Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

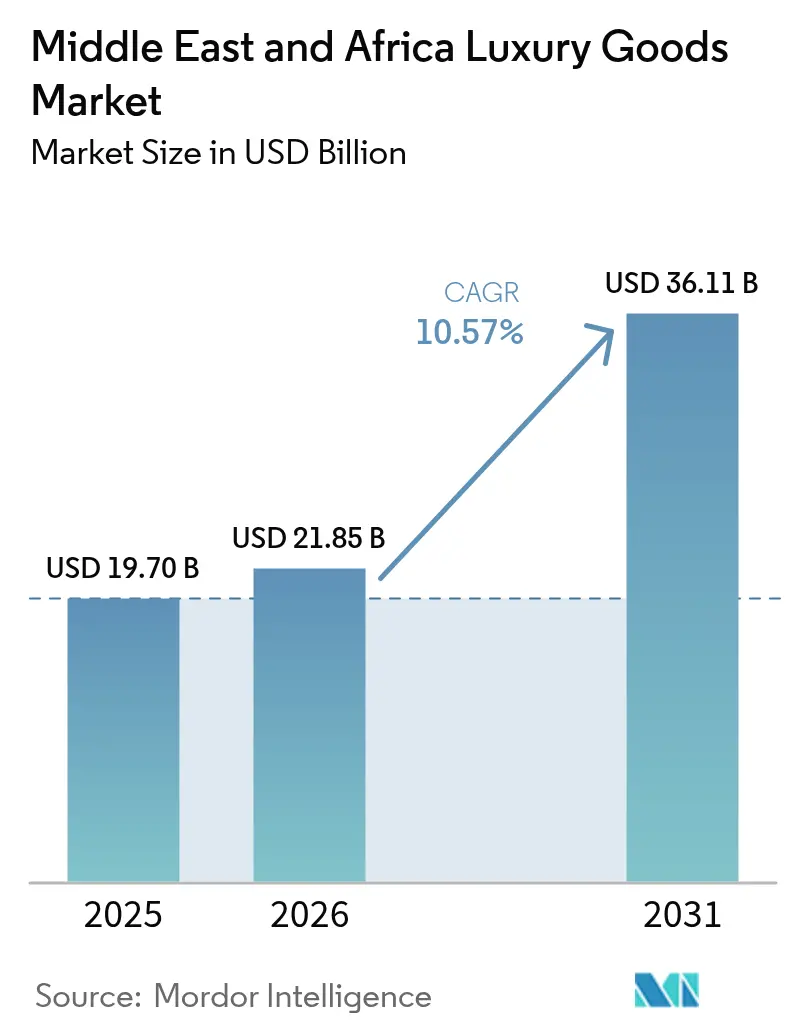

| Base Year Market Size (2025) | USD 19.70 Billion |

| Market Size (2026) | USD 21.85 Billion |

| Market Size (2031) | USD 36.11 Billion |

| Growth Rate (2026 - 2031) | 10.57% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Luxury Goods Market Analysis by Mordor Intelligence

The Middle East and Africa luxury goods market size was USD 19.70 billion in 2025 and is projected to reach USD 21.85 billion in 2026 and USD 36.11 billion by 2031, growing at a CAGR of 10.57% from 2026 to 2031. Urbanization, sovereign-wealth diversification, and high-net-worth immigration are concentrating demand in Gulf Cooperation Council cities where flagship real estate, world-class airports, and tax-efficient shopping converge to replicate European luxury hubs. Rising intra-African tourism, currency stabilization in key economies, and policy incentives that attract foreign direct investment are broadening the Middle East and Africa luxury-goods market beyond traditional Gulf powerhouses. The United Arab Emirates secures the largest tourist-led basket sizes, while Saudi Arabia’s Vision 2030 retail corridors and South Africa’s post-load-shedding recovery add fresh growth layers.

Key Report Takeaways

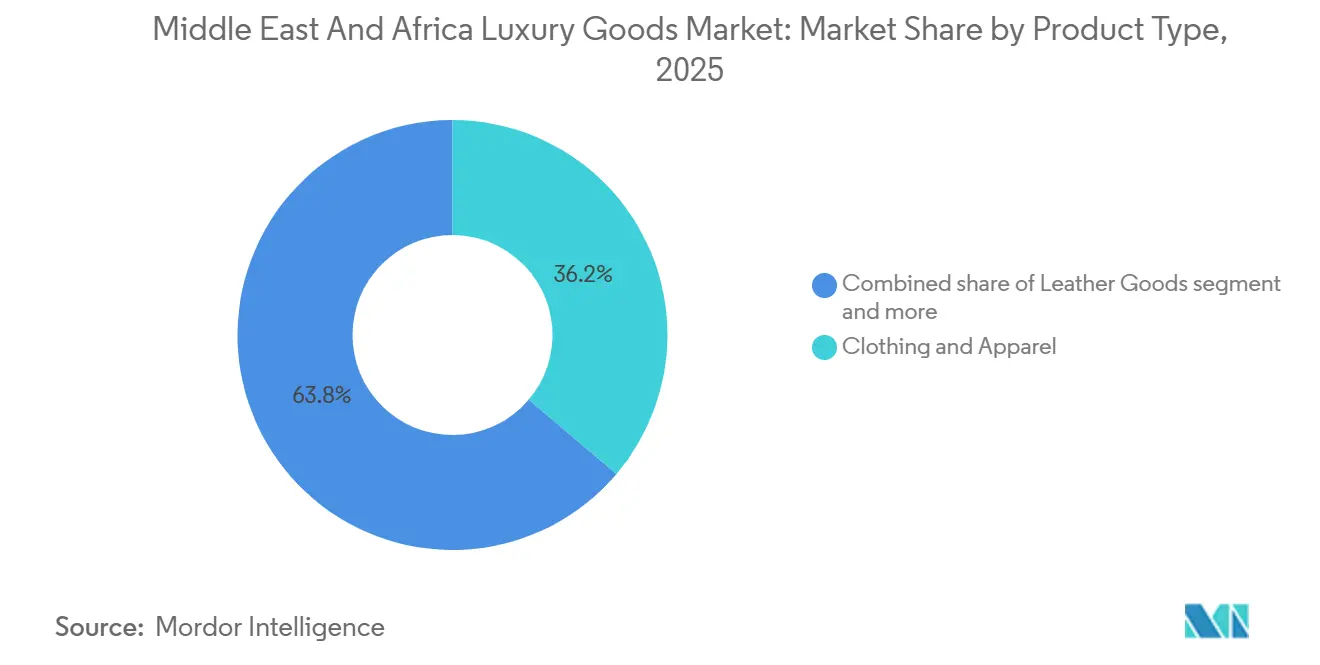

- By product type, clothing and apparel led with 36.18% revenue share in 2025; leather goods are forecast to expand at a 11.07% CAGR through 2031.

- By end-user, women held 63.22% of 2025 revenues, while the men’s segment is projected to grow at a 11.34% CAGR to 2031.

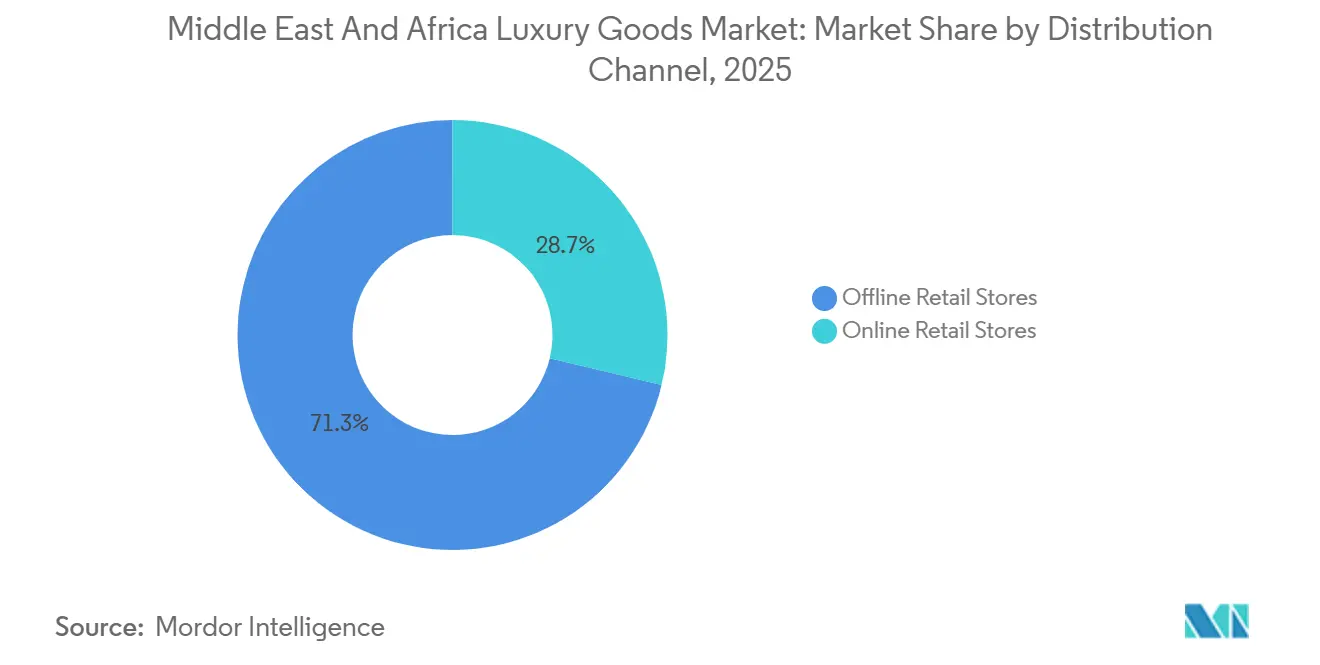

- By distribution channel, offline retail stores retained 71.27% revenue share in 2025, and online retail stores are advancing at a 10.79% CAGR through 2031.

- By geography, the United Arab Emirates commanded 35.26% share of the Middle East and Africa luxury goods market in 2025, while South Africa is forecast to register a 11.03% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Luxury Goods Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovative designs and sustainable raw materials take centre stage | +1.8% | UAE, Saudi Arabia, South Africa; spillover to Turkey and Egypt | Medium term (2-4 years) |

| Retail thrives in tourism-driven ecosystems | +2.2% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh, Jeddah), Egypt (Cairo) | Short term (≤ 2 years) |

| Mono-brand boutiques and malls are on the rise | +1.5% | UAE, Saudi Arabia, Turkey (Istanbul), Morocco (Casablanca) | Medium term (2-4 years) |

| Limited edition products captivate discerning consumers | +1.0% | UAE, Saudi Arabia, with selective launches in South Africa and Egypt | Short term (≤ 2 years) |

| Social media buzz and celebrity endorsements shape buying decisions | +1.3% | Global, with the highest penetration in the UAE, Saudi Arabia, and Nigeria | Short term (≤ 2 years) |

| Brand heritage reinforcing premium perception | +0.9% | UAE, Saudi Arabia, Turkey, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Innovative Designs and Sustainable Raw Materials Take Centre Stage

Maisons are integrating bio-fabricated leathers, recycled precious metals, and traceable gemstones to meet Gulf and African consumers' rising sustainability expectations without compromising craftsmanship. Hermès' investment in mycelium leather prototypes and Richemont's Cartier division sourcing Fairmined gold for Middle East collections signal that provenance transparency is becoming a non-negotiable attribute for high-net-worth buyers under 40. Saudi Arabia's Public Investment Fund has allocated capital to circular-economy ventures, creating a policy tailwind for brands that embed sustainability narratives into product storytelling and supply-chain audits. This driver disproportionately benefits Leather Goods and Jewelry segments, where material innovation directly impacts margin structure and brand differentiation in a market where counterfeits exploit opacity.

Retail Thrives in Tourism-Driven Ecosystems

In 2024, Dubai welcomed over 18.72 million international overnight visitors, supported by VAT refund programs for tourists, showcasing how well-coordinated policies can enhance a destination's appeal to luxury shoppers [1]Source: Department of Economy and Tourism, "Annual Visitor Report 2024", dubaidet.gov.ae. Airport duty-free channels and hotel-adjacent mono-brand stores capture impulse spending from Chinese, Indian, and European tourists who perceive Gulf pricing as advantageous due to VAT refund schemes and currency arbitrage. Egypt's luxury retail in Cairo and Sharm El Sheikh is rebounding as Ras El Hekma development proceeds, yet infrastructure bottlenecks and currency volatility constrain conversion rates compared to UAE and Saudi hubs. This driver amplifies Watches and Jewelry demand, as travelers prioritize portable, high-value items that bypass checked-baggage risks and benefit from cross-border price differentials.

Mono-Brand Boutiques and Malls Are on the Rise

Etoile Group opened 11 new stores across UAE, Saudi Arabia, Bahrain, and Kuwait in H1 2024, introducing Aquazzura, Tod's, Etro, and Chanel to previously underserved luxury corridors. Majid Al Futtaim announced 30+ luxury store additions in 2025, including Eleventy, Poltrona Frau, and Corneliani, as part of a mall-anchor strategy that leverages footfall from entertainment and F&B tenants to drive luxury conversion. Turkey's Zorlu Center and Istinye Park in Istanbul are expanding luxury wings to capture Russian and Central Asian shoppers redirected from European capitals, yet political uncertainty and lira depreciation temper long-term lease commitments. Mono-brand formats allow maisons to control merchandising, train staff on heritage narratives, and integrate digital appointment systems that reduce walk-in friction, particularly for Unisex and Men's categories, where personalized styling drives basket size.

Social Media Buzz and Celebrity Endorsements Shape Buying Decisions

Social media platforms have become a driving force in how luxury brands are discovered and purchased, significantly shaping consumer decisions. In the Gulf and North African markets, regional celebrities and influencers play a vital role by connecting luxury brands with their audiences through culturally relevant content and endorsements. This strategy helps brands build authentic relationships that resonate with local consumers. Increasingly, Arab shoppers are moving away from traditional heritage luxury brands, instead favoring those promoted on social media, where exposure often holds more influence than historical prestige. Saudi Arabia's relaxation of content-creation regulations in 2024 enabled local influencers to film luxury unboxings and mall hauls without prior approval, accelerating organic reach for brands that seed products to Riyadh and Jeddah-based creators. This driver disproportionately benefits Online Retail Stores and Eyewear segments, where visual storytelling and try-on content reduce perceived purchase risk and shorten consideration cycles among digitally native buyers aged 25-40.

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury goods grapple with the weight of hefty import taxes and duties | -1.2% | Saudi Arabia, Egypt, Nigeria, Morocco; moderate impact in South Africa and Turkey | Short term (≤ 2 years) |

| Sourcing and material regulations are becoming increasingly stringent | -0.6% | UAE, Saudi Arabia, South Africa; compliance pressure in Turkey and Egypt | Medium term (2-4 years) |

| Counterfeits are undermining brand value | -0.9% | Turkey (transit hub), Nigeria, Egypt, Morocco; enforcement gaps in free zones | Long term (≥ 4 years) |

| High dependency on brand perception consistency | -0.5% | Global, with heightened sensitivity in the UAE, Saudi Arabia, and South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeits Are Undermining Brand Value

Counterfeit products damage brand reputation and weaken consumer trust, creating unfair competition, reducing legitimate market share, and pricing power. Dubai's Commercial Compliance and Consumer Protection agency recently seized 3.5 million counterfeit goods, highlighting the widespread impact of illicit trade on luxury brand revenues and market positioning [2]Source: Dubai's Commercial Compliance and Consumer Protection, "Major Crackdown: Dubai Seizes 3.5 million Illegal Goods Worth Dh133m", dubai.ae. Counterfeit activities are often concentrated in major trade hubs and tourist destinations, making it challenging for luxury brands to protect their intellectual property and maintain their exclusive image. Nigeria and Morocco lack robust customs recordal systems, allowing counterfeit Louis Vuitton handbags and Rolex watches to saturate Lagos and Casablanca Street markets at 5-10% of authentic prices, eroding brand equity and forcing maisons to invest in blockchain authentication and consumer education campaigns. EU authorities detained 112 million counterfeit items worth EUR 3.8 billion in 2024, with Turkey and the UAE listed among the top origin countries, signaling that Gulf free zones are exploited for trans-shipment and localisation assembly, where packaging and labels are attached post-import to evade detection.

Sourcing and Material Regulations Are Becoming Increasingly Stringent

UAE's Federal Decree-Law No. 12 of 2024 mandates traceability for precious metals and gemstones, requiring hallmarking certificates and country-of-origin documentation that add 5-10% to compliance costs for the Jewelry and Watches segments, according to the UAE Ministry of Economy. Saudi Arabia's National Center for Environmental Compliance enforces chemical-content limits on leather tanning and textile dyes, compelling brands to audit Tier-2 suppliers and invest in ISO 14001-certified facilities, which extends lead times by 4-6 weeks and raises input costs by 8-12%. South Africa's National Regulator for Compulsory Specifications (NRCS) requires pre-shipment testing for Footwear and Leather Goods to verify formaldehyde and chromium levels, adding ZAR 5,000-15,000 per SKU in testing fees and delaying market entry by 2-3 months. These regulatory layers favor vertically integrated conglomerates like LVMH and Kering, which absorb compliance costs through scale, while disadvantaging independent maisons and emerging African brands that lack in-house testing labs and legal teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leather Goods Surge Past Apparel Growth

Leather goods are forecast to expand at 11.07% CAGR during 2026-2031, outpacing all other categories despite clothing and apparel commanding 36.18% market share in 2025. Asprey's February 2024 collaboration with Princess Nourah Al Faisal on a limited-edition pochette capsule featuring Saudi embroidery exemplifies how localized leather goods generate cultural resonance and command premiums over standard SKUs. Footwear remains a steady performer, buoyed by athleisure-luxury hybrids from Balenciaga and Golden Goose that resonate with Gulf millennials, yet faces margin pressure from Turkish and Vietnamese contract manufacturers that supply parallel importers. Eyewear benefits from prescription-luxury convergence, where brands like Cartier and Dior integrate optician services into boutiques, capturing medical-necessity spending at luxury price points.

Jewelry and watches collectively represent the highest per-transaction values, with Watches averaging USD 8,000-15,000 in Gulf markets and Jewelry purchases exceeding USD 20,000 during wedding and Ramadan seasons. Richemont's May 2024 opening of Cartier's Riyadh flagship and Van Cleef & Arpels' 600-square-meter Dubai Mall store signals confidence in high-jewelry demand, particularly among Saudi and Emirati nationals allocating sovereign-wealth gains into portable stores of value. Other Product Types, encompassing fragrances, home décor, and luxury stationery, capture share but grow at below-market rates due to gifting-season concentration and limited repeat-purchase frequency. Fabergé's January 2024 launch on Ounass, the Middle East's leading luxury e-tailer, demonstrates how niche categories leverage digital platforms to bypass physical retail economics and access geographically dispersed collectors.

By End-User: Men's Luxury Accelerates Amid Dress-Code Shifts

Men accounted for a smaller share in 2025 but are projected to grow at 11.34% CAGR through 2031, the fastest among end-user segments, driven by Saudi Arabia's Vision 2030 workforce diversification and the UAE's expansion of finance and tech sectors that elevate professional wardrobes. Gulf national men aged 25-40 are adopting tailored suits, luxury sneakers, and smartwatches as status markers in corporate and social settings, a behavioral shift that Etoile Group capitalized on by introducing Etro and Corneliani to Kuwait and Bahrain in H1 2024. Women retained 63.22% share in 2025, anchored by high-value jewelry, handbags, and couture purchases during weddings and religious festivals, yet growth moderates as market penetration among Gulf nationals approaches saturation, and incremental gains depend on African market expansion.

Unisex products, including fragrances, leather accessories, and minimalist jewelry, appeal to younger buyers who prioritize versatility and gender-fluid aesthetics. Piaget's January 2025 collaboration with Emirati designer Shamsa Alabbar for a Ramadan-timed Limelight Gala watch integrated Arabic calligraphy and moon-phase complications, positioning the piece as a culturally rooted unisex heirloom that transcends traditional gender segmentation. Ounass reported that unisex fragrance sales grew year-on-year in 2024, with Amouage, an Omani perfumery in which L'Oréal acquired a minority stake in April 2025, leading the category through oud-based compositions that resonate across genders and age cohorts.

By Distribution Channel: Digital Gains Traction Without Displacing Flagships

Offline retail stores held 71.27% share in 2025, reflecting the luxury industry's reliance on tactile experiences, personalized service, and the social signalling value of shopping in Dubai Mall or Riyadh's Kingdom Centre. Majid Al Futtaim's announcement of more than 30 luxury store additions in 2025, including Eleventy and Poltrona Frau, underscores that physical retail remains the primary revenue driver, particularly for high-ticket Jewelry and watches, where in-person authentication and sizing are non-negotiable. Mono-brand boutiques enable maisons to control merchandising, train staff on heritage narratives, and integrate digital appointment systems that reduce walk-in friction, a model that Hermès employed when it became the majority shareholder in its UAE retail operations in January 2024, subsequently achieving 109.6% revenue growth.

Online retail stores are expanding at 10.79% CAGR through 2031, propelled by platforms like Ounass, which achieved year-on-year growth in 2024, and average order values of USD 550. Ounass's 89-minute average delivery time in the UAE and 2-3 hour hyper-fast service in Dubai convert impulse purchases that would otherwise require mall visits, while its November 2024 opening of Ounass Maison, a VIP personal-shopping space inside Dubai's Mandarin Oriental, blends digital convenience with physical exclusivity to capture high-net-worth clients who value privacy over public retail theater. E-commerce's share will plateau by 2031 as categories like Jewelry and Watches, where authentication concerns and emotional purchase drivers favor in-person transactions, resist full digital migration, yet Eyewear and Leather Goods will see online penetration exceed as augmented-reality try-ons and blockchain provenance certificates reduce perceived risk.

Geography Analysis

The United Arab Emirates captured 35.26% market share in 2025, anchored by Dubai's international overnight visitors in 2024 and Abu Dhabi's cultural-tourism investments that position the Emirates as the region's luxury retail nucleus. Richemont's Van Cleef & Arpels opened a 600-square-meter Dubai Mall flagship, while Cartier staged a two-day "Journey of Wonders" exhibition at Al Shindagha Museum in February 2025, showcasing over 300 high-jewelry pieces and reinforcing the maison's 25-year UAE presence through maritime and Emirati heritage narratives. Dubai Customs intercepted 68 intellectual property violations worth AED 42.195 million in Q1 2025, yet small-parcel e-commerce channels remain under-policed, allowing counterfeit leather goods to erode brand equity.

Saudi Arabia commands the second-largest share, driven by Vision 2030's retail infrastructure mega-projects and consumer spending that reached trillions in 2024. Diriyah Square awarded a billion-dollar contract in July 2025 for 400 retail units, with Majid Al Futtaim operating VOX Cinemas and 7 lifestyle brands, positioning the development as a cultural-retail hybrid. Dior opened a 2,500-square-meter "Designer of Dreams" exhibition at the National Museum in November 2024, illustrating how heritage-led activations convert cultural engagement into commercial outcomes. Etoile Group opened 11 new stores across the UAE, Saudi Arabia, Bahrain, and Kuwait in H1 2024, introducing Aquazzura, Tod's, Etro, and Chanel to previously underserved corridors.

South Africa is forecast to register the fastest geographic CAGR of 11.03% through 2031, propelled by post-load-shedding infrastructure recovery and Johannesburg-Cape Town corridor premiumization. Black middle-class professionals in Johannesburg and Cape Town are allocating a marginal portion of their discretionary income to luxury menswear and leather goods as economic mobility accelerates, creating white-space opportunities for brands that tailor assortments to local tastes and offer flexible payment terms. Turkey serves as a manufacturing and transit hub, with OECD data showing that Turkey seized counterfeit goods destined for the EU, underscoring supply-chain vulnerabilities as Turkish routes feed African markets. Zorlu Center and Istinye Park in Istanbul are expanding luxury wings to capture Russian and Central Asian shoppers, yet lira depreciation and political uncertainty temper long-term lease commitments.

Competitive Landscape

The Middle East and Africa luxury goods market registers a concentration, indicating that LVMH, Kering, Richemont, and Hermès control flagship real estate, brand partnerships, and high-net-worth client databases, yet white-space opportunities persist in Tier-2 African cities and mono-brand boutique formats that bypass traditional wholesale. Boucheron's December 2025 strategic joint venture with Al Tayer Group, which granted Al Tayer control of UAE operations, signals that even Richemont-owned maisons are ceding operational autonomy to regional specialists who possess superior customer intelligence and government relationships.

Kering's November 2024 opening of Bottega Veneta Waves in Dubai and LVMH's Louis Vuitton Jeddah flagship in the same month illustrate synchronized expansion strategies where conglomerates race to secure prime mall anchors before Vision 2030 infrastructure saturates available retail space. Emerging disruptors include regional e-commerce platforms like Ounass, which achieved year-on-year growth in 2024 by offering 89-minute delivery in the UAE and exclusive brand launches such as Skims and Fear of God, converting digitally native buyers who bypass physical retail entirely.

L'Oréal's April 2025 minority investment in Amouage, an Omani perfumery, exemplifies how global conglomerates acquire regional heritage brands to access niche categories and authentic Middle Eastern narratives that resonate with local and diaspora buyers. Technology adoption is bifurcated: leaders like Richemont deploy blockchain authentication for high-jewelry and integrate augmented-reality try-ons for Eyewear, while smaller players struggle with customs recordal systems and lack the capital to invest in anti-counterfeit infrastructure.

Middle East And Africa Luxury Goods Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Compagnie Financière Richemont SA

-

Chanel S.A

-

Prada S.p.A.

-

Kering S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Casio marked Saudi National Day with the launch of a limited-edition watch that reimagines a classic square-faced model through Saudi cultural motifs, partnering with artist Lina Malaika and fashion label Hindamme to position the watch as a pop-culture icon rather than a mere accessory.

- June 2025: Kalyan Jewellers has expanded its United Arab Emirates footprint to 22 stores by opening two new outlets one in Sharjah and one in Dubai continuing its aggressive growth strategy in the Gulf, aligned with a broader franchise-led expansion plan for FY2025-26.

- April 2025: De Beers introduced its flagship store in the United Arab Emirates at the Dubai Mall. The store showcased unique High Jewelry pieces, crafted to highlight the beauty of the Earth's finest diamonds.

- March 2025: Chic Brand launched an exclusive high-end leather goods and fashion collection in Dubai, positioning a private-label luxury line that fuses traditional craftsmanship with contemporary design to elevate the region’s premium retail experience. The range spans men’s Arabic sandals celebrated across the Gulf Cooperation Council alongside boots, formal shoes, and smart-casual options, plus women’s exotic leather handbags, footwear, and more.

Middle East And Africa Luxury Goods Market Report Scope

Luxury goods are premium, high-quality products that are not necessary for living but add value to consumers' appearance. The Middle East and Africa Luxury Goods Market is Segmented by Product Type (Clothing and Apparel, Footwear, Leather Goods, Watches, Eyewear, and More), End-User (Men, Women, and Unisex), Distribution Channel (Offline Retail Stores and Online Retail Stores, and Geography (South Africa, Saudi Arabia, United Arab Emirates, Nigeria, Egypt, and More). The Market Forecasts are Provided in Terms of Value (USD).

Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Other Product Types |

End-User

| Men |

| Women |

| Unisex |

Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Other Product Types | |

| End-User | Men |

| Women | |

| Unisex | |

| Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| By Geography | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large will the Middle East and Africa luxury goods market be by 2031?

It is forecast to reach USD 36.11 billion by 2031, expanding at a 10.57% CAGR from 2026 to 2031.

Which product category is growing fastest in the region?

Leather Goods are projected to outpace all other categories at an 11.07% CAGR thanks to high margins and cultural collaborations.

What role does e-commerce play in regional luxury sales?

Online Retail Stores are growing at 10.79% CAGR and could capture channel share by 2031, led by fast-delivery specialists like Ounass.

How are brands combating counterfeits in the region?

Leading maisons deploy blockchain certificates, NFC tags, and customs recorded filings, while Dubai Customs and other agencies intensify seizure operations to protect intellectual property.

Page last updated on: