Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

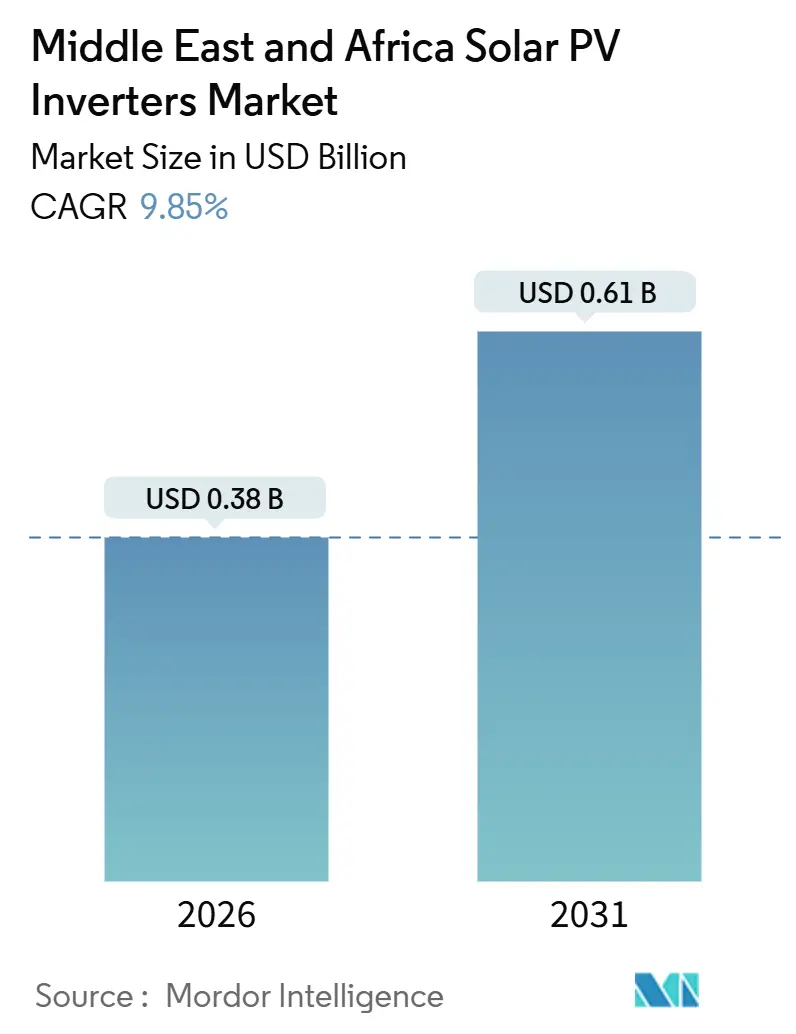

| Market Size (2026) | USD 0.38 Billion |

| Market Size (2031) | USD 0.61 Billion |

| Growth Rate (2026 - 2031) | 9.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Solar PV Inverters Market Analysis by Mordor Intelligence

The Middle East And Africa Solar PV Inverters Market size is estimated at USD 0.38 billion in 2026, and is expected to reach USD 0.61 billion by 2031, at a CAGR of 9.85% during the forecast period (2026-2031).

The expansion reflects a decisive shift away from hydrocarbons toward renewable baseload capacity, encouraged by sovereign-wealth diversification programs in the Gulf and grid-reliability concerns across sub-Saharan economies. Utility-scale tender pipelines, harmonized smart-inverter grid codes, and advances in high-temperature, dust-hardened designs are accelerating equipment turnover, while cost-focused Chinese suppliers and premium European incumbents vie for project awards. Rising residential rooftop adoption, driven by net-metering incentives in Israel and South Africa and chronic grid instability in Nigeria and Egypt, supports the distributed-generation wave. Hybrid inverters are emerging as a preferred solution in weak-grid environments, and cybersecurity requirements embedded in Gulf regulations are reshaping product roadmaps. Supply-chain volatility for power semiconductors and fragmented after-sales networks remain headwinds, yet the overall demand dynamic keeps the Middle East and Africa solar PV inverters market on an upward trajectory.

Key Report Takeaways

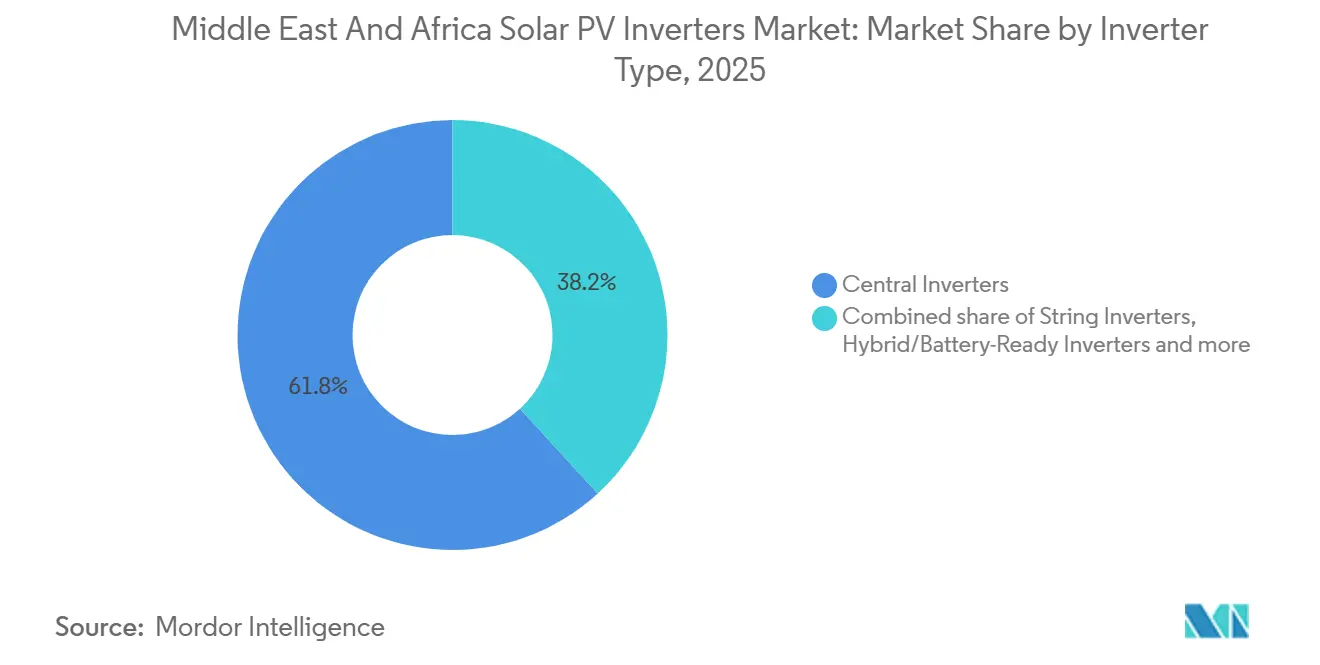

- By inverter type, central inverters commanded 61.8% of the Middle East and Africa solar PV inverters market share in 2025. By inverter type, microinverters are forecast to grow at an 11.1% CAGR to 2031.

- By phase, three-phase units represented 80.1% of 2025 shipments, whereas single-phase devices will rise at a 10.2% CAGR.

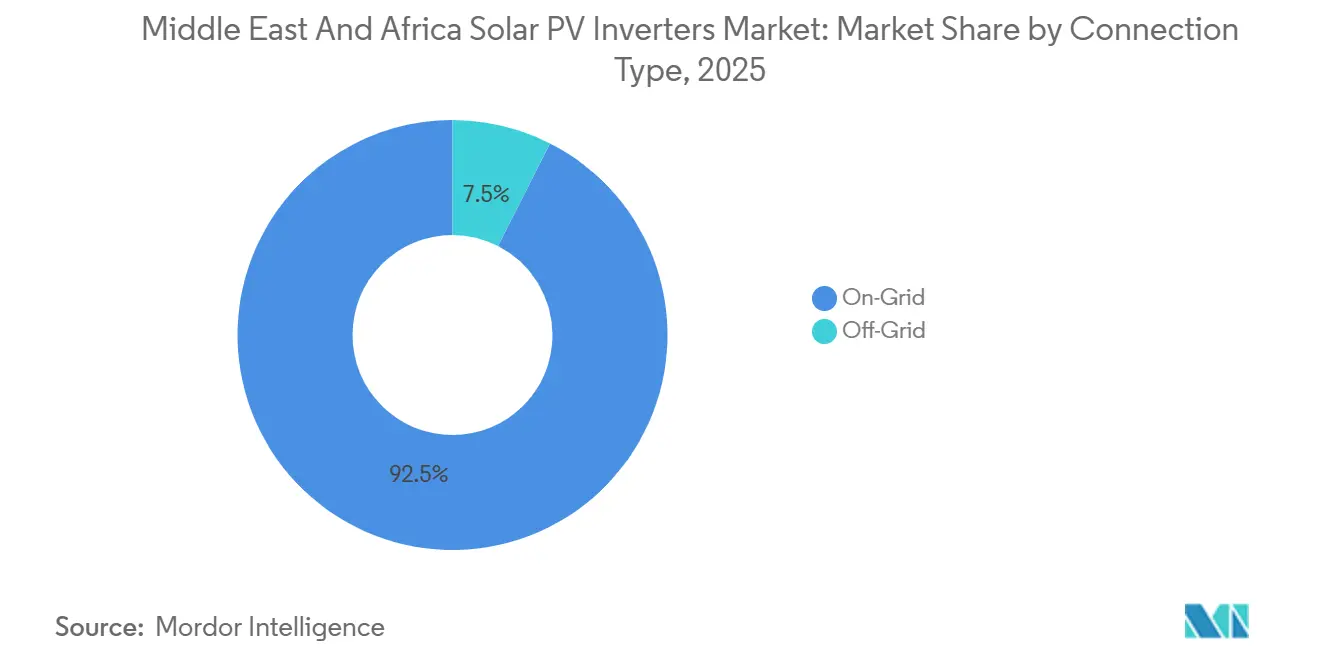

- By connection type, on-grid configurations accounted for 92.5% of 2025 demand, but off-grid systems will post an 11.5% CAGR.

- By application, utility-scale projects held 70.4% of 2025 revenue, while residential installations are projected to expand at a 10.6% CAGR.

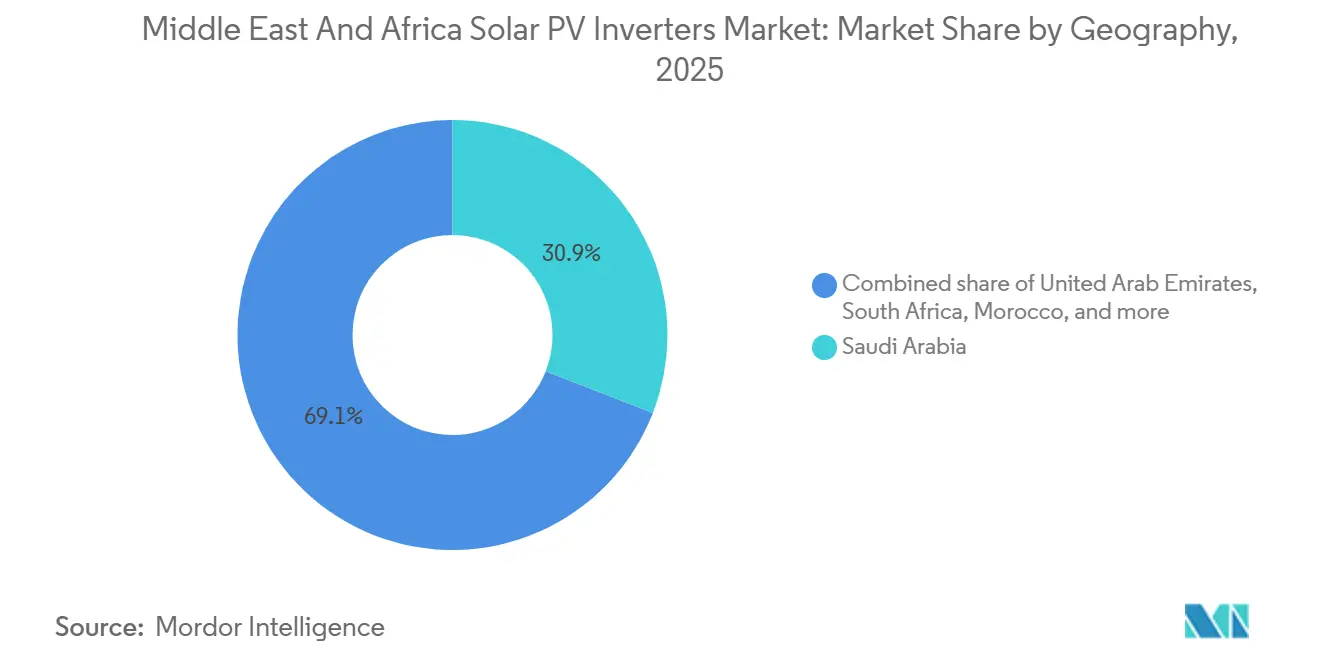

- Saudi Arabia led geography rankings with a 30.9% share in 2025, and the UAE is expected to deliver the fastest 12.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Solar PV Inverters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar-tender pipeline across GCC and North Africa | +2.8% | Saudi Arabia, UAE, Egypt, Morocco, Kuwait | Medium term (2–4 years) |

| Net-metering and rooftop incentives in Israel and South Africa | +1.5% | Israel, South Africa, spillover to Egypt | Short term (≤ 2 years) |

| Mandatory smart-inverter grid codes | +2.1% | Saudi Arabia, UAE, Kuwait, Bahrain | Medium term (2–4 years) |

| High-temperature, dust-hardened designs | +1.7% | Saudi Arabia, UAE, Kuwait, Oman, Egypt, Morocco | Long term (≥ 4 years) |

| Hybrid-inverter demand in weak-grid sites | +2.3% | Nigeria, Egypt, South Africa, Kenya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Solar-Tender Pipeline Across GCC and North Africa

Government-backed solar solicitations topped 25 GW of announced capacity during 2025, anchored by Saudi Arabia’s Public Investment Fund pledge of USD 8.3 billion for 15 GW of projects with ACWA Power and Masdar partners.[1]Public Investment Fund, “PIF Launches Renewable Projects,” pif.gov.sa A 2 GW solar-plus-storage award from Dubai Electricity and Water Authority in late 2024 and Abu Dhabi’s Zarraf and Khazna projects, each at 1.5 GW, reinforce predictable utility-scale demand for central inverters. Contract structures increasingly bundle operations, maintenance, and local assembly, trimming margins for pure-play hardware vendors yet deepening market stickiness for integrated suppliers. Kuwait’s 1.1 GW Al Dibdibah plant entering commercial service in 2024 and Egypt’s 1.2 GW Infinity Power financing round magnify the multi-country pull for grid-connected equipment. The resulting procurement certainty underpins utility developers’ preference for suppliers with bankable product warranties and sovereign-grade service footprints.

Net-Metering and Rooftop Incentives in Israel and South Africa

Israel’s feed-in tariff and net-metering rules covering systems up to 50 kW lifted residential solar penetration to 8% of eligible rooftops in 2025, doubling the 2023 level. South Africa’s municipal programs allow commercial sites to offset Eskom tariff hikes that averaged 12% annually during 2020–2025, while 2024 Electricity Regulation Act amendments cut grid-connection approvals for sub-1 MW arrays from 18 months to 6 months. These measures steer demand toward string and microinverters, whose modular architectures cope with shading and orientation constraints common on rooftops. Financiers and installers report that falling balance-of-system costs have brought five-year paybacks within reach for households and malls, substantially widening the total addressable market for distributed inverters.

Mandatory Smart-Inverter Grid Codes

Saudi Arabia’s Grid Code 2024 obliges all inverters above 500 kW to furnish dynamic reactive-power support, ride-through voltage dips beyond 30%, and respond to frequency deviations within 200 ms.[2]National Grid SA, “Saudi Grid Code 2024,” ngsa.com.sa Gulf Cooperation Council standards IEC 62116:2024, IEC 61727:2014, and IEC 62934:2024 formalize anti-islanding, interconnection, and power-quality norms, prompting firmware redesigns and hardware upgrades that raise bill-of-materials by 8–12%. The UAE and Kuwait adopted comparable rules in 2025, narrowing the competitive field to suppliers with pre-certified smart-grid features. Incumbents SMA and Schneider Electric benefit from prior European deployments, whereas cost-focused entrants must allocate roughly USD 500,000 per product line for full compliance testing.

High-Temperature, Dust-Hardened Designs Lowering O&M Costs

Summer ambient temperatures topping 50 °C and high particulate loads cut inverter efficiency by up to 15% annually without specialized enclosures, according to a 2024 King Abdulaziz University study.[3]King Abdulaziz University, “Impact of High Temperatures on PV Inverters,” kau.edu.sa Sungrow’s 1+X 2.0 platform, introduced in 2025, maintains rated output at 52 °C with IP66 protection, and SolarEdge’s temperature-derating algorithm holds 95% output at 45 °C. Both Huawei and Fronius deployed active-cooling systems that extend the mean time between failures from 15 years to 20 years in desert climates. Lower unplanned maintenance visits improve project bankability for utility developers bound by performance-based power-purchase agreements, reinforcing the appeal of ruggedized designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor supply-chain volatility | −1.4% | UAE, Saudi Arabia, South Africa | Short term (≤ 2 years) |

| Fragmented after-sales and certification | −0.9% | Nigeria, Egypt, Morocco, Kenya | Medium term (2–4 years) |

| Cybersecurity concerns over remote access | −0.6% | Saudi Arabia, UAE, Israel | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility

Insulated-gate bipolar transistors and silicon-carbide MOSFET lead times stretched to 8–12 weeks in early 2025, deferring project commissioning and inflating working-capital requirements. SMA Solar Technology disclosed a 15% shipment shortfall in 1H 2024 owing to chip shortages.[4]SMA Solar Technology, “Annual Report 2024,” sma.de Huawei countered by securing multi-year wafer contracts, but smaller firms lacking scale endured spot-market price spikes that complicated fixed-price EPC bids.

Fragmented After-Sales and Certification Ecosystem

Average inverter-replacement lead times exceeded six weeks in Nigeria, Egypt, and Morocco during 2024, mainly due to limited spares and certified technicians, according to the African Solar Industry Association. Disparate national standards, SANS 62109 in South Africa, EOS approvals in Egypt, NF rules in Morocco, force manufacturers to fund multiple product variants, adding 15–20% to compliance costs and slowing market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inverter Type: Central Inverters Anchor Utility Procurement

Central inverters captured 61.8% of the Middle East and Africa solar PV inverters market in 2025, a dominance linked to megawatt-scale projects in Saudi Arabia and the UAE that prioritize low installed cost per watt. String inverters serve commercial and industrial arrays where modularity outweighs minimal cost savings, while microinverters secured double-digit growth thanks to rooftop uptake in Israel and South Africa. Hybrid and battery-ready models add value in Nigeria and Egypt, where load-shedding propels storage integration. The shift toward bifacial modules and 2,000-V system architectures further tilts procurement toward string and central platforms engineered for higher input voltages.

Central inverters simplify interconnection studies yet represent single points of failure, creating openings for multi-MPPT string units in terrains with variable irradiance. Microinverters, though costlier, deliver module-level optimization and enhanced safety, but their complexity limits utility-scale prospects. Hybrid units bridge the gap between on-grid and off-grid needs, dovetailing with tariff structures that reward time-of-use arbitrage. As bifacial and high-voltage trends mature, legacy 1,000-V equipment faces obsolescence, stimulating replacement sales across the Middle East and Africa solar PV inverters market.

By Phase: Three-Phase Configurations Reflect Commercial Bias

Three-phase units comprised 80.1% of 2025 shipments, mirroring the prevalence of commercial, industrial, and utility installations requiring balanced load distribution. Single-phase products, typically under 10 kW, will climb at a 10.2% CAGR as rooftop solar permeates middle-income housing in Israel, South Africa, and Egypt.

Cost-effective plug-and-play single-phase kits entice residential do-it-yourself segments, while three-phase devices must meet stricter harmonic limits, such as the Saudi Electricity Company’s 5% THD cap. Consequently, three-phase vendors invest in active filtering and grid-synchronization algorithms, raising entry barriers but enhancing grid compliance credentials in the Middle East and Africa solar PV inverters industry.

By Connection Type: On-Grid Dominance Conceals Off-Grid Potential

On-grid architectures held 92.5% of 2025 demand, yet off-grid systems are projected to enjoy an 11.5% CAGR as rural electrification programs proliferate in Nigeria, Kenya, and Ethiopia. On-grid units enable bidirectional flow under net-metering, whereas off-grid solutions manage batteries and local loads autonomously.

High diesel prices above USD 0.30 per kWh and costly grid extensions exceeding USD 10,000 per km underpin solar-plus-storage economics, boosting off-grid installations that already serve 1.2 million Nigerian households. Grid-tied markets such as Israel face saturation constraints, prompting inverter makers to court off-grid niches with robust hybrid offerings, thereby broadening the addressable field for the Middle East and Africa solar PV inverters market.

By Application: Utility-Scale Dominance Masks Residential Momentum

Utility-scale plants held 70.4% of 2025 revenue, reflecting large tenders backed by sovereign offtake guarantees in Saudi Arabia, the UAE, and Egypt. Residential arrays, however, are forecast to post a 10.6% CAGR, buoyed by net-metering in Israel and South Africa and by households in Nigeria seeking relief from unreliable grids. Commercial and industrial customers sit between these poles, exploiting accelerated depreciation and demand-charge reductions.

Land-acquisition and grid-interconnection hurdles can push utility project timelines out 18 months, whereas rooftop systems deploy within weeks, offering faster realization of energy savings. A 2024 African Development Bank study showed South African commercial arrays now achieve four-to-six-year paybacks, catalyzing demand for inverters with integrated energy-management software. Collectively, these factors diversify revenue streams in the Middle East and Africa solar PV inverters market and insulate suppliers from over-reliance on utility awards.

Geography Analysis

Saudi Arabia secured 30.9% of 2025 revenue, propelled by Vision 2030’s 58.7 GW renewable target and robust procurement pipelines awarding central-inverter contracts under long-term PPAs. The Saudi Grid Code 2024 raises technical barriers, steering awards toward vendors with proven dynamic-support features. The UAE is the fastest-growing geography at a 12.4% CAGR, riding on Dubai’s 2 GW solar-plus-storage award and Abu Dhabi’s 3 GW Zarraf and Khazna projects. Harmonized IEC standards simplify certification for European incumbents while incentivizing Chinese suppliers to localize assembly.

South Africa leverages municipal net-metering and double-digit Eskom tariff escalations to push commercial rooftops beyond 300 MW in 2025, favoring string and microinverters. Egypt advanced a 1.2 GW solar-plus-storage financing round and benefits from strong development-finance support, while Morocco edges toward commercial operation of Noor Midelt hybrids. Nigeria’s off-grid capacity hit 1.2 GW in 2025, with hybrid inverters taking a 60% share amid chronic outages. Kuwait, Bahrain, Oman, Kenya, and Ethiopia together contributed 15% of the 2025 demand, offering incremental growth through utility projects and rural electrification schemes.

Overall, Gulf sovereign wealth capital ensures steady utility-scale momentum, whereas distributed generation flourishes in markets with permitting reforms and tariff pressures. This geographic mosaic confirms that no single inverter platform suffices for the entire Middle East and Africa solar PV inverters market, compelling manufacturers to maintain diversified portfolios and service models.

Competitive Landscape

Market concentration is moderate, with Huawei and Sungrow exploiting economies of scale to price aggressively in utility bids, while SMA, Fronius, and Schneider Electric defend premium niches via advanced grid-support and cybersecurity features. Chinese suppliers are establishing regional assembly plants to satisfy Saudi and UAE local-content quotas, pressuring margins for pure-play hardware vendors. Joint ventures between European firms and EPC contractors seek to preserve share through integrated service offerings.

Software differentiation gains importance as Saudi and UAE codes demand sub-200 ms frequency response. Huawei’s 87 grid-forming patents and AI-enabled diagnostics hint at a shift toward software-defined power electronics. IEC 62934:2024 harmonizes compliance testing, lowering procedural barriers for smaller brands yet imposing capital outlays for laboratories. IEC 62443 cybersecurity certification, mandatory in Gulf tenders, favors incumbents with mature security frameworks and complicates entry for cost-focused challengers.

White-space opportunities include hybrid inverters for weak-grid markets and microinverters for rooftop applications. Regional integrators bundling hardware with performance guarantees erode standalone hardware margins. As local-content and cybersecurity rules tighten, suppliers that combine manufacturing footprints with digital services stand best placed to capture value in the Middle East and Africa solar PV inverters market.

Middle East And Africa Solar PV Inverters Industry Leaders

Huawei Technologies

Sungrow Power Supply

SMA Solar Technology

SolarEdge Technologies

FIMER SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Sineng Electric has made significant strides in the Middle East and Africa, sealing a deal to supply 4GW of photovoltaic (PV) inverters for Phase 6 of the Saudi PIF Solar Power Plant Project.

- November 2025: The Iranian Energy Ministry's renewables division, SATBA, announced its collaboration through a memorandum of understanding (MoU) with the presidential office for science and technology, emphasizing the commitment to local solar inverter production.

- October 2024: Sungrow, a global leader in PV inverters and energy storage systems, is supplying inverters for a 60MWp solar PV plant. Emerge, a joint venture of Masdar and EDF, is developing the plant for the Sharjah National Oil Corporation (SNOC). Al Mustakbal Clean Tech has been awarded the project as the EPC contractor, and the plant is poised to be Sharjah’s largest solar power facility.

Middle East And Africa Solar PV Inverters Market Report Scope

Solar PV inverters are power inverters that change the electricity produced by photovoltaic (PV) solar panels from direct current (DC) to alternating current (AC) at utility frequency. This can be applied to local off-grid electrical networks like microgrids or electrical grids for homes and businesses.

The Middle East and Africa solar PV inverters market is segmented by inverter type, phase, connection type, application, and geography. By inverter type, the market is segmented into central, string, microinverters, and hybrid/battery-ready. By phase, the market is segmented into single-phase and three-phase. By connection type, the market is segmented into on-grid and off-grid. By application, the market is segmented into residential, commercial and industrial, and utility-scale. The report also covers the market size and forecasts for the Middle East and Africa solar PV inverters market across major countries. The market size and forecasts for each segment are based on revenue (USD).

By Inverter Type

| Central Inverters |

| String Inverters |

| Microinverters |

| Hybrid/Battery-Ready Inverters |

By Phase

| Single-Phase |

| Three-Phase |

By Connection Type

| On-Grid |

| Off-Grid |

By Application

| Residential |

| Commercial and Industrial |

| Utility-Scale |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Iran |

| South Africa |

| Egypt |

| Nigeria |

| Morocco |

| Rest of Middle East and Africa |

| By Inverter Type | Central Inverters |

| String Inverters | |

| Microinverters | |

| Hybrid/Battery-Ready Inverters | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Connection Type | On-Grid |

| Off-Grid | |

| By Application | Residential |

| Commercial and Industrial | |

| Utility-Scale | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Iran | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Morocco | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What growth rate is expected for inverter demand in the Middle East and Africa through 2031?

The market is forecast to post a 9.85% CAGR between 2026 and 2031, rising from USD 380 million in 2026 to USD 610 million by 2031.

Which segment currently dominates inverter sales?

Utility-scale applications led with a 70.4% revenue share in 2025 because of large tenders in Saudi Arabia and the UAE.

Why are hybrid inverters gaining popularity?

Chronic grid outages in Nigeria and Egypt and falling battery costs make hybrid units attractive for seamless solar-plus-storage operation.

Which country will grow fastest in inverter adoption?

The UAE is projected to achieve a 12.4% CAGR through 2031, supported by multi-gigawatt solar-plus-storage projects.

How are new grid codes affecting product design?

Saudi and UAE regulations now mandate dynamic reactive-power, low-voltage ride-through, and rapid frequency response, prompting manufacturers to integrate advanced control firmware and higher-cost components.

What supply-chain risk worries inverter makers most?

Limited availability of power semiconductors, particularly silicon-carbide devices, stretches lead times and complicates fixed-price project bids.

Page last updated on: