Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

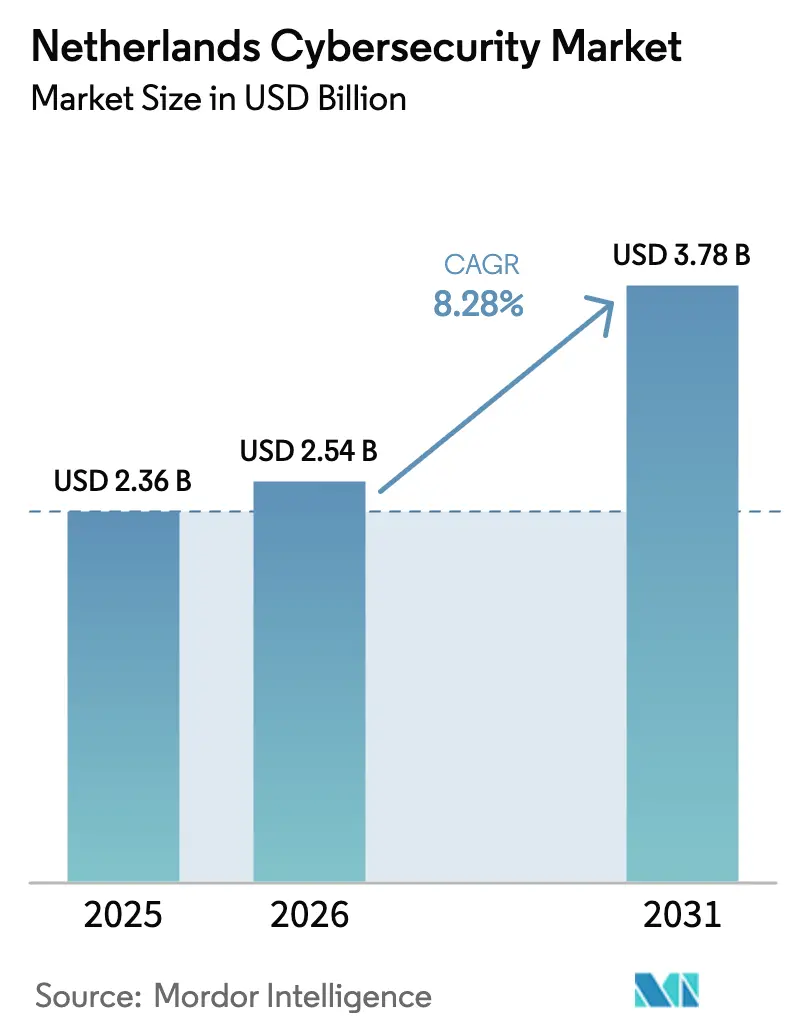

| Base Year Market Size (2025) | USD 2.36 Billion |

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

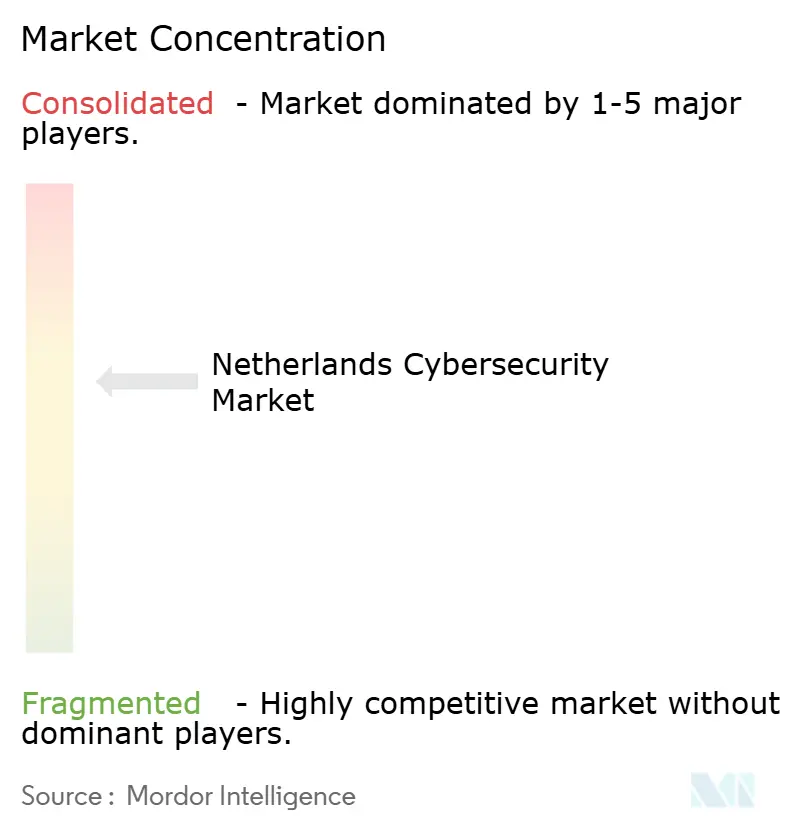

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Cybersecurity Market Analysis by Mordor Intelligence

The Netherlands cybersecurity market size is projected to expand from USD 2.36 billion in 2025 and USD 2.54 billion in 2026 to USD 3.78 billion by 2031, registering a CAGR of 8.28% between 2026 to 2031. Heightened enforcement of the NIS2 Directive, sovereign-cloud mandates, and the rapid migration of critical workloads to public-cloud platforms are accelerating security spending across both public and private sectors. Government funding of EUR 568 million (USD 640 million) through 2028 underlines the strategic focus on critical-infrastructure resilience and baseline security for public bodies. Enterprises are shifting toward managed detection and response as the scarcity of certified professionals makes in-house security operations centers harder to sustain. Cloud deployments already dominate, reflecting Digital Operational Resilience Act requirements that formalize third-party risk management for banks and insurers. Vendor competition is intensifying as global providers localize data residency and Dutch scale-ups win mid-market contracts with incident-response retainers.

Key Report Takeaways

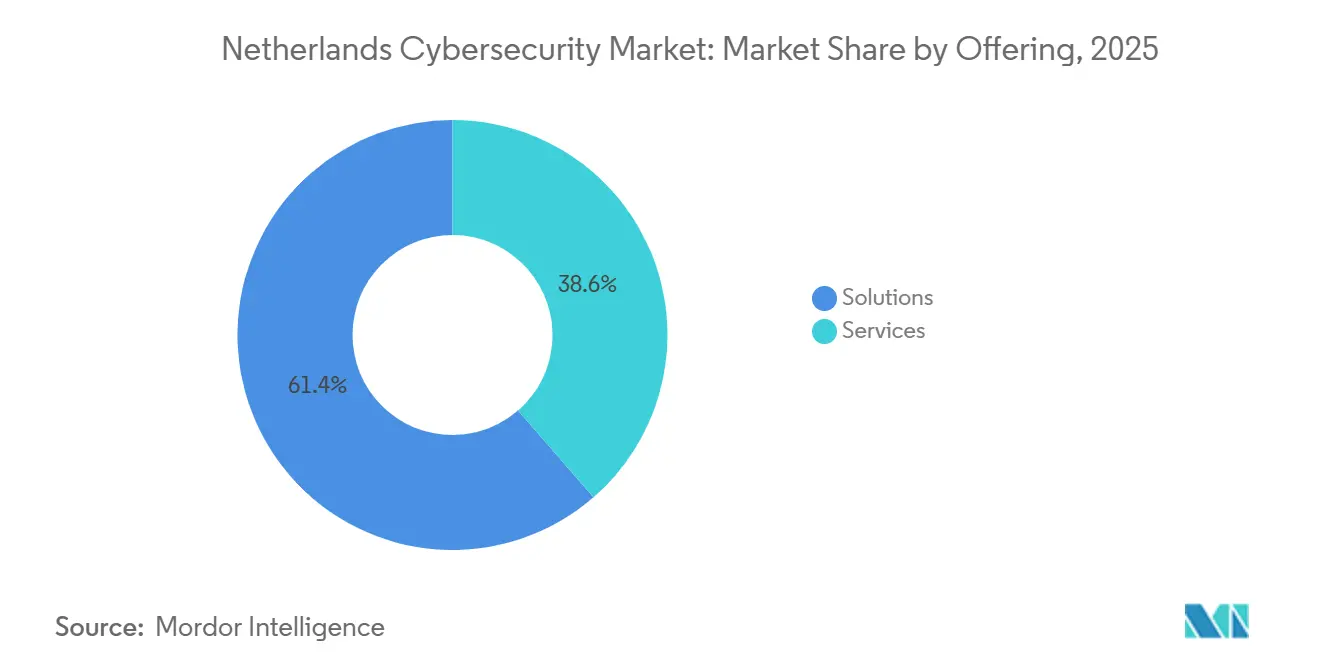

- By offering, solutions led with 61.38% of Netherlands cybersecurity market share in 2025, while services are projected to grow at an 9.23% CAGR through 2031.

- By deployment mode, cloud commanded 62.73% share of the Netherlands cybersecurity market size in 2025 and is expected to expand at a 10.04% CAGR to 2031.

- By organisation size, large enterprises held 72.65% of Netherlands cybersecurity market share in 2025; SMEs record the fastest 8.6% CAGR to 2031.

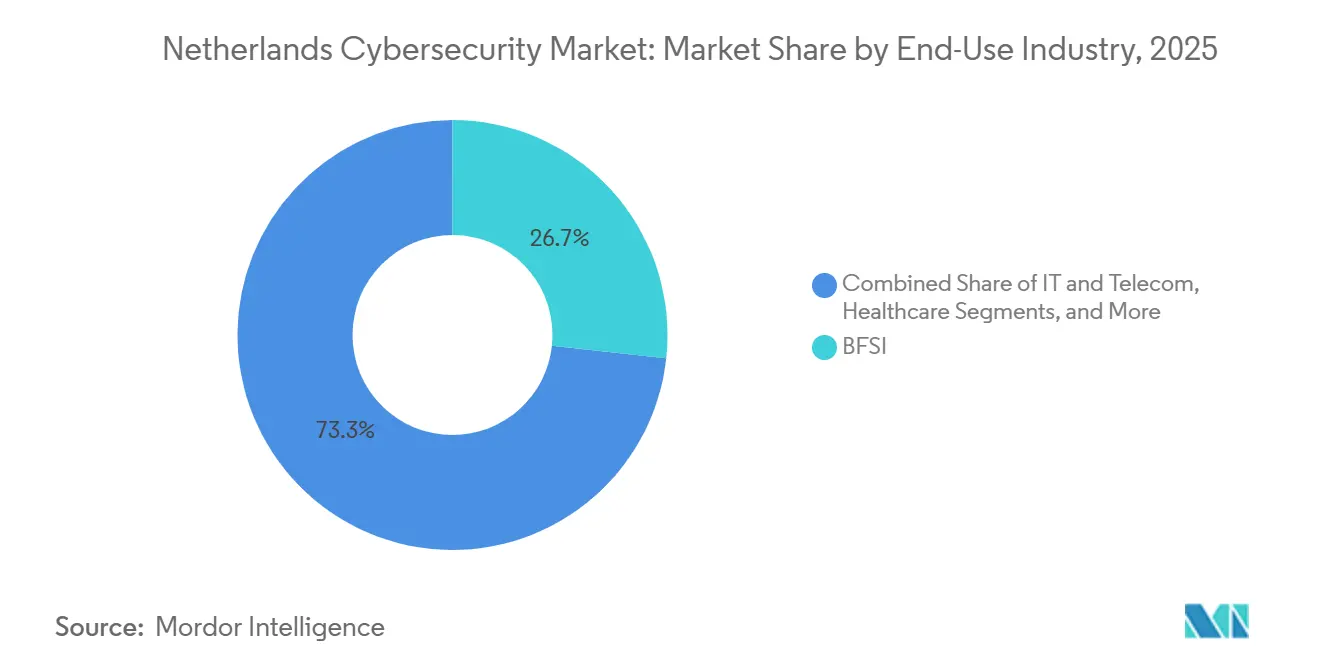

- By end-user vertical, BFSI led with 26.73% revenue share in 2025; healthcare is advancing at a 10.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cyber Attacks on Critical Infrastructure | +2.3% | National, led by Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Accelerated Government Digital Services | +1.9% | National, early gains in Bogotá, Barranquilla, Cartagena | Medium term (2-4 years) |

| Enforcement of Data-Protection Regulation | +1.6% | National | Medium term (2-4 years) |

| Surge in Cloud Adoption among SMEs | +1.8% | National, higher urban penetration | Medium term (2-4 years) |

| Fintech Sandbox Expansion Driving API Security | +1.4% | Bogotá fintech corridor | Short term (≤ 2 years) |

| Nearshore Outsourcing Boosting Compliance Demand | +1.5% | Bogotá, Medellín, Barranquilla | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Compliance With NIS2 Directive

The October 2024 transposition of NIS2 expanded the number of essential and important entities from roughly 200 to over 1,800, forcing mid-market utilities, logistics firms, and digital-infrastructure providers to establish 24-hour incident-reporting workflows and board-level governance.[1]European Commission, “Digital Operational Resilience Act,” EC.EUROPA.EU The Dutch National Cyber Security Centre released sector-specific guidance in early 2025 that requires root-cause analyses within 72 hours, accelerating adoption of automated security information and event-management platforms. Non-compliance fines of up to EUR 10 million (USD 11.3 million) or 2% of global turnover have elevated cybersecurity to a budget priority even in cost-sensitive sectors. Unified risk-management dashboards that combine vulnerability scanning, asset inventory, and regulatory reporting are in high demand. Software suppliers are meeting new supply-chain clauses by embedding secure-by-design requirements and software bills of materials, thereby raising the broader security baseline across the Netherlands cybersecurity market.

Rising Cloud Migration of Critical Workloads

Dutch banks migrated an estimated 40% of core systems to public clouds between 2024 and 2025 to satisfy Digital Operational Resilience Act testing mandates. The Dutch Court of Audit flagged over-reliance on a narrow set of U.S. providers, prompting ministries to evaluate multi-cloud and sovereign architectures. Hospitals, reacting to the Maastricht University Medical Center ransomware event, now use immutable cloud snapshots for backup, driving uptake of cloud security posture management and data-loss-prevention tools. Energy operators such as TenneT are moving grid-analytics workloads into cloud platforms, but this IT-OT convergence is enlarging the attack surface and requires micro-segmentation controls. Hyperscalers have responded by opening Dutch sovereign regions, which further accelerates cloud adoption inside the Netherlands cybersecurity market.

Rapid Uptake of Zero Trust Architecture

The central government mandated zero-trust principles for all new IT projects in 2025, establishing continuous verification of user identity, device posture, and application permissions. Corporate procurement references the NIST and European Union Agency for Cybersecurity frameworks, pushing large enterprises to replace broad virtual private network access with software-defined perimeters and privileged-access tools. The Port of Rotterdam segmented its terminal networks into micro-zones during 2024, foiling a state-sponsored reconnaissance attempt and showcasing zero-trust benefits in operational-technology settings. KPN’s CISO Circle of Trust shares implementation roadmaps that reveal difficulty modernizing legacy applications without modern authentication. Cyber-insurance carriers now insist on multi-factor authentication and endpoint detection, making zero-trust controls a prerequisite for coverage and deepening adoption across the Netherlands cybersecurity market.

Accelerating Digitalization Across Dutch SMEs

The Digital Gateway initiative delivered subsidized assessments to 3,000 SMEs in 2025, exposing gaps in incident response and multi-factor authentication for 62% and 48% of firms respectively. Regional hubs in Noord-Brabant and Zuid-Holland operate collective-defense models that pool security-operations resources and threat feeds, lowering per-firm costs. The Dutch Banking Association extended real-time fraud-alert services to SME members, after EUR 120 million (USD 135 million) in cyber-related losses during 2024. E-commerce platforms require stronger payment-card security from third-party sellers, indirectly boosting SME maturity. Managed detection and response subscriptions tailored to companies with under 250 staff are therefore expanding faster than product licenses, supporting long-term growth in the Netherlands cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Sensitivity among SMEs | -1.2% | Secondary cities nationwide | Medium term (2-4 years) |

| Acute Cybersecurity Talent Shortage | -1.5% | Bogotá and Medellín | Long term (≥ 4 years) |

| Limited Cyber Insurance Penetration | -0.7% | National | Medium term (2-4 years) |

| Fragmented Rural Connectivity | -0.6% | Remote and rural locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Cybersecurity Talent in Netherlands

Unfilled security roles rose 8% during 2025 even as the workforce expanded, pointing to demand that outstrips supply.[2]ISC2 Research Team, “Cybersecurity Workforce Study 2025,” ISC2.ORG The national strategy earmarks EUR 50 million (USD 56 million) for fast-track certification and apprenticeships, yet graduates will not enter the labor pool quickly enough. Global vendors opening Dutch security centers offer salary packages local firms cannot match, driving SMEs toward managed services while delaying in-house adoption of threat-hunting and purple-team practices. Dependence on external providers poses knowledge-transfer challenges in operational-technology settings that need domain expertise. The talent deficit therefore slows zero-trust rollouts and elevates costs within the Netherlands cybersecurity market.

Fragmented IT Environments in Legacy Sectors

Industrial plants and port facilities operate decades-old supervisory control systems alongside modern analytics, producing visibility gaps that hinder patch management. Many terminal operators lacked full device inventories in 2024, leaving blind spots that adversaries exploit for persistence. Retrofitting encryption or authentication on proprietary protocols is often infeasible, so operators rely on passive monitoring and network segmentation that add complexity and cost. Similar challenges confront chemical processors that cannot patch control systems without costly downtime. Such heterogeneity impedes adoption of unified security platforms and keeps specialized OT-security appliances in demand, partially offsetting growth in other segments of the Netherlands cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions on Outsourcing Wave

Solutions commanded 61.38% of Netherlands cybersecurity market share in 2025, but services are forecast to grow at a 9.23% CAGR through 2031 as organizations outsource threat detection and compliance reporting. Professional assessments, penetration testing, and architecture consulting are increasingly bundled with managed detection and response subscriptions, allowing providers to lock in multi-year contracts and expand wallet share. The talent shortage has made external 24/7 monitoring more economical than building internal security operations centers, especially for entities newly covered by NIS2. Cloud-security, identity-and-access, and integrated-risk-management offerings drive product demand, yet they are often consumed through service wrappers that guarantee outcomes rather than licenses. Application-security adoption is rebounding as software suppliers embed secure-by-design principles to meet supply-chain clauses in NIS2.

The Netherlands cybersecurity market size for managed services is expected to surpass USD 1.5 billion by 2031, reflecting a structural pivot from capital to operating expenditure models. Vendors such as Palo Alto Networks report faster EMEA revenue growth in cloud-native security than in hardware firewalls, indicating that consumption preferences mirror cloud adoption. KPN’s SecurX program trained 500 partners on compliance workflows in 2025, creating a nationwide channel system designed for SMEs. Identity and access management remains critical under zero-trust mandates, while network-security and endpoint-protection growth is decelerating as markets mature. The upshot is a service-centric trajectory that blurs lines between consulting, integration, and continuous operations across the Netherlands cybersecurity market.

By Deployment Mode: Cloud Dominates as Hyperscalers Localize

Cloud held 62.73% Netherlands cybersecurity market share in 2025 and is advancing at a 10.04% CAGR, driven by resilience-testing mandates under the Digital Operational Resilience Act. Microsoft’s Dutch sovereign regions, announced in 2024, addressed data-residency concerns and unlocked public-sector procurement avenues.[3]Microsoft, “Azure Netherlands Sovereign Regions,” MICROSOFT.COM Financial institutions now deem sovereign public clouds acceptable for core workloads provided that exit plans are documented, thereby boosting adoption of cloud-security-posture and workload-protection platforms. Healthcare operators embrace immutable snapshots to prevent ransomware encryption of backups, while energy utilities integrate OT telemetry into cloud analytics for predictive maintenance.

On-premises deployments remain relevant for defense and industrial sites that require physical segregation, yet even these environments replicate logs to cloud analytics for advanced correlation. Multi-cloud security platforms that enforce consistent policies across AWS, Azure, and Google Cloud are increasingly preferred by ministries following the Dutch Court of Audit’s warnings on single-provider lock-in. The Netherlands cybersecurity market size attributed to cloud delivery is projected to exceed USD 2.7 billion by 2031, implying that more than 70% of spend will involve cloud control planes. The remaining on-premises share will focus on specialized OT monitoring, ultra-low-latency environments, and classified workloads that cannot leave restricted facilities.

By End-Use Industry: Healthcare Surges Amid Digitalization

Banking, financial services and insurance accounted for 26.73% of spending in 2025, reflecting stringent supervision by De Nederlandsche Bank and early adoption of cloud controls for payment security. Yet healthcare is the fastest-growing vertical, with a 10.16% CAGR expected through 2031, following the Maastricht University Medical Center ransomware shock that highlighted vulnerabilities in device segmentation. Hospitals deploy zero-trust micro-segmentation and immutable backup vaults, while telemedicine and electronic health-record expansion widen the attack surface. Energy and utilities operators also accelerate investments in OT visibility and anomaly detection as they integrate renewable assets and smart-grid analytics.

Retail and e-commerce platforms enforce stronger payment-data controls on third-party merchants, indirectly lifting security maturity among small sellers. Industrial manufacturing companies adopt OT security to protect connected production lines; ASML implemented global micro-segmentation across factories in 2024 to mitigate supply-chain espionage. IT and telecom firms roll out 5G network-slicing isolation features that require continuous monitoring against edge-based threats. Collectively, the diversification of demand underpins long-run resilience in the Netherlands cybersecurity market.

By End-User Enterprise Size: SMEs Accelerate as Compliance Expands

Large enterprises captured 68.23% of revenue in 2025, but SMEs are projected to post a 10.84% CAGR, lifting their share of the Netherlands cybersecurity market size beyond 35% by 2031. NIS2 brought many mid-market logistics, utility, and tech firms into the regulatory perimeter, compelling them to adopt incident-response and asset-management tooling. The Digital Gateway initiative subsidizes assessments and awareness training, lowering entry barriers for firms with under 250 staff. Managed service providers certified under KPN’s SecurX scheme deliver standardized playbooks that map directly to directive controls, helping SMEs avoid costly internal hiring.

Micro-enterprises remain under-protected as budget constraints lead to reactive rather than proactive investments. However, collective-defense models in Noord-Brabant and Zuid-Holland pool resources so that clusters of SMEs can share threat feeds and security-operations capacity. Banks’ extension of fraud-alert platforms to SME clients also mitigates exposure to business-email compromise scams. As insurance underwriters insist on endpoint detection and multi-factor authentication, even the smallest entities must procure baseline controls, reinforcing demand across the Netherlands cybersecurity market.

Geography Analysis

The Randstad metropolitan area anchors the Netherlands cybersecurity market, concentrating banks, government ministries, and tech hubs that collectively generate the bulk of enterprise demand. Amsterdam hosts dense data-center clusters and hyperscale regions, prompting investments in physical access, network segmentation, and compliance certifications aimed at financial clients. Rotterdam’s 2024 launch of a Cyber Resilience Centre illustrates regional leadership in OT security, coordinating threat intelligence among terminals that manage 30% of European container throughput. The Hague, home to the Dutch Data Protection Authority, handed down EUR 45 million (USD 51 million) in GDPR fines during 2024, reinforcing accountability in data-handling practices.

Regional innovation ecosystems are distributing capability beyond the Randstad. Eindhoven’s high-tech campus cultivates startups in quantum-safe cryptography and AI-driven threat detection, while Delft University of Technology advances OT-security research. Noord-Brabant and Zuid-Holland hubs pilot collective-defense models that lower SME costs and boost coverage. Government subsidies and the Digital Gateway initiative extend risk assessments into rural provinces, narrowing the urban-rural gap in baseline security.

Cross-border cooperation remains robust; the Netherlands participates in EU-wide cyber exercises and NATO drills that stress-test critical infrastructure resilience. Sovereign-cloud priorities are steering ministries toward European vendors, opening opportunities for Dutch scale-ups like Northwave and Tesorion that offer local support and comply with strict residency rules. Geographic concentration of talent, capital, and critical infrastructure will persist, yet targeted initiatives are broadening participation in the Netherlands cybersecurity market.

Competitive Landscape

Global vendors including Cisco, Palo Alto Networks, Fortinet, and CrowdStrike vie with Dutch incumbents KPN Security, Northwave, Fox-IT, and Tesorion, producing a moderately fragmented Netherlands cybersecurity market. Platform strategies that bundle endpoint, network, cloud, and identity controls raise switching costs and give integrated providers an advantage. Cisco’s USD 28 billion acquisition of Splunk in March 2024 strengthened its observability and AI-analytics capabilities, enabling unified threat detection across IT and OT environments. Microsoft addressed data-sovereignty concerns by announcing Azure Netherlands sovereign regions in 2024, unlocking public-sector contracts. Dutch scale-ups differentiate through rapid incident-response retainers and domain expertise, as evidenced by Northwave’s placement in the Financial Times growth champions list.

Technology integration is the chief battleground. Palo Alto Networks’ Cortex XSIAM automates alert correlation, reducing mean time to respond for under-resourced SOCs. CrowdStrike’s Falcon platform focuses on behavior analytics that detect signature-less exploits.

Fortinet emphasizes OT-specific firewalls and anomaly detection for energy and manufacturing clients. KPN’s CISO Circle of Trust convenes sector CISOs to share indicators of compromise ahead of public disclosure, effectively creating a private threat feed that sidesteps commercial solutions. Consolidation is expected to intensify as vendors acquire niche capabilities in cloud-native application protection and quantum-safe encryption while insurers enforce technical prerequisites that set a de facto baseline across the Netherlands cybersecurity market.

Netherlands Cybersecurity Industry Leaders

Northwave Group B.V.

Tesorion B.V.

Fox-IT B.V.

KPN Security (Koninklijke KPN N.V.)

ON2IT B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The Dutch government mandated the BIO2 baseline security standard for all central-government entities, requiring multi-factor authentication, endpoint detection, and continuous vulnerability scanning by year-end.

- May 2025: The Dutch Parliament approved the creation of a national “Rijkscloud” to bolster sovereign data management.

- March 2025: Northwave Group was listed in the Financial Times Europe’s Long-Term Growth Champions 2025, underscoring rapid expansion of its incident-response and threat-intelligence services among mid-market enterprises.

- March 2025: Eye Security raised EUR 36 million (USD 42.36 million) in Series B funding led by J.P. Morgan Growth Equity Partners.

Netherlands Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Netherlands Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Netherlands cybersecurity market in 2026?

It is expected to reach USD 2.54 billion, continuing toward USD 3.78 billion by 2031 at an 8.28% CAGR.

Which segment grows fastest through 2031?

Cloud deployments expand at a 10.04% CAGR, driven by sovereign-cloud regions and resilience-testing mandates.

Why is healthcare security spending accelerating?

The Maastricht University Medical Center ransomware attack exposed critical gaps, pushing hospitals to adopt zero-trust micro-segmentation and immutable backups, resulting in a 10.16% CAGR.

What drives SME demand for managed security?

NIS2 compliance obligations and the Digital Gateway program subsidize assessments, so SMEs adopt managed detection and response instead of staffing internal SOCs.

How does NIS2 influence investment priorities?

Non-compliance fines of up to EUR 10 million (USD 11.88 million) or 2% of global turnover force entities to implement automated incident reporting and unified risk-management platforms quickly.

Which region within the Netherlands shows the highest cybersecurity spending?

The Randstad Amsterdam, Rotterdam, The Hague, and Utrecht concentrates spending due to the presence of financial institutions, ministries, and data-center hubs.

Page last updated on: