Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

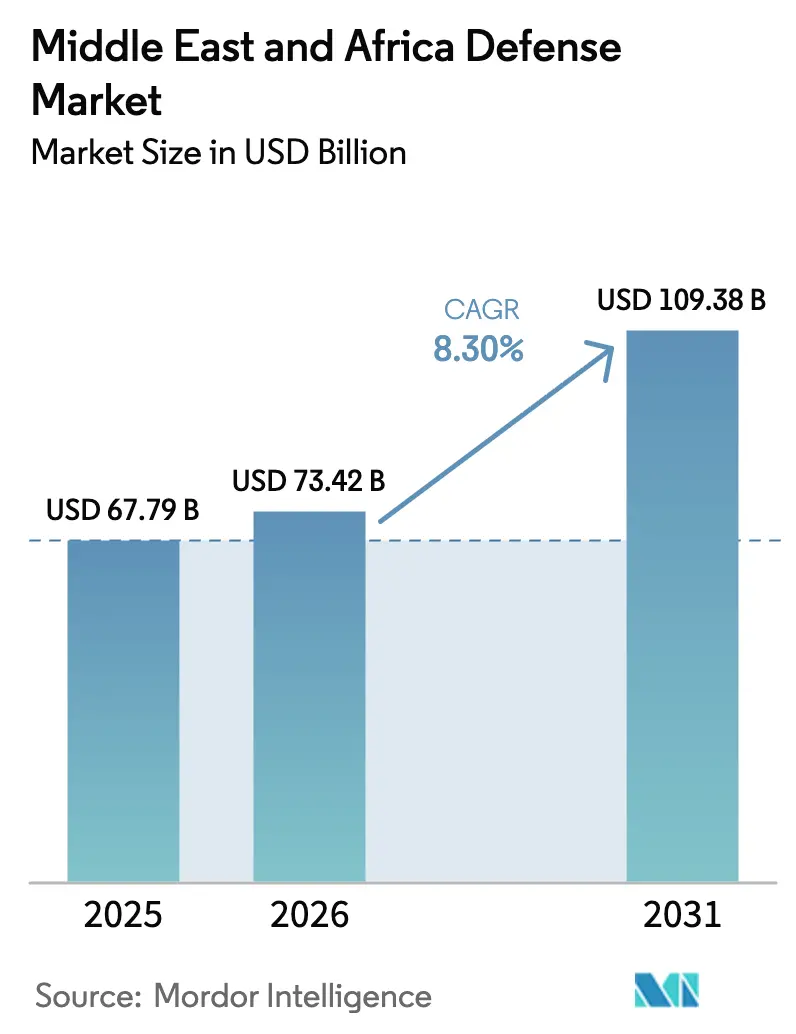

| Base Year Market Size (2025) | USD 67.79 Billion |

| Market Size (2026) | USD 73.42 Billion |

| Market Size (2031) | USD 109.38 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

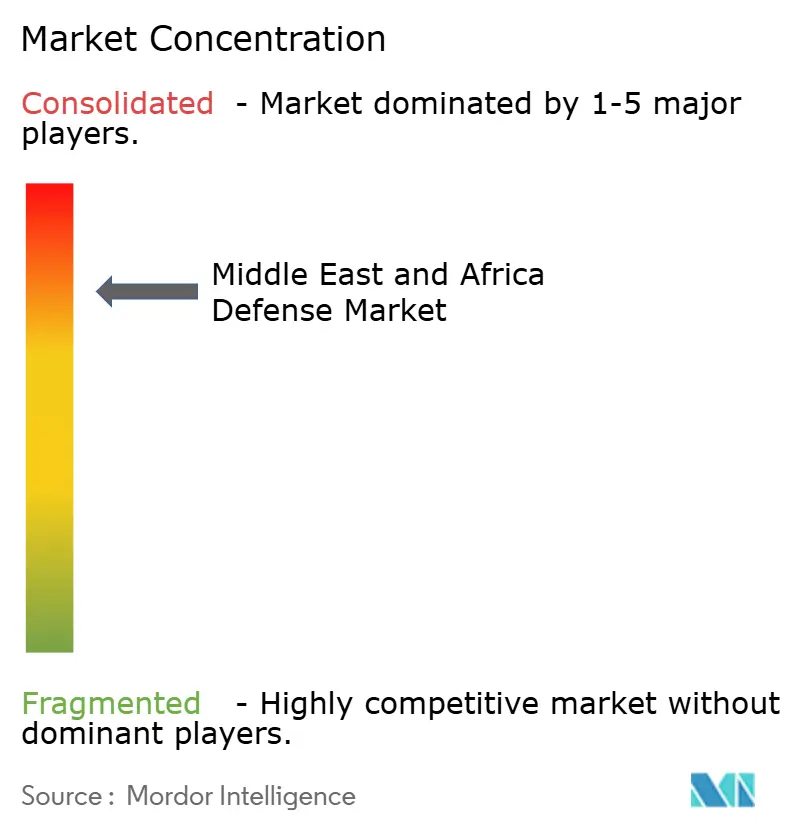

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Defense Market Analysis by Mordor Intelligence

The Middle East and Africa defense market size is expected to grow from USD 67.79 billion in 2025 to USD 73.42 billion in 2026 and is forecasted to reach USD 109.38 billion by 2031 at an 8.30% CAGR over 2026-2031. Growth rests on sustained conflict in the Levant, the Gulf, and the Sahel, where defense ministries continue to prioritize force modernization over fiscal discipline. Saudi Arabia increased its outlays from USD 75.8 billion in 2024 to USD 81.4 billion in 2025, while Israel boosted its defense budget by 65% in 2024, underscoring demand that is largely shielded from commodity price swings. Sovereign wealth funds from the Gulf are now underwriting African joint ventures, broadening the Middle East and Africa defense market, and cementing cross-regional influence. Unmanned platforms, directed-energy weapons, and space-based intelligence, surveillance, and reconnaissance (ISR) programs are eclipsing traditional procurements, and European lenders have relaxed earlier environmental, social, and governance (ESG) limits, unblocking new credit lines for manufacturers.

Key Report Takeaways

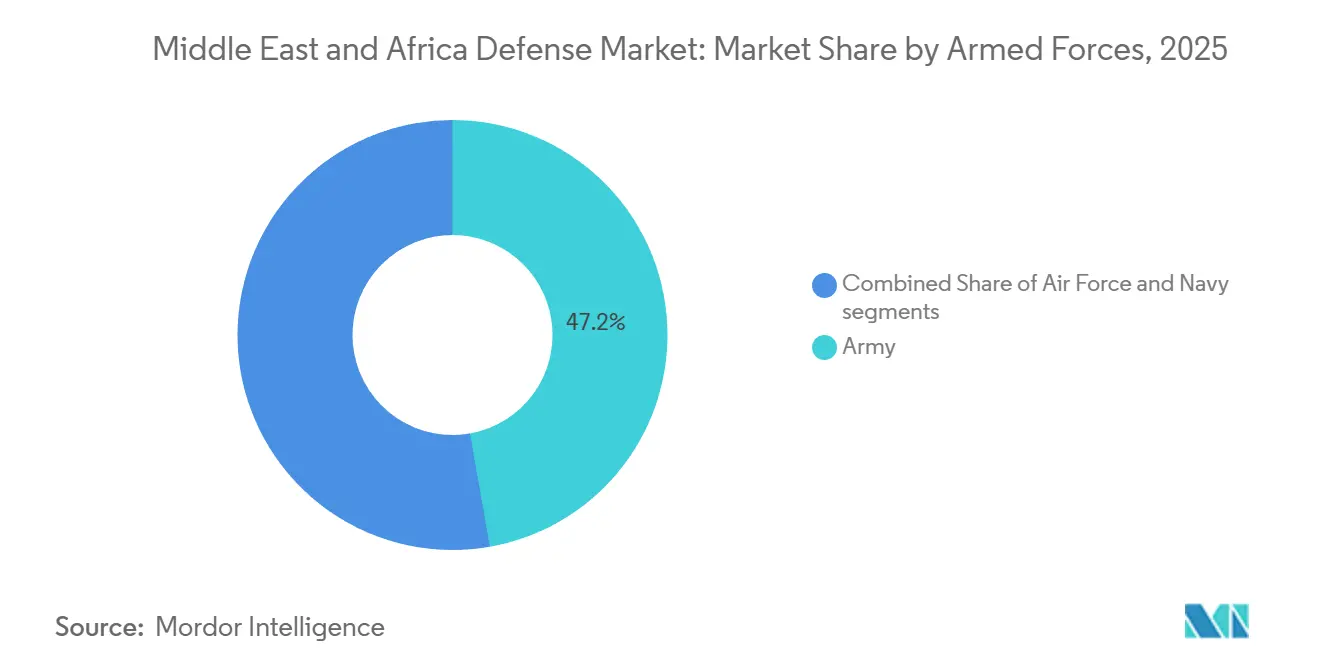

- By armed forces, the army equipment captured 47.21% of the Middle East and Africa defense market share in 2025, whereas naval programs are advancing at a 9.23% CAGR through 2031.

- By type, vehicles accounted for 24.45% of the Middle East and Africa defense market size in 2025; however, unmanned systems are projected to post the highest CAGR of 11.54% from 2026 to 2031.

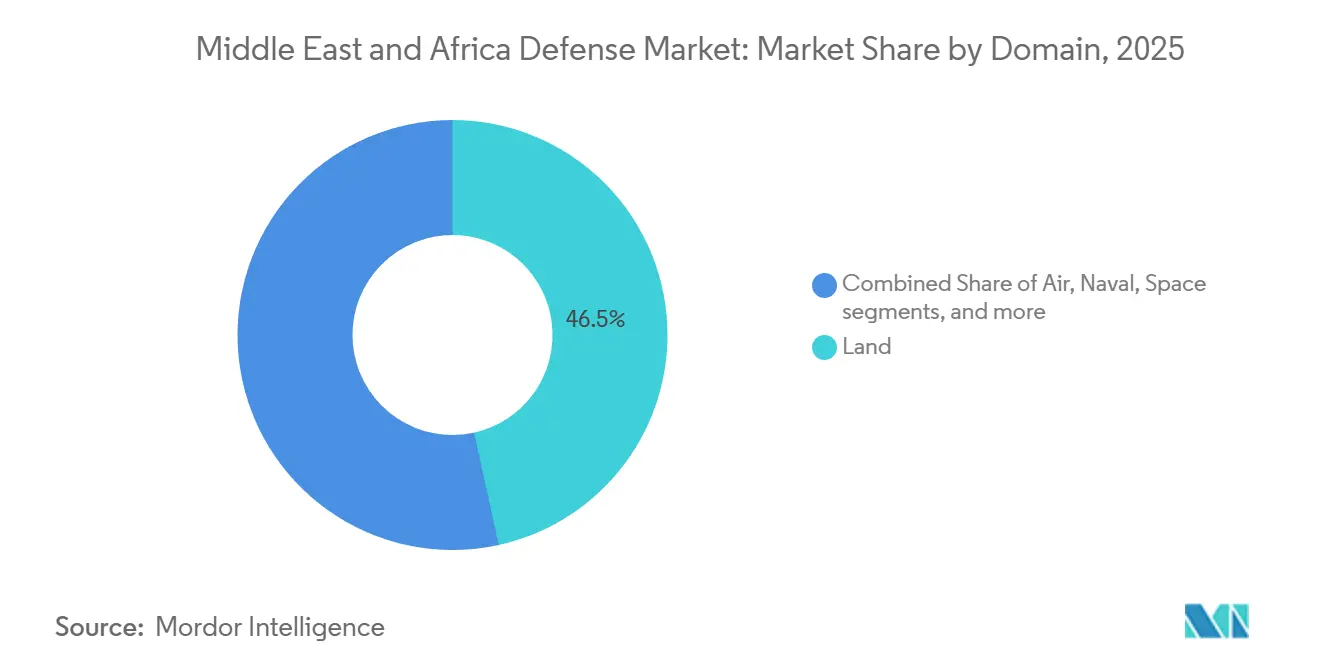

- By domain, land operations held a 46.54% share of the Middle East and Africa defense market in 2025; space-based ISR is forecast to expand at a 9.21% CAGR through 2031.

- By procurement nature, foreign purchases represented 66.34% of spending in 2025, while indigenous production is growing at a 9.75% CAGR.

- By geography, the Middle East commanded 81.45% of expenditure in 2025, whereas Africa is expected to register a 10.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained geopolitical instability driving continuous defense preparedness | +2.1% | Middle East, Sahel | Long term (≥ 4 years) |

| Oil- and gas-backed defense spending across GCC modernization programs | +1.8% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| National defense localization and industrialization mandates | +1.5% | Saudi Arabia, UAE, Egypt, Algeria, South Africa | Long term (≥ 4 years) |

| Accelerated adoption of unmanned, autonomous, and precision-strike systems | +2.3% | Regionwide | Short term (≤ 2 years) |

| Sovereign wealth fund–led defense investment and export financing into Africa | +0.9% | UAE, Saudi investments in Africa | Medium term (2-4 years) |

| Emergence of regional space-based ISR and surveillance capabilities | +1.2% | UAE, Saudi Arabia, Morocco, Israel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained Geopolitical Instability Driving Continuous Defense Preparedness

Persistent conflict in Yemen, Syria, and Gaza keeps regional forces on high alert, ensuring steady demand for munitions, EW upgrades, and counter-rocket systems. Israel placed a USD 210 million order with Elbit Systems in November 2025 to upgrade Merkava tanks with artificial-intelligence sights, reflecting lessons learned in recent Gaza operations.[1]Leo Feierberg, “Elbit Wins USD 210 Million Deal to Upgrade Israel’s Merkava Tanks,” The Jerusalem Post, jpost.com Houthi attacks on Red Sea shipping have accelerated Saudi and Egyptian naval purchases, while Sahel insurgencies spur African requirements for light armored vehicles and secure communications. Each new clash underscores the need for next-generation capabilities, insulating defense budgets from broader austerity measures and keeping the Middle East and Africa defense market on an upward trajectory.

Oil- and Gas-Backed Defense Spending Across GCC Modernization Programs

Hydrocarbon revenue continues to underwrite the majority of Gulf budgets. Riyadh’s USD 142 billion framework with the US for F-15 fighters, THAAD interceptors, and maritime patrol aircraft was structured to ride out short-term oil-price volatility. Qatar added more than USD 800 million in Boeing training and sustainment contracts for its F-15QA fleet. The UAE ordered four Airbus A330 Multi-Role Tanker Transport (MRTT) aircraft in July 2024, including technology-transfer clauses that channel knowledge to local firms.[2]Airbus Press Office, “Saudi Arabia Orders Four Additional Airbus A330 MRTTs,” airbus.com Because these programs also create advanced-manufacturing jobs, they remain politically untouchable even during commodity downturns.

National Defense Localization and Industrialization Mandates

Vision 2030 obliges Saudi Arabia to localize over 50% of its defense spending by 2030, a target enforced through offset clauses across every major contract. Lockheed Martin awarded canister and pallet work for the THAAD system to Saudi firms in February 2024, marking the first indigenous production of the interceptor’s critical components. Egypt’s M1A1 Abrams co-production line and Algeria’s licensed assembly of Russian vehicles reveal that localization is now a region-wide policy instrument to secure jobs and strategic autonomy.

Accelerated Adoption of Unmanned, Autonomous, and Precision Strike Systems

Israel contracted Elbit Systems for USD 40 million in December 2024 to deliver swarm UAVs and micro-unmanned platforms capable of searching, identifying, and striking without human input. Turkey’s Bayraktar TB2 has spread across Libya, Ethiopia, and Morocco, showing that medium-altitude UAVs are no longer limited to NATO suppliers. Gulf states are blending Chinese Wing Loong UAVs with domestic designs to diversify sourcing. Meanwhile, USD 60 million in January 2025 for Elbit’s ReDrone counter-UAS suite points to a parallel boom in anti-UAS technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exposure of defense budgets to hydrocarbon price volatility | -1.4% | Gulf, Algeria | Short term (≤ 2 years) |

| Export-control restrictions and sanctions on advanced defense subsystems | -1.1% | Middle East, parts of Africa | Medium term (2-4 years) |

| Rising ESG-related constraints on defense-sector financing | -0.6% | Regionwide | Medium term (2-4 years) |

| Shortages of skilled labor and secure electronics supply chains | -0.8% | Saudi Arabia, UAE, Egypt, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exposure of Defense Budgets to Hydrocarbon Price Volatility

When Brent crude dropped below USD 40 per barrel in 2020, Riyadh deferred multiple programs and renegotiated milestone payments with US contractors. Algeria likewise trimmed 2024 procurement after natural gas revenues dipped, delaying negotiations for Su-57 fighters. Although sovereign wealth funds buffer shocks, a two-year stretch under USD 60 would still force Gulf states to shift spending from modernization toward payroll and readiness.

Export-Control Restrictions and Sanctions on Advanced Defense Subsystems

The US International Traffic in Arms Regulations (ITAR) require case-by-case licenses for active electronically scanned array radars and long-range missiles, extending timelines by up to 18 months. Israel’s qualitative military edge doctrine downgrades sensitive exports to Gulf clients, while European embargoes restrict specific lethal systems for African buyers, nudging them toward Chinese or Russian suppliers. Financing hurdles add a second layer of delay as banks calibrate ESG policies on a deal-by-deal basis.[3]Financial Conduct Authority, “Our Position on Sustainability Regulations and UK Defence,” fca.org.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Naval Modernization Outpaces Land and Air

Naval acquisition budgets are growing at a 9.23% CAGR, eclipsing the expansions of the air force and the army as states prioritize control of the Strait of Hormuz, the Suez Canal, and the Bab el-Mandeb. L3Harris Technologies, Inc., and SAMI signed an agreement in April 2025 with Zamil Shipyards to build modular unmanned surface vessels, a clear indicator that littoral security now drives platform roadmaps. In contrast, the army, despite accounting for 47.21% of 2025 expenditure, faces slower growth because most of its heavy-armor inventory has already been recapitalized. Ongoing upgrades to the M1A1 and Merkava emphasize digital fire-control and active-protection systems over raw tonnage. Naval spending also benefits from multinational task forces that share operational costs, enabling smaller Gulf states to field higher-end corvettes and mine-countermeasure (MCM) ships within collective frameworks. The Middle East and Africa defense market, therefore, concentrates new-build activity along coastlines while armies pivot to sustaining platforms already in service.

A second growth lever is the migration from crewed hulls to optionally manned or fully autonomous vessels. Saudi trials of unmanned surface craft signal appetite for persistent surveillance and cost-effective deterrence. Israel’s Iron Beam laser program, although primarily focused on air defense, will transition to shipboard testing, reinforcing naval modernization with directed energy capabilities. Because sea lanes carry most regional trade, even brief disruptions in the Red Sea or Gulf of Aden incur outsized economic penalties, prompting defense ministries to allocate budget headroom toward hulls, sensors, and missile systems that ensure open passage.

By Type: Unmanned Systems Disrupt Traditional Platform Hierarchies

Vehicles still accounted for 24.45% of 2025 spending, while unmanned systems are rising at an 11.54% CAGR. The Middle East and Africa defense market for unmanned platforms is projected to surpass USD 25 billion by 2031, reflecting global shifts toward lower-risk, 24/7 ISR and precision-strike capabilities. Israeli, Turkish, and Chinese producers dominate medium-altitude long-endurance (MALE) exports, while Gulf states are seeding indigenous designs to hedge against export-license risks. Parallel investment in counter-UAS suites, such as Elbit’s ReDrone system, ensures that every new offensive capability spurs equal demand for defense.

C4ISR and EW budgets are also rising as militaries integrate sensors, edge computing, and artificial intelligence. Because network-centric doctrines require resilient data links, spending on hardened communications and passive detection gear increases in lockstep. Ammunition remains a volume business, driven by attrition warfare in Yemen and Gaza, yet stocks are shifting toward smart artillery and guided rockets. Emerging subcategories, including space and cyber tools, combine for a modest base today but carry steep growth curves, particularly as satellite data becomes central to targeting.

By Domain: Space and Cyber Emerge as Strategic Frontiers

Land operations accounted for 46.54% of total operations in 2025, anchored by troop deployments in Yemen, the Sinai, and the Sahel. Yet the space segment climbs at a 9.21% CAGR, fueled by Morocco’s satellite deal and Gulf launch schedules that extend sovereign coverage across chokepoints. The Middle East and Africa defense market share for cyber-electromagnetic projects, although currently below 5%, is doubling every five years as commanders view spectrum dominance as a prerequisite for both manned and unmanned operations. Air programs remain robust due to Saudi, Qatari, and Israeli fighter and tanker buys, but payload integration timelines temper dollar growth before 2031.

Electromagnetic spectrum budgeting overlaps with cyber line items, producing blended requirements for EW pods, threat-hunting software, and secure cloud infrastructure. Israel’s January 2025 contract for F-16I self-protection systems exemplifies how airborne platforms are increasingly incorporating cyber resilience features at the point of inception.[4]FlightGlobal, “Israel Picks Elbit Systems for F-16I Self-Protection Upgrade,” flightglobal.com As regional powers network satellites, UAVs, and ground sensors into a unified picture, the payoff is faster kill chains and improved battle damage assessment, reinforcing the premium on space and cyber capabilities.

By Procurement Nature: Indigenous Production Gains Momentum

Foreign procurement still covered 66.34% of 2025 demand; however, indigenous production is growing at a 9.75% CAGR as offset rules tighten. The Middle East and Africa defense market size, driven by local manufacturing, is expected to reach USD 45 billion by 2031, provided that Vision 2030 and similar programs achieve their milestones. Lockheed’s THAAD canister transfer and Boeing’s rotary-wing joint venture with SAMI exemplify how tier-one primes embed local partners to safeguard market access. Egypt’s Abrams tank line, Algeria’s armored vehicle licenses, and South Africa’s Denel restructuring all aim to increase self-reliance while maintaining export potential.

Local content requirements also promote workforce development, with Saudi Arabia aiming to create 100,000 skilled defense jobs by 2030. Edge-to-factory digital twins, additive manufacturing, and composite airframe shops accelerate the diffusion of technology across national economies. Even so, complex subsystems such as active electronically scanned array (ESA) radars often remain imported because they are subject to US or European export controls. Success, therefore, hinges on building sovereign microelectronics fabs and securing long-term intellectual property rights.

Geography Analysis

The Middle East accounted for 81.45% of total outlays in 2025, led by Saudi Arabia, the UAE, and Israel, each with multibillion-dollar modernization roadmaps. Riyadh’s USD 142 billion framework agreement for fighters, interceptors, and patrol aircraft represents a single-buyer commitment unmatched worldwide. The UAE added four Airbus A330 MRTTs and embedded industrial participation to uplift local supply chains. Israel, facing multi-front pressures, expanded its munitions and EW budgets in 2024 and continues to contract for autonomous systems at a rapid pace.

Africa, although starting from a smaller base, is the fastest-growing territory, with a 10.23% CAGR through 2031. Algeria remains the largest African spender, though budget dips tied to gas revenue have delayed some fighter talks. Egypt leverages M1A1 co-production to anchor a domestic armored fleet, while Morocco’s spy satellite buy extends national ISR coverage over Western Sahara. Sahel states are channeling Gulf and European aid toward light armored vehicles, UAVs, and secure radios to counter insurgencies, and South Africa’s Denel aims to revive export lines for artillery and UAVs. Sovereign wealth fund financing from Saudi Arabia and the UAE serves as a catalyst, underwriting African contracts that might otherwise stall due to fiscal constraints.

Cross-regional ties are broadening. Israeli suppliers tap normalization accords to market precision munitions and counter-UAS kits across the Gulf and Morocco. Turkey’s Baykar Tech rides competitive pricing to secure orders in Libya and Ethiopia. Meanwhile, European lenders, having relaxed their ESG standards, are once again underwriting working capital for second-tier firms, ensuring supply chain liquidity for contracts in the Middle East and Africa.

Competitive Landscape

The Middle East and Africa defense market features a concentrated tier of Western primes, including Lockheed Martin Corporation, The Boeing Company, BAE Systems plc, Northrop Grumman Corporation, and RTX Corporation, which dominate high-ticket sales, especially in air and missile defense. Regional champions Saudi Arabian Military Industries (SAMI), Israel Aerospace Industries Ltd., Rafael Advanced Defense Systems Ltd., Elbit Systems Ltd., and EDGE Group have scaled rapidly, integrating electronics assembly, missile component machining, and unmanned system final assembly lines. Israeli firms can leverage fewer export restrictions to offer turnkey strike and counter-UAV packages, winning multi-year contracts, such as Elbit’s USD 2.3 billion international deal in November 2025. Turkey’s Baykar Tech competes aggressively in the medium-altitude UAVs niche, often pricing its products 30-40% below those of Western rivals.

Joint ventures are the preferred entry route for new technologies. L3Harris Technologies, Inc., SAMI, and Zamil Shipyards are field-testing unmanned surface vessels (USVs) that meld Western command-and-control (C2) software with local hull production. French, German, and Italian banks are openly marketing defense financing, reversing earlier ESG pullbacks and expanding lending pools for mid-cap suppliers. Chinese contractors are promoting integrated air-defense batteries accompanied by soft financing, while South Korean armor producers are seeking assembly partnerships in Saudi Arabia and the UAE, thereby intensifying competition in tracked and wheeled vehicles.

White-space opportunities lie in cyber defense, directed-energy weapons (DEWs), and small-satellite launch services. Because localization mandates favor technology transfer, primes that pair intellectual-property sharing with training programs gain an edge. Supply chain resilience is another battleground; firms able to guarantee secure semiconductor access and robust logistics attract preference in multi-year tenders.

Middle East And Africa Defense Industry Leaders

EDGE Group PJSC

Lockheed Martin Corporation

Israel Aerospace Industries Ltd.

Elbit Systems Ltd.

Saudi Arabian Military Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Elbit Systems secures a USD 2.3 billion contract with the UAE, highlighting the UAE's focus on advanced defensive technologies to enhance aircraft protection and survivability rather than strike capabilities.

- December 2025: France delivers three Rafale jets to Egypt, enhancing its Air Force modernization and strengthening defense capabilities.

- December 2025: The Pentagon awarded The Boeing Company an USD 8.6 billion contract to design, integrate, test, produce, and deliver 25 new F-15IA fighter jets for the Israeli Air Force.

Middle East And Africa Defense Market Report Scope

The Middle East and African defense market analyzes different defense equipment used to maintain the region's military strength. The study covers all aspects and is expected to provide insights into budget allocation and spending in the Middle East and African defense market during the forecast period.

The Middle East and Africa defense market is segmented into armed forces, type, domain, procurement nature, and geography. By armed forces, the market is segmented into the air force, the army, and the navy. By type, the market is segmented into personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems. By domain, the market is segmented into land, air, naval, space, and cyber and electromagnetic spectrum. By procurement nature, the market is segmented into indigenous production and foreign procurement. The report also covers the market sizes and forecasts for the major countries across the region. The market sizing and forecasts have been provided in value (USD).

By Armed Forces

| Air Force |

| Army |

| Navy |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

By Geography

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Israel | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Algeria | |

| Rest of Africa |

| By Armed Forces | Air Force | |

| Army | ||

| Navy | ||

| By Type | Personnel Training and Protection | |

| C4ISR and Electronic Warfare (EW) | ||

| Vehicles | ||

| Weapons and Ammunition | ||

| Unmanned Systems | ||

| Space and Cyber Systems | ||

| By Domain | Land | |

| Air | ||

| Naval | ||

| Space | ||

| Cyber and Electromagnetic Spectrum | ||

| By Procurement Nature | Indigenous Production | |

| Foreign Procurement | ||

| By Geography | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Israel | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Algeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa defense sector by 2031?

The Middle East and Africa defense market is expected to reach USD 109.38 billion by 2031.

Which segment is projected to grow fastest in regional defense budgets?

Unmanned systems are forecasted to record an 11.54% CAGR through 2031.

How large is naval spending compared with other armed-forces allocations?

Navy programs are on track for a 9.23% CAGR, outpacing land and air investments.

Why are Gulf states investing in African defense ventures?

Sovereign wealth funds use joint ventures to diversify revenue and extend strategic influence while meeting African demand for modern equipment.

What role does localization play in procurement policy?

Gulf and African governments now require extensive technology transfer and local assembly, driving indigenous production growth at a 9.75% CAGR.

How are export controls shaping purchase decisions?

License delays and subsystem downgrades encourage buyers to diversify suppliers and pursue domestic manufacturing to safeguard timelines and capabilities.

Page last updated on: