Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

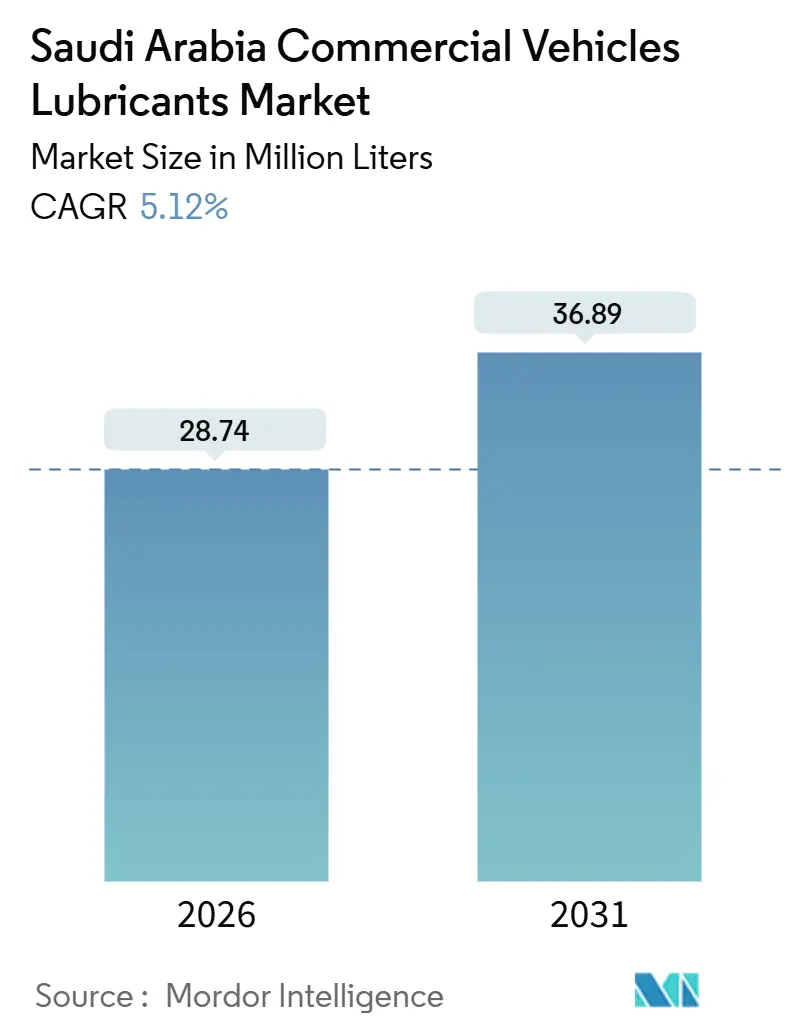

| Market Volume (2026) | 28.74 Million liters |

| Market Volume (2031) | 36.89 Million liters |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Commercial Vehicles Lubricants Market Analysis by Mordor Intelligence

The Saudi Arabia Commercial Vehicles Lubricants Market size is estimated at 28.74 million liters in 2026, and is expected to reach 36.89 million liters by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). Record infrastructure awards support growth under Vision 2030, logistics densification that keeps heavy-duty vehicles moving year-round, and a steady shift toward synthetic formulations engineered for desert operating temperatures above 50 °C. Seasonal pilgrimage peaks, the rise of predictive-maintenance contracts that lock in premium multi-year volumes, and Aramco’s downstream push after the Valvoline acquisition have intensified competition, widened service expectations, and reduced supplier lead times. At the same time, electrification of last-mile fleets and public buses is starting to flatten long-run engine oil volumes, forcing suppliers to diversify into driveline fluids, battery coolants, and greases.

Key Report Takeaways

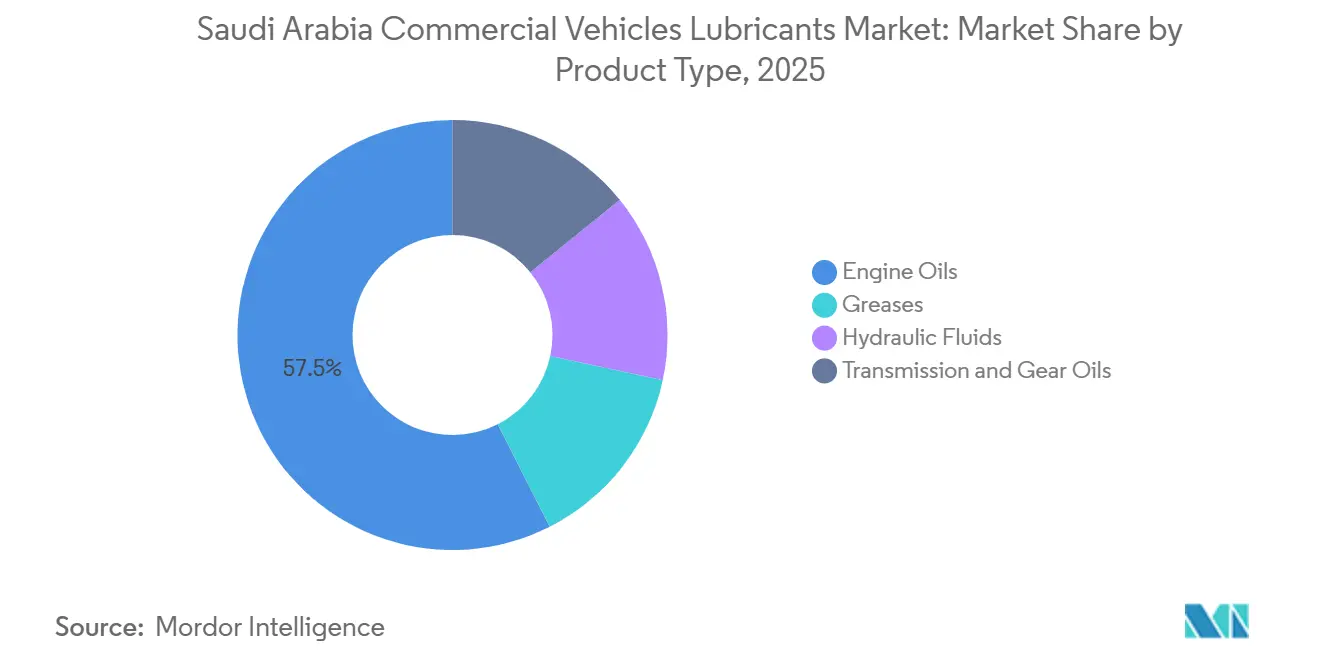

- By product type, engine oils held 57.46% of the Saudi Arabian commercial vehicles lubricants market share in 2025, while transmission and gear oils are forecast to expand at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Commercial Vehicles Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure megaprojects under Vision 2030 fueling construction and fleet lubricant demand | +1.2% | National, with concentration in Riyadh, NEOM, Jeddah, and Eastern Province industrial zones | Medium term (2-4 years) |

| Booming logistics/e-commerce miles increasing lubricant consumption intensity | +0.9% | National, with urban density in Riyadh, Jeddah, Dammam driving last-mile delivery growth | Short term (≤ 2 years) |

| Shift toward synthetic HDDEO for extended drain intervals in extreme desert climate | +0.7% | National, particularly high-temperature regions (Rub' al Khali, Northern Border Province) | Long term (≥ 4 years) |

| Seasonal Hajj-Umrah pilgrimage peaks creating predictable bus-fleet maintenance cycles | +0.5% | Western Province (Mecca, Medina, Jeddah), with spillover to national coach operators | Short term (≤ 2 years) |

| Digital predictive-maintenance adoption driving premium bundled lubricant contracts | +0.6% | National, with early adoption by large logistics fleets (DHL, Aramex, FedEx) and public-transport operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Megaprojects Under Vision 2030 Fueling Construction and Fleet Lubricant Demand

Saudi Arabia’s construction pipeline between 2023 and 2030 is mobilizing thousands of haul trucks, excavators, and concrete mixers that collectively consume large volumes of engine oils, hydraulic fluids, and greases each year[1]Saudi Aramco, “Aramco and ExxonMobil Sign JV Framework Agreement for Samref VFA,” aramco.com. NEOM’s 170-kilometer linear city, the Amiral petrochemical complex at Jubail, and the Samref VFA expansion at Yanbu each deploy equipment that operates almost continuously in ambient temperatures exceeding 45 °C, shortening drain intervals and demanding oxidation-stable synthetics. The planned logistics centers designed to lift non-oil GDP further amplify truck density and extend operating hours for forklifts and yard tractors. Local blenders that secure Group II/III base-oil supply through Luberef’s new Yanbu train have begun shortening customer lead times from weeks to days, capturing fleet renewals tied to civil-works contracts. Together, these projects cement a multi-year uplift in Saudi Arabia's commercial vehicles lubricants market demand, especially for heavy-duty diesel engine oils and shock-load hydraulic fluids.

Booming Logistics and E-Commerce Miles Increasing Lubricant Consumption Intensity

The national freight and logistics sector is set to grow, driven by rising expectations for same-day deliveries and enhanced cross-border ties with Gulf ports. Major players like Aramex, Ajex (backed by DHL), and FedEx are broadening their hub-and-spoke networks, boasting a combined fleet of vehicles. Notably, many of these vehicles still depend on diesel engines for their long-haul journeys. Every additional mile driven by these fleets translates directly to lubricant consumption. Telematics data reveals a shift: urban vans now cover greater distances daily. While pilot initiatives, like Aramex's electric Farizon 8-tonner, hint at a forthcoming shift, the pace of this transition remains slow. As a result, the Saudi Arabian market for commercial vehicle lubricants continues to be closely tied to traditional internal combustion cycles throughout the forecast period.

Shift Toward Synthetic HDDEO for Extended Drain Intervals in Extreme Desert Climate

Field tests in the Empty Quarter reveal that Group III-based 5W-40 synthetics outlast mineral 15W-40 by retaining viscosity and total base number longer[2]Luberef, “Luberef Awards EPC Contract for Yanbu Refinery Expansion Project,” luberef.com.sa. This advancement enables fleets to extend oil drains without surpassing iron wear thresholds. Blenders are capitalizing on the new Yanbu base-oil train to produce premium HDDEO grades locally. This shift reduces reliance on imports from Singapore and South Korea, effectively curbing currency-related price fluctuations. While these premium oils carry a price markup over their mineral counterparts, a comprehensive total cost of ownership analysis reveals net savings when accounting for diminished downtime and fewer filter purchases. This economic advantage is propelling adoption among organized fleets that emphasize whole-life cost considerations.

Seasonal Hajj–Umrah Pilgrimage Peaks Creating Predictable Bus-Fleet Maintenance Cycles

During the 2025 Hajj season, a fleet of buses and taxis, bolstered by mobile workshops and tow trucks, operated over a concentrated four-week maintenance window. This effort consumed significant amounts of engine oil and transmission fluid. Hafil, servicing a large number of buses between Ramadan and Dhul-Hijjah, has led suppliers to strategically pre-position inventory in Jeddah and Medina. Although Mecca's newly introduced electric BRT fleet in late 2025 has diminished the demand for engine oil in urban shuttle routes, intercity coaches still rely on diesel. This ensures that the peaks of pilgrimage seasons continue to set a reliable volume floor for Saudi Arabia's commercial vehicle lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility and intense price competition squeezing margins | -0.8% | National, with spillover effects from global Brent crude pricing and OPEC+ production decisions | Short term (≤ 2 years) |

| Counterfeit and low-quality products eroding brand share and trust | -0.5% | National, with higher incidence in secondary distribution channels and independent workshops | Medium term (2-4 years) |

| Riyadh's 30% EV public-transport target gradually capping long-term engine-oil demand | -0.4% | Urban centers (Riyadh, Jeddah, Dammam), with national spillover as EV adoption accelerates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility and Intense Price Competition Squeezing Margins

Brent crude prices lingered at a stable level throughout 2025. This trend compressed base-oil spreads, compelling blenders to either absorb cost fluctuations or offer steep discounts in a market where brand loyalty frequently wavers. The arrival of a fully integrated Aramco–Valvoline entity has raised the stakes, as a state-backed supplier can underwrite promotions during soft quarters, pressuring independents to defend share with extended credit terms and bundled services rather than outright price cuts.

Counterfeit and Low-Quality Products Eroding Brand Share and Trust

In January 2024, the Ministry of Commerce confiscated counterfeit lubricant items. Despite this, smaller workshops along the Riyadh–Dammam corridor persist in stocking unverified oils, often undercutting branded prices. By the close of 2024, SASO’s Product Safety Program achieved compliance. However, with authentication labs facing capacity constraints, rogue distributors have found opportunities to exploit enforcement gaps. In response, genuine suppliers have introduced QR-coded packs, tamper-evident seals, and rigorous distributor audits. Yet, the challenge remains: rebuilding a tarnished brand equity is both costly and time-intensive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Volume, Transmission Fluids Lead Growth

Engine oils commanded 57.46% of the 2025 volume, driven by Saudi Arabia's fleet of trucks, buses, and vans. These vehicles operate in high-temperature, dusty conditions, leading to shorter drain intervals and busier service bays. The market for engine oils in Saudi Arabia's commercial vehicle lubricants sector is set to grow in the coming years, despite the encroaching influence of electrification. Fleet managers are increasingly opting for API CK-4 and OEM-licensed 5W-40 synthetics, not only to safeguard against warranty claims but also to benefit from longer service intervals, reducing downtime and filter purchases.

Transmission and gear oils, while accounting for a smaller absolute tonnage, are the fastest-growing line at a 6.18% CAGR. This growth is fueled by the rising adoption of automated manual and continuously variable transmissions in new long-haul tractors. Leading OEMs like Volvo, Daimler, and FAW are specifying API GL-5 and MT-1 fluids, known for their enhanced shear stability. In response, blenders are reformulating with synthetic base stocks to ensure gear protection at sump temperatures of 200 °C. Meanwhile, greases and hydraulic fluids are experiencing steady growth, largely driven by the need for construction equipment uptime. Suppliers are introducing advanced chemistries, such as calcium-sulfonate and polyurea thickeners, which not only enhance performance but also extend relubrication intervals. Collectively, these trends highlight a shift in the Saudi Arabian market, moving from traditional bulk engine oils to specialty driveline fluids that offer higher profit margins.

Geography Analysis

Riyadh is the country’s largest demand center, accounting for a significant share of Saudi Arabia's commercial vehicles lubricants market volume. The city’s metro expansion, ring-road widening, and airport logistics park projects generate thousands of daily trips by earthmovers, dump trucks, and ready-mix concrete mixers, each consuming lubricants at accelerated rates under stop-start conditions. Government tenders now stipulate WASL compliance, so vendors able to integrate drain alerts into the platform have secured multi-year contracts with municipal bus operators, refuse collectors, and construction fleets.

Western Province demand is dominated by Jeddah-Mecca pilgrimage flows that cause predictable spikes in June–July. The launch of the Mecca electric BRT corridor reduces diesel lubricant intensity within the urban core but leaves intercity coach routes untouched, so the overall Saudi Arabia commercial vehicles lubricants market share from the Western Province is expected to remain stable.

The Eastern Province supplies the bulk of Group II/III base oil via Luberef’s Yanbu site, giving local blenders a logistics advantage in serving petrochemical complexes at Jubail and Yanbu industrial cities, where equipment works continuously. Heavy-haul trucking that links these plants to Dammam’s King Abdulaziz Port remains diesel-dependent, sustaining robust engine oil and gear oil demand. NEOM in the northwest introduces a greenfield hotspot where sustainability mandates will eventually favor electric and hydrogen equipment; however, bulk earthworks through the coming years will still rely on diesel-fueled machinery, ensuring a transitional lubricant revenue stream for suppliers that establish on-site service hubs.

Competitive Landscape

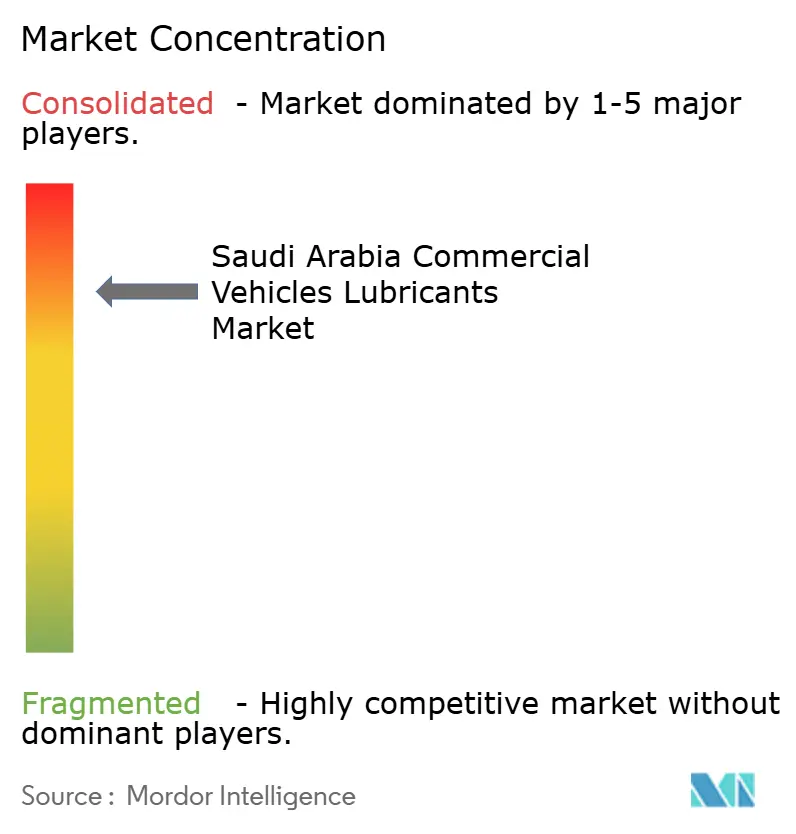

The Saudi Arabia Commercial Vehicles Lubricants Market is consolidated. Aramco’s acquisition of Valvoline and its interest in BP’s Castrol unit reflect a strategic bid to internalize blending margins and leverage unmatched base-oil access, giving the state champion a cost position few can match. Service bundling is emerging as a moat. Digital natives such as Eagle-IoT insert themselves between fleet and lubricant supplier, monetizing data while directing volume to partners that pay referral fees. As electrification spreads, first movers with e-driveline fluids and battery coolant portfolios stand to capture early share.

Saudi Arabia Commercial Vehicles Lubricants Industry Leaders

Petromin Corporation

Shell plc

BP plc

ExxonMobil Corporation

FUCHS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP plc initiated the sale of its Castrol lubricants division, valued at up to USD 10 billion, under a broader USD 20 billion divestment program to 2027. The sale could reshape Castrol’s presence in Saudi Arabia, where it holds a significant market share in the commercial vehicles lubricants.

- May 2025: TotalEnergies introduced next-generation engine oils meeting API SQ and ILSAC GF-7 standards, including Quartz 9000 Future FGC 5W-30 and Quartz 7000 Future GF-7 5W-30, designed for turbocharged and GDI engines.

Saudi Arabia Commercial Vehicles Lubricants Market Report Scope

Engine oils, gear oils, and greases, collectively known as commercial vehicle lubricants, are high-performance fluids crafted to minimize friction, wear, and heat in heavy-duty engines, transmissions, and axles. These lubricants, tailored for demanding operating conditions, high mileage, and prolonged drain intervals, play a crucial role in safeguarding, cleaning, and cooling components within commercial transport fleets.

The Saudi Arabia commercial vehicles lubricants market is segmented by product type. By product type, the market is segmented into engine oils, greases, hydraulic fluids, and transmission and gear oils. For each segment, the market sizing and forecasts have been done based on revenue (Litres).

By Product Type

| Engine Oils |

| Greases |

| Hydraulic Fluids |

| Transmission and Gear Oils |

| By Product Type | Engine Oils |

| Greases | |

| Hydraulic Fluids | |

| Transmission and Gear Oils |

Key Questions Answered in the Report

What is the projected volume for Saudi Arabia's commercial vehicles' lubricants by 2031?

What is the projected volume for Saudi Arabia's commercial vehicle lubricants by 2031?

Which product type is growing fastest?

Transmission and gear oils lead growth with a 6.18% CAGR through 2031.

How does Vision 2030 influence lubricant demand?

Construction megaprojects drive heavy-equipment hours, lifting consumption of engine oils, hydraulic fluids, and greases.

What impact will fleet electrification have?

Electrification will gradually cap engine-oil volumes but raise demand for e-axle fluids and battery coolants.

Page last updated on: