Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.4 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Transformer Market Analysis by Mordor Intelligence

Canada Transformer Market size in 2026 is estimated at USD 1.04 billion, growing from 2025 value of USD 0.98 billion with 2031 projections showing USD 1.4 billion, growing at 6.14% CAGR over 2026-2031.

This momentum aligns with federal plans to invest more than CAD 60 billion (USD 45 billion) in clean-power assets over the next decade and to achieve net-zero grid emissions by 2035.(1)Natural Resources Canada, “Powering Canada’s Future: A Clean Electricity Strategy,” NATURAL-RESOURCES.CANADA.CA Canada's transformer market growth is further reinforced by projections that national electricity output will need to more than double by 2050 to service electrification across transportation, industry, and heating. Medium-power units currently dominate the market due to distribution utility upgrades; however, large transformers above 100 MVA represent the fastest-growing category as renewable megaprojects demand higher ratings. Federal tax credits covering 15% of eligible transmission investments, alongside a CAD 3 billion (USD 2.3 billion) Smart Renewables fund, anchor steady procurement lines for manufacturers. Canada's transformer market participants are also responding to load-center densification, where air-cooled units are gaining favor for data centers and urban settings, even though oil-cooled equipment still holds the leadership.

Key Report Takeaways

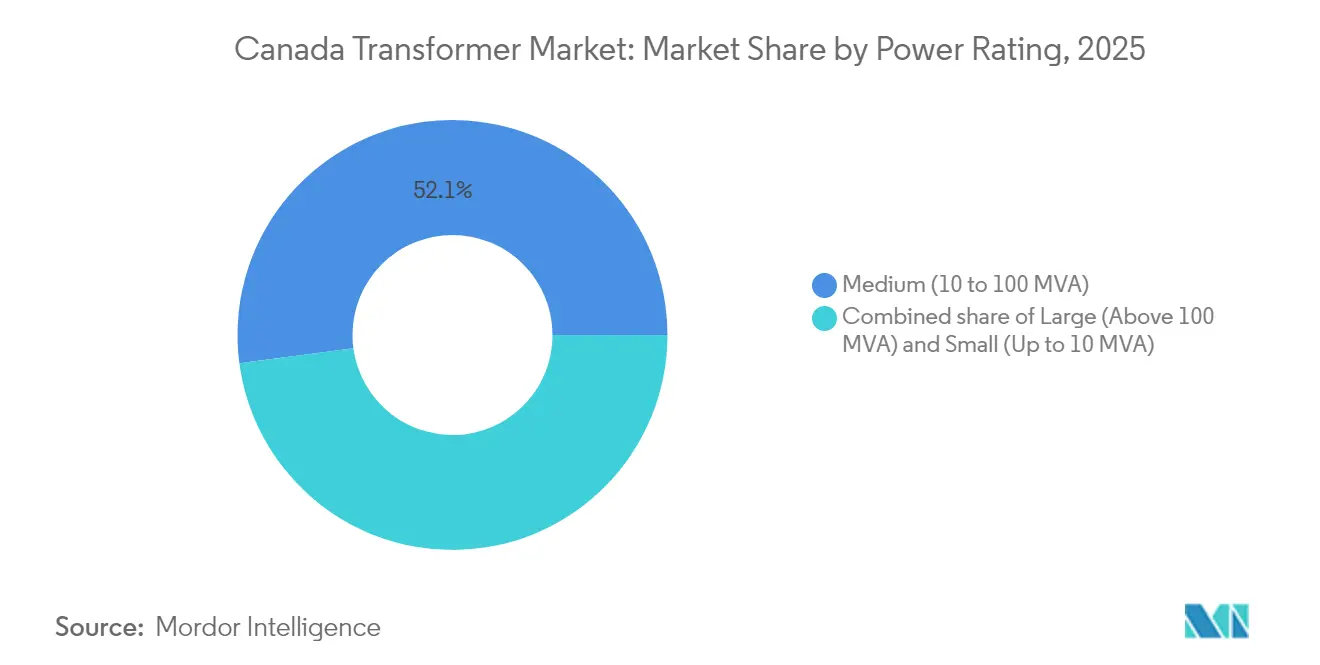

- By power rating, medium-power transformers held a 52.10% revenue share in 2025, while large-power units are projected to record the fastest growth of 6.74% CAGR through 2031.

- By cooling type, oil-cooled designs captured 62.20% of Canada's transformer market share in 2025; however, air-cooled counterparts are set to advance at a 6.93% CAGR to 2031.

- By phase, three-phase equipment commanded a 73.60% share of the Canadian transformers market size in 2025 and is forecast to grow at a 7.22% CAGR during 2026-2031.

- By transformer type, distribution transformers accounted for 59.10% of the Canada transformer market size in 2025, whereas power transformers show lower volumes but higher ticket prices.

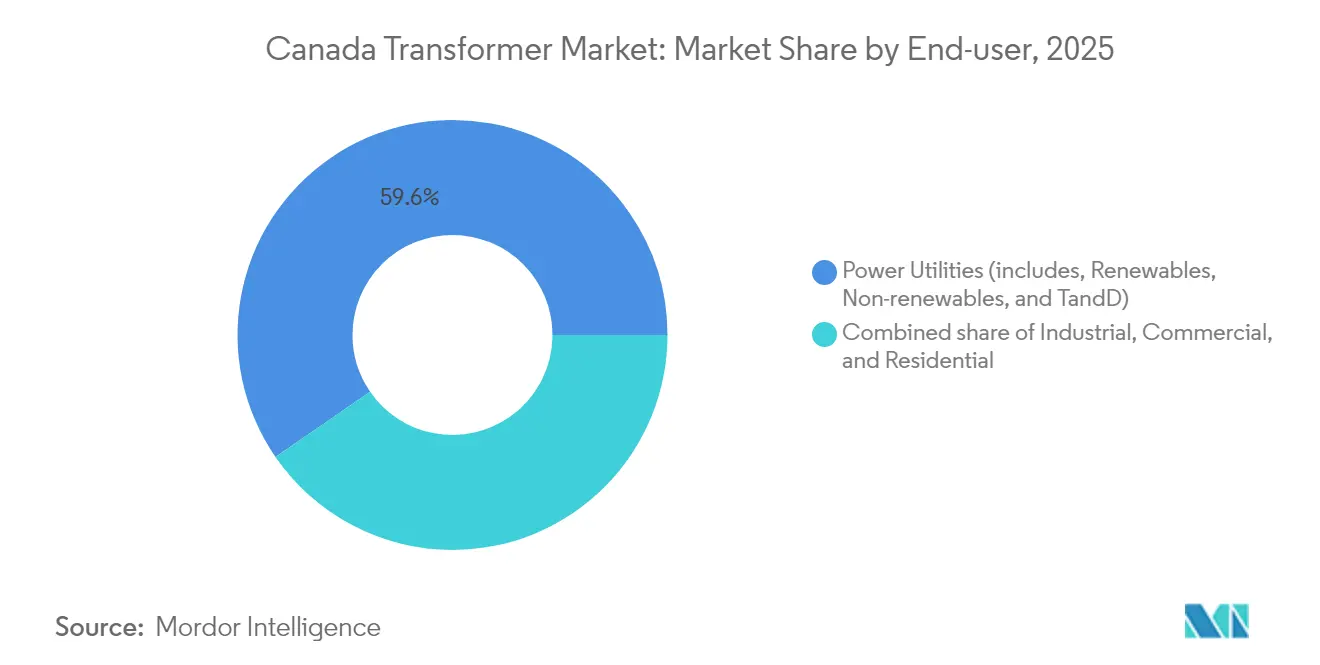

- By end-user, utilities remained the top spenders with a 59.60% share in 2025; however, industrial customers are poised for the sharpest growth, with a 7.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electricity demand and grid-modernization programs | 2.1% | National, concentrated in Ontario, Quebec, Alberta | Medium term (2-4 years) |

| Surge in renewable-energy interconnections | 1.8% | Western provinces, spill-over to Atlantic Canada | Short term (≤ 2 years) |

| Federal "Clean Electricity Regulations" incentivising T-D upgrades (proposed 2025) | 1.5% | National excluding territories | Long term (≥ 4 years) |

| Electrification of heavy industries in Western Canada (steel, mining, LNG) | 1.2% | Alberta, Saskatchewan, British Columbia | Medium term (2-4 years) |

| Utility-led adoption of digital twin-enabled transformers (under-reported) | 0.8% | Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Micro-grid deployments in Indigenous & remote communities (under-reported) | 0.6% | Northern territories, remote First Nations communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Clean Electricity Regulations Drive Unprecedented Infrastructure Investment

Canada’s Clean Electricity Regulations, published in December 2024, require all generating units of at least 25 MW that connect to the North American grid to meet annual intensity limits of 65 tCO₂/GWh from 2035 and zero after 2050.(2)Environment and Climate Change Canada, “Clean Electricity Regulations: SOR/2024-263,” CANADA.CA Asset owners therefore face a mandatory retirement or retrofit pathway that boosts demand for replacement high-voltage and medium-voltage transformers throughout the Canada transformers market. Federal modeling indicates 181 Mt CO₂e of cumulative abatement by 2050, necessitating vast transmission additions so that renewable projects in resource-rich regions can move power to urban load hubs. A CAD 25.7 billion (USD 19.3 billion) investment-tax-credit pool accelerates procurement schedules, though prevailing-wage clauses tighten labor supply and raise project budgets, prompting utilities to prefer manufacturers with domestic footprints.

Renewable Integration Accelerates Large Transformer Demand

Federal clean-power programs already back 2,700 MW of new renewables and 2,100 MWh of storage, and upcoming procurements in British Columbia, Ontario, and Quebec total 17.5 GW. Each wind or solar block requires step-up transformers in the 90-200 MVA, 240/34.5 kV range. The North American Electric Reliability Corporation recommends 12-14 GW of fresh interprovincial links to mitigate extreme-weather blackouts, translating into larger HV units and converter step-ups. These project clusters provide the Canadian transformers market with strong forward visibility and encourage manufacturers to expand their domestic test bays, capable of certifying 800 kV class equipment.(3)Hitachi Energy, “Hitachi Energy Announces Modernization of Power Transformer Factory,” HITACHIENERGY.COM

Digital Twin Technology Adoption Enhances Asset Management

Hydro-Québec’s CAMP program links sensor-equipped transformers into a real-time twin, which reduced unplanned outages during the summer peak of 2025 by 14%. Utilities in Ontario and British Columbia replicate the model, requesting embedded fiber-optic winding temperature probes, dissolved gas analyzers, and LTE gateways in new units. Natural Resources Canada’s Digital Utility Platform in Cobourg demonstrates how load-flow analytics identify overloaded transformers and trigger preventive dispatch.(4)Natural Resources Canada, “Powering Canada’s Future: A Clean Electricity Strategy,” NATURAL-RESOURCES.CANADA.CA Adoption barriers include retrofit costs for legacy fleets, data-serialization gaps, and the need for cybersecurity compliance across provincial regimes. Even so, bid specifications now routinely mandate digital-ready features, fostering a smart-equipment premium inside the Canada transformers market.

Supply Chain Bottlenecks Constrain Market Growth

Average transformer lead times have increased from 50 weeks in 2020 to nearly two years for units exceeding 100 MVA. Canada exports approximately 47% of U.S. laminated stacked cores, but domestic grain-oriented electrical steel (GOES) still fails to meet surging needs.(5)U.S. Department of Energy, “Large Power Transformers and HVDC Systems Supply Chain Deep-Dive,” ENERGY.GOV With copper prices 60-80% higher than five years ago, overall transformer pricing has risen at similar rates. Skilled manufacturing labor is also scarce, particularly for coil winding and brazing specialties, which are concentrated in Ontario and Quebec factories. These constraints shave roughly 0.9 percentage points from the attainable CAGR of the Canada transformers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long permitting cycles for new high-voltage substations | -1.2% | National, with delays concentrated in Ontario, Alberta | Short term (≤ 2 years) |

| Supply-chain bottlenecks in grain-oriented electrical steel | -0.9% | Global, with spillover to Canadian manufacturing | Medium term (2-4 years) |

| Exchange-rate volatility impacting imported core components (under-reported) | -0.6% | National, particularly affecting import-dependent manufacturers | Short term (≤ 2 years) |

| Scarcity of skilled transformer-design engineers in Canada (under-reported) | -0.5% | Ontario, Quebec manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Approval Delays Impact Project Timelines

Major switching stations need certificates from provincial regulators, environmental clearances, and Indigenous consultations. Nova Scotia Power’s NS-NB Reliability Intertie, which includes a 345 kV substation rebuild, illustrates the typical 2-3 year wait between filing and groundbreaking. Lengthy reviews defer transformer procurement and inflate carrying costs for utilities, removing roughly 1.2 percentage points from the five-year CAGR potential of the Canada transformers market.

Skilled Labor Shortages Threaten Manufacturing Capacity

Roughly one-third of Canada’s journey-level transformer trade workers will retire within five years. Although federal apprenticeship incentives reach CAD 17,000 (USD 12,700) per hire, the pipeline remains thin. Manufacturers must raise wages and invest in automated coil-winding, moves that can lift unit costs and constrain delivery schedules for the Canadian transformers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Large Transformers Lead Growth Despite Medium Dominance

Medium-power units, ranging from 10 MVA to 100 MVA, held the largest slice of Canada's transformer market share in 2025, driven by distribution utility replacements and industrial service upgrades. Orders in the 40-60 MVA range increased sharply after utilities introduced loop schemes to enhance redundancy, and smaller municipalities opted for 25 MVA units to facilitate feeder reconfiguration. Despite this dominance, the Canada transformers market size for large-power equipment (>100 MVA) is forecast to rise 6.74% annually to 2031 as renewable megaprojects require 120-200 MVA step-ups.

Large-scale growth is evident in Alberta wind contracts and Ontario long-term resource plans, which together specify more than 30 units exceeding 150 MVA through 2028. Supply constraints mean lead times stretch up to four years, forcing buyers to secure slots early and often from the Varennes facility or U.S. plants that recently added 800 kV bays. This dynamic positions large-transformer makers for margin upside while driving consortium bids that bundle financing and service warranties in the Canada transformers market.

By Cooling Type: Air-Cooled Growth Accelerates Urban Applications

Oil-cooled transformers retained a 62.20% share of the Canada transformers market in 2025 because they achieve higher power density, support overload cycles, and fit existing substation footprints. Utilities still prefer oil for bulk systems, but stringent fire-protection and spill-containment rules introduced in 2024 increase secondary costs. The alternative air-cooled segment—comprising cast-resin and ventilated dry-type designs—will notch a 6.93% CAGR by 2031 as data-center clusters in Toronto, Montréal, and Vancouver demand equipment that meets low-smoke and confined-space codes.

End-users also favor air-cooled transformers for temporary feeders, underground vaults, and modular micro-grids where oil pans are impractical. Cast-resin cores rated at 2.5-10 MVA are the dominant choice for these applications. Suppliers refine epoxy formulations to handle tropical storage and rapid load changes, thereby expanding the addressable revenue for air-cooled producers within the Canadian transformers market.

By Phase: Three-Phase Dominance Reflects Grid Architecture

Three-phase transformers represented 73.60% of the Canadian transformers market size in 2025, a figure that is expected to increase as utilities decommission aging single-phase banks in favor of integrated units. Advantages include smaller footprints, factory-calibrated impedance balance, and simplified protection schemes. The segment’s anticipated 7.22% CAGR rests on bulk procurement programs tied to the Clean Electricity Regulations.

Single-phase demand holds in rural feeders and certain industrial processes; however, its share continues to erode as municipalities convert overhead reconstruction projects to three-phase backbone structures. Manufacturers address residual single-phase demand through standard designs ranging from 167 kVA to 500 kVA; however, investment emphasis remains on three-phase innovations, such as flux-shunted cores and lower no-load losses, for the Canadian transformers market.

By Transformer Type: Distribution Segment Leads Utility Modernization

Distribution transformers captured 59.10% of the Canadian transformer market share in 2025, driven by accelerated pole-top and pad-mount replacement plans. Federal grid-modernization grants support voltage conversion from 4.16 kV to 13.8 kV in small towns, stimulating orders for 50 kVA to 167 kVA units with amorphous-metal cores. Upgraded CSA C802.3 efficiency rules, effective 2025, further drive swap-outs of legacy silicon-steel cores, adding volume to the distribution category.

While power-transformer volumes are lower, average selling prices can exceed USD 4 million for 300 MVA autotransformers, contributing materially to the overall Canada transformers market size. Domestic fabrication remains limited to a single plant, so utilities secure positions at least 36 months in advance. This gap sparks interest in joint-venture factories that could localize production of 230 kV-400 kV class if demand persists.

By End-User: Industrial Growth Outpaces Utility Segment

Utilities booked 59.60% of transformer spending in 2025, driven by aging infrastructure; however, industrial customers—from miners to AI data center operators—will grow the fastest at a 7.58% CAGR to 2031. The mining electrification wave in British Columbia and Alberta favors mobile 25-40 MVA skid packages with onboard harmonic filters. Data-center investors specify redundant dry-type units fed from ring banks to maintain Tier IV uptime.

Commercial office retrofits are migrating toward smaller, high-efficiency pad-mounts that comply with noise ordinances, while residential heat-pump uptake is pushing distribution utilities to reinforce split-phase service transformers. Together, these shifts diversify revenue streams and enhance resilience against regulatory delays in the Canada transformers market.

Geography Analysis

Ontario remains the largest provincial buyer, underpinned by Hydro One's CAD 11.8 billion (USD 8.8 billion) capital plan through 2027, which allocates roughly CAD 900 million (USD 675 million) annually to station rebuilds and distribution hardening. Projects such as the CAD 1.2 billion (USD 900 million) East-West Tie spur high-voltage transformer demand, and automotive battery factories in Windsor add mid-range substation orders. Ontario's grid-integration roadmap estimates 650 MVA of incremental transformer capacity per year through 2030, positioning the province as a central player in Canada's transformer market opportunities.

Quebec functions as both a production hub and a major demand center. Hitachi Energy's Varennes plant, which underwent a CAD 140 million (USD 105 million) upgrade in 2024, can now build and test single-unit ratings of up to 1,200 MVA. Hydro-Québec's plan to add 3,900 MW of hydro and wind capacity by 2030 necessitates large-scale step-ups and converter transformers. Provincial incentives also foster digital-twin pilots that utilize advanced sensors and communication modules, reinforcing technology leadership and underscoring Quebec's strategic role in the Canadian transformers market.

Western provinces record the fastest growth. Alberta's competitive renewables auction pipeline exceeds 6 GW, while British Columbia's 5 GW wind procurement and Site C megaproject call for multiple 240/34.5 kV and 500/230 kV transformers. Cross-border power-export ambitions and energy storage rollouts add further pull. Although the volumes in Manitoba and Saskatchewan are smaller, interconnection plans, such as the Kivalliq Hydro-Fibre Link, introduce new high-voltage corridors that are expected to raise transformer needs by the late 2020s. Collective western demand is projected to represent roughly 29.20% of the Canada transformers market size by 2031, up from 22.60% in 2025.

Competitive Landscape

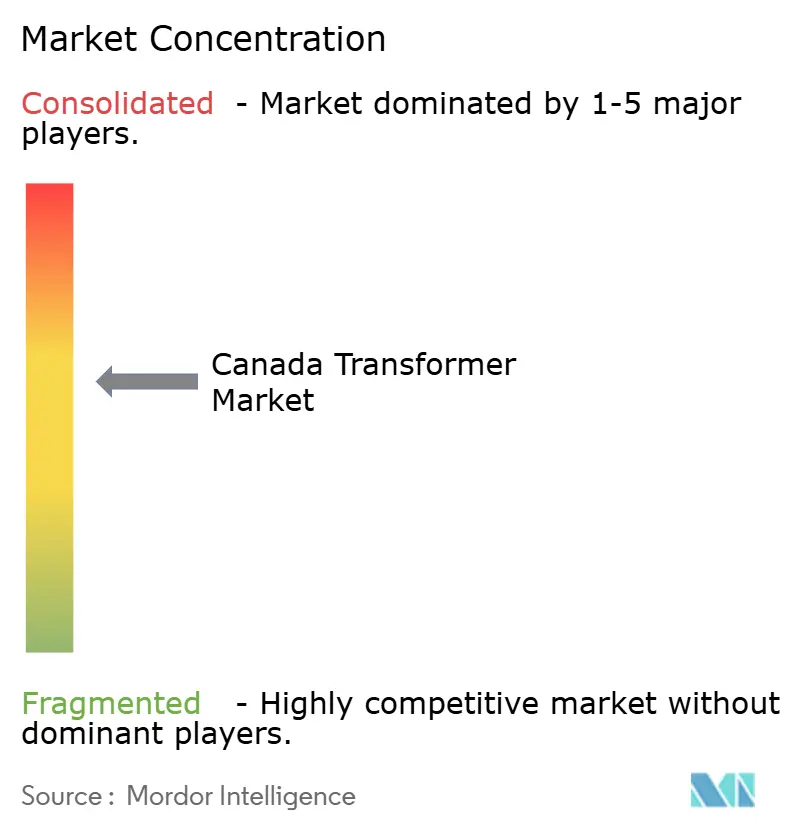

The Canada transformer market exhibits moderate concentration. The five largest vendors control an estimated 60% of national revenue, with recent mergers tightening capacity in distribution grades. Central Moloney’s February 2024 purchase of Cam Tran formed a 1,000-employee network across eight plants, giving the group scale in amorphous-core production while retaining dual branding. The combined entity now markets rapid-ship 50-kVA pole units under 12-week delivery commitments that appeal to rural utilities facing storm rebuilds.

Hitachi Energy holds the pole position for high-voltage and HVDC transformers thanks to its Varennes complex. The 130,000-square-foot high-voltage test bay, added in 2025, trims certification lead times by several months, making the plant the only North American site that can type-test 800 kV equipment locally. The company followed up with a USD 250 million global expansion in 2025, allocating roughly 40% of the funds to North American facilities that support Canadian orders.

Domestic independents such as PTI Transformers, Atlas Transformer, and Niagara Transformer compete on customization and after-sales service. Their core proposition lies in manufacturing agility—encompassing short runs, quick design changes, and bilingual field crews. Yet, they face rising input costs and must navigate the scarcity of GOES Partnerships. However, joint material purchasing and recycling programs with utilities help partly offset volatile steel prices. Overall, strategic investments and supply-chain integration maintain competitive intensity at a high level, enabling customers to diversify risk while still achieving lifecycle support within Canada.

Canada Transformer Industry Leaders

Siemens AG

Schneider Electric SE

ABB Ltd

Hammond Power Solutions Inc

Hitachi Energy Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy has earmarked an additional USD 250 million for global capacity, dedicating over 40% of this amount to North American transformer lines that will serve Canadian utilities.

- February 2025: CG Power and Industrial Solutions sold its Canadian Power Transformer business to PTI Holdings Corporation, continuing the restructuring of its parent's footprint.

- December 2024: Environment and Climate Change Canada finalized the Clean Electricity Regulations, locking in net-zero grid mandates by 2035 and extending 15% refundable tax credits on transmission and distribution projects.

- April 2024: Hitachi Energy announced a CAD 140 million (USD 105 million) modernization of its Varennes factory, including a 130,000 sq ft high-voltage test facility slated for completion in 2027.

- February 2024: Central Moloney acquired Cam Tran, forming one of North America’s largest distribution and transformer producers while maintaining both brand identities.

Canada Transformer Market Report Scope

A transformer is an electrical device that transfers energy from one electric circuit to another using the electromagnetic induction principle. It is intended to change the AC voltage between the circuits while keeping the current's frequency constant.

The Canadian transformers market is segmented by power rating, cooling type, and transformer type. By power rating, the market is segmented into large, medium, and small. By cooling type, the market is segmented into oil-cooled and air-cooled). By transformer type, the market is segmented into power transformer and distribution transformer.

For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Cooling Type

| Air-cooled |

| Oil-cooled |

By Phase

| Single-Phase |

| Three-Phase |

By Transformer Type

| Power |

| Distribution |

By End-User

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Cooling Type | Air-cooled |

| Oil-cooled | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Transformer Type | Power |

| Distribution | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current value of the Canada transformers market?

It stood at USD 1.04 billion in 2026 and is projected to reach USD 1.4 billion by 2031.

How fast is transformer demand growing across Canada?

The market is forecast to post a 6.14% CAGR from 2026 to 2031, aided by clean-power investments and grid upgrades.

Which transformer segment is expanding the quickest?

Large-power units above 100 MVA are expected to grow at a 6.74% CAGR through 2031, mainly for utility-scale renewable interconnections.

Why are air-cooled transformers gaining traction in Canada?

Data-center buildouts and urban substation space limits are driving adoption of dry-type or cast-resin units that avoid oil-spill compliance burdens.

How are federal regulations affecting transformer procurement?

The Clean Electricity Regulations mandate net-zero grid emissions by 2035 and offer 15% tax credits on transmission projects, accelerating purchases of both distribution and high-voltage transformers.

Page last updated on: