Middle East And Africa Transformer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

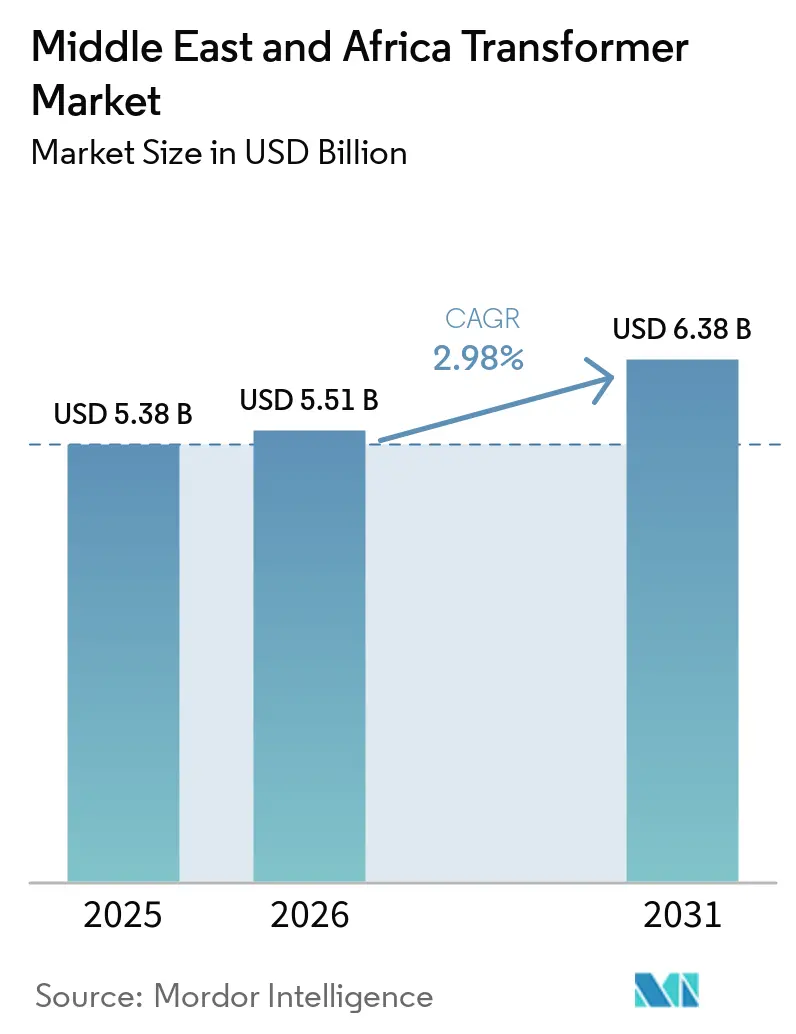

| Base Year Market Size (2025) | USD 5.38 Billion |

| Market Size (2026) | USD 5.51 Billion |

| Market Size (2031) | USD 6.38 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Transformer Market Analysis by Mordor Intelligence

The Middle East And Africa Transformer Market size is expected to increase from USD 5.38 billion in 2025 to USD 5.51 billion in 2026 and reach USD 6.38 billion by 2031, growing at a CAGR of 2.98% over 2026-2031.

Measured growth conceals structural shifts as sovereign wealth funds steer capital toward grid-modernization megaprojects, while utility budgets remain sensitive to oil price cycles. Specialized high-voltage demand rises sharply around marquee investments such as Saudi Arabia’s NEOM, where converter stations and HVDC links supersede conventional distribution additions.[1]Freshfields, “Inside Infrastructure—MENA Trends,” freshfields.com Supply-chain challenges intensify this dynamic; Hitachi Energy cautions that new power-class units now command three-year lead times, prompting utilities to over-order and regional players to localize production.[2]POWER Magazine, “Digital Sensor Expands Asset Management,” powermag.com At the same time, air-cooled designs gain traction in dense urban districts and hyperscale data centers, reflecting both tightening environmental regulations and the need for compact equipment.

Key Report Takeaways

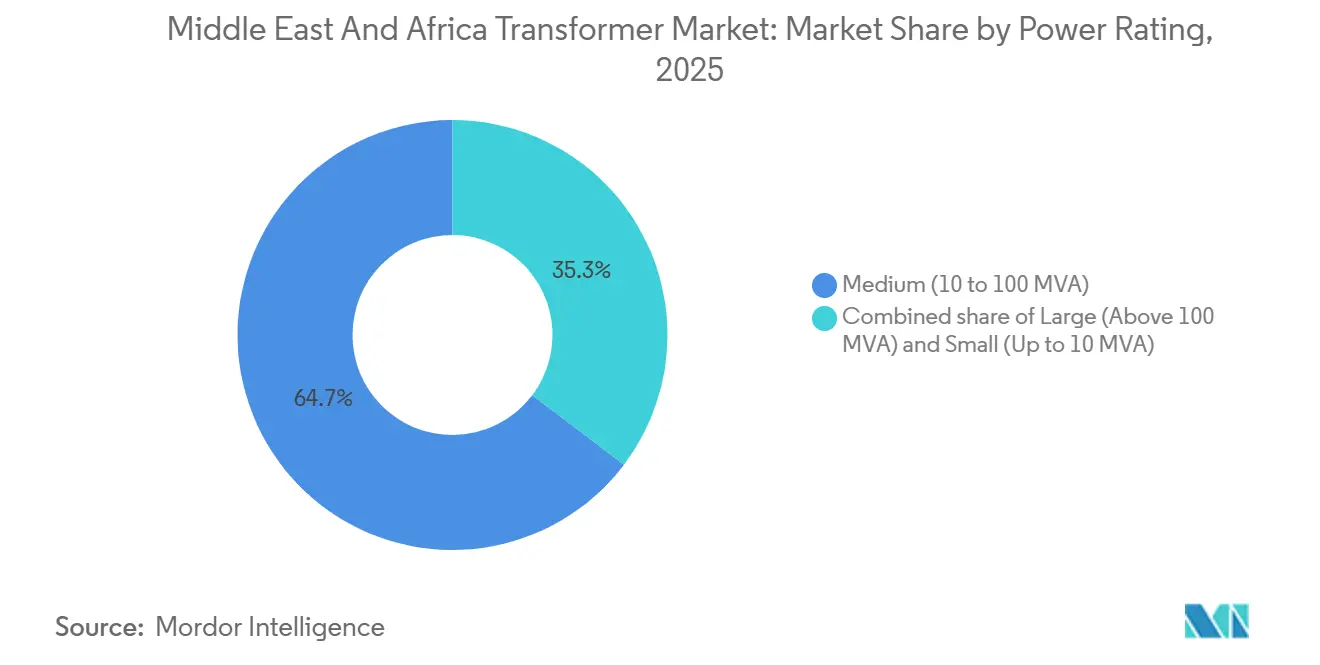

- By power rating, medium-rated transformers held 64.7% of the Middle East and Africa transformer market share in 2025, while large units above 100 MVA are expected to grow at a 4.9% CAGR through 2031.

- By cooling type, oil-cooled designs commanded 84.3% revenue share in 2025; air-cooled variants are projected to post the fastest 5.2% CAGR to 2031.

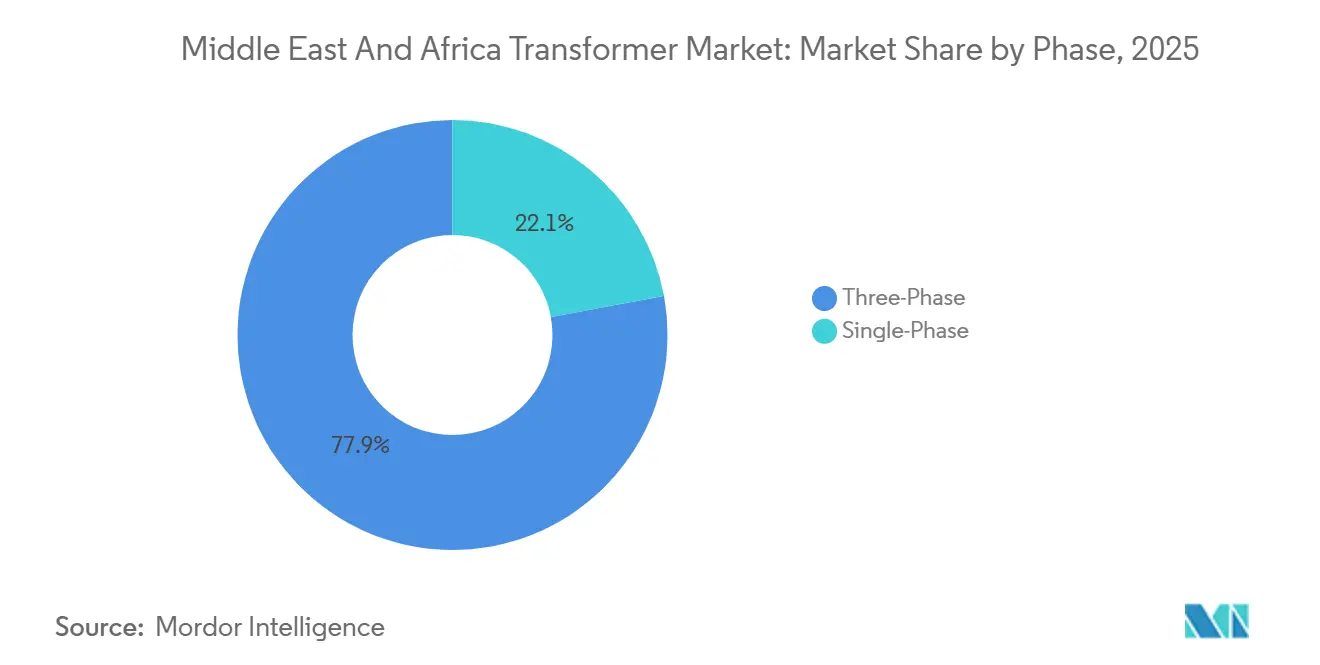

- By phase, three-phase units led with 77.9% share in 2025 and is expected to grow at a 3.6% CAGR, outstripping single-phase replacements.

- By transformer type, power transformers held 60.0% share in 2025; distribution transformers is expected to grow at 4.5% through 2031 on last-mile electrification in Nigeria and peri-urban Gulf districts.

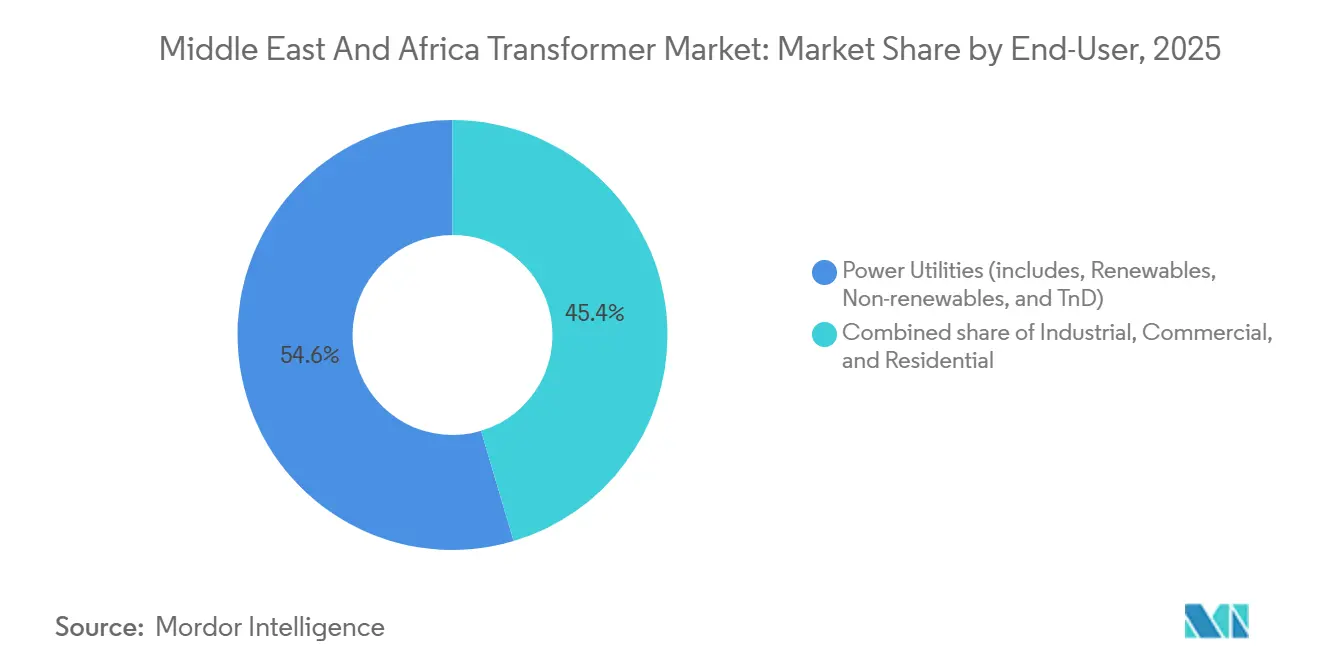

- By end-user, power utilities represented 54.6% of 2025 demand, while industrial buyers are expected to log the highest 4.7% CAGR on process-intensive investments across mining, petrochemicals, and desalination.

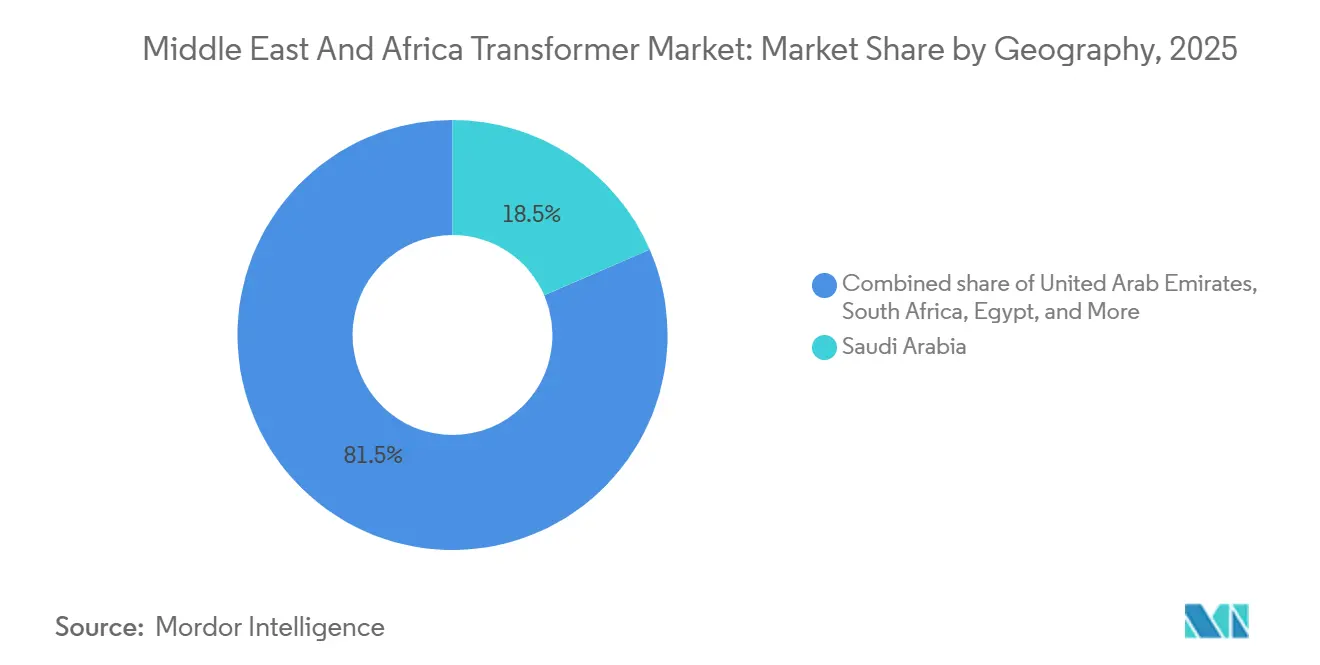

- By geography, Saudi Arabia led the Middle East and Africa transformer market with an 18.5% share in 2025; Egypt is expected to register the strongest 5.3% CAGR to 2031 as it prepares the grid to absorb 20 GW of renewables.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility-scale renewables driving grid expansion | +1.2% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2–4 years) |

| Rising urban electricity demand | +0.8% | UAE, Egypt, Nigeria | Long term (≥ 4 years) |

| State-funded grid modernization programmes | +0.9% | Saudi Arabia, Egypt, Qatar | Medium term (2–4 years) |

| Mining-led micro-grid investments | +0.4% | South Africa, West Africa | Short term (≤ 2 years) |

| Desalination plant electrification | +0.3% | Saudi Arabia, UAE | Medium term (2–4 years) |

| Cross-border HVDC links | +0.5% | Egypt–Saudi corridor, GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Utility-Scale Renewables Driving Grid Expansion

Saudi Arabia’s Public Investment Fund allocated USD 50 billion to solar and wind under Vision 2030, a commitment that pulls forward orders for step-up transformers and reactive-power devices at each new generation site.[3]Dubai Municipality, “Building Code Update 2024,” dm.gov.ae The UAE’s 2 GW Al Dhafra PV plant uses 180 pad-mounted units rated 33/0.4 kV to funnel inverter output onto the 400 kV backbone.[4]Public Investment Fund, “Vision 2030 Renewable Allocations,” pif.gov.sa Egypt’s Benban complex sourced turnkey packages from Asian vendors, pricing 15% below European peers, intensifying margin pressure on Western OEMs. South Africa’s 2024 IPP round added 27 projects, each demanding Eskom-approved tap-changer transformers able to ride through coal-related frequency swings. IEC 60076-16 compliance for wind duty is now embedded in most tenders, screening out suppliers without accredited labs.

Rising Urban Electricity Demand

Dubai’s population topped 3.6 million in 2025, pushing summer peak load to 13.5 GW and prompting DEWA to build 42 new 132/11 kV substations by 2026. Each site installs two 90 MVA transformers with on-load tap changers for redundancy and ±5% voltage control during air-conditioning spikes. Cairo’s metro extensions need 25 MVA rectifier transformers at each traction substation to feed 1.5 kV DC rolling stock. Lagos is tackling 30% distribution losses with smart, sensor-equipped units compatible with Schneider Electric’s EcoStruxure suite. Secondary cities such as Jeddah, Sharjah, and Alexandria are switching from informal feeders to pad-mounted or vault-type transformers that suit crowded rights-of-way.

State-Funded Grid Modernisation Programmes

Saudi Electricity Company earmarked SAR 28 billion (USD 7.5 billion) in 2024 to replace legacy 115 kV lines with 380 kV digital substations, retiring roughly 1,200 transformers commissioned before 2005. Egypt secured EUR 600 million from the EBRD to reinforce Aswan-to-Mediterranean corridors, specifying partial-discharge monitoring and extra DGA ports. Qatar’s Kahramaa placed a QAR 1.2 billion order for 18 substations equipped with SF₆-free switchgear and ester-filled transformers aligned with its 2030 carbon roadmap. As a group, these programs value digital twins and analytics, rewarding OEMs with integrated software.

Mining-Led Micro-Grid Investments

South Africa’s platinum belt and West Africa’s gold corridor have turned to containerized 5–25 MVA transformers that power autonomous haulage and ventilation without full grid extension. Mobility, IECEx certification, and rapid relocation matter more than the lowest price. Siemens delivered a 132/33 kV mobile substation to Egypt’s New Administrative Capital in 2025, collapsing on-site works from 14 months to 8 weeks. Eaton’s IECEx-approved 11 kV dry-type series now addresses methane-rich shafts where oil-filled gear is unacceptable. High copper prices keep rental rates attractive, giving specialized lessors room to expand fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price driven utility CAPEX cuts | -0.9% | Saudi Arabia, UAE, Qatar, Nigeria | Short term (≤ 2 years) |

| Low-cost Asian imports intensifying price pressure | -0.7% | Region-wide | Medium term (2–4 years) |

| Skilled maintenance-labor shortage | -0.3% | Saudi Arabia, UAE, South Africa | Long term (≥ 4 years) |

| Resin supply bottlenecks for dry-type units | -0.2% | UAE, Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Driven Utility CAPEX Cuts

Brent crude averaged USD 72 per barrel in Q1 2025, prompting Saudi Aramco Power and Abu Dhabi National Energy to defer non-critical substation awards by up to a year. Historical data show a 0.6 correlation between quarterly oil revenue and GCC utility spending, with a two-quarter lag. Nigeria mirrored the squeeze, postponing 14 projects and leaving 8.2 GW of stranded generation. Deferred demand usually resurfaces once oil stabilizes above USD 80, but the short-term shock trims factory utilization and raises working-capital needs for OEMs.

Low-Cost Asian Imports Intensifying Price Pressure

Chinese exporters shipped CNY 64.6 billion (USD 9.1 billion) worth of transformers in 2025, 22% of which landed in the Middle East and Africa transformer market. Won depreciation lets Korean makers under-bid European rivals by 12-18% on ≤50 MVA units. Utilities now split tenders into “technology-critical” lots reserved for IEC-certified incumbents and commodity lots open to all, producing a two-tier price curve. Saudi 30% and UAE 25% local-content rules cushion the blow, but Asian OEMs are countering through joint ventures such as Mitsubishi Electric-Alfanar.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Large Units Anchor Mega-Projects

Large transformers rated above 100 MVA constitute the critical link between gigawatt-scale solar parks, HVDC terminals, and national backbones within the Middle East and Africa transformer market. The segment is forecast to grow at 4.9%, exceeding the overall trajectory as Egypt–Saudi, GCC, and Ethiopia–Kenya corridors add converter capacity. Medium-rated units hold the broadest footprint, securing 64.7% of 2025 demand. Their standardized designs attract aggressive Asian bidding, squeezing margins but enabling rapid scale-out of distribution feeders and mid-tier industrial plants. NEOM alone could pull 180 large transformers by 2030, concentrating procurement into a handful of blockbuster tenders.

Adoption of factory-assembled skids and mobile substations is shortening lead times and redirecting a slice of capex toward integration services. Siemens’ eight-week deployment to Egypt’s new capital showcased a time-to-energy gain that utilities increasingly value. IEC 60076-57 validation and harmonic endurance now form the ticket to play for any OEM courting orders above 300 MVA. Only six to eight suppliers worldwide meet that bar, effectively insulating the top tier from race-to-bottom pricing.

By Cooling Type: Safety Priorities Propel Dry-Type Uptake

Oil-filled designs kept an 84.3% revenue hold in 2025, favored for thermal headroom and lower upfront cost inside outdoor yards across the Middle East and Africa transformer market. Yet municipal fire codes in Dubai, Doha, and Riyadh are steering enclosed substations, hospitals, and data halls toward cast-resin technology at a brisk 5.2% CAGR. Dubai Municipality’s 2024 rule barring oil-immersed units above the 20th floor immediately swung 35% of new high-rise projects to dry-type solutions.

Efficiency gaps have narrowed to 0.3 percentage points, undercutting the total-cost-of-ownership penalty that once deterred adoption. Ester fluid hybrids appear set to straddle both camps, offering fire resistance with liquid cooling. Saudi Electricity Company’s 2024 ester pilot in Riyadh logged 15% cooler windings and zero PD alarms over 18 months. NFPA 70 references are creeping into Gulf codes, foreshadowing formal mandates by 2028.

By Phase: Three-Phase Preference Mirrors Industrial Load Patterns

Three-phase transformers supplied 77.9% of 2025 shipments and are expected to post a 3.6% growth arc through 2031 as industrial clusters, desalination plants, and HVDC terminals demand balanced power. Single-phase units persist in rural electrification, with Egypt fielding 48,000 pole-mounted devices in 2024. However, rising urbanization and near-total household access across the Gulf constrict that sub-segment.

Industrial centers in Jubail, Yanbu, and Ras Al-Khair rely on dedicated 380/132 kV grids housing dozens of 50–150 MVA three-phase transformers. Superior power density and inherent phase balance keep three-phase as the de facto choice for ratings above 100 kVA, allowing OEMs to bundle digital monitoring and service contracts that lift lifecycle value.

By Transformer Type: Distribution Units Lead Volume, Utilities Anchor Value

Power transformers captured 60.0% of the 2025 spend as Saudi, Egyptian, and South African utilities uprated backbones to absorb renewable intermittency. Yet distribution units will clock the quicker 4.5% CAGR on Nigeria’s electrification drive and mixed-use sprawl in Gulf suburbs. Standard 1 MVA pad-mounted units from Chinese plants land at USD 8,000–10,000, undercutting European tags by up to 35%. OEMs competing here must lean on logistics speed, warranty service, and local content compliance to defend their share.

Power-class procurement remains dominated by tight specs, type tests, and long-term service, creating stickier revenue streams. Siemens’ EUR 180 million award for 24 × 250 MVA units in Egypt hinged on digital-twin analytics rather than headline price.

By End-User: Industrial Demand Narrows the Gap With Utilities

Utilities consumed 54.6% of 2025 deliveries, but industrial buyers, such as petrochemicals, mining, and desalination, should expand at a 4.7% clip through 2031. Saudi Aramco’s Jafurah complex needs 42 × 33/6.6 kV transformers for compressors and refrigerants. South African platinum mines are electrifying underground haulage to trim diesel and emissions, requiring IECEx-rated transformers that few suppliers offer. Data-center growth from Abu Dhabi to Nairobi favors dry-type or ester-filled units with N+1 redundancy and onboard fiber sensors, channels where Schneider Electric and Eaton hold entrenched positions.

Geography Analysis

Saudi Arabia dominated the Middle East and Africa transformer market with an 18.5% revenue slice in 2025, riding Vision 2030 mega-projects and a 380 kV mesh that ties industrial hubs to western load centers. Hitachi Energy’s USD 200 million Dammam plant, active since mid-2024, cuts lead times to 28 weeks and secures local-content bonus points.

Egypt is on a faster 5.3% CAGR path as the national utility preps the grid to accept 20 GW of solar and wind by 2030, slashing technical losses from 22% to 12%. The mix spans 500 kV backbone reinforcements and distribution build-outs for the New Administrative Capital and Suez industrial zone.

The UAE blends mature frameworks in Abu Dhabi and Dubai with greenfield demand up the coast. DEWA’s 2025 budget of AED 7.8 billion earmarked 28% for transmission gear supporting a 100% clean-energy ambition. Qatar hinges transformer demand on LNG output; North Field South’s expansion will require 34 × 132/33 kV units by 2030.

South Africa’s transmission shortfalls curtail generation dispatch to 22 GW despite 30 GW installed; Eskom counts 18% of transformers beyond 40-year life. Nigeria’s potential sits trapped behind tariff deficits, though the 2024 Electricity Act opens private investment in transmission grids. Morocco, Kenya, Ghana, and smaller Gulf states round out the rest of the MEA bucket, where donor-funded mini-grids and mining drive lumpy, project-specific volumes.

Competitive Landscape

Market concentration is moderate. The top five OEMs, Hitachi Energy, Siemens, ABB, GE, Schneider Electric, captured 42% of transmission-tier revenue in 2025, yet only 18% of commoditized distribution volume. Global players stress service-intensive, digitally enabled propositions, while regional fabricators and Asian entrants prioritize price and delivery speed. Hitachi Energy’s Saudi factory illustrates why localization unlocks both lead-time and policy rewards.

Asian challengers leverage export credit and currency arbitrage. Chinese bids bundled with defer-pay terms are hard for cash-strapped utilities to refuse, forcing Western OEMs either to match financing or pivot to lifecycle services. ABB’s Ability TRAFCOM portal monitors DGA and winding temps in real time, lifting asset life 15–20% and forging recurring revenue ABB.COM. Siemens’ Sensformer embeds fiber optics that flagged hotspots early enough to win a premium-priced Egypt award in 2024.

Future share battles will hinge on data analytics, predictive maintenance, and software ecosystems more than core copper-steel engineering. Local fabricators may find niche wins in mining micro-grids and desalination skids where engineering-to-order flexibility trumps global scale. As digital twins creep into procurement specs, OEMs that marry hardware with cloud diagnostics appear best placed to out-run pure-play fabricators.

Middle East And Africa Transformer Industry Leaders

Siemens AG

General Electric Company

Toshiba Corporation

Eaton Corporation Plc

HD HYUNDAI ELECTRIC CO. LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: GE Vernova completed its acquisition of Prolec GE, enhancing its transformer manufacturing capabilities and global grid-equipment portfolio. While primarily focused on North America, this acquisition bolsters GE Vernova’s capacity to meet the growing transformer demand in emerging Middle East and African markets through increased production capacity and product diversity.

- March 2025: TCL launched TCL SunPower Global, focusing on Europe, the Middle East, and Africa with SunPower-branded solar solutions. This initiative indirectly supports transformer demand in MEA by facilitating regional solar PV deployment, which requires grid-connected step-up/step-down transformers and other balance-of-system electrical equipment.

- March 2025: Saudi Power Transformers Company won a SAR 129.3 million contract to design and supply transformers for a significant Saudi EPC project. This 18-month agreement strengthens Saudi Arabia’s role as a key transformer manufacturing hub for grid-expansion projects across the Middle East and Africa.

- February 2024: Elsewedy Electric launched new oil‑immersed distribution transformers in Egypt, offering a full range from 50 kVA to 15 MVA at 36 kV, including hermetically sealed, conservator‑type, pole‑mounted, grid‑mounted, eco, smart, and special‑application units. The products aim to boost local transformer manufacturing, reduce imports, and support Egypt’s grid‑modernization efforts.

Middle East And Africa Transformer Market Report Scope

A transformer is an electrical energy transfer device that either steps up or down the voltage from one alternating-current circuit to one or more other circuits.

The Middle East and Africa Transformer Market report is segmented by power rating, cooling type, phase, transformer type, end-user, and geography. By power rating, the market is segmented into large (above 100 MVA), medium (10 to 100 MVA), and small (up to 10 MVA). By cooling type, the market is segmented into air-cooled and oil-cooled. By phase, the market is segmented into single-phase and three-phase. By transformer type, the market is segmented into power transformers and distribution transformers. By end-user, the market is segmented into power utilities, industrial, commercial, and residential. By geography, the market covers Saudi Arabia, the United Arab Emirates, Qatar, South Africa, Egypt, Nigeria, the rest of the Middle East, and Africa. For each segment, the market sizing and forecasts are based on the revenue (USD Billion).

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

| Air-cooled |

| Oil-cooled |

| Single-Phase |

| Three-Phase |

| Power |

| Distribution |

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| South Africa |

| Egypt |

| Nigeria |

| Rest of Middle East and Africa |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Cooling Type | Air-cooled |

| Oil-cooled | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Transformer Type | Power |

| Distribution | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected revenue for the Middle East and Africa transformer market by 2031?

It is forecast to reach USD 6.38 billion, climbing from USD 5.51 billion in 2026.

Which country currently commands the largest share of transformer demand in the region?

Saudi Arabia led with an 18.5% share in 2025 on the back of Vision 2030 grid expansion.

Which segment is growing fastest within the Middle East and Africa transformer market?

Large units above 100 MVA are expected to post the quickest 4.9% CAGR through 2031.

How are fire-safety regulations influencing transformer technology choices?

Stricter urban codes in Dubai, Doha, and Riyadh are propelling 5.2% annual growth for dry-type transformers.

Why are Asian OEMs winning distribution-class tenders?

Currency advantages, export credit, and local joint ventures allow Asian suppliers to under-price rivals by up to 18%.

What digital trends shape competitive advantage among leading OEMs?

Integrated monitoring platforms like ABB Ability and Siemens Sensformer extend asset life and create recurring service revenue.

Page last updated on: