Netherlands Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

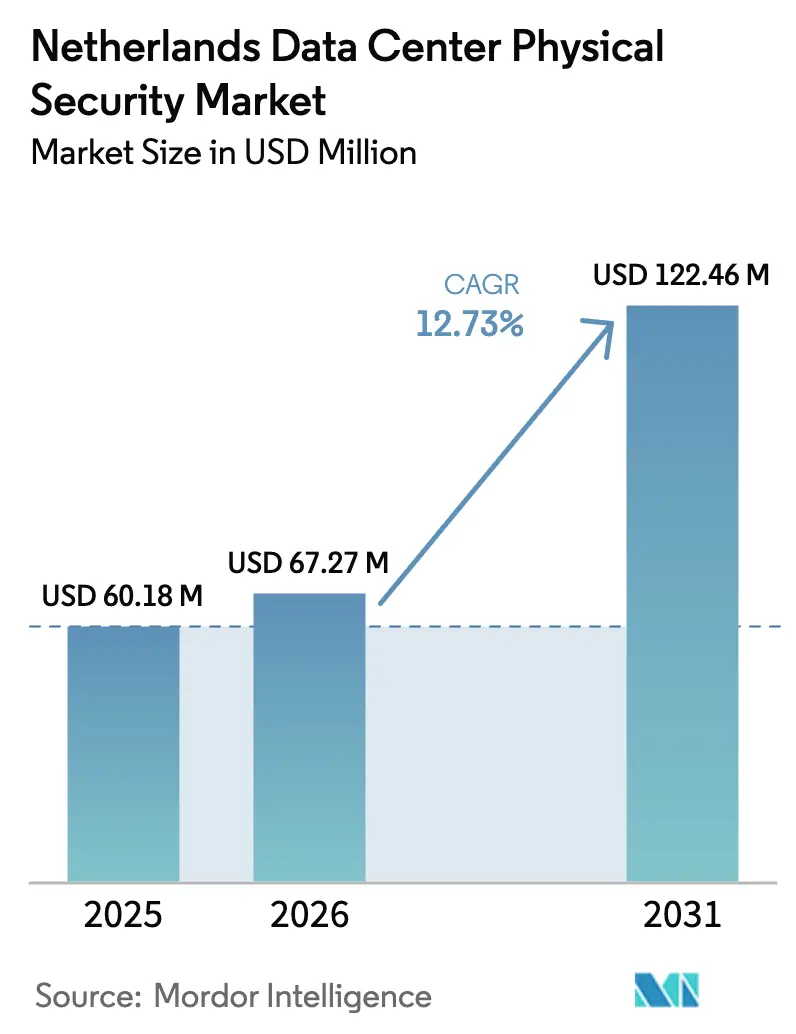

| Base Year Market Size (2025) | USD 60.18 Million |

| Market Size (2026) | USD 67.27 Million |

| Market Size (2031) | USD 122.46 Million |

| Growth Rate (2026 - 2031) | 12.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Data Center Physical Security Market Analysis by Mordor Intelligence

The Netherlands data center physical security market size is expected to increase from USD 60.18 million in 2025 to USD 67.27 million in 2026 and reach USD 122.46 million by 2031, growing at a CAGR of 12.73% over 2026-2031. Growth is powered by hyperscale buildouts, NIS2 enforcement, and the escalating complexity of blended cyber-physical attacks. Operators now specify AI video analytics, multi-factor biometrics, and fiber-optic intrusion sensing in base build packages, elevating physical security to a board-level capital priority. Energy taxation and system-integration complexity restrain near-term budgets, yet the nation’s hub status, dense subsea-cable routes, and predictable regulation keep the long-run outlook strong. Investments topping USD 3 billion since 2024 confirm sustained confidence in Dutch connectivity and rule-based governance.

Key Report Takeaways

- By data center type, colocation facilities held 58.43% of the Netherlands data center physical security market share in 2025, while hyperscalers are forecast to post a 13.85% CAGR through 2031.

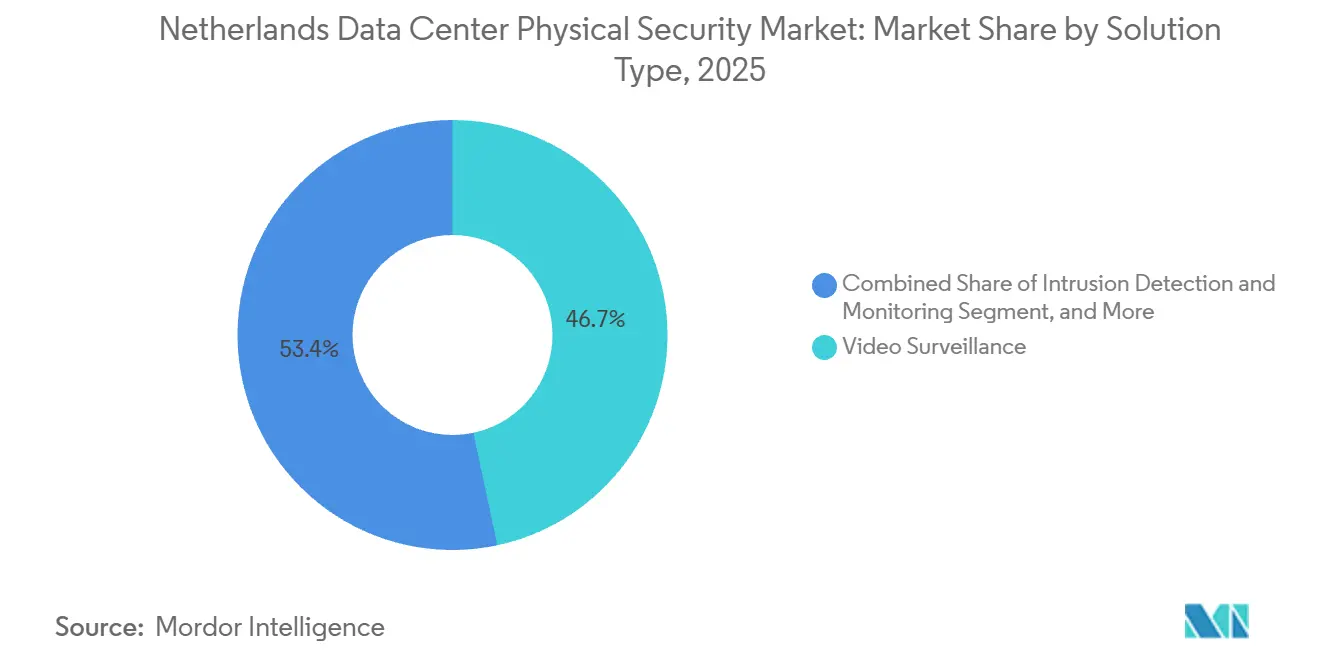

- By solution type, video surveillance led at 46.65% in 2025, yet intrusion detection and monitoring is set to rise at a 13.63% CAGR to 2031.

- By service type, consulting accounted for 39.34% of the Netherlands data center physical security market in 2025; integration and deployment services are projected to grow at a 13.45% CAGR during the forecast period.

- By tier, tier 3 facilities commanded 44.12% of 2025 spending, while tier 4 sites displayed the fastest 13.73% CAGR outlook.

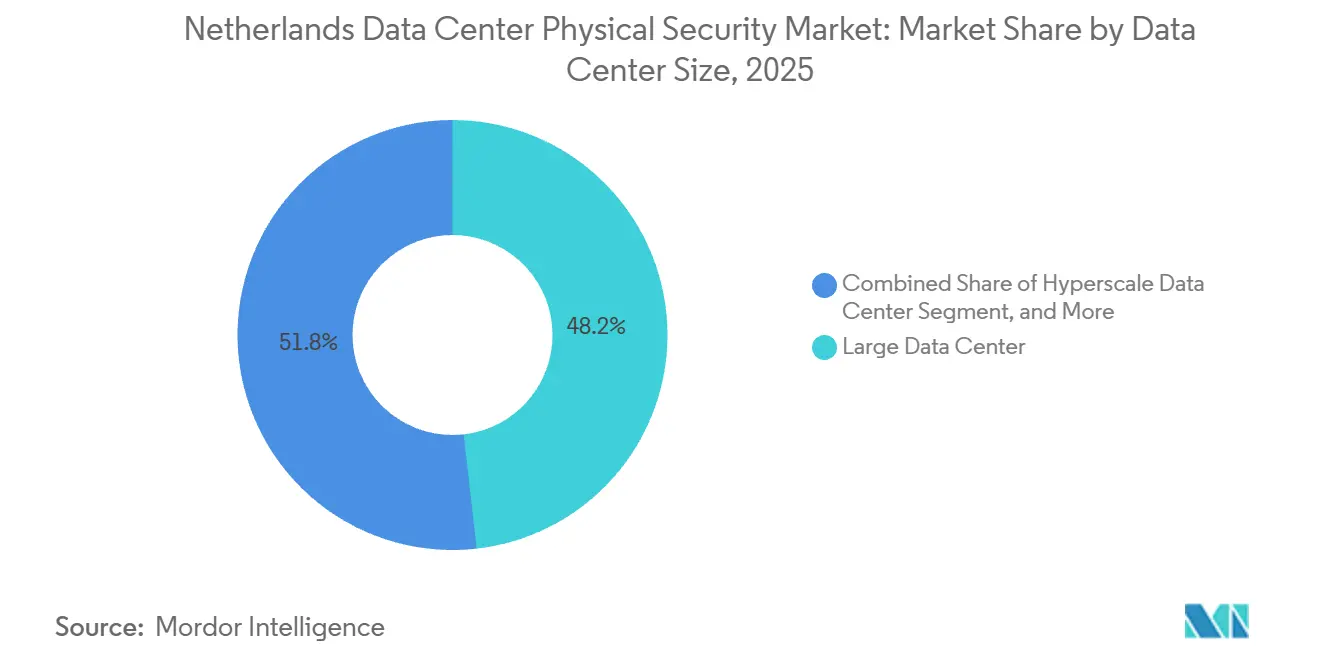

- By data center size, large facilities accounted for 48.21% of 2025 revenue, yet hyperscale campuses are expected to expand at a 13.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Each country contributes a share rather than an absolute position, and Netherlands is evaluated within that framework. The data center physical security market share in Mordor Intelligence's global report defines how those shares are distributed worldwide.

Netherlands Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Hyperscale and Colocation Data Center Investments | +3.2% | Netherlands national, concentrated in Amsterdam metropolitan area and Lelystad | Medium term (2-4 years) |

| Regulatory Mandates for GDPR and Critical Infrastructure Protection | +2.8% | Netherlands national, aligned with EU-wide NIS2 Directive enforcement | Short term (≤ 2 years) |

| Growing Sophistication of Cyber-Physical Threats | +2.1% | Global, with elevated risk in high-density data center corridors including Netherlands | Medium term (2-4 years) |

| Increasing Adoption of AI-Enabled Video Analytics for Perimeter Security | +1.9% | Netherlands national, early adoption in Tier 3 and Tier 4 facilities | Medium term (2-4 years) |

| Emergence of Micro Data Centers at Edge Locations Supporting 5G Networks | +1.4% | Netherlands national, urban centers and industrial zones | Long term (≥ 4 years) |

| Insurance Premium Discounts for Certified Physical Security Compliance | +1.3% | Netherlands national, influenced by European insurance market practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale and Colocation Investments

Capital pledges topping EUR 3 billion (USD 3.2 billion) during 2024-2026 are reshaping the Netherlands data center physical security market as greenfield builds integrate unified security ecosystems from day one.[1]Equinix, “Equinix announces €1.5 billion data center campus in Lelystad,” equinix.comEquinix’s EUR 1.5 billion (USD 1.6 billion) Lelystad campus and Pure DC’s EUR 1 billion (USD 1.07 billion) Westpoort project both embed fiber-optic DAS, AI cameras, and biometric portals, shrinking procurement cycles.[2]Pure DC, “Pure DC commences construction on €1 billion Amsterdam Westpoort campus,” puredc.comGoogle’s EUR 600 million (USD 640 million) Groningen build further anchors hyperscale optimism. Cluster effects around Amsterdam permit shared labor pools and streamline logistics, lowering per-sensor cost even as absolute spend climbs. Five-to-seven-year vendor frameworks lock in recurring demand for surveillance, access, and perimeter solutions.

Regulatory Mandates for GDPR and Critical-Infrastructure Protection

NIS2 classifies data centers as essential entities, setting 24-hour early-warning and 72-hour incident-report deadlines backed by fines up to EUR 10 million or 2% of global revenue.[3]European Union Agency for Cybersecurity, “NIS2 Directive,” enisa.europa.eu Despite transposition delays into 2025, Dutch operators pre-invested in centralized SOCs that stream badge logs, camera feeds, and power telemetry in real time. ISO 27001 and IEC 62443 certifications now function as de-facto proof of diligence, lowering liability and unlocking insurance incentives. Regulation therefore converts directly into incremental spending within the Netherlands data center physical security market.

Growing Sophistication of Cyber-Physical Threats

Attackers increasingly exploit cameras, door controllers, and legacy BMS gateways to pivot into IT networks, making physical safeguards central to cyber posture. Tier 4 builds use radar, thermal imaging, and AI vision to detect fence climbs, tunneling, or drone flyovers in seconds. Edge inference lowers latency and bandwidth, while zero-trust policies require biometrics for every entry, shrinking insider-risk windows. Because blended threats jeopardize uptime SLAs, spending on next-generation perimeter tools rises across colocation and hyperscale sites alike.

Increasing Adoption of AI-Enabled Video Analytics for Perimeter Security

Machine-learning engines turn cameras into proactive sentries that flag atypical behavior, restricted-zone breaches, or tailgating in real time. Edge chips perform inference locally, maintaining detections during network drops and meeting NIS2’s rapid-notification mandate. Unified VMS platforms overlay threat trajectories on facility maps and automate guard dispatch. Insurers are beginning to factor AI analytics into risk models, offering premium discounts that accelerate adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex for Advanced Physical Security Infrastructure | -1.8% | Netherlands national, particularly acute for retrofit projects | Short term (≤ 2 years) |

| Complex Integration Challenges with Legacy BMS and DCIM Systems | -1.5% | Netherlands national, concentrated in facilities built before 2020 | Medium term (2-4 years) |

| Rising Energy Taxation Impacting Budget Allocation for Security Upgrades | -1.1% | Netherlands national, driven by national energy policy | Medium term (2-4 years) |

| Skilled Labor Shortages in Physical Security Engineering | -0.9% | Netherlands national, reflecting broader European talent constraints | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Advanced Physical Security Infrastructure

A full deployment combining AI cameras, biometric portals, and fiber-optic DAS can top USD 2 million for a 10 MW hall, with maintenance adding 15-20% annually. Retrofit projects need gateways, VLAN segmentation, and recertification, inflating budgets. Energy-tax hikes cut margins, prompting midsize operators to defer discretionary upgrades. Security-as-a-service subscriptions from Securitas Technology spread costs but raise lock-in concerns. High entry cost thus remains the immediate brake on Netherlands data center physical security market acceleration.

Complex Integration Challenges with Legacy BMS and DCIM Systems

Pre-2020 facilities rely on BACnet or Modbus stacks, lacking IP hooks for modern security. Middleware orchestration adds latency and failure points, while constant patching is needed to align DCIM updates with access-control firmware. IEC 62443-certified gear eases some hurdles, yet much of the installed base remains non-compliant. Converging security networks with IT widens attack surfaces, demanding segmentation and deep-packet inspection. Limited OT-IT talent lengthens project cycles and raises labor costs, delaying go-live dates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Intrusion Detection Gains Momentum

Video surveillance retained 46.65% share in 2025, yet intrusion detection and monitoring is projected to grow at 13.63% CAGR. Fiber-optic acoustic sensing from Senstar detects fence cuts or digging and auto-triggers PTZ cameras. Gallagher’s radar tracks drones and vehicles, integrating with VMS for confirmation. As false-alarm rates fall, intrusion solutions narrow the share gap with cameras, responding to NIS2’s early-warning needs.

Cameras themselves shift to edge processing, fusing visible, thermal, and radar data. Milestone XProtect and Genetec Security Center unify these feeds. Verkada’s subscription VMS offers capex-free rollouts favored by midsize colocation operators, though data-sovereignty concerns keep hyperscalers on hybrid architectures. Mobile credentials from ASSA ABLOY and biometrics from HID bind identity to video for audit-ready chains.

By Service Type: Integration Complexity Drives Demand

In 2025, consulting held a 39.34% share as operators adopted NIS2, IEC 62443, and Tier-Certification mapping. Integration and deployment are set for a 13.45% CAGR, driven by retrofits requiring API bridges, VLAN redesigns, and accreditation testing. Securitas Technology's managed SOC bundles address skill shortages and ensure 24-hour compliance, while training in AI alert triage and lockdown drills transforms product projects into lifecycle engagements.

Managed SOC subscriptions are growing as operators seek 24-hour coverage without in-house teams. Vendors bundle log analytics, patch management, and incident-response drafting into contracts, streamlining compliance with NIS2’s alert and reporting windows. Labor shortages in OT-IT convergence skills drive demand for managed services, prompting integrators to expand training academies certifying technicians on IEC 62443 standards. Schneider Electric mandates dual-certified engineers for resale authorization, ensuring post-deployment support quality. Unified service-level agreements are boosting the market share of full-lifecycle providers in the Netherlands' data center physical security market, projected to grow steadily through 2031.

By Tier Type: Tier 4 Facilities Demand Redundant Security

Tier 3 controlled 44.12% of 2025 spend, balancing uptime with capex, yet Tier 4 shows a 13.73% CAGR as finance and government workloads demand fault-tolerant architectures. Certification audits check for dual-power cameras and redundant access-control buses, driving mirrored NVR clusters and dual-LAN card controllers.

Schneider Electric’s IEC 62443-certified EcoStruxure IT correlates entry events with voltage anomalies, proving both physical and cyber resilience. Tier 3 adopters increasingly pre-cable racks for future cameras, deferring device capex until occupancy rises. This phased model cushions capex shocks while preserving upgrade paths, supporting sustained demand across the Netherlands data center physical security market.

By Data Center Size: Hyperscale Drives Innovation

Large facilities held 48.21% revenue in 2025, yet hyperscale sites will log a 13.21% CAGR as cloud giants chase sovereign-data rules and AI training. Multi-building campuses secure exclusive supply deals for cameras, biometrics, and DAS, tailoring firmware to internal DevSecOps pipelines.

Fiber loops span kilometers, feeding AI correlators that blend vibration with weather data to refine detections. Medium sites adopt modular sensor arrays and outsource SOC functions, while edge pods deploy compact appliances bundling video, access, and environmental monitoring, relaying only metadata to cloud dashboards. This demand spectrum sustains diversified product lines.

By Data Center Type: Colocation Leads, Hyperscalers Accelerate

Colocation retained 58.43% share in 2025, serving enterprises that offload NIS2 compliance to landlords. Multi-tenant access systems carve badges by cage yet grant central oversight. Hyperscalers, meanwhile, will post a 13.85% CAGR, embedding proprietary identity platforms and custom biometrics in dedicated campuses. Enterprises and edge operators require open-API devices that marry with corporate SIEM and IAM stacks, as illustrated by Cisco Meraki cameras integrating via SAML.

Mid-sized colocation halls are adopting subscription-based video platforms for flexible operating expenses, with Verkada's bundled solution cutting first-year capital costs by up to 40%. Insurers now require multi-tenant campuses to segregate visitor traffic and maintain 24-hour SOC monitoring for loss-mitigation discounts. Edge operators use compact appliances combining video, access, and environmental sensors, transmitting alert metadata via LTE to centralized dashboards. This reduces maintenance visits, supports carbon-tracking mandates, and boosts the Netherlands' data center physical security market by 2031. Vendors offering standardized firmware across colocation, hyperscale, and edge platforms are well-positioned for multi-year rollouts and uniform compliance audits.

Geography Analysis

Amsterdam, Lelystad, and Groningen anchor the Netherlands data center physical security market, hosting roughly 200 active facilities. About 45 installations each exceeded 10 GWh power draw in 2024, contributing 4.6% of national electricity use. Capacity concentration enables bulk sensor procurement and rapid innovation cycles yet heightens target attractiveness, compelling multi-layered security. Greenfield projects worth over EUR 3 billion since 2024, including Equinix Lelystad and Pure DC Westpoort, have locked in multi-year hardware frameworks that cement vendor footprints.

Regulatory delays after the missed October 2024 NIS2 deadline drove operators to over-invest in SOC gear to pre-empt penalties. Energy-tax surcharges lifted data-center electricity costs by 6% in 2025, squeezing margins and nudging phased security upgrades. The Dutch Data Center Association lobbied for tax credits on energy-efficient AI inference hardware, arguing that smarter cameras cut server load and HVAC demand. Insurers offering risk-based premiums now discount policies for ISO 27001 or IEC 62443 badges, channeling capital toward certified upgrades.

Edge-computing nodes along 5G corridors introduce dispersed risk, with micro sites in industrial parks and rooftops. EdgeInfra’s Amsterdam deployments showcase 8 kW IP65 pods using passive IR cameras, piezoelectric door sensors, and LTE backup links to remote SOCs. Unmanned operations require self-healing security appliances that recalibrate autonomously and log tamper events, broadening the Netherlands data center physical security market into non-traditional footprints.

Mordor Intelligence's coverage of the global data center physical security market extends across other regions including Europe, Africa, and South America, while country-specific intelligence is also available for Sweden, United Kingdom, South Africa, Brazil, Spain, and France, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

Axis Communications, Bosch, and Hikvision lead AI-camera shipments, collectively commanding a significant slice of the Netherlands data center physical security market. Schneider Electric and Honeywell play in convergence, correlating intrusion telemetry with power and HVAC anomalies through IEC 62443-certified DCIM suites. Senstar and Gallagher specialize in high-security perimeters, offering fiber DAS and dual-band radar arrays to Tier 4 clients.

Nedap leverages local presence for customized badge-reader deployments aligned with NIS2 contractor-vetting clauses. Cloud-native challenger Verkada bypasses integrators by bundling camera, storage, and VMS into subscriptions that appeal to capex-constrained midsize operators. Managed-service partners such as Securitas Technology fill talent gaps by providing 24-hour monitoring and incident documentation compliant with NIS2.

Vendors with ISO-aligned DevSecOps pipelines gain advantage in RFPs emphasizing supply-chain trust. Hybrid cloud video platforms from Milestone and Genetec, storing sensitive footage onsite while pushing analytics to the cloud, strike adoption sweet spots among hyperscalers. Additionally, the growing emphasis on data privacy regulations is driving demand for secure and compliant video storage solutions.

Netherlands Data Center Physical Security Industry Leaders

Axis Communications AB

ABB Ltd.

Securitas Technology

Bosch Sicherheitssysteme GmbH

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Pure DC started construction of its EUR 1 billion (USD 1.07 billion) Amsterdam Westpoort hyperscale campus with AI cameras, biometrics, and fiber DAS in phase 1.

- December 2025: Equinix unveiled a EUR 1.5 billion (USD 1.6 billion) six-building campus in Lelystad, specifying unified VMS-access-intrusion stacks for Tier III standards.

- December 2025: Digital Realty launched AMS11, a 27 MW Amsterdam hall running Schneider Electric EcoStruxure IT for integrated physical-power analytics.

- November 2025: EdgeInfra announced micro data-center pods in Amsterdam using compact, self-healing security appliances for unmanned sites.

Netherlands Data Center Physical Security Market Report Scope

The data center physical security market refers to the industry focused on providing products and services to safeguard the physical infrastructure and assets of data centers. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. Key components of data center physical security may include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The Netherlands Data Center Physical Security Market Report is Segmented by Solution Type (Video Surveillance, Access Control Solutions, Intrusion Detection and Monitoring, and Other Solutions), Service Type (Consulting, Integration and Deployment, Maintenance and Support, and Managed Services), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge). The Market Forecasts are Provided in Terms of Value (USD).

| Video Surveillance |

| Access Control Solutions |

| Intrusion Detection and Monitoring |

| Other Solutions Types |

| Consulting |

| Integration and Deployment |

| Maintenance and Support |

| Managed Services |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| By Solution Type | Video Surveillance |

| Access Control Solutions | |

| Intrusion Detection and Monitoring | |

| Other Solutions Types | |

| By Service Type | Consulting |

| Integration and Deployment | |

| Maintenance and Support | |

| Managed Services | |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center | |

| By Data Center Type | Colocation Data Center |

| Hyperscalers Data Center/CSPs | |

| Enterprise and Edge Data Center |

Key Questions Answered in the Report

What is the value of the Netherlands data center physical security market?

The market stands at USD 67.27 million in 2026 and is projected to reach USD 122.46 million by 2031.

How does NIS2 affect Dutch data centers?

NIS2 classifies data centers as essential entities, mandating 24-hour alerts, 72-hour reports, and potential fines up to EUR 10 million for non-compliance.

Which solution category is expanding fastest?

Intrusion detection and monitoring systems are forecast to grow at a 13.63% CAGR through 2031.

Why are hyperscale projects critical for future demand?

Facilities like Equinix Lelystad and Pure DC Westpoort embed high-spec security from inception, driving a 13.21% CAGR for hyperscale sites.

How do energy taxes influence security budgets?

Higher power levies tighten margins, prompting phased upgrades that prioritize compliance-critical controls first.

Can certified security lower insurance premiums?

Yes, insurers increasingly offer discounts when facilities hold ISO 27001 or IEC 62443 certification, incentivizing investment in certified safeguards.

Page last updated on: