Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

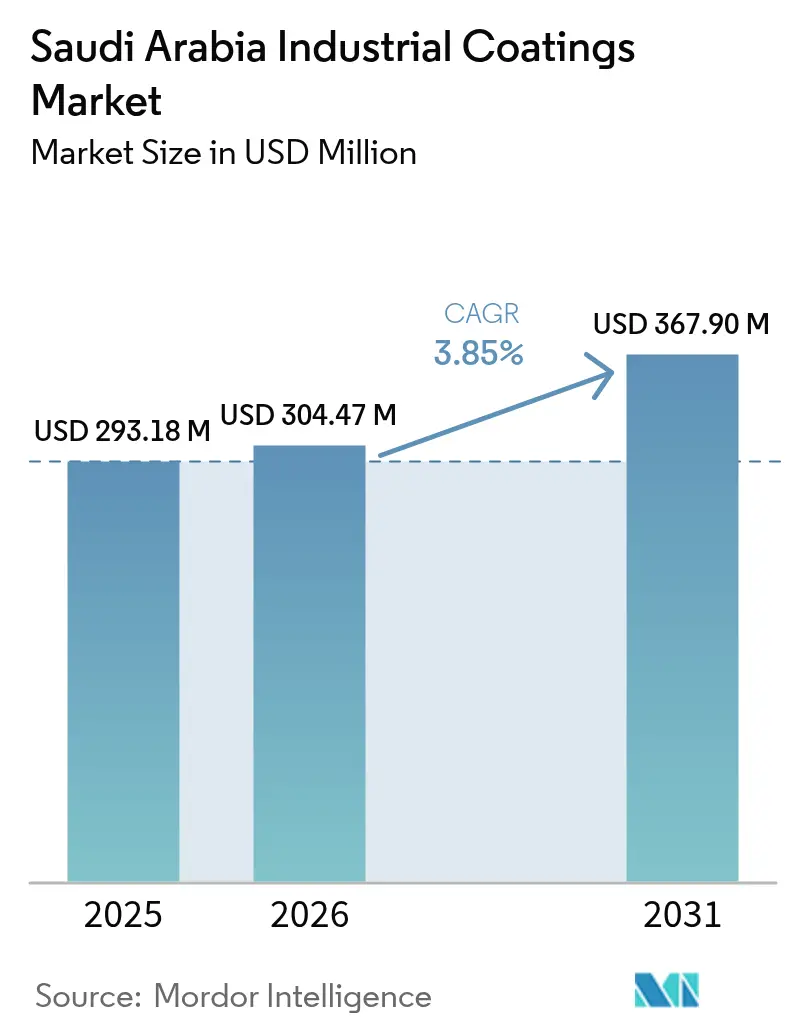

| Base Year Market Size (2025) | USD 293.18 Million |

| Market Size (2026) | USD 304.47 Million |

| Market Size (2031) | USD 367.9 Million |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

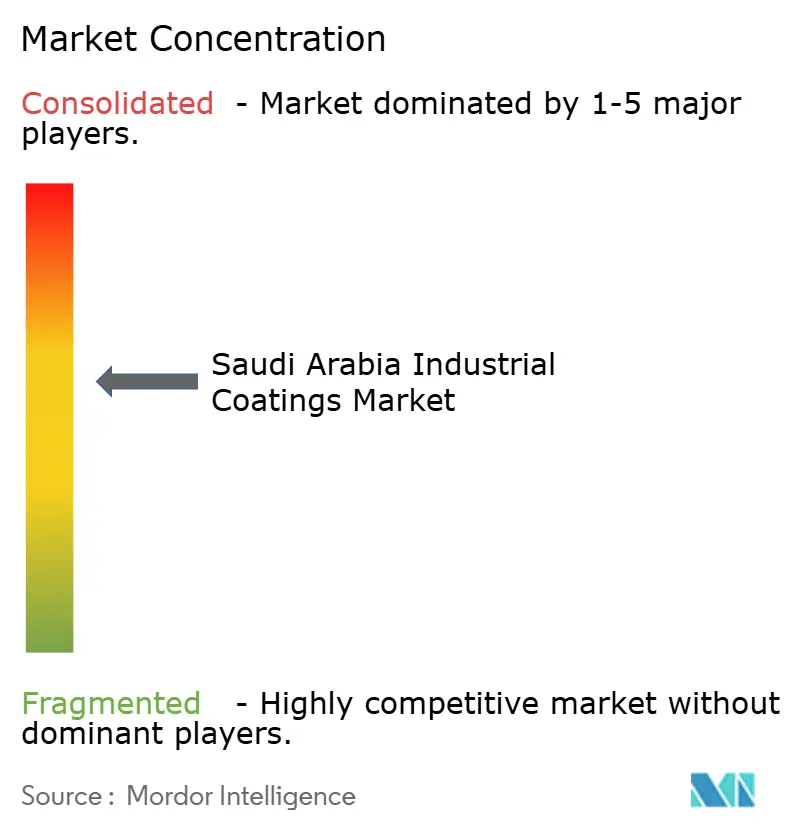

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Industrial Coatings Market Analysis by Mordor Intelligence

The Saudi Arabia Industrial Coatings Market size is expected to grow from USD 293.18 million in 2025 to USD 304.47 million in 2026 and is forecast to reach USD 367.9 million by 2031 at 3.85% CAGR over 2026-2031. Continued industrial diversification under Vision 2030, a pipeline of giga-projects, and tightening SASO environmental norms have amplified demand for high-performance protective and specialty systems. Rapid downstream capacity additions, localization of automotive production in the King Salman Automotive Cluster, and widespread adoption of automated application methods further accelerate market expansion. International suppliers leverage global research and development to meet increasingly stringent specifications, while local producers scale up their capacity to provide cost-competitive supply. Raw-material price volatility and a shortage of certified applicators are the principal near-term challenges.

Key Report Takeaways

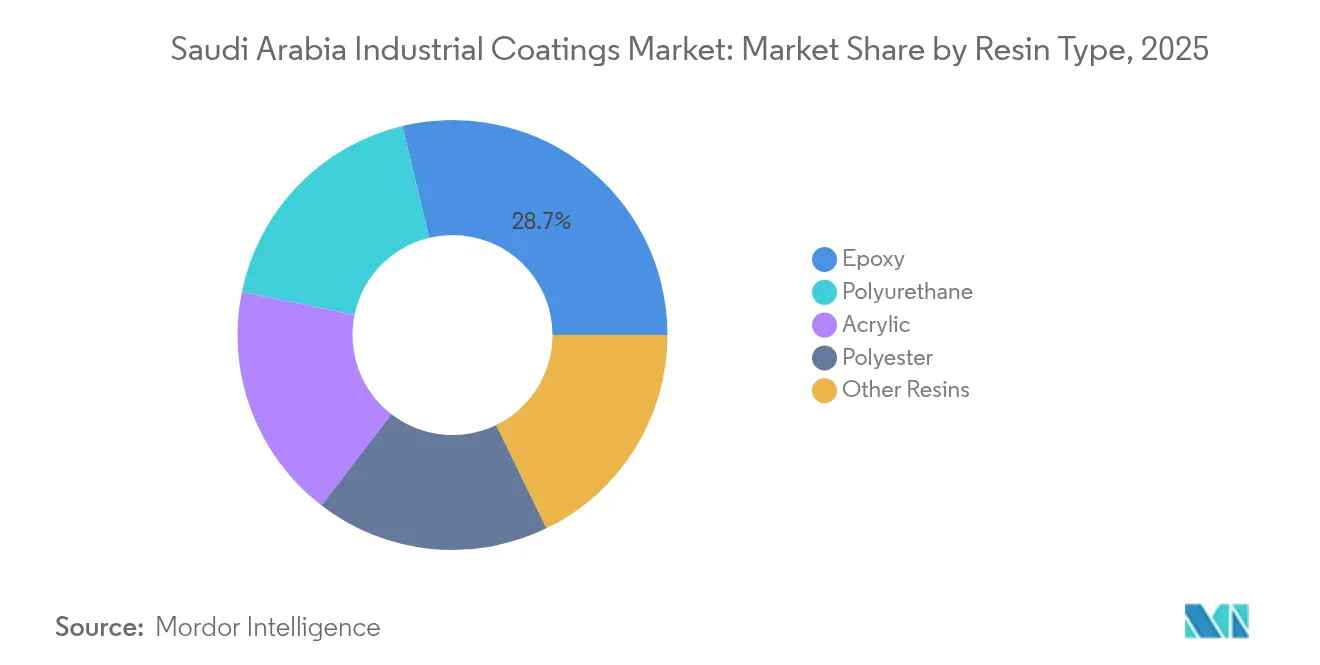

- By resin type, epoxy led the Saudi Arabia industrial coatings market with a 28.74% share in 2025, whereas polyurethane resins are forecast to grow at a 3.92% CAGR through 2031.

- By technology, solvent-borne products commanded 36.21% of the Saudi Arabian industrial coatings market share in 2025; water-borne systems are projected to expand at a 4.31% CAGR through 2031.

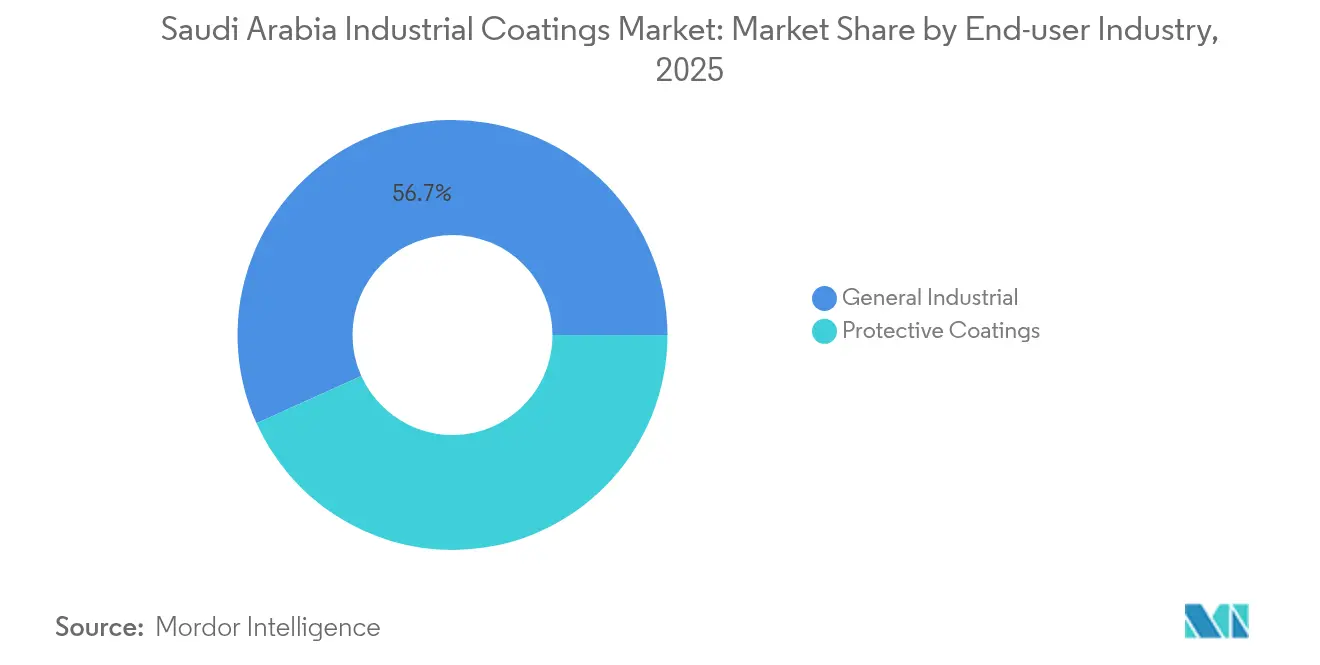

- By end-user industry, general industrial applications accounted for a 56.74% share of the Saudi Arabia industrial coatings market size in 2025 and are projected to advance at a 4.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Industrial Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-projects pipeline | +1.2% | National, with early gains in NEOM, Red Sea, Qiddiya | Medium term (2-4 years) |

| Rapid expansion of oil-and-gas downstream maintenance cycles | +0.8% | Eastern Province core, spill-over to Jubail Industrial City | Short term (≤ 2 years) |

| Localization of automotive manufacturing and parts under NIDLP | +0.6% | Central Region focus, King Salman Automotive Cluster | Medium term (2-4 years) |

| Tightening SASO/SABER compliance favouring high-performance, low-VOC systems | +0.5% | National | Short term (≤ 2 years) |

| Surge in offshore wind / green-hydrogen assets needing specialty coatings | +0.4% | NEOM, Red Sea coastal areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Projects Drive Unprecedented Coating Specifications

Landmark projects, including NEOM, The Red Sea Project, and Qiddiya, shape the Saudi Arabian industrial coatings market. NEOM’s masterplan needs coatings that withstand desert heat above 50 °C while delivering architectural aesthetics for The Line’s mirrored façades. Marine-grade, coral-safe systems are now mandatory at The Red Sea Project, while fire-resistant and anti-graffiti layers protect Qiddiya’s entertainment venues. Contractors have moved to robotic spray lines and automated film-thickness scanners to meet large-scale delivery schedules.

Oil and Gas Downstream Expansion Accelerates Protective Demand

Saudi Aramco’s gas program and SABIC integration have increased call-offs for protective coatings on new processing trains, storage tanks, and offshore pipelines. Aramco’s SAES standards specify epoxy and polyurethane systems with Level 1 and Level 2 inspection oversight, compelling suppliers to certify products for each service environment[1]Arab News, “Petrochemical Growth Accelerates with Vision 2030,” arabnews.com . Hydrogen and offshore wind ventures at NEOM require coatings that resist hydrogen embrittlement and salt-spray corrosion for 25-year lifecycles.

NIDLP Automotive Localization Creates New Supply Chains

Lucid Motors plans to assemble vehicles, and the Ceer-Foxconn joint venture expands component lines in Riyadh. The shift necessitates OEM-grade primers, basecoats, and clearcoats formulated for Gulf Coast climates, plus battery-housing coatings that provide thermal and EMI shielding. Local content mandates encourage international paint majors to license technology or establish plants in partnership with Saudi companies.

SASO Compliance Drives High-Performance, Low-VOC Adoption

The 2024 Product Safety Law imposes fines and permits criminal liability for unsafe products. Manufacturers are rapidly reformulating to water-borne or high-solids chemistries that meet VOC caps while maintaining corrosion performance. Global players gain an edge through certified labs and traceable quality control, whereas smaller suppliers face costly upgrades[2]Human Resource and Social Development, “Procedural Guide for Engineering Profession Saudization,” hrsd.gov.sa .

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy anti-dumping duties on TiO₂ and coated aluminium raising raw-material costs | -0.7% | National | Short term (≤ 2 years) |

| Acute shortage of certified applicators and inspectors for Aramco standards | -0.4% | Eastern Province, industrial clusters | Medium term (2-4 years) |

| Stricter New Product-Safety Law penalties elevating compliance costs | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Anti-Dumping Duties Escalate Raw-Material Costs

New trade remedies on imported titanium dioxide, coated aluminum, and PVC-coated fabrics inflate pigment and substrate expenses, as TiO₂ accounts for a significant portion of formulation cost. Domestic producer Tasnee explores backward integration to cushion volatility, yet near-term margins remain under pressure.

Certified Applicator Shortage Constrains Quality Assurance Capacity

Only a limited pool of Level 1 and Level 2 inspectors meets Aramco criteria, triggering project delays and rework. With the Kingdom projected to lack skilled workers by 2030, companies are investing in in-house vocational programs, such as Jazeera Paints Academy, although industry-wide uptake is slower than demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Polyurethane Challenge

Epoxy retained a 28.74% share of the Saudi Arabia industrial coatings market in 2025, underpinned by its widespread use on offshore rigs, storage spheres, and cross-country pipelines. The Saudi Arabia industrial coatings market size for epoxy systems is forecast to expand steadily as Aramco’s gas processing units are commission through 2031. Polyurethane registers the fastest 3.92% CAGR, propelled by demand for UV-resistant finishes on NEOM’s iconic landmarks and flexible weatherproof membranes on The Red Sea Project. Local formulators increasingly blend high-solids polyurethane hybrids to balance compliance and performance, while acrylics and polyesters maintain niche roles in coil and appliance lines.

The segment landscape mirrors Vision 2030 diversification. High-film-build epoxies protect corrosive petrochemical reactors, whereas elastomeric polyurethanes coat entertainment parks and lightweight bridge decks. International vendors differentiate themselves via amine-accelerated epoxies that cure at temperatures below 10 °C, ideal for winter shutdowns in Tabuk, while Saudi firms highlight low-temperature cure polyurethanes suited for modular onsite fabrication.

By Technology: Water-Borne Systems Gain Despite Solvent Leadership

Solvent-borne chemistries held a 36.21% share in the Saudi Arabia Industrial Coatings Market in 2025 due to their entrenched performance in abrasive offshore and refinery conditions. The Saudi Arabia industrial coatings market size for solvent-borne protective grades continues to grow alongside petrochemical debottlenecking, yet water-borne alternatives now log a 4.31% CAGR. SASO’s VOC thresholds and penalties under the Product Safety Law spur rapid switchovers in general industrial and OEM lines.

Powder coatings benefit from 0-VOC profiles and reclaim efficiency, finding traction in appliance shells and electric-vehicle chassis. UV-cure and high-solids systems target electronics, packaging, and 3-D-printed parts, though uptake remains niche due to capital outlays for curing units. Equipment suppliers report a rise in orders for robotic booths that can interchange between wet and powder lines in the same cell, reflecting hybrid production strategies at automotive tier suppliers.

By End-User Industry: General Industrial Applications Lead Growth

General industrial users accounted for 56.74% of demand in 2025 and are projected to rise at a 4.07% CAGR through 2031. Factory expansions across construction materials, consumer durables, and packaging sustain steady call-offs for primers, enamels, and maintenance topcoats. Protective oil-and-gas coatings follow mega-project cycles but remain the single largest high-value subsegment. Renewable power, including green hydrogen units at NEOM, necessitates specialized anti-hydrogen and anti-sparking layers.

Infrastructure projects, such as the Riyadh Metro, high-speed rail, and cross-kingdom bridges, prefer low-maintenance fluoropolymer-modified systems. Mining operations in the Northern Province spur abrasion-resistant linings for haul trucks and ore crushers. Together, these diversified outlets reduce reliance on upstream hydrocarbon spending and sustain a balanced volume base.

Geography Analysis

The Eastern Province contributed a significant portion of Saudi Arabia's industrial coatings market share in 2025, primarily driven by Jubail’s chemical plants. The region's growth rides on Aramco’s gas expansion, SABIC’s new polypropylene trains, and maritime yard upgrades along the Arabian Gulf. Tank farms, LNG terminals, and offshore jackets dominate protective demand, while maintenance repaint cycles align with five-year turnaround schedules.

Vision 2030 programs have earmarked significant value for mixed-use, transit, and manufacturing complexes, pushing volume for architectural primers, steelwork coatings, and OEM automotive finishes. The King Salman Automotive Cluster catalyzes new coil-coating lines for aluminum body panels and plastic parts requiring specialty primers compatible with EV batteries.

The Red Sea Project and NEOM’s coastal megastructures drive marine-grade and UV-stable coatings, while Jeddah’s logistics hub triggers demand for warehouse floor epoxies and container coatings. Northern and Southern provinces remain nascent, but mining concessions and border infrastructure provide future upside, particularly for abrasion-resistant and heat-reflective technologies in arid terrains.

Competitive Landscape

The Saudi Arabia Industrial Coatings Market is moderately consolidated. Global firms leverage research and development, as well as ISO-certified product lists compliant with SAES and SABER, to secure flagship contracts at NEOM and Aramco refineries. Each operates regional plants or toll blends in Dammam to satisfy Saudi content mandates. Product differentiation hinges on Gulf-climate durability, low-VOC formulations, and digital application aids. Leading firms are piloting drone-enabled surface inspection and AR-guided spraying to reduce labor bottlenecks. Niche disruptors develop graphene-enhanced barriers for hydrogen pipelines and single-coat polyurethanes with salt-fog resistance. Procurement teams at mega-projects weigh lifecycle cost, SAES prequalification, and local-content scorecards ahead of award decisions, giving agile domestic producers room to capture mid-tier packages while multinationals secure complex turnkey scopes.

Saudi Arabia Industrial Coatings Industry Leaders

Jotun

AkzoNobel N.V.

Al-Jazeera Paints

PPG Industries Inc.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SIPCO (Saudi Industrial Paint Company) has completed the acquisition of Premium Paints Company to boost local capacity and broaden its industrial and decorative portfolio.

- March 2024: Sherwin-Williams unveiled Repacor SW-1000, a 100%-solids repair coating certified to NORSOK M-501 for offshore wind steel structures.

Saudi Arabia Industrial Coatings Market Report Scope

The Saudi Arabia Industrial Coatings Market report includes:

By Resin Type

| Epoxy |

| Polyurethane |

| Acrylic |

| Polyester |

| Other Resins (Alkyd, Fluoropolymer) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies (UV-/EB-Cured and High Solids) |

By End-user Industry

| General Industrial | |

| Protective Coatings | Oil and Gas |

| Power Generation | |

| Infrastructure | |

| Mining | |

| Other Protective Coatings |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Polyester | ||

| Other Resins (Alkyd, Fluoropolymer) | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder Coatings | ||

| Other Technologies (UV-/EB-Cured and High Solids) | ||

| By End-user Industry | General Industrial | |

| Protective Coatings | Oil and Gas | |

| Power Generation | ||

| Infrastructure | ||

| Mining | ||

| Other Protective Coatings | ||

Key Questions Answered in the Report

How large is the Saudi Arabian industrial coatings market in 2026?

It is valued at USD 304.47 million and is projected to grow at a 3.85% CAGR to 2031.

Which resin type currently dominates demand?

Epoxy systems lead with 28.74% share due to extensive use in petrochemical protection.

What is driving the shift toward water-borne technologies?

SASO VOC limits and the 2024 Product Safety Law push manufacturers toward low-emission formulations.

Who are the key suppliers?

Jotun, AkzoNobel N.V., Al-Jazeera Paints, PPG Industries Inc., and The Sherwin-Williams Company are major players in the market.

What challenges threaten near-term growth?

TiO₂ anti-dumping duties raise raw-material costs, and a shortage of certified applicators delays project execution.

Page last updated on: