Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 5.20 Billion |

| Market Size (2030) | USD 7.90 Billion |

| Growth Rate (2025 - 2030) | 8.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Agricultural Films Market Analysis by Mordor Intelligence

The Asia Pacific agricultural films market size reached USD 5.2 billion in 2025 and is anticipated to reach USD 7.9 billion by 2030, at an 8.7% CAGR during the forecast period. Strong public subsidies for protected cultivation, rapid shifts toward water-saving mulch technologies, and stricter rules on plastic waste disposal are pivotal to this growth path. Supplier strategies nowadays favor product portfolios that balance low-cost Low-Density Polyethylene (LDPE) with premium biodegradable alternatives, while end users increasingly demand multi-season durability and light-diffusion functionality. Regional manufacturers are scaling capacity to capture rising demand, volatile polyethylene prices, and tightening food-contact rules continue to squeeze margins and accelerate innovation.

Key Report Takeaways

- By type, low-density polyethylene held 41.0% of the Asia Pacific agricultural films market share in 2024, while biodegradable films are predicted to grow at an 18.4% CAGR through 2030.

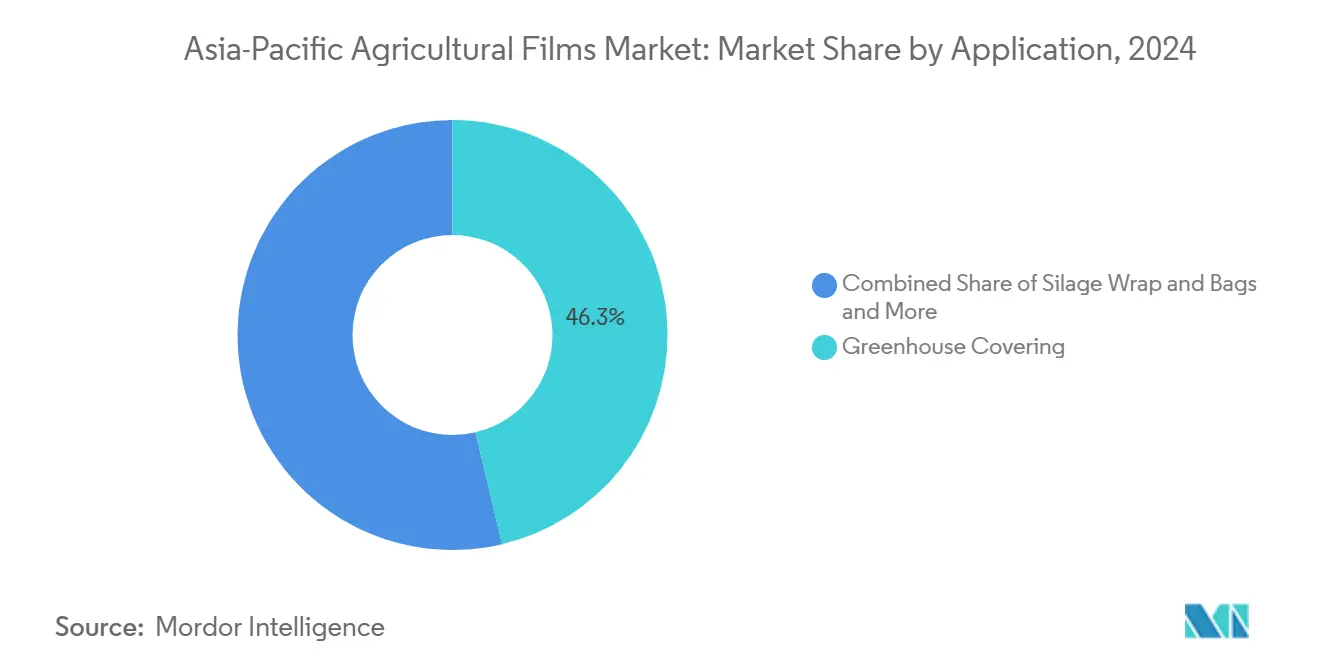

- By application, greenhouse held 46.3% market share of the Asia Pacific agricultural films market in 2024, while reservoir and irrigation canal liners are projected to grow at a 2.7% CAGR through 2030.

- By geography, China held 54.8% of the Asia Pacific agricultural films market share in 2024, while India is projected to grow at a 11.3% CAGR through 2030.

Asia-Pacific Agricultural Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing harvested area of greenhouse produce | +2.1% | China, India, and Japan | Medium term (2-4 years) |

| Growing use of mulch films in staple crops | +1.8% | Region-wide with India and China peaks | Short term (≤ 2 years) |

| Government subsidies for protected cultivation | +1.5% | India, China, and Thailand | Short term (≤ 2 years) |

| Shift toward high-value horticulture in Southeast Asia | +1.2% | Vietnam and Thailand are focal | Medium term (2-4 years) |

| Adoption of light-diffusion additives improving crop yield | +0.9% | Japan, South Korea, and Australia | Long term (≥ 4 years) |

| Emerging demand for biodegradable and recycled-content films | +1.2% | Global spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use of Mulch Films in Staple Crops

Water scarcity pressures across monsoon-dependent agricultural systems are accelerating mulch film adoption beyond traditional horticultural applications into staple crops. Government policies in China and India actively promote plastic mulching to achieve 30-40% water savings in rice and wheat cultivation, with China's agricultural subsidy framework providing targeted support for water-efficient farming technologies [1]Source: E3S Conference Proceedings, “Subsidy Mechanism in Government-Led Agricultural Supply Chain Finance,” e3s-conferences.org. Yield gains of 15–25% have persuaded smallholders to adopt low-cost Linear Low-Density Polyethylene (LLDPE) formats, while Thailand’s “3R Model” allocates 2 million hectares for mulching roll-outs by 2027. Demand momentum favors thin-gauge products that fit single-season crop cycles and minimize removal labor.

Increasing Harvested Area of Greenhouse Produce

Protected cultivation expansion reflects strategic responses to climate variability and premium market access requirements across the region. China leads with over 4 million hectares under protected cultivation, representing more than 80% of global protected vegetable production, while greenhouse coverage is expanding rapidly in low and middle-income countries due to socio-economic factors, including government support. The expansion encompasses both traditional plastic tunnels and advanced climate-controlled facilities, with greenhouse films evolving from basic polyethylene to specialized formulations incorporating light-diffusion additives that can increase tomato yields by up to 15%. India's greenhouse cultivation remains underdeveloped at approximately 50,000 hectares compared to China's 2 million hectares, creating substantial catch-up growth potential.

Government Subsidies for Protected Cultivation

Policy frameworks across major Asia-Pacific markets provide substantial financial incentives that directly reduce farmer adoption barriers for agricultural films and protected cultivation infrastructure. India reimburses up to 95% of polyhouse costs for scheduled caste and tribal growers, trimming the typical USD 627 per 100 m² outlay to USD 89 for beneficiaries [2]Source: Horticulture Department Telangana, “Unit Cost and Subsidy Pattern for Polyhouses,” horticulture.tg.nic.in. China’s multi-year support packages exceed USD 553 billion annually across agri-programs that prioritize water-saving film technologies. Such policies anchor predictable offtake for greenhouse and mulch films even when commodity cycles tighten.

Shift Toward High-Value Horticulture in Southeast Asia

Agricultural diversification strategies across Asian countries are driving farmers to transition from traditional staple crops to export-oriented fruits and vegetables that require protective film applications. Vietnam plans to raise organic acreage to 3% of farmland by 2030, a goal that favors biodegradable mulches and climate-stable greenhouse covers. Thailand’s outlook through 2027 shows rice, rubber, and cassava gains tied to improved cultivation inputs, including reservoir liners that combat drought-linked seepage. Export growth of USD 3.1 billion in United States farm goods to Vietnam underscores the premium fresh-produce channel that relies on quality-preserving films.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial investment in protected farming systems | -1.4% | India, Asian smallholder regions | Short term (≤ 2 years) |

| Adverse environmental impact of conventional plastics | -1.1% | Developed Asia-Pacific and China hot spots | Medium term (2-4 years) |

| Fragmented smallholder landholdings limiting economies of scale | -0.8% | India, Indonesia, and Philippines | Long term (≥ 4 years) |

| Sub-optimal recycling infrastructure in rural Asia Pacific | -0.6% | Rural areas excluding Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment in Protected Farming Systems

Capital requirements for greenhouse infrastructure and specialty films create significant adoption barriers, particularly for smallholder farmers who dominate agricultural landscapes across developing Asia-Pacific markets. Polyhouse costs run USD 400–500 per m² for low-tech builds and USD 2,500–4,000 per m² for fully automated units, with specialty films representing up to 20% of that spend. Even after India’s 75–95% grants, the farmer co-pay can top annual household income, deterring rapid scaling. Japan’s sector projects farm-gate output to fall from JPY 8.9 trillion (USD 57.2 billion) in 2020 to JPY 4.3 trillion (USD 27.7 billion) by 2050, limiting uptake of capital-intensive greenhouses.

Adverse Environmental Impact of Conventional Plastics

Growing regulatory scrutiny of microplastic contamination and soil degradation from conventional agricultural films is creating compliance costs and market access restrictions across the region. Film fragments below 5 mm settle into soils, curbing microbial activity and triggering local bans on standard PE mulch in fruit belts of Shandong and Xinjiang. Indonesia and Thailand nowadays give manufacturers only 12 months to certify migration compliance, elevating testing and reformulation costs. Producers that delay pivoting to degradable blends risk market exclusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biodegradable Films Drive Premium Shift

Low-Density Polyethylene (LDPE) dominated the Asia Pacific agricultural films market with a 41.0% market share in 2024, owing to low resin prices and ubiquitous converter capacity. The segment benefits from technical innovations like Dow-Mitsui's biomass-derived EVA and LDPE launched in September 2024, which maintain identical properties to petroleum-based alternatives while reducing greenhouse gas emissions [3]Source: ChemAnalyst, “Dow-Mitsui Polychemicals Commences Marketing of Biomass-Derived EVA and LDPE,” chemanalyst.com.

Biodegradable films represent the fastest-growing segment at 18.4% CAGR through 2030, driven by regulatory pressures and significant investment flows, including SKC Group's USD 100 million facility in Vietnam producing 70,000 metric tons annually of Polybutylene Adipate Terephthalate (PBAT) biodegradable plastics by 2025. Regulatory compliance frameworks like Indonesia's draft food contact material law are accelerating adoption of biodegradable alternatives, particularly in applications where end-of-life disposal creates environmental concerns.

By Application: Reservoir Liners Emerge as Growth Driver

Greenhouse covering dominates applications with 46.3% market share in 2024, reflecting the region's massive protected cultivation expansion and government support for controlled environment agriculture. Quantum dot films are emerging as a technical innovation in greenhouse applications, with research demonstrating increased radiation capture and yield improvements for lettuce and basil crops despite reduced daily light integral. Thailand's agricultural burning reduction initiatives are creating demand for alternative crop residue management solutions, potentially expanding silage film applications as farmers seek sustainable alternatives to open burning practices.

Reservoir and irrigation canal liners represent the fastest-growing application at 12.7% CAGR through 2030, driven by water scarcity pressures and infrastructure modernization programs across the region. The segment benefits from government investments in water conservation infrastructure, with China's agricultural water-saving initiatives promoting lined irrigation systems to reduce seepage losses by 30-40% in arid regions.

Geography Analysis

China commands 54.8% market share in 2024, leveraging its massive protected cultivation infrastructure and established manufacturing base for agricultural films. Environmental regulations are reshaping material preferences toward biodegradable alternatives. The country's agricultural plastic pollution reaches 570 kilotons annually, concentrated in Xinjiang and Shandong provinces, creating regulatory pressure for sustainable film solutions and driving investments in biodegradable alternatives. Government subsidies and water conservation mandates continue supporting market expansion, though polyethylene price volatility between USD 910-1190 per metric ton during 2024 created margin pressures for film manufacturers.

India emerges as the highest-growth geography at 11.3% CAGR through 2030, driven by comprehensive government support, including 95% subsidies for scheduled caste and tribal farmers, and expanding organic farming initiatives targeting 2.5-3.0% of agricultural land by 2030. In 2024, Balrampur Chini Mills' INR 20 billion (USD 221.1 million) investment in India's first industrial Poly Lactic Acid (PLA) bioplastic plant with 75,000 metric tons annual capacity demonstrates growing domestic capabilities for biodegradable film production.

Japan and South Korea face structural challenges from aging agricultural populations and declining farm entities, yet maintain focus on high-tech applications and premium film solutions that justify advanced material investments. Asia-Pacific markets, led by Vietnam and Thailand, demonstrate strong momentum through agricultural diversification toward high-value horticulture and substantial foreign investment, including SKC Group's USD 100 million biodegradable plastic facility in Vietnam and NatureWorks' USD 350 million Poly Lactic Acid (PLA) manufacturing expansion in Thailand utilizing locally sourced sugarcane feedstock.

Competitive Landscape

The Asia Pacific Agricultural film market is moderately fragmented, with many players competing in the market. Some of the players in this region include BASF SE, Berry Global Inc., Plastika Kritis SA, ExxonMobil Chemical, and RKW Group, etc. In 2024, Novamont collaborates with Bayer CropScience on Mater-Bi twine and clips, extending compostable solutions into ancillary greenhouse items. Shouzheng in China scales degradable mulch output to meet provincial quotas, while SKC Group’s Vietnam venture targets Southeast Asia’s eco-mandates. Portfolio restructuring is evident as Saudi Basic Industries Corporation (SABIC) divests lower-margin film businesses and adds 135 new products to capture a sustainability premium.

Apart from the top five players, companies such as Sumitomo Chemical Co., Ltd., The Dow Chemical Company, and Novamont S.p.A. are key players in the global market with innovative products and technologies. The competitive rivalry among these companies drives innovation and market growth. During the forecast period, technological advancements, new product development, and robust distribution networks are anticipated to support market expansion.

Strategic partnerships increasingly link material science with data platforms. Japanese sensor firms and Korean telecom operators test Internet of Things (IOT) enabled greenhouse covers that log humidity and ultraviolet exposure, offering agronomic advice through subscription services. The Asia Pacific agricultural films market thus rewards players that combine polymer innovation, sustainability credentials, and digital agronomy.

Asia-Pacific Agricultural Films Industry Leaders

Berry Global Inc.

BASF SE

ExxonMobil Chemical Company

RKW SE

Plastika Kritis SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: BASF SE introduced Tinuvin NOR 211 AR to assist film producers and converters in addressing the challenges of plasticulture, which involves the use of plastic materials in agricultural applications. This product provides an effective solution for agricultural plastics exposed to high levels of UV radiation, thermal stress, and inorganic chemicals frequently used in crop management and disinfection processes globally.

- June 2024: RKW SE partnered with Dow Chemical Company to launch two new grades of resins under Dow's Revoloop recycled plastic resin product line, including a resin containing up to 100% post-consumer recycled (PCR) plastic. While the primary announcements centered on Europe and global markets, the emphasis lies in harnessing Dow's material science and RKW's film expertise for circular packaging on a global scale.

- September 2025: Uzbekistan, in collaboration with China, plans to launch production of smart temperature-regulating greenhouse film. The technology helps maintain greenhouse temperatures 5–7°C warmer than outside in cold weather (vs. 0–2°C with standard films) and 5–8°C cooler in hot weather, ensuring better climate control. This reduces reliance on external heating and cooling, cutting energy use by over 60%. Its advanced infrared radiation features also boost photosynthesis, enabling crops to grow 1.5–2 times faster.

Asia-Pacific Agricultural Films Market Report Scope

Agricultural films are the materials used extensively for soil protection, greenhouse farming, and mulching. The benefits derived include reduced soil erosion and compaction, temperature control, nutrient conservation, seed germination, weed control, and protection against UV rays, among others. The Asia Pacific Agricultural Films Market is segmented by Type (Low-Density Polyethylene, Linear Low-Density Polyethylene, High-Density Polyethylene, Ethyl Vinyl Acetate (EVA)/Ethylene Butyl Acrylate (EBA), and Other Types), Application (Greenhouse, Silage, Mulching, and Other Applications), and Geography (China, India, Japan, Australia, and Rest of Asia Pacific). The Report Offers Market Size and Forecasts in Terms of Value in (USD) for all the Above Segments.

By Type

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| High-Density Polyethylene (HDPE) |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate (EVA/EBA) |

| Biodegradable/Compostable Films |

By Application

| Greenhouse Covering |

| Silage Wrap and Bags |

| Mulching |

| Fumigation & Soil Solarization Films |

| Reservoir & Irrigation Canal Liners |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia & New Zealand |

| Rest of Asia-Pacific |

| By Type | Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) | |

| High-Density Polyethylene (HDPE) | |

| Ethyl Vinyl Acetate / Ethylene Butyl Acrylate (EVA/EBA) | |

| Biodegradable/Compostable Films | |

| By Application | Greenhouse Covering |

| Silage Wrap and Bags | |

| Mulching | |

| Fumigation & Soil Solarization Films | |

| Reservoir & Irrigation Canal Liners | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia & New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the fastest-growing application?

Reservoir and irrigation canal liners are forecast to grow at a 12.7% CAGR owing to water-saving infrastructure investments.

Why are biodegradable films gaining ground?

Tightening waste regulations in China, Indonesia, and Thailand, plus new local PBAT and PLA capacity, propel 18.4% CAGR growth.

Which country offers the highest growth potential?

India is set to record an 11.3% CAGR owing to subsidies covering up to 95% of polyhouse costs and rising organic acreage targets.

Who is the leading company?

Berry Global holds a significant revenue share, leveraging a sustainability-centric flexible portfolio and vertically integrated operations.

Page last updated on: