Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

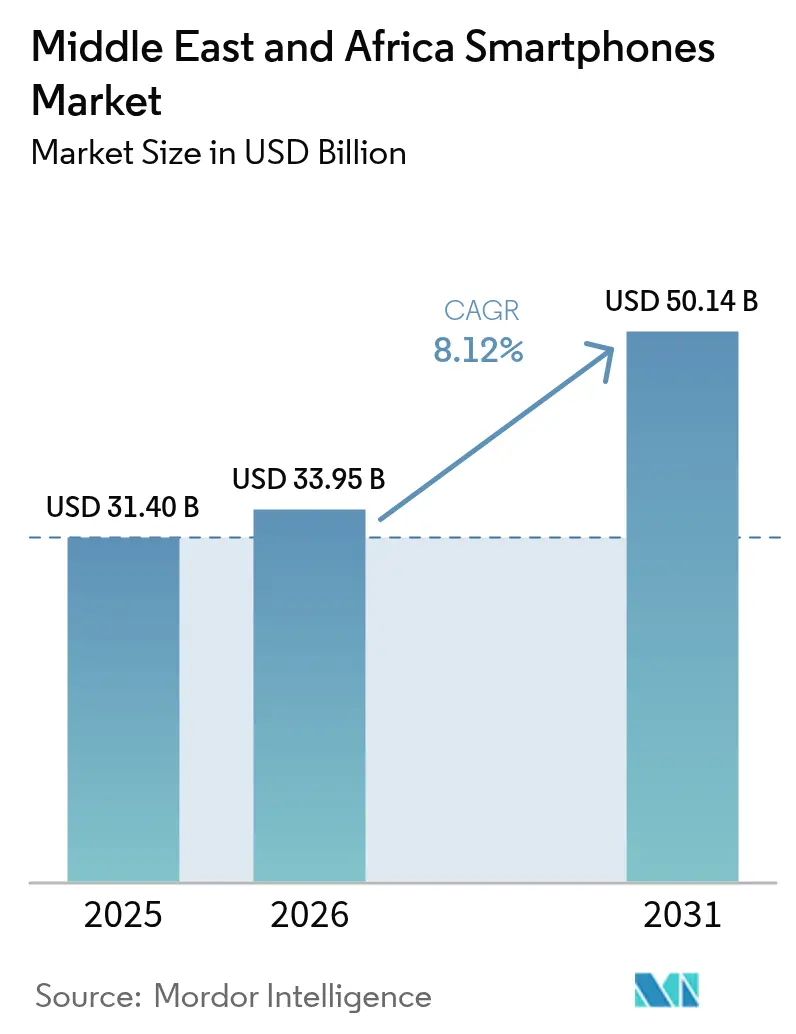

| Base Year Market Size (2025) | USD 31.40 Billion |

| Market Size (2026) | USD 33.95 Billion |

| Market Size (2031) | USD 50.14 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

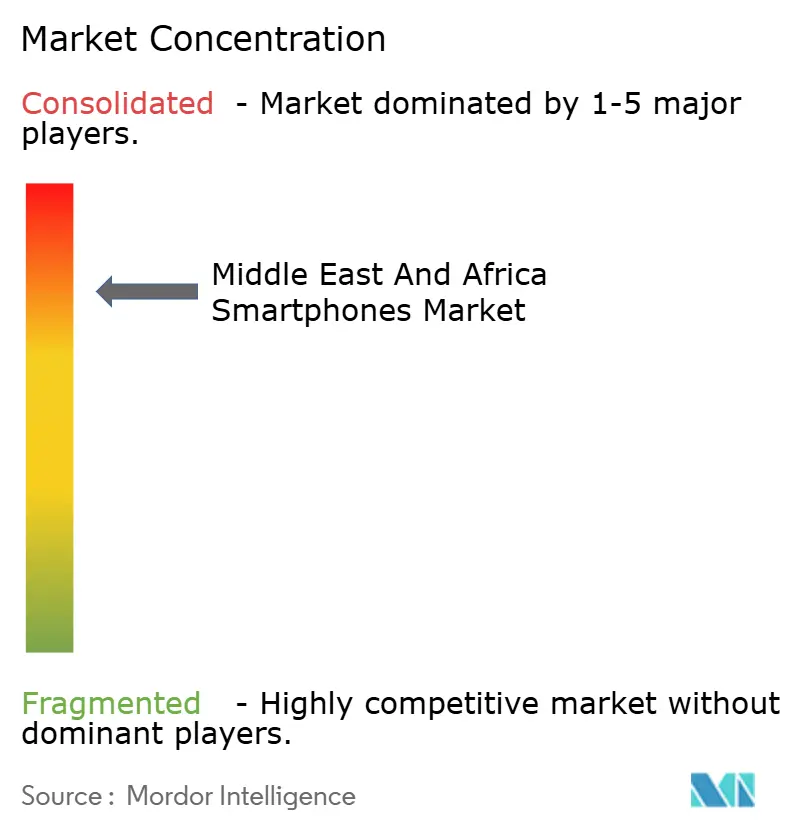

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Smartphones Market Analysis by Mordor Intelligence

The Middle East and Africa smartphones market size is expected to grow from USD 31.40 billion in 2025 to USD 33.95 billion in 2026 and is forecast to reach USD 50.14 billion by 2031 at 8.12% CAGR over 2026-2031. This swift expansion stems from sovereign digital agendas across the Gulf Cooperation Council (GCC) and a demographic dividend in Sub-Saharan Africa that together elevate smartphones from communication tools to foundational access points for e-government, mobile finance, and social commerce. Saudi Arabia’s Vision 2030 super-app ecosystem, high-velocity 5G roll-outs, and rising average selling prices in the Gulf are steering premium device upgrades, while ultra-low-cost Chinese original equipment manufacturer (OEM) strategies extend first-time ownership deep into rural Africa. At the same time, Buy-Now-Pay-Later (BNPL) models, broader e-commerce adoption, and localized manufacturing help counter foreign-exchange (FX) volatility and tariff shocks, sustaining supply security and price discipline. Competitive intensity has sharpened as tier-one global brands defend share against region-born champions and value-focused Chinese disruptors, yet localized innovation and integrated service ecosystems are proving more decisive than sheer hardware specifications.

Key Report Takeaways

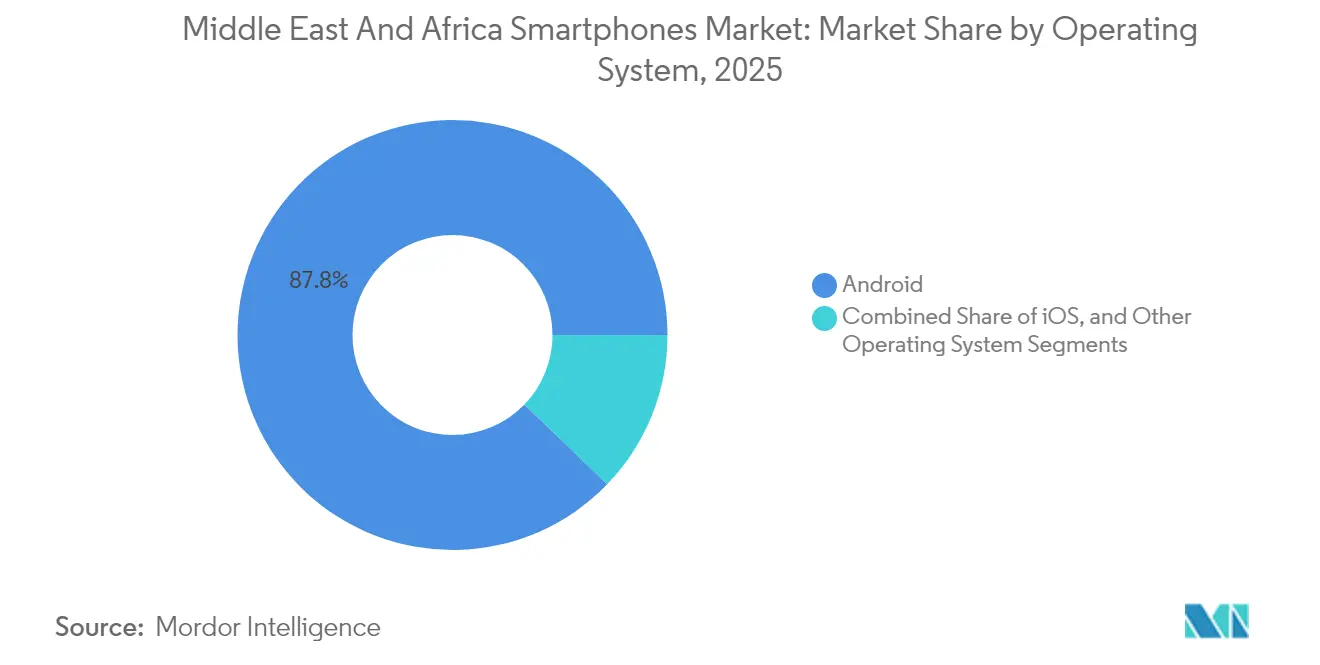

- By operating system, Android controlled 87.78% of Middle East and Africa smartphones market share in 2025 and is expanding at an 11.06% CAGR through 2031, underscoring entrenched platform consolidation.

- By price range, the budget segment captured 37.02% of the Middle East and Africa smartphones market size in 2025, whereas premium devices posted the fastest growth at 9.58% CAGR.

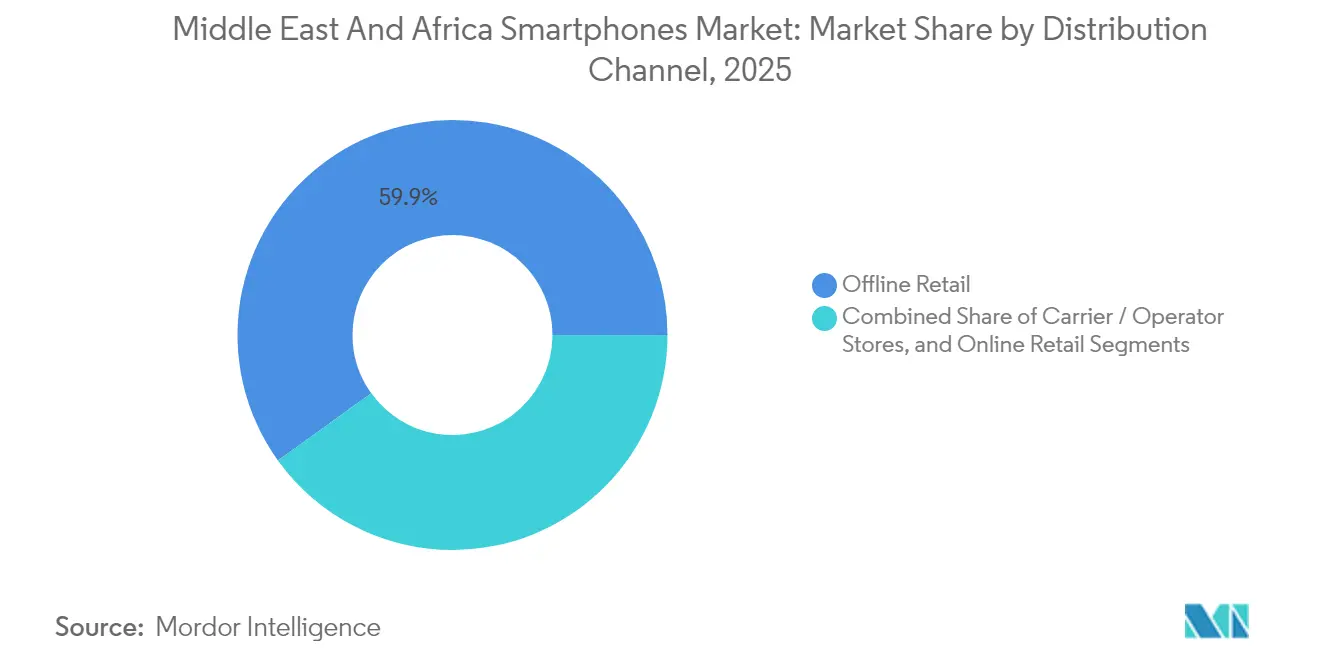

- By distribution channel, offline retail led with 59.92% revenue share in 2025 in the Middle East and Africa smartphones market; online retail is advancing at a 10.21% CAGR to 2031.

- By technology, 4G/LTE held 67.85% share in 2025 while 5G recorded the highest projected CAGR at 10.37% through 2031 in the Middle East and Africa smartphones market.

- By country, Saudi Arabia accounted for 19.21% share of the Middle East and Africa smartphones market in 2025 and is progressing at a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Smartphones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-outs across GCC operators | +2.1% | GCC core, spill-over to North Africa | Medium term (2-4 years) |

| Youth-driven first-time adoption | +1.8% | Sub-Saharan Africa rural and peri-urban | Long term (≥ 4 years) |

| Ultra-low-cost Chinese OEM proliferation | +1.5% | Africa-wide, selective Middle East | Short term (≤ 2 years) |

| E-commerce and social-commerce momentum | +1.2% | Mobile-first urban centers | Medium term (2-4 years) |

| National e-ID / super-app programs | +1.0% | GCC leadership, gradual MEA uptake | Long term (≥ 4 years) |

| BNPL financing widening affordability | +0.9% | Kenya, Nigeria, South Africa urban clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 5G roll-outs across GCC operators

GCC carriers view 5G as an economic catalyst rather than a routine network refresh, linking smartphones to smart-city services, fixed-wireless access, and enterprise Internet of Things (IoT) applications. Saudi Arabia alone expects 5G to inject USD 18 billion into its economy by 2030.[1]Arab News, “Connecting the Kingdom: Saudi Arabia’s 5G revolution,” arabnews.com Operator investments by stc, Zain, and e& already support 54.70% population coverage, prompting demand for premium-capable devices and driving higher average selling prices.

Youth-driven first-time smartphone adoption in Sub-Saharan Africa

Africa’s median age of 19.7 fuels a surge of first-time owners who leapfrog feature phones and access mobile internet services straight through affordable handsets. TRANSSION’s market-leading 47% share results from devices optimized for multi-language support and darker skin-tone photography. Asset-financing models in Kenya lifted penetration to 68.3%, illustrating the structural nature of this demand.

E-commerce and social-commerce channels accelerating device sales

Mobile-first platforms convert browsing into purchases through in-app payments, shortening the sales funnel and unlocking underserved segments. Social commerce in emerging markets is forecast to top USD 720 billion, with Middle East uptake propelled by high smartphone usage and low credit-card penetration.[2]GSMA, “Social Commerce in Emerging Markets,” gsma.com

National e-ID / super-app programs (e.g., Saudi Vision 2030)

Apps such as Nafath have logged 17.2 million downloads and 1.6 billion sign-on requests, anchoring government services to smartphone authentication and deepening device indispensability. These initiatives elevate switching costs and reinforce ongoing replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX volatility and import tariffs | -1.4% | Import-dependent economies | Short term (≤ 2 years) |

| Grey-market and counterfeit inflows | -1.1% | Africa-wide, limited Middle East exposure | Medium term (2-4 years) |

| Emerging data-localization and OTT rules | -0.8% | Regulation-active jurisdictions | Long term (≥ 4 years) |

| Power-supply unreliability in rural areas | -0.7% | Electrification-challenged Sub-Saharan regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX volatility and import tariffs inflating ASPs

Currency depreciation and import duties raise device prices, constraining discretionary spending. Egypt’s 38.5% smartphone import tax initially lowered shipments, pushing OEMs toward local assembly to sidestep tariffs.[3]Nature, “Access to electricity and digital inclusion,” nature.com Manufacturers that dual-source components locally are best positioned to absorb price shocks.

Grey-market and counterfeit handset inflows

Counterfeits account for a signficiant portion of African sales, eroding legitimate revenues and exposing consumers to safety risks. Device registration and IMEI whitelisting, already in effect in Egypt, signal a regulatory shift toward clamping down on illicit channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: Android Ecosystem Dominance

Android led the market with an 87.78% share in 2025 and is projected to register an 11.06% CAGR, reflecting the platform’s alignment with local price sensitivities and service ecosystems. This leadership reinforces the Middle East and Africa smartphones market as an Android-centric environment where open-source flexibility lowers development cost for apps in mobile banking, ride-hailing, and telemedicine. Chinese OEMs leverage Android’s customization layers to embed regional language packs and camera algorithms tailored to darker skin tones, which enhance consumer experience and loyalty. The platform’s synergy with near-field communication (NFC) standards propels digital-wallet adoption in Saudi Arabia, where Nafath’s 17.2 million users log daily transactions via biometric authentication.

The strategic edge expands beyond hardware as service bundling locks users deeper into cloud storage, payment, and identity ecosystems. Developers favor Android’s broader install base to reach scale quickly, while governments adopt Android-first approaches for national ID, tax, and health-record apps. Although iOS retains cachet in ultra-premium brackets, its niche presence does little to erode Android’s network effects. Over the forecast horizon, the Middle East and Africa smartphones market size tied to Android devices is expected to widen further as 5G coverage becomes near-ubiquitous in the Gulf and as Sub-Saharan operators sunset 2G networks.

By Price Range: Budget Dominance Amid Premium Growth

Budget devices between USD 151 and USD 299 held 37.02% share in 2025, underscoring the income realities of mass-market buyers, yet premium smartphones priced USD 600-799 are on track for 9.58% CAGR growth. The bifurcation arises from parallel consumer bases: first-time rural owners and urban digital-service power users. Budget units capitalize on subsidy programs and BNPL schemes that spread repayments across micro-instalments. In contrast, affluent Gulf consumers upgrade to premium SKUs to harness 5G, augmented-reality (AR) features, and onboard AI accelerators.

Financing innovations blur these categories as operators in Kenya and Nigeria market premium devices through pay-as-you-go contracts. Transparent installment models enable mid-income earners to aspire to higher tiers without upfront cash, thereby enlarging the Middle East and Africa smartphones market size for premium devices. The challenge for OEMs lies in balancing feature proliferation with cost control to prevent cannibalization of mid-range models.

By Distribution Channel: Digital Transformation Accelerating

Offline retail maintained a 59.92% share in 2025 because tactile inspection and immediate fulfillment still influence purchasing decisions. Yet online retail is scaling at 10.21% CAGR as logistics networks mature and last-mile costs decline. Post pandemic legacy of contactless commerce persists, driving consumer comfort with app-based transactions. Operators’ own portals contribute additional momentum through bundle offers that integrate data plans and content subscriptions.

Social-commerce ecosystems illustrate hybrid evolution: influencers run live device reviews while integrated payment links close the sale instantly. Distributors engage in omnichannel tactics whereby inventory visibility spans physical stores and online carts, letting shoppers reserve and collect locally. This synergy reduces stock-outs and aligns marketing spend closer to conversion events, heightening operational efficiency across the Middle East and Africa smartphones market.

By Technology: 5G Transition Momentum

4G/LTE commanded 67.85% share in 2025, but 5G is scaling at a forecast 10.37% CAGR, elevating the performance baseline for smartphones. Gulf networks already cover three-quarters of their populations, and trials of 5.5G promise data rates exceeding 10 Gbps. Device makers now ship entry-level 5G chipsets below USD 200, accelerating democratization. In Africa, 5G rollout proceeds in metropolitan zones, yet 4G remains the workhorse for rural voice and data. Strategic timing of 5G handset launches hinges on tariff affordability and content partnerships that showcase tangible benefits such as ultra-high-definition streaming and cloud gaming.

As operators phase out 3G, spectrum refarming frees up frequencies for 4G and 5G expansion. This shift lowers network cost per bit delivered, facilitating wider geographic coverage without proportional capital-expenditure hikes. Together, these trends reinforce the Middle East and Africa smartphones market share gains for 5G-capable models, especially in urban clusters.

Geography Analysis

Saudi Arabia anchors regional value, combining a 19.21% market share in 2025 with Vision 2030 programs that migrate authentication, healthcare, and public services onto mobile platforms. Absher’s 94% adult wallet uptake and stc’s wide 5G footprint forge an ecosystem in which smartphones serve as gateways to banking, traffic management, and digital identity. Premium-device demand intensifies as users seek seamless performance across these always-on services.

North Africa exhibits divergent patterns. Egypt’s whitelisting regulations curtailed grey imports and spurred OEMs to localize assembly, which insulates supply from FX shocks and supports aggressive pricing. Vivo’s plant in the 10th of Ramadan City adds 500,000 units monthly and 1,500 jobs, reinforcing Egypt’s ambition to triple annual output to 9 million units by 2026. Algeria and Morocco pursue similar localization to lessen current-account deficits while imposing stricter safety labels that elevate consumer confidence.

Sub-Saharan Africa remains the volume frontier where youth bulges, mobile-money ubiquity, and improving power grids converge. Research shows households with electricity access present significantly higher penetration, especially among women, underscoring infrastructure’s social dividends. TRANSSION dominates sales through deep rural distribution and culturally attuned user interfaces, while Xiaomi and Samsung target urban professionals with mid-range 5G models. Power-bank bundles and solar-charging kits mitigate off-grid limitations, ensuring sustained device usage despite patchy grid coverage.

Competitive Landscape

Competitive intensity in the Middle East and Africa smartphones market follows a three-tier hierarchy. TRANSSION heads Tier 1 with a 47% Africa share, capitalizing on price-sensitive niches and localized features that elevate user experience beyond mere affordability. Samsung occupies the premium end, leveraging brand equity, robust after-sales, and aspirational marketing to preserve a 21% regional share. Xiaomi, OPPO, and HONOR spearhead Tier 2 challengers armed with rapid product cycles and aggressive mid-range pricing; HONOR reported a 283% surge in Q1 2025 shipments, illustrating the acceleration potential of brand reinvention strategies.

Tier 3 comprises emerging GCC-based assemblers and refurbished-device suppliers clustering around Dubai’s logistics hub. The refurbished segment gains traction as inflation nudges price-conscious buyers toward certified pre-owned devices, extending handset life spans and compressing replacement cycles. Strategic differentiation is now defined more by ecosystem alignment-payments, identity, cloud storage-than by megapixel counts or chipset speeds.

OEMs shore up resilience through vertical integration. Vivo’s Egyptian factory and TRANSSION’s Ethiopian plant localize value chains, hedging against shipping disruptions and tariff shifts. Partnerships between handset brands and content platforms (e.g., Beyond ONE with TIMWETECH) embed subscription services into operator billing flows, fostering stickier revenue streams and deepening market entrenchment.

Middle East And Africa Smartphones Industry Leaders

Xiaomi Corporation

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Infinix Mobility Limited

Oppo Guangdong Mobile Communications Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Egypt unveiled plans to escalate local smartphone production to 9 million units annually by 2026, backed by four global OEMs establishing plants.

- May 2025: The GSMA MEA Regulatory Summit spotlighted early 5G performance metrics from Egypt and Tunisia, stressing high-speed connectivity’s role in economic growth.

- March 2025: Beyond ONE partnered with TIMWETECH to enable direct carrier billing for 3.5 million users in Saudi Arabia and Oman, easing payments for digital content subscriptions.

- February 2025: Vivo boosted manufacturing in Egypt, launching the Y29 from a facility capable of 500,000 units monthly and generating 1,500 jobs.

Middle East And Africa Smartphones Market Report Scope

Smartphones, with strong hardware capabilities, extensive mobile operating systems, facilitating wider software applications, internet, and multimedia functionality (music, videos, and gaming), alongside core phone functions such as voice calls and text messaging, are considered in the scope. Smartphones used for industrial purposes or otherwise known as rugged phones are not considered in the scope. The market study is focused on the trends affecting the market in the major countries in the region. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry. The study tracks the impact of COVID-19 on the overall smartphone industry and its performance.

The Smartphones Market in Middle East and Africa and is Segmented By Operating System (Android, iOS) and Country (Saudi Arabia, United Arab Emirates, South Africa, Egypt, East Africa (Kenya, Tanzania, and Uganda), West Africa (Nigeria and Ghana) Turkey). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Operating System

| Android |

| iOS |

| Other Operating Systems |

By Price Range

| Ultra-Premium (Above USD 800) |

| Premium (USD 600-799) |

| Mid-range (USD 300-599) |

| Budget (USD 151-299) |

| Ultra-Budget (Less Than or Equal USD 150) |

By Distribution Channel

| Online Retail |

| Carrier / Operator Stores |

| Offline Retail |

By Technology (Connectivity)

| 5G |

| 4G / LTE |

| 3G and Below |

By Country

| Saudi Arabia |

| United Arab Emirates |

| South Africa |

| Egypt |

| Nigeria |

| Turkey |

| Rest of Middle East and Africa |

| By Operating System | Android |

| iOS | |

| Other Operating Systems | |

| By Price Range | Ultra-Premium (Above USD 800) |

| Premium (USD 600-799) | |

| Mid-range (USD 300-599) | |

| Budget (USD 151-299) | |

| Ultra-Budget (Less Than or Equal USD 150) | |

| By Distribution Channel | Online Retail |

| Carrier / Operator Stores | |

| Offline Retail | |

| By Technology (Connectivity) | 5G |

| 4G / LTE | |

| 3G and Below | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle East and Africa smartphones market?

The market is valued at USD 33.95 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to advance at a 8.12% CAGR over 2026-2031, reaching USD 50.14 billion.

Why is Saudi Arabia a pivotal growth engine?

Vision 2030 e-government platforms, extensive 5G coverage, and high disposable income drive premium upgrades.

What factors restrain smartphone adoption in rural Africa?

FX volatility, power-supply gaps, and counterfeit influxes hamper penetration.

How are OEMs mitigating tariff and currency risks?

By localizing assembly in countries such as Egypt and Ethiopia to reduce import costs and stabilize pricing.

Page last updated on: