Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

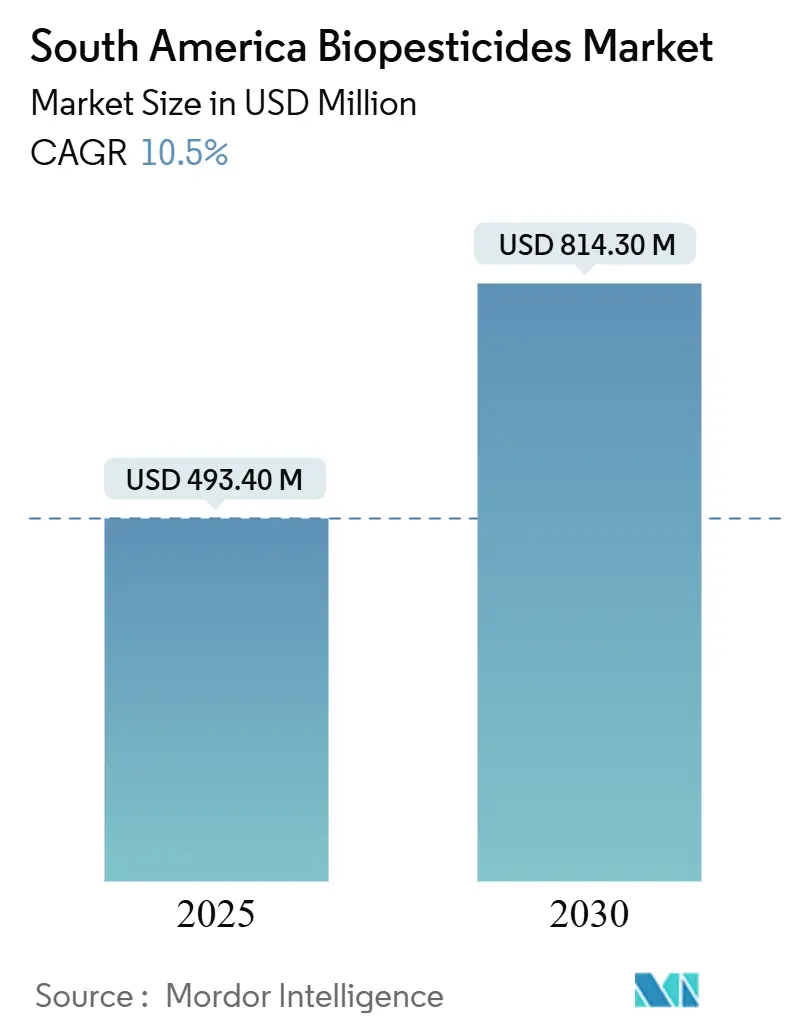

| Market Size (2025) | USD 493.40 Million |

| Market Size (2030) | USD 814.30 Million |

| Growth Rate (2025 - 2030) | 10.50% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Biopesticides Market Analysis by Mordor Intelligence

The South America biopesticides market size reached USD 493.40 million in 2025 and is forecast to climb to USD 814.30 million by 2030, advancing at a 10.50% CAGR over the period. This expansion rests on surging organic farmland, faster product approvals, and mounting pest resistance that erodes the efficacy of synthetic pesticides. The South America biopesticides market is also gaining tailwinds from residue-free export premiums, carbon-credit incentives, and state subsidies that lower on-farm production costs. Regulatory alignment across Brazil, Argentina, and Chile facilitates smooth cross-border sales, while rising investor interest fuels the development of new biofactories and joint ventures. Competitive intensity remains high as local specialists and global multinationals vie to demonstrate field performance, expand their portfolios, and establish distribution channels that reach remote farming hubs.

Key Report Takeaways

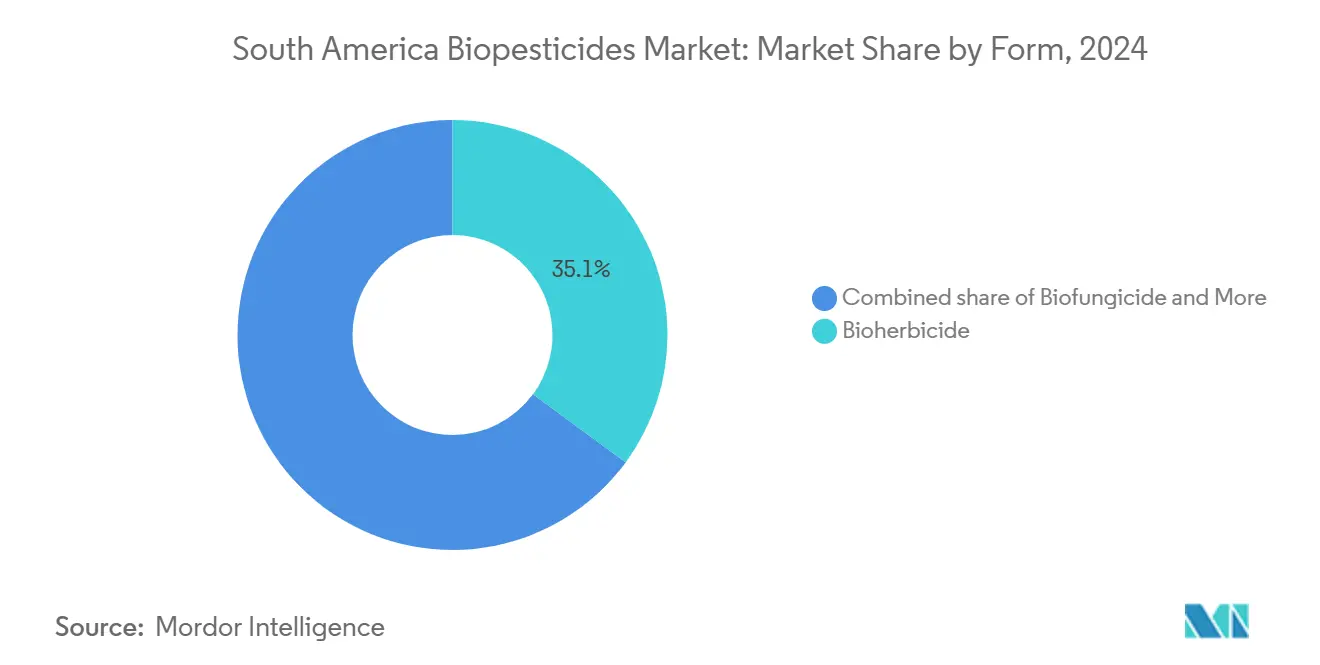

- By form, bioherbicides held 35.1% of the South America biopesticides market share in 2024, while biofungicides are forecast to post the fastest growth at a 10.6% CAGR through 2030.

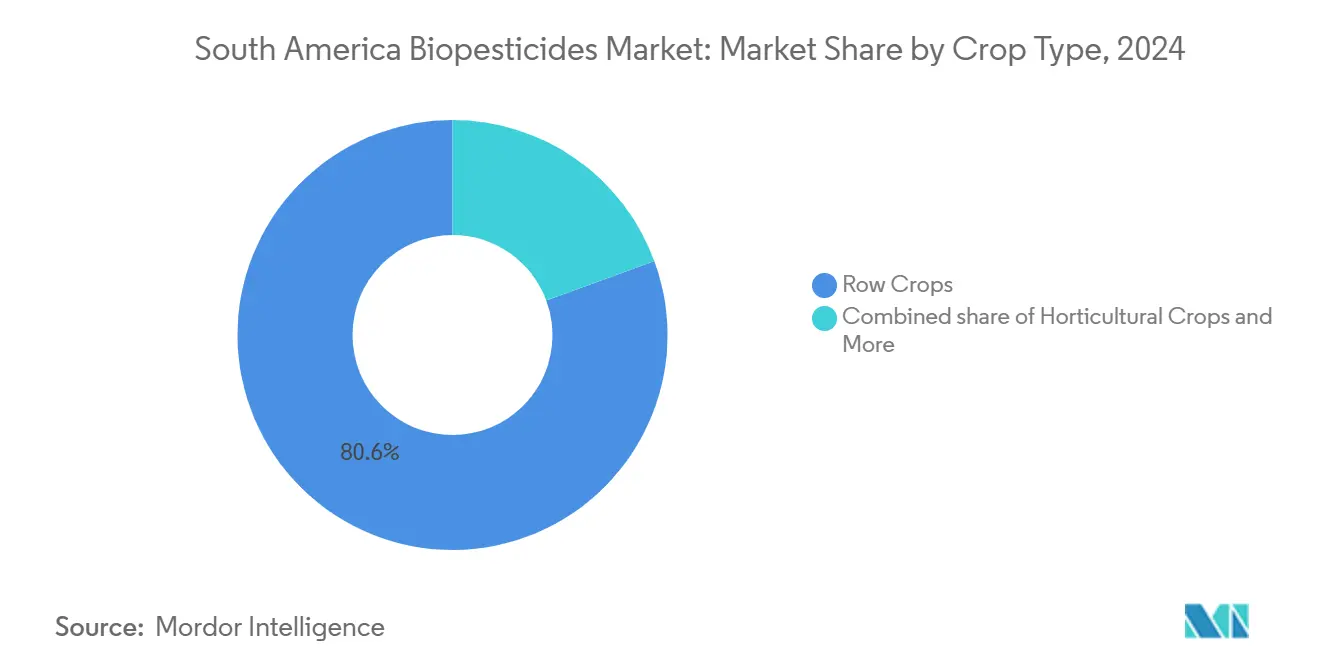

- By crop type, row crops accounted for 80.6% of the South America biopesticides market size in 2024 and are projected to grow at a 10.6% CAGR between 2025 and 2030.

- By geography, Brazil led with a 57.2% revenue share in 2024, while Argentina is projected to register the highest 11.8% CAGR from 2025 to 2030.

South America Biopesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of certified organic farmland | +2.1% | Brazil and Argentina, spillover to Chile | Medium term (2-4 years) |

| Bioinput programs and faster registration | +1.8% | Brazil national, Argentina emerging | Short term (≤ 2 years) |

| Resistance in soybean and sugarcane pests | +2.3% | Brazil, Argentina, and Paraguay | Short term (≤ 2 years) |

| Residue testing at export terminals | +1.4% | Brazil and Argentina export corridors | Medium term (2-4 years) |

| Carbon-credit linked biological demand | +1.2% | Brazil national, Argentina pilot regions | Long term (≥ 4 years) |

| State-subsidized on-farm bioreactors | +0.9% | Parana and Goias, expanding to Sao Paulo | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Certified Organic Farmland

Brazil and Argentina added 1.2 million hectares of certified organic farmland in 2024, bringing Brazil's total to 1.8 million hectares and Argentina's to 3.7 million hectares under certified production[1]Source: Brazilian Organic Association, “Organic Certification Statistics,” ORGANICSBRASIL.ORG.br. Organic rules prohibit the use of synthetic chemicals, so growers rely on the South America biopesticides market for pest control. Premium farm-gate prices, which average 25–40% above those of conventional crops, offset higher biological input costs and spur adoption. Ministry of Agriculture, Livestock and Supply (MAPA) shortened organic certification processing from 18 to 12 months, a change that speeds conversion and boosts near-term demand. Compliance with the International Federation of Organic Agriculture Movements (IFOAM) and the United States Department of Agriculture (USDA) equivalency promises export access, reinforcing the economic logic for shifting to biological inputs. As coffee, citrus, and grape exporters pursue residue-free status, certified acreage is projected to accelerate, maintaining upward pressure on the South America biopesticides market.

Bioinput Programs and Faster Registration

Brazil’s Law 15.070 of 2024 created a dedicated bioinputs lane and reduced approval time by 35%, enabling 47 new biological products to clear Ministry of Agriculture, Livestock and Supply (MAPA) in 2024, compared to 28 in 2023. Argentina mirrored the push, with the National Service of Agri-Food Health and Quality (SENASA) forming a specialized review cell that processed 23 new registrations, representing an 85% year-over-year increase [2]Brazilian Cold Chain Association, “Refrigerated Logistics Infrastructure,” ABRAFRIGO.com.br. Risk-based assessments facilitate the rapid identification of well-characterized strains while maintaining rigorous field-efficacy checks. Shorter waits trim market entry risk, encourage multinational filings, and widen product choice for growers. Alignment with Organisation for Economic Co-operation and Development (OECD) and Food and Agriculture Organization of the United Nations (FAO) protocols also enables firms to leverage data packages across borders, thereby scaling regional launches. The policy upgrade, therefore, feeds a multi-year growth cycle for the South America biopesticides market.

Resistance in Soybean and Sugarcane Pests

Whitefly populations in Brazilian soybeans exhibit 60–80% resistance to neonicotinoids, and sugarcane nematodes are increasingly tolerant to chemical nematicides. As field failure rates rise, growers are pivoting to Beauveria and Metarhizium bio-insecticides, whose 2024 registrations have jumped 40%. Trichoderma-based bio-nematicides covered 850,000 hectares in 2024, up from 620,000 hectares in 2023, representing a 37% increase. Microbials use multiple modes of action, limiting resistance build-up, and provide 75–85% control where chemicals achieve less than 50%. These efficacy gains enhance trust and increase demand, thereby reinforcing the growth trajectory of the South America biopesticides market.

Residue Testing at Export Terminals

Export hubs at Santos, Paranaguá, and Buenos Aires tightened residue screens in 2024 and now reject cargoes above stricter MRL thresholds. The European Union dropped or banned 127 synthetic actives, yet biological residues remain largely exempt. Verified low-residue soybeans earn 8–12% premiums, prompting integrated biological programs that had 23% more compliant shipments year on year. Blockchain traceability tags confirm the use of biological inputs, enabling premium payouts and placing another structural tailwind behind the South America biopesticides market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak cold-chain for microbials | -1.7% | Amazon regions, Andean routes, and remote areas | Short term (≤ 2 years) |

| Price premium versus synthetics and FX swings | -1.3% | Region-wide, acute in Argentina and Brazil | Short term (≤ 2 years) |

| Micro-climate driven efficacy variability | -0.8% | Tropical belts and high-altitude zones | Medium term (2-4 years) |

| Copy-cat strains and weak IP enforcement | -0.6% | Informal markets across the region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Cold-Chain for Microbials

Refrigerated logistics cover only 35% of agricultural corridors, and products often travel on ambient trucks, which reduces shelf life from 18 months to 6–8 months[3]Source: Brazilian Phytosanitary Defense Association, “Pest Resistance Studies,” ANDEF.com.br . The Amazon Basin and Andean routes pose particular hurdles, while achieving full cold-chain coverage would require USD 850 million, compared to the USD 180 million invested in 2024. Distributors either accept a 20–30% potency loss or face freight bills that are 25–40% higher in cost. The reliability gap erodes user confidence and hinders growth in the South America biopesticides market.

Price Premium Versus Synthetics and FX Swings

Biologicals cost 40–70% more than their chemical counterparts, and 2024 currency volatility increased Argentine list prices by 35% following the depreciation of the peso. Imported fermentation gear and active ingredients are priced in U.S. dollars, so swings in exchange rates widen the premium. Smallholders curb their use when premiums climb above 50%, especially during commodity price downturns. This affordability headwind hinders adoption and slows the expansion pace of the South America biopesticides market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form – Bioherbicides hold the lead even as biofungicides accelerate

Bioherbicides accounted for 35.1% of the South America biopesticides market share in 2024, as glyphosate resistance prompted soybean growers to adopt microbial and biochemical weed control solutions. Historical shifts from 2019 to 2024 indicate steady leadership. However, biofungicides now post a sharper 10.6% CAGR, which could see them close the gap by 2030. Brazilian producers lean on bioherbicides for large-scale soybean systems, whereas Argentine farms elevate biofungicide programs for wheat and corn disease control. The South America biopesticides market size linked to biofungicides is projected to rise in tandem with climate-driven disease pressure and the 18 newly cleared fungicidal products by the Ministry of Agriculture, Livestock and Supply (MAPA) in 2024. Complementary bioinsecticide demand remains firm as resistance to whiteflies and nematodes deepens, keeping a broad product mix in play.

Crop-specific challenges drive varied adoption patterns. Bioherbicides thrive in areas with large acreage, allowing for scale efficiencies and the integration of mechanical weeding. Biofungicides excel in high-value crops where disease outbreaks result in substantial financial losses, and growers are willing to pay for consistent Trichoderma efficacy. Regulatory fast-tracking favors disease-control actives, signaling further share gains. Because both categories tackle distinct challenges, each anchors different profit pools inside the South America biopesticides market.

By Crop Type – Row crops dominate, yet diversification gains speed

Row crops accounted for 80.6% of the South America biopesticides market size in 2024 and are forecast to maintain a 10.6% CAGR through 2030. Soybeans alone employed biologicals over 12.8 million hectares in Brazil and 8.2 million hectares in Argentina as growers fought resistance episodes. Sugarcane and corn add further scale, making row crops the volume engine for many manufacturers. Specialty cash crops, such as coffee and cocoa, use more biologicals per hectare, yet occupy smaller acreage, so their absolute volumes remain modest. Horticultural adoption is rising in export fruit sectors, where European buyers demand residue-free goods, nudging higher-value demand into the South America biopesticides market.

Regional uptake aligns with farm structure. Mato Grosso and Paraná adopt precision-sprayed biologicals at scale, whereas Buenos Aires and Santa Fe exploit program synergies with conservation farming. Row crop supremacy stems from economies of scale that drop per-hectare costs by up to one-third, thereby freeing budgets for combination programs that marry bioherbicides, biofungicides, and bioinsecticides. As copycat fear recedes and field success stories spread, new acreage is likely to open up further, keeping row crops at the heart of South America's biopesticides market growth.

Geography Analysis

Brazil contributed 57.2% of 2024 revenue as the largest tropical farming base and home to 25 million hectares under biological care. The country processed 47 approvals in 2024 and enjoys state subsidies for 300 mini biofactories, actions that underpin a steady growth rate during the forecast. Mato Grosso, Paraná, and São Paulo are the biggest users, with soybeans and sugarcane together making up two-thirds of volumes. Law 15.070 and the National Bioinputs Program streamline approvals and offer extension support, positioning Brazil to retain its leading position in the South America biopesticides market.

Argentina held the next largest share in 2024 and is projected to grow at the fastest rate, with an 11.8% CAGR, fueled by the National Service of Agri-Food Health and Quality (SENASA) swifter reviews and currency dynamics that make imported synthetics more expensive. Buenos Aires, Santa Fe, and Córdoba concentrate soybean, wheat, and corn hectarage that now adopts biological programs to secure export premiums. Argentina’s 3.7 million hectares of organic farmland necessitate biological usage, and government support alleviates the initial switching pains, solidifying its rising status in the South America biopesticides market.

The rest of South America delivered a 15.3% share, led by Chile’s fruit exports, Colombia’s coffee belt, and Peru’s modernization drive. Chile spends USD 45 per hectare on biologicals, given strict residue caps for table grapes and citrus bound for the European market. Colombia expanded biofungicide coverage over 180,000 hectares of coffee in 2024, and Peru supports biological adoption in asparagus and avocado fields via low-interest credit. Collectively, smaller nations are projected to enjoy a robust 12.3% CAGR, adding depth and diversity to the South America biopesticides market.

Competitive Landscape

The South America biopesticides market is fragmented, with the top five suppliers holding a significant share. Certis Biologicals tops the list by investing in Brazilian production and buying a distribution channel that covers 850,000 hectares. Coromandel International focuses on neem-based exports and local partnerships. Vittia used IPO proceeds to build a biofactory that lifts microbial capacity to 180 million liters. Koppert Biological Systems maintains a strong regional presence after commissioning a Piracicaba complex that combines automated insect rearing and fermentation lines for greenhouse vegetables and sugarcane programs.

Global majors seek local clout through deals such as Corteva’s broadened Symborg partnership and Sumitomo’s minority stake in Bio Insumos Nativa. Valent BioSciences leverages National Service of Agri-Food Health and Quality (SENASA) approvals to push Bacillus products into Argentina’s wheat belt, while IPL Biologicals relies on a Chilean alliance to reach fruit and vegetable growers. Technology bets on RNA interference, microencapsulation, and biofilm stabilization to create differentiation paths for research-rich companies that accept longer approval cycles. Competition also hinges on after-sales agronomic support, digital recommendation tools, and performance guarantees that reduce growers’ perceived risk when switching to biologicals.

Consolidation potential remains substantial because hundreds of small outfits lack the scale necessary for effective research and development, quality control, and marketing. As performance standards rise and cold-chain coverage improves, high-grade suppliers are well-positioned to capture market share, although nimble regional players who master local agronomics will continue to influence niche segments. Rising ESG mandates have prompted agricultural input distributors to expand biological portfolios. Several conventional pesticide dealers now dedicate at least 20% of shelf space to microbial solutions, giving leading brands valuable end-market visibility. Private-equity funds entered the space in 2024, deploying USD 210 million across five regional manufacturers, signaling confidence in the multi-year growth prospects for the South America biopesticides market.

South America Biopesticides Industry Leaders

Certis Biologicals (Mitsui & Co.)

Coromandel International Limited

Vittia S.A.

Koppert Biological Systems

Valent BioSciences LLC (Sumitomo Chemical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Koppert Biological Systems is channeling USD 93 million into its fourth facility in Brazil, set to wrap up in 2026 in Piracicaba, São Paulo. This move bolsters Koppert's strategy to expand in the region's leading market for biological inputs, with a keen focus on crop protection.

- June 2025: Koppert Biological Systems plans to invest USD 37.20 million in Brazil. By 2030, the company aims to set up two new manufacturing plants, bolstering its presence in tropical agriculture. This move comes in response to escalating pest and disease challenges in the region. The investment underscores Koppert's commitment to research and development (R&D), especially in the realm of biological crop protection tailored for tropical settings.

- October 2024: Rovensa Next announced three major milestones in Colombia and Perú. The company has secured registrations for Naturdai Mim, a plant extract biofungicide, Santem, a pyrethrin-based bioinsecticide, and Kuneka, a bioinsecticide-acaricide derived from Karanja oil and Neem extract. These registrations not only highlight Rovensa Next’s dedication to pioneering organic agriculture but also bolster its regional portfolio of biosolutions.

South America Biopesticides Market Report Scope

Biopesticides are substances derived from natural or biological sources, used to manage pests such as insects, weeds, fungi, and other harmful organisms. They are designed to minimize environmental impact and risks to human health. Biopesticides include microbial pesticides, plant-derived pesticides, and biochemical agents that support sustainable crop protection. The South America Biopesticides Market is segmented by form, including biofungicides, bioherbicides, and bioinsecticides; by crop type, including cash crops, horticultural crops, and row crops; and by geography, covering Argentina and Brazil. The market forecasts are provided in terms of value in USD and volume in metric tons.

Form

| Biofungicides |

| Bioherbicides |

| Bioinsecticides |

| Other Biopesticides |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

By Geography

| Argentina |

| Brazil |

| Rest of South America |

| Form | Biofungicides |

| Bioherbicides | |

| Bioinsecticides | |

| Other Biopesticides | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops | |

| By Geography | Argentina |

| Brazil | |

| Rest of South America |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biopesticides applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biopesticides prevent or control various pests, including insects, diseases, and weeds, from causing crop damage and yield loss.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.