Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

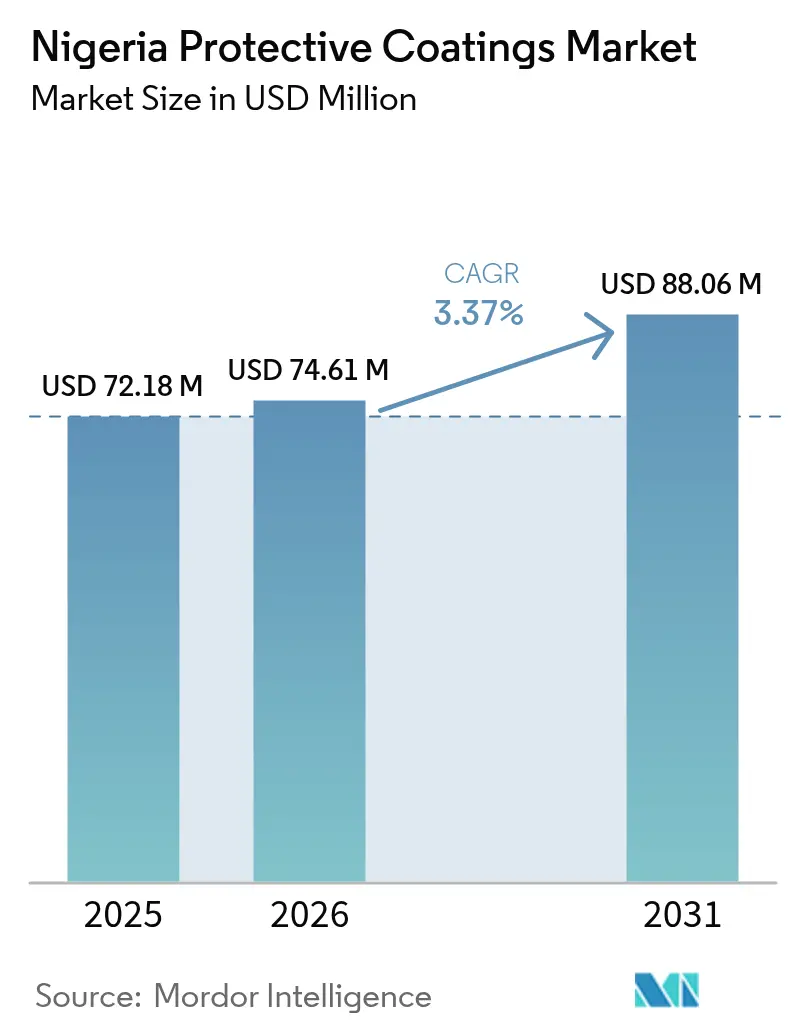

| Base Year Market Size (2025) | USD 72.18 Million |

| Market Size (2026) | USD 74.61 Million |

| Market Size (2031) | USD 88.06 Million |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

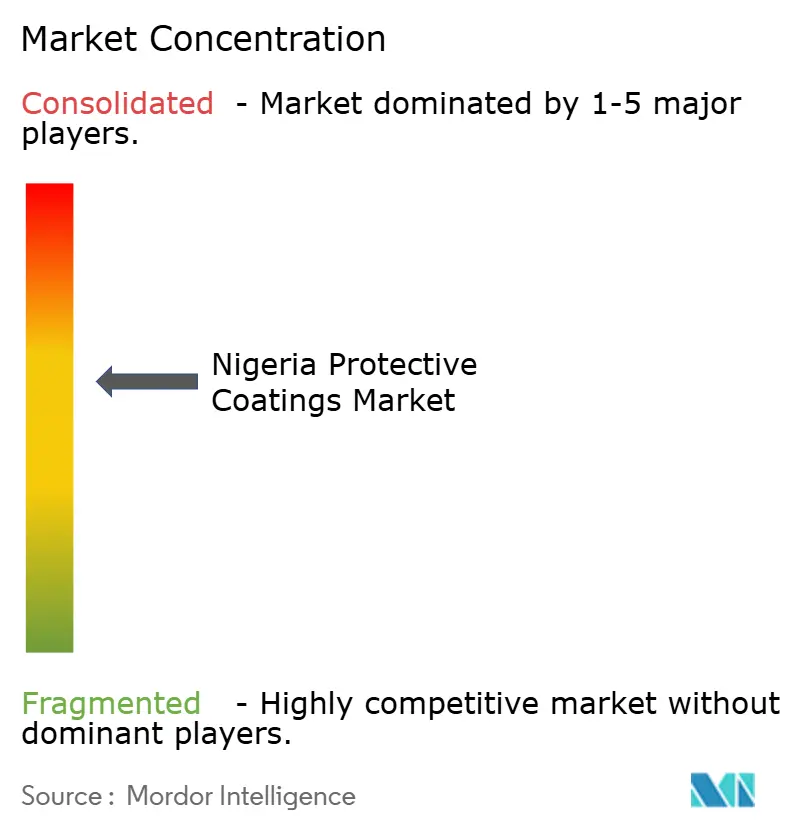

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Protective Coatings Market Analysis by Mordor Intelligence

Nigeria Protective Coatings Market size in 2026 is estimated at USD 74.61 million, growing from 2025 value of USD 72.18 million with 2031 projections showing USD 88.06 million, growing at 3.37% CAGR over 2026-2031. This market size projection highlights the sector’s strategic role in protecting the nation’s expanding infrastructure and industrial assets, particularly as owners prioritize longer service life over short-term cost savings. Demand growth aligns closely with federally backed road, rail, and housing programs, while offshore oil and gas developments around the Niger Delta add incremental volumes for high-performance marine-grade systems. Environmental mandates on volatile organic compounds (VOC) and lead content continue to reshape product portfolios, accelerating technology shifts toward water-based chemistries. Currency fluctuations that increase the cost of imported resin and pigment strengthen the case for local sourcing strategies and production efficiencies in the Nigeria protective coatings market.

Key Report Takeaways

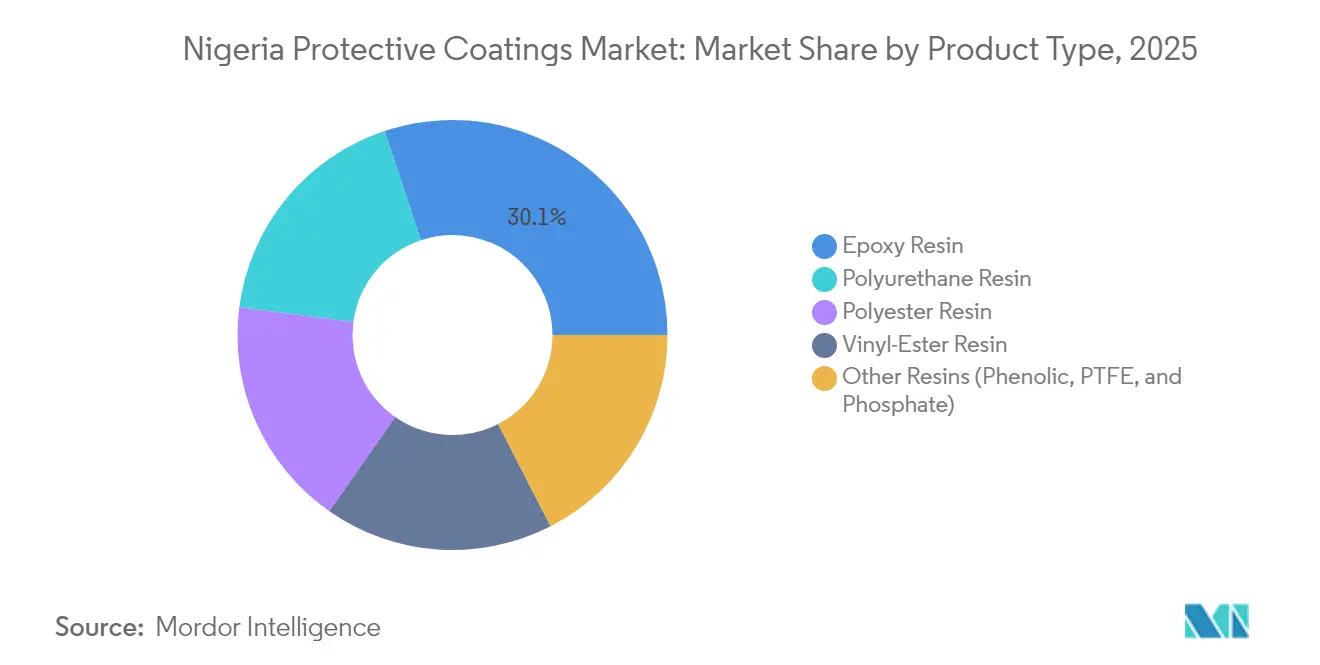

- By product type, epoxy resin captured 30.12% of the Nigeria protective coatings market share in 2025, whereas polyurethane resin posts the fastest CAGR at 3.65% through 2031.

- By technology, solvent-based systems accounted for 70.05% of the 2025 Nigeria protective coatings market size, while water-based technology is expected to exhibit a 3.91% CAGR from 2025 to 2031.

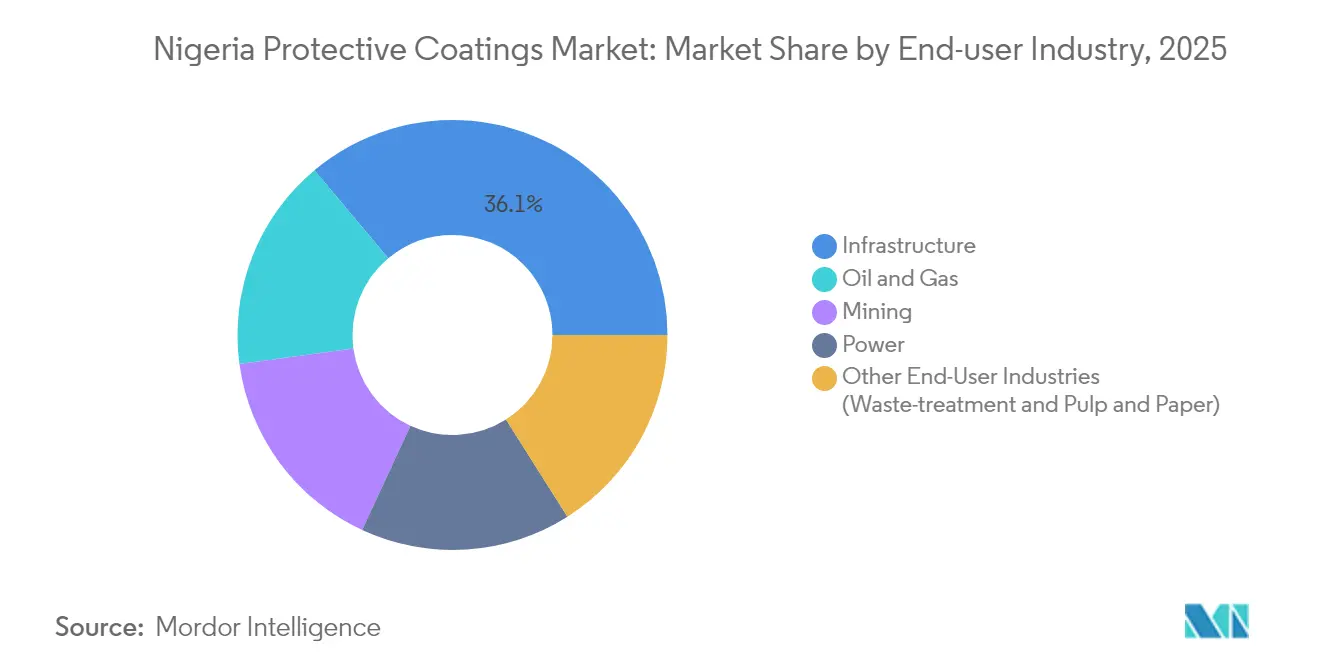

- By end-user industry, infrastructure led with a 36.10% revenue share in 2025, while the same segment is expected to advance at a 3.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Protective Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed infrastructure boom | +1.2% | Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Offshore oil and gas expansion | +0.8% | Niger Delta coastal states | Long term (≥ 4 years) |

| Decentralized mini-grid power build-out | +0.5% | Rural and semi-urban areas | Medium term (2-4 years) |

| Local-content mandate for public projects | +0.4% | Nationwide | Short term (≤ 2 years) |

| New anti-corrosion standards for rail and ports | +0.3% | Major transport corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed Infrastructure Boom

Large-scale rail, port, and housing projects now specify corrosion-resistant coatings rather than lowest-cost paints, reinforcing demand for high-solids and zinc-rich primers. The Lekki Economic Zone and the Lagos Rail Mass Transit Purple Line exemplify premium applications where lifecycle cost optimization outweighs initial price. Public procurement agencies have begun referencing ISO 12944 durability classes, compelling suppliers to certify performance data and invest in technical service teams. Consequently, premium coatings command favorable margins, sustaining the paint and protective coatings market even during cyclical slowdowns in residential construction[1]“Lagos State Investment Opportunities,” Lagos State Government, lagosstate.gov.ng.

Offshore Oil and Gas Expansion in Niger Delta

Floating production platforms and subsea pipelines require coating systems that meet ISO 12944-9 immersion standards and reach dry film thickness levels up to 800 micrometers. Global operators and Nigerian independents alike stipulate pre-qualification under NORSOK M-501 or IOGP S-715, narrowing the vendor pool to companies with track records in extreme marine conditions. These specialized specifications stimulate local investment in blast and painting yards certified to ISO 9001 and ISO 45001, lifting service capability across the paint and protective coatings market[2]“ISO 12944-9 Standard,” International Organization for Standardization, iso.org.

Decentralized / Mini-grid Power Build-out

Solar farms in Kaduna and wind installations in Plateau State require anti-reflective, UV-stable coatings with transmittance above 90%. Meanwhile, balance-of-system equipment needs abrasion-resistant topcoats that withstand dust storms. The annual growth of 3–4% in renewable capacity has persuaded several Nigerian coaters to partner with photovoltaic module importers for field-applied clear-coat solutions, creating a distinct niche in the paint and protective coatings market. Bio-based additives, sourced from local agro-feedstock, help offset foreign exchange exposure and comply with tightening VOC limits.

Local-content Mandate for Public Projects

Federal and state agencies now apply a 40-to-60% local-value threshold in tenders, measured by factory location, workforce, and material sourcing. Chemical and Allied Products (CAP) maintains an edge by combining AkzoNobel technology with domestic production, evidenced by a 52% jump in 2024 revenue to NGN 36.36 billion. Competitors without local resin reactors face higher import duties and delayed lead times, reinforcing CAP’s first-mover advantage in the paint and protective coatings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC-emission regulation (NESREA) | -0.7% | Nationwide, urban focus | Short term (≤ 2 years) |

| FX volatility inflating imported raw material cost | -1.1% | Nationwide | Short term (≤ 2 years) |

| Proliferation of counterfeit / low-grade coatings | -0.4% | Informal markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC-emission Regulation (NESREA)

The 90 ppm lead cap, introduced in 2023, forces reformulation toward water-borne and high-solid systems. Smaller local producers struggle to fund research and development (R&D) and meet testing benchmarks, risking market exit or acquisition. Larger players pass part of the compliance cost to customers, yet margins remain under pressure in price-sensitive segments of the paint and protective coatings market. Enforcement varies by state, creating temporary competitive imbalances.

FX Volatility Inflating Imported Raw Material Cost

The Naira’s slide from NGN 325 per USD in 2020 to beyond NGN 1,650 per USD by 2024 has increased the landed cost of epoxy resins, titanium dioxide, and specialty additives, which represent over 50% of the paint and protective coatings market's bill of materials. CAP reported a noticeable decline in gross profit in early 2024, despite implementing selective price adjustments. Contract hedging and local feedstock substitution have become priority strategies, yet supply chain risks remain high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Epoxy Resin Dominance amid Polyurethane Growth

Epoxy resin secured 30.12% of 2025 revenue due to its robust solvent resistance and adhesion, which are demanded by offshore platforms, high-pressure pipelines, and chemical storage tanks. Polyurethane resin, favored for ultraviolet stability on exposed superstructures, is expanding at a 3.65% CAGR, outpacing all other chemistries. The Nigeria protective coatings market size for polyurethane systems is projected to widen, especially in Lagos State’s coastal bridges, where color retention and gloss durability reduce maintenance cycles. Polyester and vinyl-ester groups hold a combined share of about 15-20%, serving niche chemical-processing assets. International standards, such as ISO 12944-5:2018, continue to shift project specifiers toward multi-layer epoxy-polyurethane stacks that extend service life up to 25 years.

By Technology: Solvent-based Leadership with Water-based Momentum

Solvent-borne coatings retained 70.05% revenue in 2025 due to their application tolerance in Nigeria’s high humidity. Yet, water-based formulas are increasing at a 3.91% CAGR, aided by NESREA’s VOC cap and by global oil majors' mandates for low-emission assets. The paint and protective coatings market share for water-borne systems remains small but gains visibility in factory-applied container coatings and galvanic primers. Powder coatings hold niche positions in the appliance and automotive parts industries, where electrostatic spray lines deliver near-zero VOC release and reclaim rates exceeding 95%. Berger Paints’ late-2024 launch of Luxol Premium Matt, an eco-friendly water-borne line, signals a broader migration toward sustainable formulations.

By End-user Industry: Infrastructure Sector Drives Dual Leadership

Infrastructure simultaneously accounts for 36.10% of 2025 revenue and boasts the highest 3.49% CAGR, underpinned by rail corridors, federal highways, and mass housing schemes. Oil and gas, the second-largest sector, depends on marine-grade epoxy and polysiloxane coatings that meet ISO 20340 cyclic aging protocols. Mining and power contribute incremental growth, as solar parks and wind farms specify anti-corrosion clear-coats for metallic supports. Waste-treatment and pulp-and-paper lines form a small but rising segment, stimulated by environmental compliance and plant upgrades. The paint and protective coatings market size allocated to infrastructure projects is expected to maintain its leading share through 2031 as federal budgets prioritize asset longevity.

Geography Analysis

Lagos State represented the single largest contributor to the Nigeria protective coatings market in 2025, supported by megacity infrastructure and coastal humidity that accelerates metal corrosion. The Lagos Rail Mass Transit Purple Line and the Lekki Port Complex generate consistent demand for ISO-certified multi-coat systems. The Niger Delta ranks second, driven by upstream offshore facilities that require high-build epoxy and polyurethane coverings with service targets of 20 years or more. Port Harcourt’s fabrication yards and Warri refineries ensure steady base-load volumes for marine and chemical-resistant products.

Northern Nigeria’s Abuja–Kaduna–Kano growth corridor records rising volumes in governmental complexes and dry-port logistics hubs. Climatic extremes necessitate abrasion-resistant coatings to mitigate harmattan dust and diurnal thermal shifts. Security risks and sporadic insurgency slow some project timelines, but do not erase long-term growth prospects. In aggregate, coastal and riverine areas deliver premium margins due to more frequent maintenance requirements, while inland states tend to gravitate toward cost-optimized single-coat alkyd and acrylic solutions.

Emerging rural electrification schemes bring mini-grid assets to communities in Plateau, Taraba, and Nasarawa States. These projects involve coated solar racking, switchgear enclosures, and steel tower segments, collectively broadening the geographic footprint of the paint and protective coatings market beyond the traditional southwest and south-south commercial hubs.

Regulatory Landscape

Nigeria protective coatings products operate within a chemicals-control and standards regime led by NAFDAC and the Standards Organisation of Nigeria (SON). NAFDACs Chemical Evaluation and Research Directorate regulates the importation, manufacture, storage, and distribution of chemical products under the gazetted NAFDAC (Chemical and Chemical Product) Regulations 2024, with a 2026 draft regulation referenced in official materials as part of ongoing updates to the framework. For market access and quality assurance, SON enforces Nigeria Industrial Standards through product certification programs and related conformity assessment processes.

For imported binders, pigments, and additives used in protective coatings, NAFDAC requires Chemical Import Permits prior to shipment arrival, with permits valid through December 31 of the year of issuance and used for clearing purposes. Compliance requirements also extend to operational controls such as Good Manufacturing Practice inspections for facilities handling chemicals, restrictions on siting warehouses in residential or market areas, and mandatory Safety Data Sheets and Globally Harmonized System (GHS) labeling for chemicals in trade, shaping both formulation choices and supply-chain documentation discipline for manufacturers and importers.

Value Chain Analysis

The value chain begins with raw-material sourcing, where resin systems, pigments (for example, titanium dioxide), and specialty additives are frequently import-dependent, increasing exposure to foreign exchange movements and import-clearance timelines. NAFDACs Chemical Import Permit process and the 2024 chemical regulations add compliance touchpoints upstream, while SONs technical standard-setting activities for paints and allied products influence quality benchmarking and product certification expectations for both locally made and imported coatings.

Midstream activities include local manufacturing, blending, and packaging by established players such as Berger Paints Nigeria Plc, Meyer PLC, and Paints and Coatings Manufacturers Nigeria Ltd. (PCMN), alongside other domestic manufacturers and licensed operators such as Sigma Coatings Nigeria Limited (a PPG licensee). Downstream, distribution combines proprietary retail networks and dealer channels for general coatings with direct-to-project supply for infrastructure and industrial users, plus site services where protective performance depends on surface preparation and application discipline (for example, industrial and oil and gas focused supply and services referenced by PCMN and specialist contractors). Across the chain, storage and warehousing compliance, SDS/GHS documentation, and anti-counterfeit quality assurance practices remain operational differentiators in a market where project specifiers increasingly reference internationally recognized corrosion-protection standards.

Competitive Landscape

The Nigeria Protective Coatings Market is moderately consolidated. CAP, Berger Paints Nigeria, Meyer Plc, Premier Paints, and Portland Paints dominate the market thanks to their local factories, ISO-certified labs, and technical licensing from global formulators. CAP’s 52% jump in 2024 revenue to NGN 36.36 billion illustrates the benefits of import substitution, backward integration in resins, and AkzoNobel know-how. Environmental certifications, particularly ISO 14001:2015, are emerging as tender prerequisites for infrastructure megaprojects, reinforcing the transition toward greener chemistries in the paint and protective coatings market.

Nigeria Protective Coatings Industry Leaders

Berger Paints Nigeria Plc

Akzo Nobel N.V.

Chemical and Allied Products PLC

PPG Industries, Inc.

Meyer PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven reformulation and specification tightening are creating whitespace for suppliers that can document performance while lowering emissions, especially as Nigeria enforces chemical controls through NAFDAC and product quality oversight through SON. The lead cap referenced in the market context (90 ppm, introduced in 2023) and evolving VOC requirements push demand toward water-borne and higher-solids systems, while procurement references to ISO 12944 durability classes on public infrastructure projects raise the value of certified test data, application know-how, and jobsite technical service.

Policy and capability-building initiatives provide additional levers for local value addition and service-led differentiation. The Nigeria Industrial Policy 2025 (launched February 2025) prioritizes industrial base re-engineering in sectors including petrochemicals and metals, aligning with protective coating demand tied to fabrication, maintenance, and asset integrity. In company activity, Jotun Paints Nigeria opened an Inspiration Centre in Victoria Island, Lagos in June 2026 as a technical advisory hub for protective, marine, and flooring solutions, signaling commercial focus on consultative selling and specification support rather than commodity competition. These shifts support opportunities for coating-plus-application models, applicator training, and localized supply strategies that reduce dependence on imported inputs and improve delivery reliability for infrastructure and oil and gas maintenance cycles.

Recent Industry Developments

- June 2026: Jotun Paints Nigeria opened a new Inspiration Centre in Victoria Island, Lagos, positioned as a technical advisory hub for protective, marine, and flooring solutions. The facility supports specification-driven selling and customer training for higher-performance systems used in coastal infrastructure and industrial maintenance. It also signals a push to deepen in-country engagement, with additional expansion locations referenced for Abuja, Ikeja, and Port Harcourt.

- October 2025: PPG Industries, Inc. announced the global launch, including Nigeria, of PPG ENVIROCRON Extreme Protection Edge Plus powder coating, a patent-pending one-coat edge-protection innovation. The launch expands powder-coating options for corrosion protection where edge coverage is a failure point, supporting fabricators seeking lower-VOC alternatives to solvent-borne systems. This strengthens competition in premium protective solutions that can reduce rework and extend service intervals.

- December 2024: BUA Group inaugurated a new gypsum plaster plant with 2,400 tons per day capacity, reinforcing momentum in construction materials supply. Increased building activity raises demand for protective coatings across associated infrastructure, including steelwork, equipment, and ancillary assets that require corrosion control. The commissioning also underlines the role of domestic capacity additions in sustaining project pipelines that consume industrial coatings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the Nigeria protective coatings market as the value of coatings mainly used to protect assets from corrosion, abrasion, chemicals, moisture, and weathering across industrial and infrastructure environments, sold for use within Nigeria.

Scope exclusions: This sizing excludes decorative or architectural wall paints and coatings that are primarily bought for aesthetics rather than protection.

Segmentation Overview

- By Product Type

- Epoxy Resin

- Polyurethane Resin

- Polyester Resin

- Vinyl-Ester Resin

- Other Resins (Phenolic, PTFE, Phosphate)

- By Technology

- Water-based

- Solvent-based

- Powder-based

- By End-user Industry

- Oil and Gas

- Mining

- Power

- Infrastructure

- Other End-User Industries (Waste-treatment, Pulp and Paper)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with Nigeria macro and industry direction, and then it was narrowed down to protective coatings demand pools. We used public sources such as the National Bureau of Statistics, the Nigeria Upstream Petroleum Regulatory Commission, the Central Bank of Nigeria, and the Nigeria Ports Authority to understand project activity, trade movement, and investment signals that link to corrosion protection needs.

To ground the inputs, we also referred to sources such as UN Comtrade and World Bank indicators, plus standards or guidance material available from bodies such as ISO. Company filings, investor presentations, and reliable press coverage on major industrial and infrastructure projects were used to capture how coating specifications are framed in tenders and contracts. Where needed, paid subscriptions were used for company financials and intelligence, patent databases, and shipment-level import-export checks to validate directionally what was seen in public data. The sources listed above are illustrative and not exhaustive, and other references were also reviewed to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on validating what actually gets specified and applied on Nigerian sites, and how pricing moves when conditions change. We spoke with manufacturers, distributors, applicators, EPC-linked stakeholders, and end users across oil and gas, marine, power, and infrastructure. This coverage helped test assumptions on volumes, maintenance cycles, and typical system selection.

Because this is a single-country market, respondent coverage was balanced across major industrial clusters and port-linked corridors, and then checked again through follow-up questions whenever desk signals and field responses did not line up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 20% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

The core model uses a top-down build that reconstructs Nigeria demand from protective coatings linked activity, and then it is pressure-tested with selective bottom-up approximations. In practice, we tied coating demand to signals such as industrial and infrastructure project flow, asset maintenance intensity, import patterns for coatings and key raw materials, and the mix of high corrosion exposure environments that typically pull epoxy and polyurethane systems.

To keep the model repeatable, a small set of measurable inputs was used and reviewed each cycle, including project starts and completions in energy and infrastructure, crude and refined products activity that affects terminal and pipeline maintenance, marine and port throughput as a proxy for coastal asset load, typical repaint intervals for steel structures, and observed pricing ranges by resin system and technology. Forecasting was then carried using scenario analysis supported by expert consensus on project timing and inflation. The output was checked against trend consistency rather than relying on one single assumption. Where bottom-up checks had gaps, we used sampled price x volume points from channel discussions to bracket the missing pieces and keep totals realistic.

Data Validation & Update Cycle

Validation is done through several rounds of checks so the numbers remain aligned with real market signals. We compare model outputs against independent indicators, such as import movement, project activity, and maintenance spending cues, and then investigate outliers by tracing them back to either volume, pricing, or timing assumptions.

Before sign-off, another analyst reviews the logic, unit conversions, and year-to-year movements so unusual spikes are explained or corrected. Reports are refreshed annually, and material events (for example, sharp currency moves or major project delays) trigger interim updates and selective re-contacts. Right before delivery, a final pass is completed so the latest public releases and field feedback are reflected in the view shared with clients.

Mordor Intelligence's Nigeria Protective Coatings Market Size Versus Other Published Estimates

Different published market values for Nigeria protective coatings can vary widely because the scope line is drawn differently and the demand drivers used are not always the same. Some studies lean more on broad coatings totals or use aggressive pricing escalation, while others apply conservative project pipelines and exclude repaint work, which shifts the end result.

Decorative paints and general architectural coatings sit outside Mordor Intelligence's scope, and this single exclusion is a major reason the 2025 value is much lower than estimates that combine protective coatings with the wider paints and coatings pool. Differences also come from how import parity pricing is handled during currency swings, whether maintenance cycles are counted in addition to new-build coating demand, and how frequently assumptions are refreshed when large oil and gas or infrastructure projects change timelines.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 72.18 M (2025) | |

| Industry Publisher A | USD 711.28 M (2025) | Uses a broader Nigeria paints and coatings total that likely includes decorative and architectural categories, so the addressable value expands beyond protective use cases. |

| Trade Source B | USD 85.00 M (2026) | Shows a later-year snapshot and may emphasize new project coatings more than repaint and maintenance demand, which can lift or compress the total depending on project timing. |

Taken together, the spread is mainly explained by what is counted as a protective coating and how the model treats maintenance versus new-build activity in Nigeria. By tying the estimate to observable project and asset signals and then cross-checking with channel pricing and application realities, the resulting market size stays traceable to clear inputs and can be updated in a repeatable way when conditions change.

Key Questions Answered in the Report

How large is Nigeria’s protective coatings market in 2026?

The Nigeria protective coatings market size stands at USD 74.61 million in 2026, with a 3.37% CAGR projected to 2031.

Which end-user sector generates the highest demand for coatings in Nigeria?

Infrastructure leads with 36.10% revenue share in 2025, owing to large rail, port, and housing projects.

What product chemistry dominates Nigeria’s protective-coatings demand?

Epoxy resin holds 30.12% market share because of its strong adhesion and chemical resistance on oil and gas assets.

How is regulation impacting product formulation strategies?

NESREA’s 90 ppm lead cap and tighter VOC rules are accelerating shifts toward water-based and high-solid formulations.

Which coating technology is growing the fastest?

Water-based systems post a 3.91% CAGR due to environmental compliance and multinational corporate policies.

Page last updated on: