Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

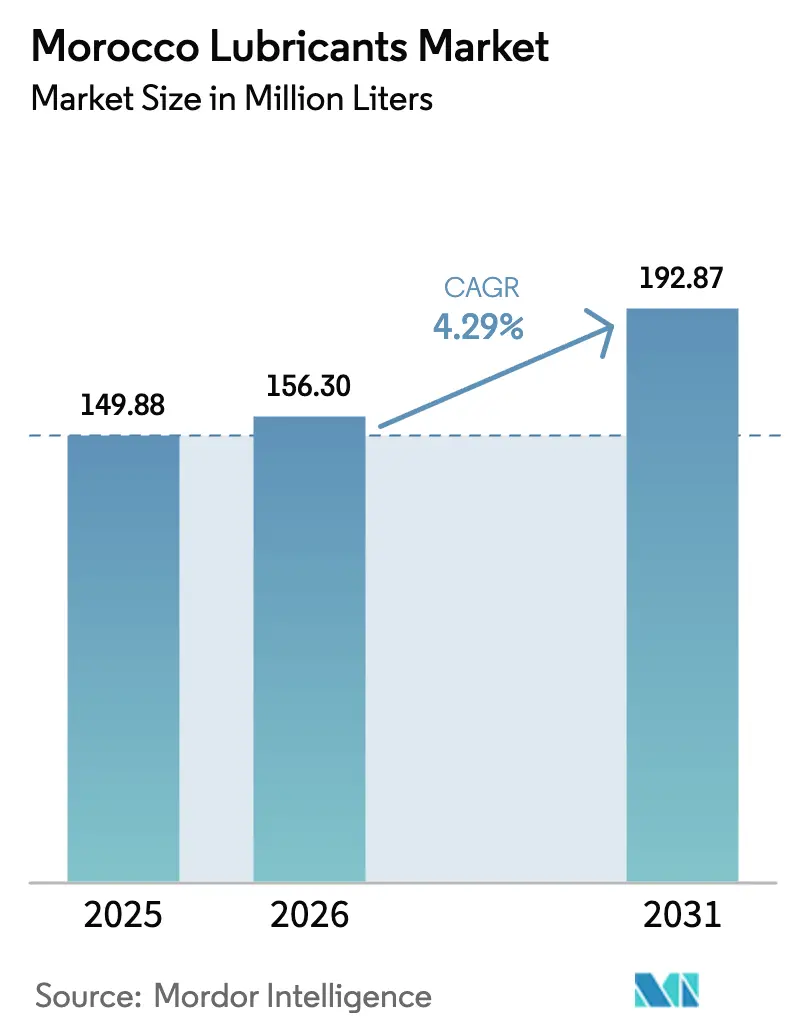

| Base Year Market Size (2025) | 149.88 Million liters |

| Market Volume (2026) | 156.30 Million liters |

| Market Volume (2031) | 192.87 Million liters |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

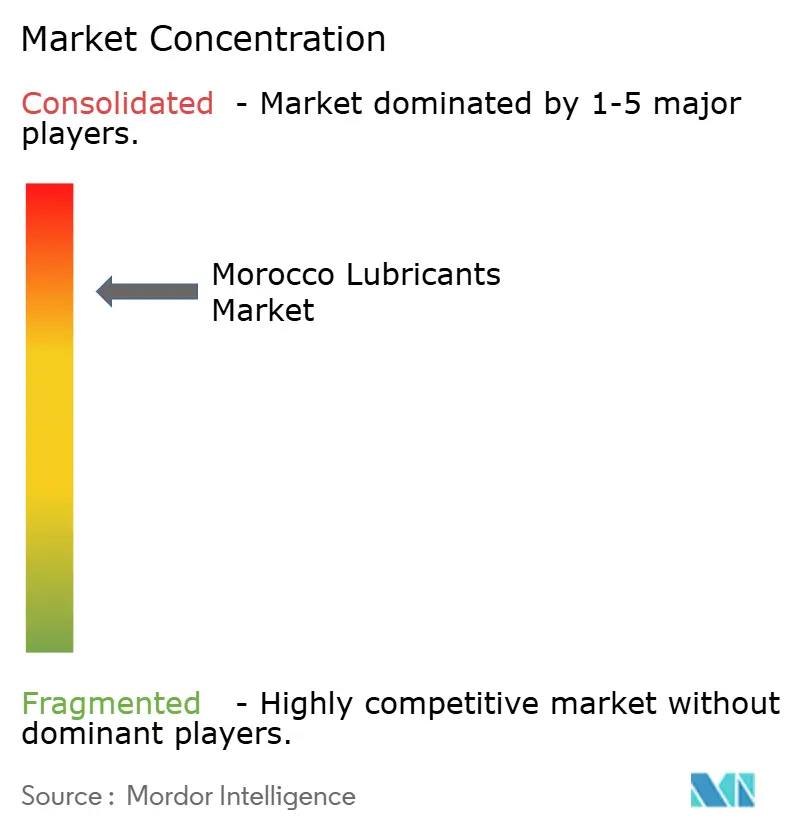

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Lubricants Market Analysis by Mordor Intelligence

The Morocco Lubricants Market size is projected to be 149.88 Million liters in 2025, 156.30 Million liters in 2026, and reach 192.87 Million liters by 2031, growing at a CAGR of 4.29% from 2026 to 2031. The steady ascent is linked to the scale-up of local automotive output, the roll-out of Euro 6/VI fuel standards, and multibillion-dollar green-energy investments that expand specialty-fluid demand. Factory-fill volumes climb as Stellantis and Renault lift installed capacity, while low-SAPS synthetics gain ground in both the factory and aftermarket because ultra-low-sulfur diesel now dominates retail pumps. Parallel spending on 5 GW of renewable power, a 1 GW green-hydrogen complex, and a 1,500 km high-speed-rail build-out anchors long-cycle demand for turbine oils, hydraulic fluids, and biodegradable greases. Market concentration remains high: the three largest suppliers jointly hold just under half of the Morocco lubricants market and differentiate through blending scale, OEM tie-ups, and digital service tools.

Key Report Takeaways

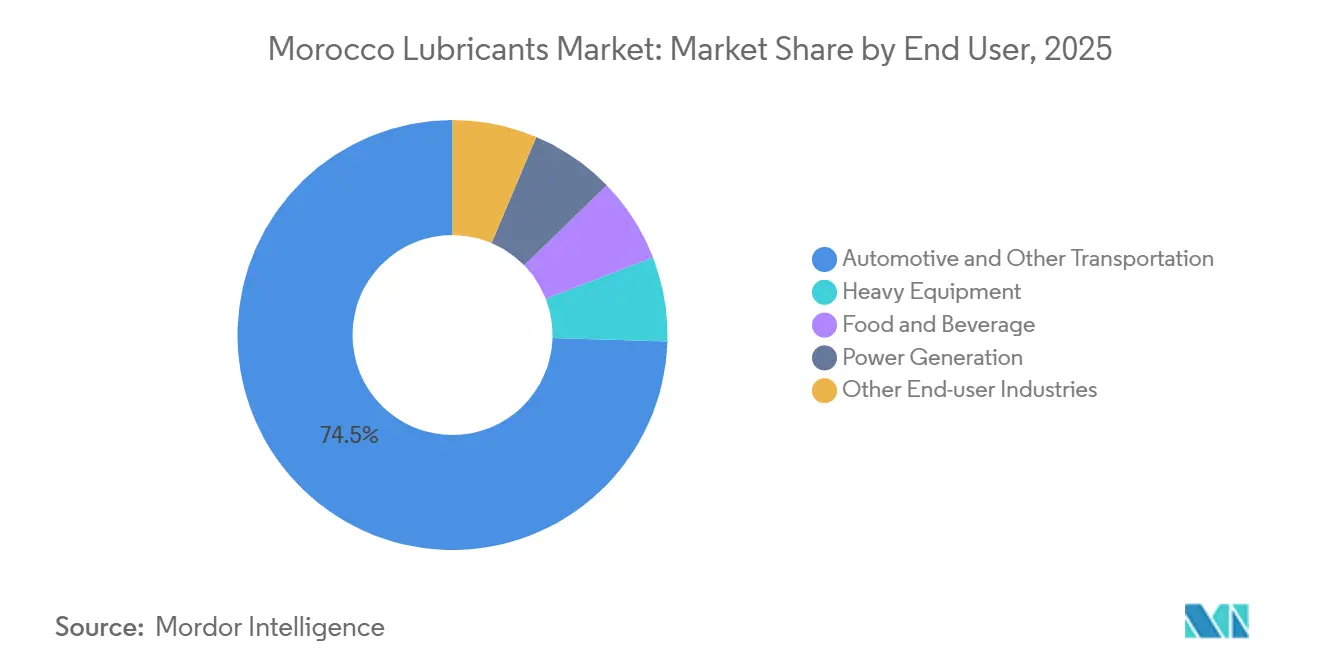

- By end user, automotive and other transportation led with 74.51% of the Morocco lubricants market share in 2025 and is expanding at a 6.10% CAGR through 2031.

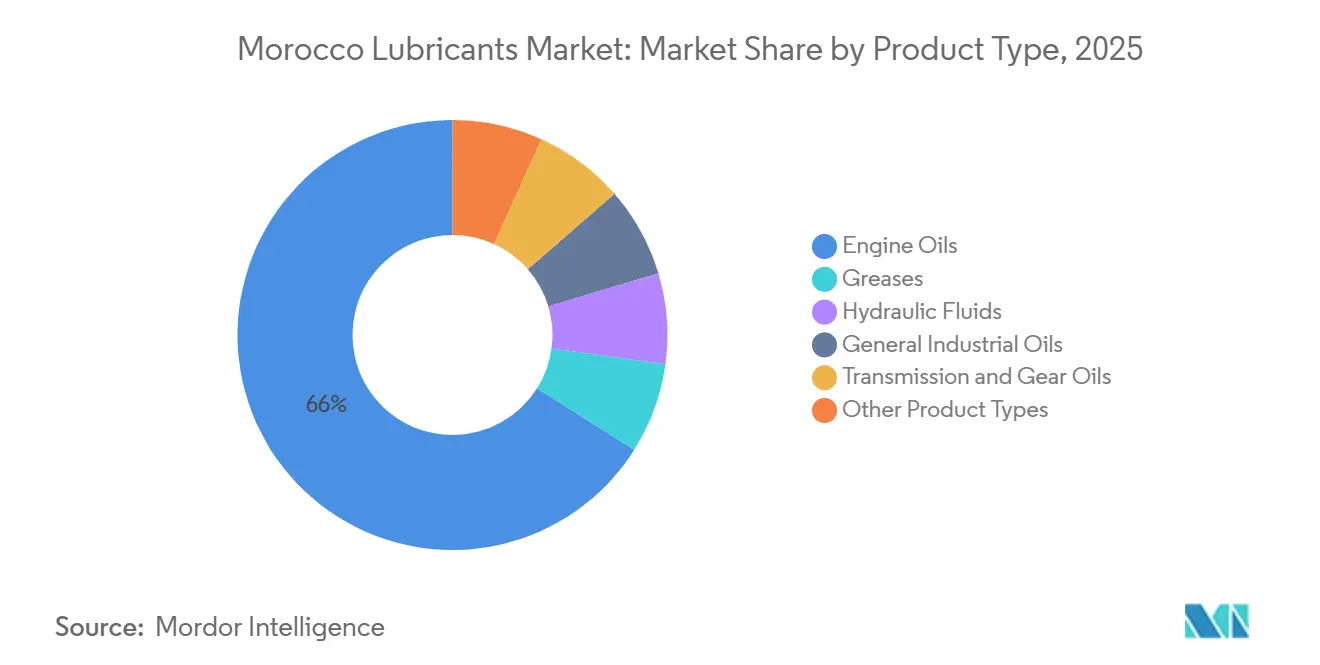

- By product type, greases are projected to post the fastest 5.38% CAGR, although engine oils continue to command 66.04% of the Morocco lubricants market size in 2025

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of Morocco's OEM automotive production hubs | +0.8% | National, concentrated in Tanger-Tétouan-Al Hoceima and Casablanca-Settat | Medium term (2–4 years) |

| Continued infrastructure and mining investments driving heavy-equipment lubricant demand | +1.2% | National, with highest intensity in Khouribga-Jorf Lasfar, Gantour-Meskala-Safi, Tarfaya-Boucraa-Laayoune, and Al Boraq rail corridor | Long term (≥4 years) |

| Growing shift toward premium synthetics as vehicle parc modernises | +0.9% | National, early gains in Casablanca, Rabat, Marrakech urban centers | Medium term (2–4 years) |

| Government fuel-quality upgrades mandating low-sulfur, higher-spec lubricants | +0.7% | National | Short term (≤2 years) |

| Planned green-hydrogen megaprojects creating demand for specialty fluids | +0.5% | Regional, concentrated in coastal zones (Chbika, Dakhla) and OCP industrial complexes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Morocco's OEM Automotive Production Hubs

In 2024, Morocco produced vehicles, with ongoing plant expansions set to increase capacity significantly. This surge in production directly boosts the demand for factory-fill engine oils, transmission fluids, and assembly greases. Notably, Stellantis's upgrade is set to increase its engine output. Meanwhile, Renault is ramping up its hybrid initiatives, highlighted by the launch of a new engineering center. Each additional line incorporates high-precision stamping presses, machining centers, and paint booths that consume hydraulic oils, cutting fluids, and heat-transfer media. EV and hybrid output also introduces niche requirements such as ester-based dielectric coolants and ultra-low-friction wheel-bearing greases. Collectively, these factors keep the Morocco lubricants market on a firm upward trajectory despite efficiency gains.

Continued Infrastructure and Mining Investments Driving Heavy-Equipment Lubricant Demand

OCP is channeling significant investments into its Green Investment Program, aiming to ramp up fertilizer production by 2027[1]OCP Group, “OCP Green Investment Program,” ocpgroup.ma. This initiative also sees the installation of renewable energy across three major mining corridors. As a result, there's a secured long-term demand for hydraulic and gear oils, essential for excavators, haul trucks, and conveyors. In tandem, a rail strategy is broadening the Al Boraq network, while the Dakhla Atlantic Port is now under construction. Every step, from concrete pouring and rail welding to dredging, is dependent on biodegradable hydraulics and extreme-pressure greases that meet ISO 15380 standards. Additionally, wind and Concentrated Solar Power (CSP) plants in Ouarzazate are introducing turbine oils and synthetic heat-transfer fluids, expanding Morocco's lubricants market reach beyond just passenger vehicles.

Growing Shift Toward Premium Synthetics as Vehicle Parc Modernizes

With the introduction of Euro 6 vehicles and the use of 10 ppm diesel fuel, longer drain intervals are now achievable. This advancement is driving a notable shift towards fully synthetic, low-SAPS formulations. TotalEnergies’ Quartz 9000 range, now validated to ACEA C3, delivers improved fuel economy over its predecessor[2]TotalEnergies, “Quartz Product Range,” totalenergies.ma . Shell, in collaboration with Vivo Energy, has launched the Helix Ultra, boasting API SP and a host of OEM approvals. Meanwhile, Afriquia is scaling local blending runs, targeting West Africa's export markets with its Chevron-sourced Delo and Havoline lines. As synthetic formulations gain traction, they elevate the average unit value in Morocco's lubricants market, despite a slight dip in per-vehicle volumes.

Government Fuel-Quality Upgrades Mandating Low-Sulfur, Higher-Spec Lubricants

Order 1948-21 lowered national diesel sulfur starting January 2023, paving the way for particulate filters and selective catalytic reduction on new trucks. Lubricant blenders must therefore formulate ACEA C2/C3 oils with reduced sulfated ash to prevent after-treatment fouling. IMANOR certification and spot inspections, aided by a Climate and Clean Air Coalition technical-assistance grant, tighten compliance across retail channels. The new regime accelerates the substitution of legacy mineral grades, expanding the value share of synthetics within the Morocco lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent counterfeit/sub-standard lubricant trade | -0.5% | National, with higher incidence in informal retail channels | Short term (≤2 years) |

| Accelerating EV and hybrid penetration in urban centres | -0.6% | Urban centers: Casablanca, Rabat, Marrakech, Tangier | Medium term (2–4 years) |

| Tightening waste-oil disposal rules raising compliance costs | -0.4% | National, with stricter enforcement in industrial zones (Casablanca-Settat, Tanger Med) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Counterfeit/Sub-Standard Lubricant Trade

OECD research flags Morocco as a provenance economy for counterfeit goods entering the EU, and similar informal networks distribute non-spec oils domestically, undercutting reputable brands. Sub-standard blends shorten engine life, erode consumer trust, and compress legitimate distributors’ margins. While Afriquia rebranded stations and introduced loyalty programs to signal authenticity, rural channels still escape routine lab testing. Enhanced border inspections and stiffer penalties are essential to safeguard the Morocco lubricants market’s premium tier.

Accelerating EV and Hybrid Penetration in Urban Centers

In 2024, Morocco registered a small EV fleet. However, this number is set to grow significantly in the coming years, supported by the establishment of a battery gigafactory. Pure electric vehicles (EVs) have eliminated the demand for engine oil, leading to a substantial reduction in total fluid consumption per vehicle. Meanwhile, hybrid vehicles have managed to cut annual oil changes. While there's a rise in specialized dielectric and thermal-management fluids, their volumes remain limited. This is expected to continue until EV penetration in the market surpasses a significant threshold—a milestone not anticipated before the late 2020s. This delay poses a medium-term challenge for Morocco's lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Automotive Dominance Masks Emerging Industrial Complexity

Automotive and other transportation represented 74.51% of the Morocco lubricants market share in 2025, and the segment is on track for a 6.10% CAGR to 2031, buoyed by record vehicle exports and rising fleet maintenance needs. Factory-fill requirements expand in tandem with OEM capacity, while aftermarket demand benefits from a passenger-car parc. Yet a deeper reading shows heavy equipment, though smaller, outpaces headline growth as OCP ramps conveyor installations and the rail-port build refreshes demand for hydraulic and gear oils.

Second-order effects widen the industrial user base. Power producers purchase turbine and transformer oils as renewable capacity climbs, and food processors convert to NSF H1-certified greases for export compliance. Collectively, these shifts lift the Morocco lubricants market size for non-automotive consumers, even as per-vehicle usage shows a gradual decline.

By Product Type: Engine Oils Lead, Greases Accelerate on Mining and EV Demand

Engine oils retained 66.04% of the Morocco lubricants market size in 2025, but their CAGR lags the overall market because electrification and extended oil-drain intervals erode volume per asset. Greases, in contrast, post a 5.38% CAGR through 2031, fueled by high-load conveyors in phosphate mines and by wind-turbine main bearings that require calcium-sulfonate complexes rated NLGI 2.

Hydraulic fluids capitalize on sustained capex in open-pit mines and civil-works machinery, whereas specialty oils such as heat-transfer fluids record double-digit growth inside CSP plants and battery-cell coating lines. This nuanced mix signals a pivot from high-volume, lower-margin SKUs to targeted, higher-value chemistries inside the broader Morocco lubricants market.

Geography Analysis

Casablanca-Settat captured a significant share of lubricant demand thanks to its dense cluster of automotive assembly, chemical fabrication, and offshore finance that concentrates vehicle parc and industrial activity. The corridor hosts Afriquia’s primary blending site and TotalEnergies’ lube plant, facilitating just-in-time deliveries to OEMs and fleets.

Tanger-Tétouan-Al Hoceima, home to Renault’s Tangier plant and Africa’s largest container port, is a key region by growth rate. The free-zone logistics chain pulls in marine lubricants for ship-to-shore cranes and biodegradable hydraulic oils for port reach-stackers. Hybrid and EV assembly lines under the 2025 Renault accord will further diversify lubricant needs, cementing the region as a fast-rising pole within the Morocco lubricants market.

Marrakech-Safi and the southern mining corridor contribute a smaller base yet register notable gains as OCP’s Green Investment Program unfolds. New high-speed rail links and the Dakhla Atlantic Port extend commercial reach, meaning specialty fluids for construction equipment and ammonia synthesis units will disperse beyond core coastal hubs. The geographic profile of the Morocco lubricants market is therefore evolving from a Casablanca-centric model to a multi-node network anchored by automotive, mining, logistics, and renewable-energy clusters.

Competitive Landscape

The Morocco Lubricants Market is consolidated. Afriquia draws on Chevron’s Delo and Havoline technology and exports to 14 African states, leveraging ISO 9001 blending lines in Jorf Lasfar. Mid-tier entrants compete on niche chemistries or regional distribution, often importing finished goods rather than blending locally. Digitalization is a secondary battleground. Vivo’s predictive LubeAnalyst reduces unscheduled downtime for mining fleets, while TotalEnergies’ QR-code traceability counters counterfeit infiltration. These tech advances, combined with widening synthetic portfolios, allow leading suppliers to protect their share even as the Morocco lubricants market fragments under e-commerce and cross-border import pressure.

Morocco Lubricants Industry Leaders

TotalEnergies

Afriquia

Shell Plc

OLA Energy

FUCHS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP Plc initiated a sale process for its Castrol division, valued at up to USD 10 billion, signaling potential changes in regional supply agreements that currently include Morocco.

- May 2025: TotalEnergies launched next-generation engine oils meeting API SQ and ILSAC GF-7, including Quartz 9000 Future FGC 5W-30, designed for turbocharged and GDI engines.

Morocco Lubricants Market Report Scope

Lubricants, substances designed to manage friction, play a pivotal role in reducing wear between surfaces in relative motion. Beyond merely minimizing friction, these versatile agents can dissipate heat, remove wear debris, introduce additives at contact points, transmit power, and offer protection and sealing capabilities.

The Morocco lubricants market is segmented by end user and product type. By end user, the market is segmented into automotive and other transportation, heavy equipment, food and beverage, power generation, and other end-user industries. By product type, the market is segmented into engine oils, greases, hydraulic fluids, general industrial oils, transmission and gear oils, and other product types. For each segment, the market sizing and forecasts have been done based on revenue (Litres).

By End User

| Automotive and Other Transportation |

| Heavy Equipment |

| Food and Beverage |

| Power Generation |

| Other End-user Industries |

By Product Type

| Engine Oils |

| Greases |

| Hydraulic Fluids |

| General Industrial Oils |

| Transmission and Gear Oils |

| Other Product Types |

| By End User | Automotive and Other Transportation |

| Heavy Equipment | |

| Food and Beverage | |

| Power Generation | |

| Other End-user Industries | |

| By Product Type | Engine Oils |

| Greases | |

| Hydraulic Fluids | |

| General Industrial Oils | |

| Transmission and Gear Oils | |

| Other Product Types |

Key Questions Answered in the Report

How big is the Morocco lubricants market?

It reached 156.30 million liters in 2026 and is forecast to climb to 192.87 million liters by 2031.

What CAGR is projected for Morocco’s lubricant demand through 2031?

The market is expected to register a 4.29% CAGR from 2026 to 2031, led by automotive factory-fill and mining equipment needs.

Which end-user group consumes the most lubricants?

Automotive and other transportation account for 74.51% of total volume and are still growing at 6.10% per year.

Why are synthetic lubricants gaining share?

Euro 6 fuel standards, longer drain intervals, and OEM approvals are pushing buyers toward low-SAPS, fully synthetic oils.

How is electrification affecting lubricant suppliers?

EVs cut traditional engine-oil volumes, but they open smaller niches in dielectric coolants and thermal-management fluids, prompting suppliers to diversify.

Page last updated on: