Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

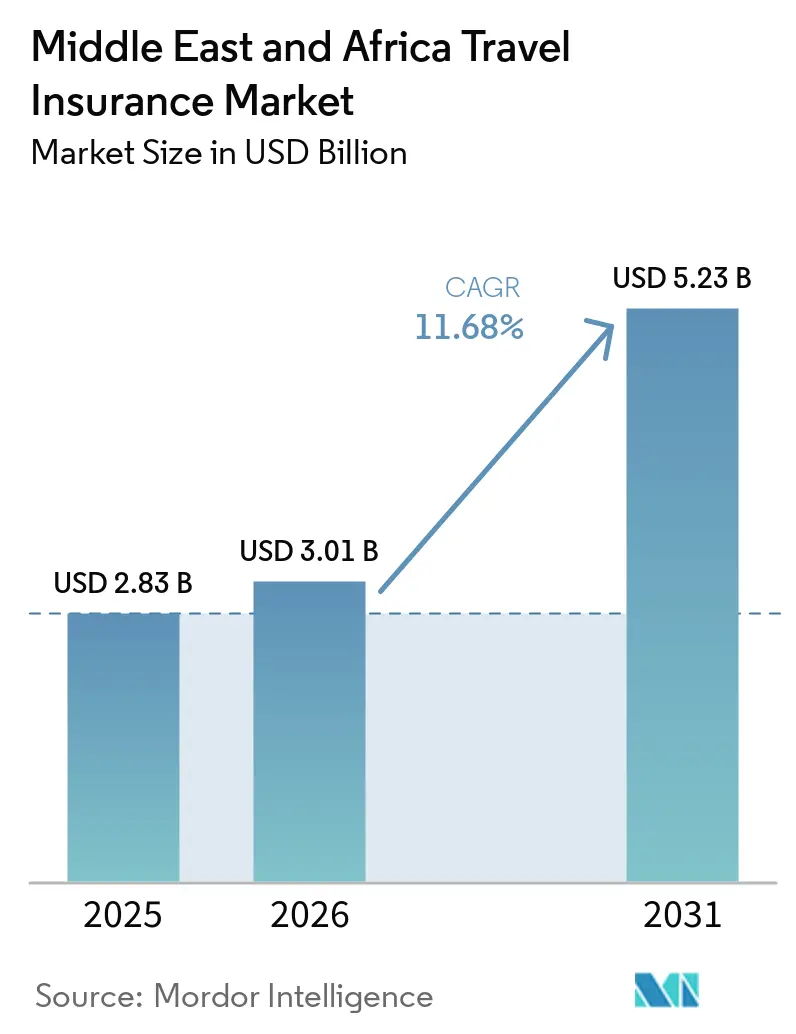

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 11.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Travel Insurance Market Analysis by Mordor Intelligence

The Middle East And Africa Travel Insurance Market size is projected to be USD 2.83 billion in 2025, USD 3.01 billion in 2026, and reach USD 5.23 billion by 2031, growing at a CAGR of 11.68% from 2026 to 2031.

The Middle East and Africa travel insurance market is benefiting from sustained recovery in international air connectivity, the spread of inbound medical cover mandates across key corridors, and the integration of embedded products within airline and online travel ecosystems. The Middle East continues to anchor growth due to hub dominance and pilgrimage seasonality, while Africa is on a faster growth path supported by improving travel corridors and digital adoption. Regulatory oversight in core Gulf markets is sharpening compliance and strengthening distribution quality, which is reinforcing consumer trust and attachment rates. Airlines, banks, and insurers are using digital channels to streamline issuance and claims processing, improving product access for frequent travelers and families. IATA and leading Gulf infrastructure operators report strong traffic and service momentum into 2026, which supports premium expansion in the Middle East and Africa travel insurance market when coverage is embedded at the booking and payment stages.

Key Report Takeaways

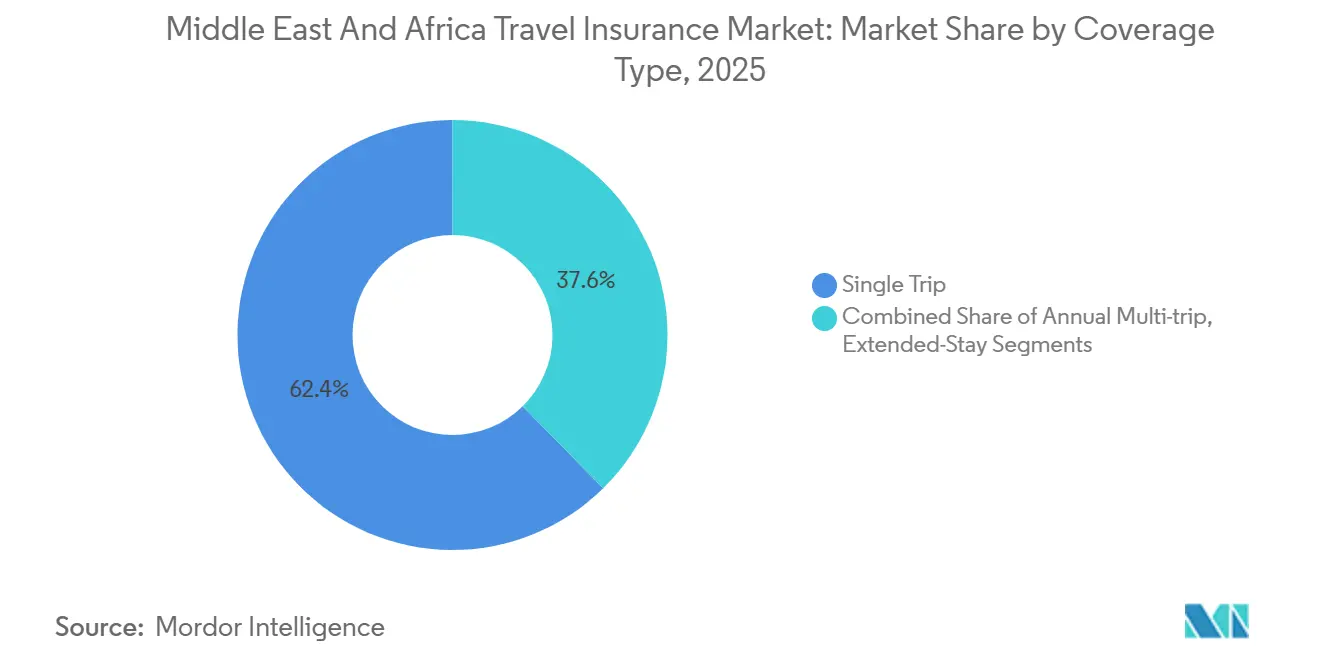

- By coverage type, single-trip policies led with 62.37% share of the Middle East and Africa travel insurance market in 2025, while annual multi-trip policies are projected to advance at a 6.88% CAGR through 2031.

- By end user, senior citizens accounted for 31.46% share of the Middle East and Africa travel insurance market in 2025, while business travelers are forecast to grow at a 22.68% CAGR through 2031.

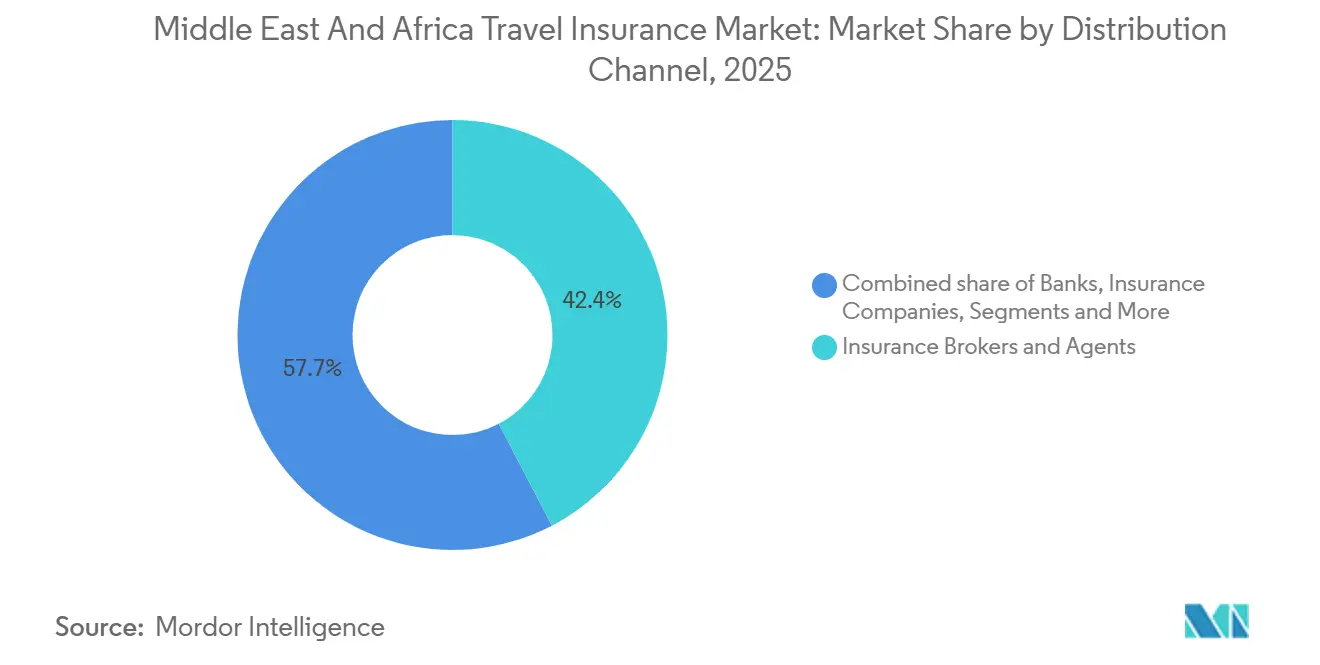

- By distribution channel, insurance brokers and agents held 42.35% share of the Middle East and Africa travel insurance market in 2025, while insurance aggregators are projected to grow at a 23.73% CAGR through 2031.

- By geography, the Middle East accounted for 65.35% of the Middle East and Africa travel insurance market in 2025, while Africa is projected to record a 12.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Travel Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Visa-linked mandatory medical cover in key corridors is catalyzing policy uptake | +2.8% | Global, with early gains in Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Airline/OTA embedded insurance expansion lifting attach rates | +2.4% | GCC core and selected African routes | Short term (≤ 2 years) |

| Recovering ME air travel volumes and hub connectivity | +2.1% | Middle East hubs, including Dubai, Abu Dhabi, Riyadh, Doha, Jeddah | Short term (≤ 2 years) |

| Digital aggregators and bancassurance are widening distribution in the GCC | +1.6% | GCC markets, including the UAE, Qatar, Saudi Arabia, Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Takaful-compliant offerings unlocking demand among Sharia-sensitive segments | +1.4% | Middle East and selected African markets | Long term (≥ 4 years) |

| Student and skilled-worker mobility to Europe and North America | +1.4% | Nigeria, Ghana, Saudi Arabia, UAE, Egypt, outward flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Visa-Linked Mandatory Medical Cover in Key Corridors Catalyzing Policy Uptake

Mandatory medical cover across key entry corridors is turning mobility decisions into insured transactions. Inbound health insurance rules within the Gulf are strengthening compliance discipline for visitors and residents, which familiarizes households with health coverage structures and reduces friction when purchasing cross-border travel protection. The United Arab Emirates consolidated insurance oversight under the central bank, tightened licensing, and expanded mandatory health coverage to deepen baseline protection, which also supports a smoother path for travel medical policy adoption when residents and inbound visitors cross borders[1]Central Bank of the U.A.E., “Annual Statistical Report for the Insurance Sector 2024,” Central Bank of the U.A.E., centralbank.ae. Saudi pilgrimage travel adds consistent seasonal demand and reinforces the use of medical coverage for short-duration religious trips, which encourages families to add emergency and travel assistance riders as part of standard trip planning, especially where airlines and agencies bundle options during booking. Gulf regulators have harmonized oversight around anti-money laundering and conduct standards, which is improving policy issuance and claims governance for inbound products sold by licensed insurers. As more outbound travelers from the Middle East consider Europe and other destinations with consular coverage checks, insurers see higher take-up driven by compliance norms and digital checkout flows that reduce time-to-issue. This regulatory framing sustains premium growth in the Middle East and Africa travel insurance market as compliance pathways standardize demand into repeatable purchase behavior.

Airline/OTA Embedded Insurance Expansion Lifting Attach Rates

Embedding travel protection within airline and OTA journeys is raising conversion because coverage is offered at the moment of payment and itinerary confirmation. New card-led programs that pair rewards with built-in insurance are expanding the addressable base among frequent travelers and corporate accounts, which supports higher multi-trip adoption and faster renewals. In February 2026, Riyadh Air and Mastercard launched a global partnership that introduced digital-first cards for consumers and a B2B virtual-card program for the travel trade, with bundled insurance enhancing value for flyers and partners who want seamless settlement and cover in one flow[2]Mastercard, “Riyadh Air and Mastercard Take Off Together to Redefine the Global Travel Experience,” Mastercard Newsroom, mastercard.com. Insurtech distribution has matured with configurable policy engines and instant underwriting at checkout, so airlines and agencies can localize benefits by route, trip length, and destination risk without manual handling, which supports scale economics in high-volume hubs. Carriers and aggregators report that attach rates improve when coverage is visible during seat and add-on selection, which aligns with customer expectations for one-stop purchase experiences within travel super-apps. Regulatory rules in the UAE that require premiums to be paid directly to insurers are encouraging players to automate settlement through embedded rails, which further professionalize the Middle East and Africa travel insurance market distribution model.

Recovering Middle East Air Travel Volumes and Hub Connectivity

Steady growth in passenger flows is driving policy issuance, especially on international routes where medical cover is required and trip interruption risks are higher. IATA reported that 2026 opened with positive traffic momentum globally and that February 2026 demand expanded further, which sustains higher volumes across Gulf hubs where long-haul itineraries dominate[3]Mastercard, “Riyadh Air and Mastercard Take Off Together to Redefine the Global Travel Experience,” Mastercard Newsroom, mastercard.com. Abu Dhabi Airports reported record traffic in 2025, with Zayed International emerging as one of EMEA’s fastest-growing mega-airports, adding new routes and carriers, thereby expanding the pool of travelers exposed to embedded insurance offers during booking or check-in. Regional tourism flows recovered strongly into 2026 off a high base, and visitors across leisure, family, and business segments continue to route through Gulf gateways with efficient visa processes and high service standards. As itineraries lengthen and multi-destination trips become more common, customers are more likely to secure comprehensive cover with expanded benefits such as medical evacuation, travel delay, and baggage loss. The combination of traffic growth, network expansion, and digital servicing supports premium resilience across the Middle East and Africa travel insurance market.

Digital Aggregators and Bancassurance Widening Distribution in GCC

Digital aggregators give travelers choice and speed, which helps raise conversion among price-sensitive customers and families shopping across carriers. Licensed banks in the Gulf are bundling travel protection with premium cards, and automatic enrollment reduces opt-in friction and helps corporates enforce coverage standards for employees who book through approved channels. In the UAE, RAKBANK’s Elevate World Elite credit card includes comprehensive medical travel insurance as a built-in benefit with digital claims support, which illustrates how banks use cross-sell to boost adoption while aligning with customer expectations for simplified protection benefits. Insurers are also strengthening mobile experiences, as shown by GIG Gulf’s app that supports policy management, claims tracking, and teleconsultation, which reinforces loyalty and repeat purchase behavior among frequent flyers and families. Qatar Insurance Company has compressed travel policy issuance to under two minutes through its online platform, demonstrating how real-time underwriting and document automation can materially reduce drop-off rates during checkout. Regulatory changes in the UAE that prohibit brokers from collecting premiums are steering distribution toward direct payments and embedded channels that improve governance and data integrity, a structural shift that should continue to benefit scalable digital models in the Middle East and Africa travel insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated visa refusal rates for several African outbound markets | -2.9% | Sub-Saharan Africa origins | Short term (≤ 2 years) |

| Geopolitical and security exclusions with travel advisories | -1.8% | Middle East hotspots and adjacent corridors | Medium term (2-4 years) |

| FX controls and hard-currency shortages | -1.6% | Parts of Africa and the Levant | Medium term (2-4 years) |

| Low non-life insurance penetration and price sensitivity | -2.1% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Visa Refusal Rates Dampening Insured Trip Volumes

High visa refusal rates for some African outbound markets reduce the number of trips that convert into active policies. Travelers often purchase medical coverage and prepare full documentation as part of their application files, but rejected applicants abandon or delay trips, which lowers repeat purchase probability. Families and students are especially sensitive to sunk costs from application processes, so confidence can weaken when approvals are unpredictable. Insurers attempt to cushion this through limited visa-denial riders, but those features require careful documentation and can add complexity to underwriting. When approvals improve in specific corridors, attach rates can rise quickly because applications already include coverage steps that customers understand. Over time, smoother approvals and better transparency would help stabilize demand in the Middle East and Africa travel insurance market.

FX Controls and Hard-Currency Shortages Constraining Premium Payment and Repatriation

Restrictions on access to hard currency can delay claims settlement and disrupt cross-border premium flows, which is challenging for medical evacuations and high-cost treatments billed in foreign currency. IATA reported that blocked airline funds across parts of the Middle East and North Africa remained material in 2025, reflecting frictions that can also affect insurance settlements routed through the same payment ecosystems. These delays pose an operating risk to local assistance partners and can lead to conservative coverage decisions or tighter limits when liquidity risk is high. Insurers and reinsurers often mitigate this with settlement clauses and retention accounts, but that can increase costs and reduce competitiveness for price-sensitive travelers. Where central banks ease controls and digitize settlement channels, carriers can restore service standards and improve turnaround times. The Middle East and Africa travel insurance market benefits when payments flow predictably, which supports customer confidence during emergencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Single-Trip Policies Anchor the Base, Multi-Trip Plans Accelerate

Single-trip policies accounted for 62.37% of premium volume in 2025, supported by leisure travel, family itineraries, and pilgrimage flows that align with short-duration coverage. The Middle East and Africa travel insurance market has relied on these products because they align with seasonal demand patterns for inbound and outbound trips to and from Gulf hubs. Airlines and digital platforms have made single-trip issuance fast within the booking flow, and many carriers add policy offers alongside seat selection and baggage, which keeps attach rates visible to casual travelers. Insurers have optimized benefit sets for emergency medical, trip delay, and baggage loss to short travel windows, helping manage pricing for cost-conscious customers. As consumer awareness of health insurance mechanics has improved in the UAE and neighboring markets, travelers more readily add international medical cover to protect against unexpected expenses during short holidays or visits, which sustains this segment’s share in the Middle East and Africa travel insurance market. Digital journeys from leading regional insurers now enable near-instant issuance with email confirmation and mobile-wallet support, which reduces abandonment and encourages same-day purchases when visas are granted.

Annual multi-trip policies are projected to grow faster at a 6.88% CAGR through 2031 as corporate mobility normalizes, and frequent travelers seek convenience and predictable coverage. Card-linked programs from banks and airline partnerships keep annual protection always-on for cardholders, which cuts per-journey friction and improves compliance for firms with travel policies. Built-in benefits on premium cards are a key vector, and issuers in the Gulf offer digital claims and simple documentation to speed reimbursements for delays, interruptions, and medical expenses. As destinations diversify and itineraries include multiple stops each quarter, customers favor annual plans that cover cumulative trips without repetitive forms. Embedded insurance at booking also nudges frequent flyers toward upgrades that include broader medical evacuation and high-limit coverage, which makes annual products attractive from a value perspective. The Middle East and Africa travel insurance market is also expanding multi-trip features for families and small businesses, with mobile-first management and omnichannel assistance improving service standards.

By End User: Senior Citizens Dominate the Base, Business Travelers Lead Growth

Senior citizens represented 31.46% of customers in 2025 due to higher medical risk, longer stays, and a preference for comprehensive assistance. This cohort often seeks coverage with emergency medical, hospitalization, evacuation, and teleconsultation, supported by global assistance networks. Digital claims, medical hotlines, and clear benefit wording matter because families want predictable support during emergencies while traveling with older relatives. In Gulf markets, stronger domestic health insurance norms have improved familiarity with coverage terms, which lowers friction when buyers select higher medical limits before international trips. Insurers and banks also tailor products for multi-generational travel with simplified enrollment and bundled features, which align with the service expectations of older customers who want 24/7 help. The Middle East and Africa travel insurance market continues to position senior-friendly products with transparent exclusions and hospital networks to maintain trust and repeat purchase behavior.

Business travelers are projected to expand at a 22.68% CAGR through 2031, reflecting a normalization of corporate travel to client sites and regional hubs. Corporate cards and airline loyalty tiers now pair travel rewards with embedded protection that activates automatically when tickets are issued, which improves compliance and speeds coverage activation. The 2026 partnership between Riyadh Air and Mastercard that combined digital-first consumer and B2B solutions with bundled insurance is a clear example of these converging rails that make travel protection part of the standard purchase flow. Fast claims review matters for business trips because interruptions lead to revenue impact and rescheduling costs; carriers respond by accelerating digital documentation, status updates, and direct reimbursements. Education and family travelers continue to contribute steady demand due to consular requirements and school timetables, and group policies help reduce per-person costs for multi-destination itineraries. As hub throughput and connectivity deepen in the Gulf, the Middle East, and Africa travel insurance market will continue to expand higher-limit products suited to corporate and professional services users, supported by assistance partners and clear travel policy alignment.

By Distribution Channel: Intermediaries Hold the Lead, Aggregators Scale Fast

Insurance brokers and agents accounted for 42.35% of distribution in 2025 by leveraging established client relationships and cross-selling travel coverage. In the Gulf, brokerages have historically leaned on relationships developed in motor, health, and property to introduce travel products, while strengthening service with digital documentation and claims support. Regulatory tightening in the UAE that requires direct premium payments to insurers is shifting how intermediaries operate, reducing cash handling and encouraging digital settlement that improves consumer confidence. Direct channels are also gaining relevance in the Middle East and Africa travel insurance market as insurers invest in web and mobile experiences that reduce friction at issuance and renewal. Banks complement these efforts with card-linked protection that auto-enrolls eligible customers, increasing attachment and supporting more consistent adoption among business travelers and families.

Aggregators are expected to record the fastest growth at a 23.73% CAGR through 2031, as travelers compare benefits and prices online and complete issuance in minutes. Qatar Insurance Company’s digital platform demonstrates the impact of streamlined journeys, with quick policy issuance and mobile-first checkout that reduces drop-off and improves conversion for outbound trips[4]Qatar Insurance Company, “QIC Offers a Variety of Travel Insurance Plans Gearing Up for Summer,” QIC Group, qic-group.com. Insurers in the region report that improved app experiences, instant policy documents, and clear benefit summaries are critical drivers of adoption, especially for first-time buyers. Assistance features such as teleconsultation, digital claims status, and 24/7 helplines create confidence and support word-of-mouth growth, which is valuable in family and community networks. Over time, aggregators integrate more granular underwriting at the point of sale, which helps tailor benefits to trip length, destination, and passenger risk, improving price-to-benefit alignment. These trends, coupled with governance rules that standardize payment flows, are reinforcing the maturity of the Middle East and Africa travel insurance industry across distribution segments.

Geography Analysis

The Middle East accounted for 65.35% of premiums in 2025, reflecting hub dominance and steady throughput across major gateways. This share underscores how the Middle East and Africa travel insurance market concentrates activity around high-connectivity corridors that attract both leisure and business demand. Traffic expansion into 2026 continued to support policy issuance, with IATA reporting global growth at the start of the year and again in February, which provided a positive base for Gulf routes that rely on long-haul flows. Abu Dhabi Airports reported record traffic in 2025 as Zayed International rose among EMEA’s largest hubs, which directly expands the exposure base that embedded insurance can reach during booking journeys. Pilgrimage travel continues to provide strong seasonal flows that translate into short-duration policies, and air is the primary mode of arrival, supporting consistent attach opportunities at the point of ticketing. Gulf regulators have sharpened oversight of intermediaries and insurers, which has helped streamline premium settlement and bolster consumer protection, sustaining confidence in travel protection offerings.

The Middle East and Africa travel insurance market also sees momentum in Qatar, where digital insurer regulations provide a pathway for technology-led products and faster approvals for embedded distribution. Qatar Insurance Company used a mobile-first approach to compress policy issuance times, which helped lift seasonal adoption during peak travel windows. The combination of hub growth, digital readiness, and consistent regulatory enforcement is improving attach rates and benefit awareness among residents and visitors. Airlines and banks are important conduits for policy offers, with card-linked benefits and embedded flows at checkout driving repeat purchases among frequent travelers. The Middle East and Africa travel insurance market share is therefore anchored by the Gulf, where infrastructure and policy frameworks converge to create a stable base for premium growth.

Africa represented 34.65% of 2025 premiums and is projected to grow at a 12.44% CAGR through 2031, supported by improving travel corridors, digital payments, and gradual facilitation in selected visa pathways. Payment and currency bottlenecks remain a headwind, with IATA reporting blocked funds in some markets that affect aviation and related payment ecosystems for cross-border services, including insurance. As embedded channels expand through airlines, OTAs, and bank-led apps, more first-time travelers will see travel protection as part of a standard booking journey. Better mobile claim support and clear language around benefits will help build trust in markets where non-life penetration is low. Over the forecast window, increasing route density across North, East, and West African gateways should broaden the exposure base. These shifts, combined with firm-level investments in digital service and assistance networks, position the Middle East and Africa travel insurance market to capture incremental growth across African corridors while the Gulf continues to lead in absolute premium terms.

Competitive Landscape

The Middle East and Africa travel insurance market features a mix of global carriers, regional champions, and Takaful-oriented providers that serve distinct customer cohorts. Regulatory capital and conduct requirements in the Gulf are raising the bar on governance, cybersecurity, and data integrity, which encourages consolidation around well-capitalized insurers and distributors. Digital capabilities increasingly differentiate leaders, as fast issuance, transparent benefit displays, and streamlined claims accelerate customer adoption, especially among frequent travelers and families. Banks and airlines play visible roles in embedding protection into purchase flows, which reinforces habitual buying and smooths compliance for corporate travelers. With consistent hub growth and rising cross-border trips, the competitive focus is shifting toward experience quality, automation depth, and assistance strength rather than headline price alone.

Strategic moves highlight how embedded and card-linked rails are reshaping attach. Riyadh Air and Mastercard launched digital-first consumer cards and a B2B virtual-card program that bundles insurance alongside travel rewards and settlement solutions, broadening the base of pre-covered travelers and partners who value frictionless service. Qatar Insurance Company has used its online platform to compress travel policy purchase times to under two minutes, showing how automation increases conversion during seasonal peaks. GIG Gulf’s mobile app integrates policy management, claims tracking, and teleconsultation, an experience-led approach that supports loyalty and renewal among core customer segments. These initiatives reflect a broader pivot in the Middle East and Africa travel insurance market toward seamless, embedded coverage that is visible at the point of sale and supported by reliable assistance networks.

Consumer intent indicators are also helpful for planning. Allianz Partners’ Travel Index for the UAE reported strong purchase intent for travel insurance in 2025 among surveyed residents, led by personal security and medical benefits as top reasons to buy. This aligns with the Gulf’s maturity in health coverage and the region’s reliance on international air travel, both of which support premium growth. Insurers are therefore directing investment toward instant issuance, easy documentation, and reliable roadside and airport assistance add-ons that complement core medical and trip benefits. Banks are reinforcing these patterns through card-linked enrollment and online claims portals that maintain service quality for premium customers. The Middle East and Africa travel insurance market is likely to see more integrated airline and bank partnerships as players seek to raise attach without adding friction to the booking journey.

Middle East And Africa Travel Insurance Industry Leaders

Allianz Partners

Gulf Insurance Group (GIG)

AIG (Travel Guard)

Qatar Insurance Company

Sukoon Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Riyadh Air and Mastercard announced a strategic global partnership featuring digital-first credit and prepaid cards bundling travel insurance with flight rewards, plus a B2B virtual-card program for travel-trade settlements (the first airline-branded initiative of its kind globally), reinforcing Saudi Arabia’s role as a global travel hub.

- December 2025: Allianz Partners announced a major expansion of its Allianz Health & Benefits Network through a partnership with SanlamAllianz, creating the first integrated global employee health benefits network across Africa. While focused on employee benefits, this strengthens Allianz’s travel-related assistance and mobility insurance footprint across Africa.

- July 2025: Allianz Partners published its Travel Index 2025 for the UAE, reporting strong intent to purchase travel insurance among surveyed residents and highlighting personal security and medical benefits as primary motivations.

- March 2025: Qatar Insurance Company reported a 50% increase in outbound travelers purchasing travel insurance for Eid al-Fitr 2025 compared to Eid 2024, with more than half of policyholders considering European itineraries and completing transactions via its online platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Middle East and Africa travel insurance market as the total gross written premium generated by stand-alone or embedded policies that protect residents and visitors against medical emergencies, trip cancellations, baggage loss, and related travel contingencies while crossing an international border.

Scope exclusion: we do not size purely domestic trip cover issued for travel within one country.

Segmentation Overview

- By Coverage Type

- Single Trip

- Annual Multi-Trip

- Extended-Stay and Others

- By End User

- Senior Citizens

- Education Travelers

- Business Travelers

- Family Travelers

- Other End-Users

- By Distribution Channel

- Insurance Companies

- Banks

- Insurance Brokers and Agents

- Insurance Aggregators and Online Platforms

- By Geography

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Kuwait

- Bahrain

- Oman

- Israel

- Jordan

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Egypt

- Morocco

- Rest of Africa

- Middle East

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting heads at composite insurers, digital aggregators operating in GCC hubs, and retail brokers in South Africa and Kenya. Discussions validated average premium per policy, claims ratios, and seasonality shifts, while short consumer pulse surveys helped us gauge policy penetration among family, senior, and business traveler cohorts.

Desk Research

We began with publicly available datasets such as UNWTO departure statistics, IATA passenger flows, airport authority traffic bulletins, and central-bank foreign-exchange earnings, which anchor outbound-trip volumes and spend. Next, policy wording archives, regulatory circulars, and actuarial journals clarified mandatory cover rules and premium corridors. Our team also mined D&B Hoovers financials, Dow Jones Factiva news, and Questel patent filings to benchmark insurer revenue disclosures, digital-channel uptake, and product innovation. These sources form the quantitative spine; many other references supported finer validation.

Market-Sizing & Forecasting

A top-down construct converts outbound departures into an insurable demand pool, multiplies by estimated policy-take-up rates, and then applies weighted average premiums in USD. Selective bottom-up checks, such as sampled aggregator sales and insurer channel splits, fine-tune totals. Key variables tracked include visa issuance volumes, average length of stay, mandatory Hajj/Umrah medical cover, online aggregator share of new policies, and currency movements against the dollar. Multivariate regression, guided by expert consensus on tourism growth and premium elasticity, projects values through 2030. Any data voids are bridged with conservative midpoint assumptions reviewed by subject specialists.

Data Validation & Update Cycle

Outputs pass three layers of anomaly screening, peer review, and variance reconciliation against independent tourism receipts and insurer earnings. Reports refresh annually, and we trigger mid-cycle updates when material events, such as regulatory changes and major health crises, shift baseline drivers. A fresh analyst pass precedes each client delivery.

Why Our Middle East and Africa Travel Insurance Baseline Commands Credibility

Published figures often diverge because firms differ on what counts as insurable travel, which premium components are included, and how frequently models are refreshed.

Key gap drivers stem from (a) some publishers folding in domestic cover and parametric specialty lines, (b) the use of multi-year rolling averages that inflate 2024 values, and (c) limited channel checks that overlook rapid aggregator-led discounting.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.51 B (2025) | Mordor Intelligence | - |

| USD 2.77 B (2024) | Global Advisory Firm A | Includes domestic policies and service-fee markups; model not refreshed post-pandemic |

| USD 2.85 B (2024) | Regional Databook B | Bundles parametric insurtech products; limited verification of premium compression in online channels |

The comparison shows that our disciplined scope selection, live channel interviews, and annual refresh cadence yield a balanced, transparent baseline that decision-makers can readily trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook for the Middle East and Africa travel insurance market?

The Middle East and Africa travel insurance market size was USD 2.83 billion in 2025 and is projected to reach USD 5.23 billion by 2031, reflecting an 11.68% CAGR to the end of the forecast period.

Which segments lead and which are growing the fastest within the Middle East and Africa travel insurance market?

Single-trip policies led with 62.37% share in 2025, and annual multi-trip plans are set to grow fastest at a 6.88% CAGR through 2031, supported by corporate travel recovery and embedded distribution.

How is regulation influencing distribution models in the Middle East and Africa travel insurance market?

UAE regulatory rules require direct premium payments to insurers, which favors embedded, direct, and bank-led channels and raises governance standards across intermediaries. This supports consumer confidence and faster digital issuance.

What role do airlines and payment networks play in shaping the Middle East and Africa travel insurance market?

Airline and payment partnerships are embedding coverage into checkout and card benefits, which drives higher attach rates and smoother claims, as shown by the Riyadh Air and Mastercard program launched in 2026.

Which geographies are most influential in the Middle East and Africa travel insurance market?

The Middle East accounted for 65.35% of 2025 premiums, driven by Gulf hub connectivity and consistent inbound and outbound flows, while Africa is projected to grow at 12.44% CAGR through 2031. Strong hub traffic supports ongoing premium growth.

What factors could constrain growth in the Middle East and Africa travel insurance market?

Visa refusal rates in some corridors, currency controls, and geopolitical exclusions can dampen insured trip volumes and delay claims, though improvements in digital settlement and governance help mitigate these risks.

Page last updated on: