAN and SASE Enterprise Deployments

Enterprises shifting from MPLS to software-defined fabrics need to prove dynamic path-selection logic and zero-trust policies at scale. VIAVI’s TeraVM emulates thousands of VPN clients to stress-test SASE links. Real-world evidence such as Sixt reducing latency 15% after adopting Cato Networks underscores why pre-deployment validation is now a board-level mandate. As vendors converge networking and security into single-vendor clouds, the network emulator market is widening toward multi-tenant SaaS test models.

Adoption of Cloud-Native Network Digital Twins for DevSecOps

Keysight’s Network Digital Twin ecosystem reproduces entire telco stacks, enabling CI/CD pipelines that continuously validate new VNFs against cyber-attack scenarios.[3]Keysight Technologies, “Network Digital Twin Overview,” keysight.com ISL Networks’ open 5G core server shows how smaller entrants leverage open-source to cut TCO for full-stack verification. The shift positions services teams as critical partners, explaining why the services segment leads CAGR growth.

Growing Regulatory Focus on Critical-Infrastructure Resiliency Testing

The FCC’s proposed BGP security rule would force broadband providers to simulate RPKI and ROA deployments at lab scale before production rollout. CISA’s FOCAL plan and Executive Order 14144 add governance mandates that translate into budget line-items for continuous emulation of attack chains. Compliance spending boosts premium testing demand, especially among energy, finance, and transportation operators classified as critical infrastructure.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of nanosecond-precision impairment hardware | –1.4% | Global; HFT hubs and 5G labs | Medium term (2–4 years) |

| Fragmented open-source tools diluting commercial ROI | –0.9% | Global; higher in academia and SMEs | Short term (≤ 2 years) |

| Budget freezes in 4G-focused CSPs of emerging economies | –0.7% | Africa, Latin America, Southeast Asia | Medium term (2–4 years) |

| Environmental regulations on electronic test-bed e-waste | –0.5% | EU; spreading to NA and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Nanosecond-Precision Impairment Hardware

High-frequency traders demand 5–85 ns precision across 130+ exchanges, yet only a handful of Grandmaster-clock silicon vendors can meet IEEE-1588 compliance at volume. MiFID II pushes banks to migrate from NTP to PTP, inflating hardware costs and lengthening lead times. Similar timing rigor now applies to URLLC and V2X, constraining rapid uptake in segments that rely on off-the-shelf appliances.

Fragmented Open-Source Tools Diluting Commercial ROI

Mininet’s penetration across 100+ universities shows how containerized labs reproduce hundreds of nodes at near-zero cost.[4]Mininet Project, “About Mininet,” mininet.org VT-Mininet and CORE add virtual-time and NFV hooks, reducing the perceived gap with proprietary test suites. While open tools often falter at carrier scale, their “good enough” fidelity diverts entry-level customers, forcing vendors to differentiate via integrated analytics and support SLAs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services-Led Acceleration Redefines Hardware Economics

Hardware retained 60.20% share of the network emulator market in 2025, thanks to purpose-built impairment appliances for 400/800 G Ethernet and millimeter-wave 5G. Yet services revenue is pacing a 13.89% CAGR, outstripping any other component. Keysight reported that software-and-services now account for 39% of total sales, posting 16% ARR growth in Q1 2025, according to Keysight. Vendors are bundling perpetual licenses with managed support to monetize continuous testing across DevSecOps pipelines rather than one-time equipment drops.

The shift stems from cloud-native disaggregation: customers prefer subscription test-as-a-service that scales elastically with lab demand. Rohde & Schwarz positions its analytics service to benchmark 5G beamforming and MIMO, relieving operators from in-house tooling. Meanwhile, modular chassis like Anritsu’s MT8000A extend lifespan through firmware keys, protecting capex while steering users toward recurring support. This service surge is a structural pivot, ensuring that the network emulator industry maintains profitability even as hardware ASPs flatten.

By Application: 5G RAN and Core Testing Surges Ahead of SD-WAN Maturity

SD-WAN and SASE retained 31.12% revenue leadership in 2025, buoyed by MPLS offload projects. However, 5G RAN and Core verification is the fastest-rising application at a 13.12% CAGR, reflecting worldwide standalone roll-outs. The network emulator market size for 5G test systems is projected to expand steadily as network slicing, URLLC, and non-terrestrial networking add layers of protocol complexity.

Open-RAN interoperability checks need emulators that pair RF impairment shelves with cloud PaaS simulators. Joint solutions from Rohde & Schwarz and VIAVI deliver O-RU conformance kits, giving manufacturers a turnkey route to NTIA funding eligibility. In parallel, Spirent’s A1 400G platform targets AI data-center fabrics, previewing demand beyond telecom toward high-density Ethernet. As SD-WAN penetrates even late-adopter SMBs, its growth moderates, but the installed base continues to purchase maintenance-heavy licenses, sustaining revenue.

By End-User Vertical: Automotive Outpaces Traditional Telecom Spend

Telecom operators still anchor 45.28% of 2025 revenue, yet automotive is sprinting at a 12.44% CAGR. Software-defined vehicle programs require fault-injection tests for automotive Ethernet, CAN-FD, and TSN, boosting orders for Keysight’s Novus mini launched in 2025. Defense-aerospace remains resilient as militaries validate satellite-cellular interoperability for battlefield comms, while banking underscores the latency race discussed earlier.

Automotive OEMs shift from prototype benches to over-the-air update validation in hardware-in-loop labs. UNH IOL’s independent TSN certification brings third-party assurance to suppliers. This demand profile nudges traditional telecom-centric vendors into adjacent mobility and industrial segments, diversifying revenue while cementing higher gross margins relative to commoditized carrier spending.

By Network Type: 5G/LTE Dual Leadership Shows No Sign of Plateau

5G/LTE commands 38.05% of 2025 sales and concurrently registers the highest CAGR at 13.4%. That dual leadership underscores a still-early upgrade cycle: transition from NSA to SA demands wholesale re-testing of core and RAN slices. Network emulator market share gains for 5G products will persist while Open-RAN, NTN, and 6G research extend the roadmap.

Wi-Fi 6/7 test demand rises as enterprises push extended-reality use cases that strain deterministic latency. Ethernet/IP continues its central role as AI lifts demand for 400 G and 800 G leaf-spine fabrics. Meanwhile, satellite operators running LEO constellations need multi-link emulation to model Doppler shift and differential delay before commercial activation, fueling an emerging niche that commands premium contract values.

Geography Analysis

North America generated 37.35% of 2025 revenue, propelled by 5G mid-band deployments, Wall Street latency mandates, and cybersecurity statutes such as Executive Order 14144 that compel continuous resilience testing. The same region hosts head offices for VIAVI, Keysight, and Spirent’s Ethernet unit, concentrating R&D and reinforcing home-market advantage. AI-centric data-centers in Silicon Valley and Northern Virginia are early adopters of 800 G traffic emulation, catalyzing local sales pipelines.

Asia-Pacific is the fastest-growing region with a 13.05% CAGR. China and India deploy standalone 5G at a massive scale, pushing local OEMs to procure advanced emulation gear. Median 5G download speeds already reach 524 Mbps in Kuala Lumpur, underscoring aggressive spectrum utilization. Japan fosters open-source-driven test labs such as ISL Networks’ 5GC server, enabling lower TCO for domestic carriers upgrading rural coverage. Automotive supply chains in Japan and South Korea amplify demand for TSN and Ethernet validation.

Europe shows mature yet steady expansion. The WEEE Directive 2012/19/EU obliges vendors to design recyclable test equipment, increasing BOM scrutiny and nudging a shift toward modular, software-defined chassis. Germany’s automotive cluster invests in in-vehicle network testing, while the EU’s focus on open, secure supply chains makes Open-RAN conformance a strategic priority supported by NTIA’s allied funding window. In smaller Middle East and African markets, budget limits steer operators toward open-source plus light commercial tooling, but the long-term 4G-to-5G upgrade path will slowly lift ASPs.

Competitive Landscape

Industry consolidation is reshaping vendor hierarchies. VIAVI’s USD 1.27 billion Spirent acquisition combines radio, core, and assurance assets under one roof, expanding cross-sell potential into satellite, aerospace, and security segments for investors. Keysight’s carve-out of Spirent’s Ethernet line for USD 410 million adds high-density port emulation to its IXIA stable while sidestepping concentration concerns.

Patent velocity indicates where next-gen competition will emerge. Meta’s filing on low-latency path failover algorithms for extended reality highlights big-tech influence on enterprise test needs. Qualcomm’s XR streaming patents require multi-link emulation across cellular and Wi-Fi, creating fresh SKU opportunities. Rohde & Schwarz posted EUR 2.93 billion FY 2024 revenue, citing 23% order growth on security-centric test systems. Keysight’s Communications Solutions Group delivered USD 1.30 billion in Q1 2025 with 5% YoY rise, backed by auto-Ethernet test orders.

Open-source remains a disruptive undercurrent but rarely displaces tier-1 buying centers that mandate turnkey support. Vendors counter price erosion by embedding analytics, AI-driven root-cause engines, and cloud-hosted lab orchestration. Early movers in quantum-safe cryptography testing, such as VIAVI’s Inertial Labs pick-up, are designing differentiation ahead of regulatory demand curves. As a result, competitive intensity is migrating from bit-rate races to solution breadth and compliance coverage.

Network Emulator Industry Leaders

Spirent Communications plc

Apposite Technology, Inc.

iTrinegy

Polaris Networks

Keysight Technologies Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Keysight confirmed the cash acquisition of Spirent, coupled with a USD 410 million divestment of Spirent’s Ethernet and security units to VIAVI; the deal closes in H1 FY 2025

- March 2025: VIAVI agreed to buy Spirent for USD 1.27 billion, eyeing USD 75 million cost synergies within two years

- February 2025: VIAVI acquired Inertial Labs for USD 150 million plus earn-outs, boosting aerospace and defense test revenue by USD 50 million

- February 2025: Spirent unveiled the A1 400G AI-traffic emulator, the first high-density system tuned for AI workloads

Global Network Emulator Market Report Scope

Network emulation appliances are an integral part of proving a solution before deploying because it is used to test the performance of a real network. These devices can also be used for quality assurance, proof of concept, or troubleshooting. Available as hardware or software solutions, a network emulator allows network architects, engineers, and developers to accurately gauge an application's responsiveness, throughput, and quality of end-user experience before applying making changes or additions to a system. In the report scope, the existing technology provider landscape also covered, which consists of major players operating in the market. The study also focuses on the impact of COVID-19 on the market ecosystem.

| Hardware |

| Software |

| Services |

| SD-WAN and SASE |

| Cloud and Data-Centre |

| IoT and Industrial |

| 5G RAN and Core |

| Satellite and Aerospace |

| Telecommunication Service Providers |

| Defense and Aerospace |

| Banking and Financial Services |

| Technology and Cloud Providers |

| Automotive and Transportation |

| Energy and Utilities |

| Other Enterprises |

| 5G / LTE |

| Wi-Fi 6/7 |

| Ethernet/IP |

| LEO / GEO Satellite |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| UAE | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa | |

| South Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | SD-WAN and SASE | |

| Cloud and Data-Centre | ||

| IoT and Industrial | ||

| 5G RAN and Core | ||

| Satellite and Aerospace | ||

| By End-user Vertical | Telecommunication Service Providers | |

| Defense and Aerospace | ||

| Banking and Financial Services | ||

| Technology and Cloud Providers | ||

| Automotive and Transportation | ||

| Energy and Utilities | ||

| Other Enterprises | ||

| By Network Type | 5G / LTE | |

| Wi-Fi 6/7 | ||

| Ethernet/IP | ||

| LEO / GEO Satellite | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| South Africa | ||

Key Questions Answered in the Report

What is driving the rapid growth of the network emulator market?

5G standalone migrations, SD-WAN & SASE roll-outs, and tighter cybersecurity mandates jointly propel a 10.21% CAGR through 2031.

Which component segment is expanding fastest?

Services, growing at a 13.89% CAGR, outpace hardware as customers shift toward subscription-based, cloud-hosted test environments.

How big is the opportunity in 5G RAN & Core testing?

5G RAN & Core is the fastest-growing application, advancing at 13.12% annually as operators validate slicing, URLLC, and non-terrestrial extensions.

Why is Asia-Pacific the hottest regional market?

Massive standalone 5G builds in China, India, and Japan plus government-backed tech programs yield a 13.05% regional CAGR.

How are mergers reshaping competitive dynamics?

VIAVI’s and Keysight’s Spirent transactions blend core, Ethernet, and security assets, creating larger portfolios that bundle hardware, software, and assurance.

What level of market concentration exists?

The market earns a score of 6 on a 1–10 scale, meaning the top five control≈60% share, leaving meaningful room for niche and regional challengers.

Page last updated on: