Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

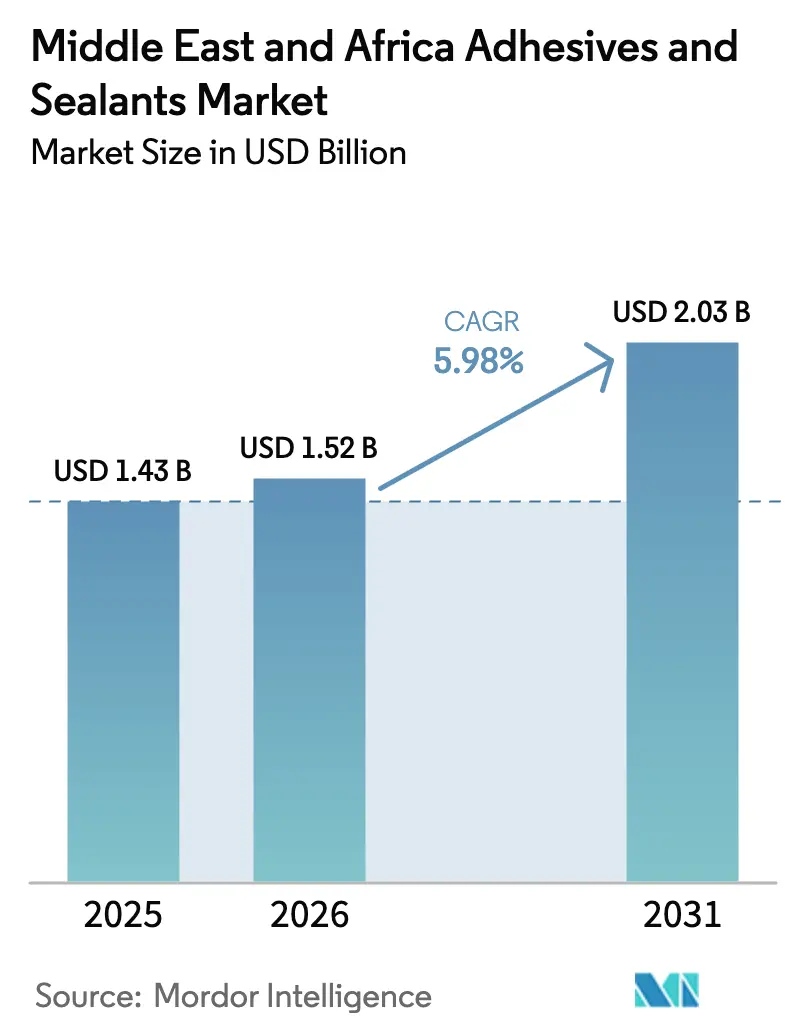

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Adhesives And Sealants Market Analysis by Mordor Intelligence

The Middle East And Africa Adhesives And Sealants Market size was valued at USD 1.43 billion in 2025 and is estimated to grow from USD 1.52 billion in 2026 to reach USD 2.03 billion by 2031, at a CAGR of 5.98% during the forecast period (2026-2031). Structural shifts toward water-borne and reactive chemistries, along with large-scale infrastructure spending in Saudi Arabia and tightening volatile-organic-compound (VOC) limits across the Gulf, underpin this expansion. Growing medical-device assembly in free zones, heightened e-commerce packaging demand, and rapid automotive output in Morocco and Egypt further lift demand. Multinationals use localized blending plants in Jeddah, Dubai, and Cairo to shorten lead times, while regional specialists safeguard their share with custom formulations and on-site technical support. Feedstock price swings and cold-chain gaps in East Africa remain headwinds, yet sustained capital inflows into modular housing, wind energy, and EV battery production continue to unlock new opportunities.

Key Report Takeaways

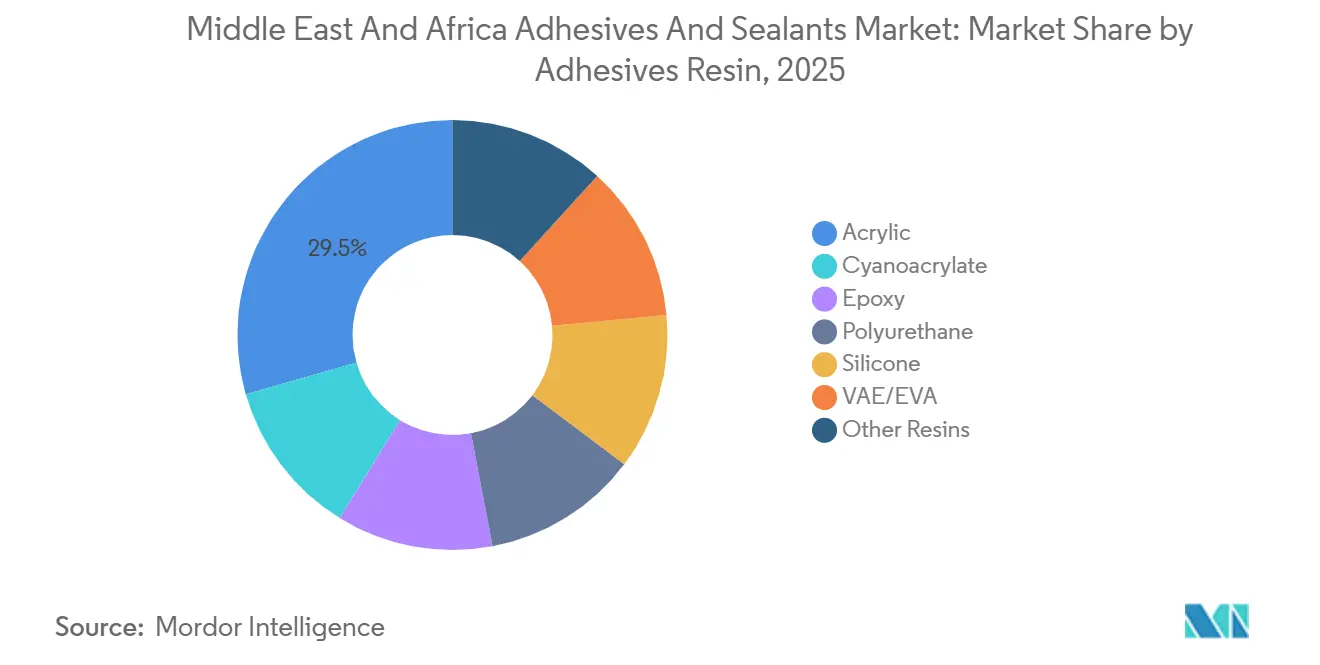

- By adhesive resin, acrylics captured 29.46% of 2025 demand, while polyurethanes are projected to post the fastest 6.24% CAGR through 2031.

- By adhesive technology, water-borne grades commanded 37.28% of 2025 demand; reactive systems expand at a leading 6.31% CAGR through 2031.

- By sealant resin, polyurethanes led with 41.37% share in 2025, whereas silicones are set to grow at 6.18% CAGR on façade and solar applications.

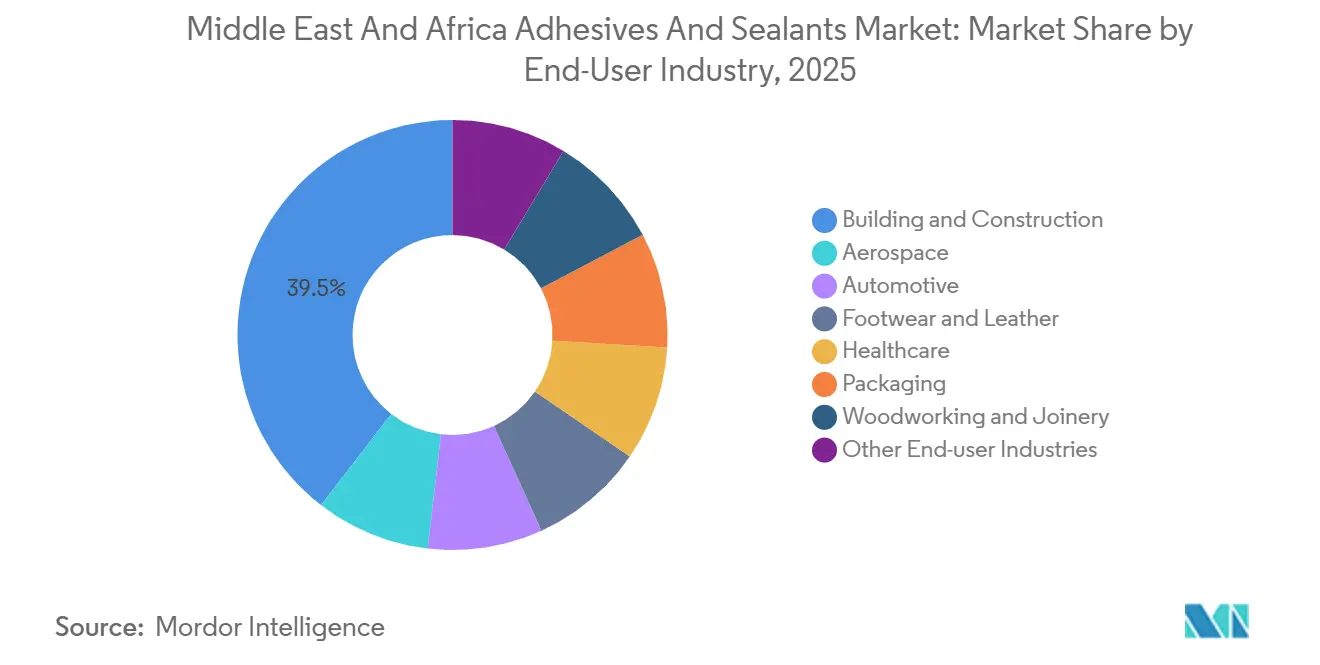

- By end-user, construction generated 39.52% of 2025 demand; healthcare adhesives deliver the fastest 6.27% CAGR thanks to wearable-sensor production in the UAE and Saudi Arabia.

- By geography, Saudi Arabia held a dominant 34.48% 2025 share, yet the United Arab Emirates is forecast to post a 6.12% CAGR on the back of Expo City and Masdar City projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Adhesives And Sealants Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction mega-projects under Saudi Vision 2030 | +1.8% | Saudi Arabia, with spill-over to UAE and Qatar | Long term (≥ 4 years) |

| E-commerce–led packaging boom across GCC and Egypt | +1.2% | GCC core (UAE, Saudi Arabia, Kuwait), Egypt | Medium term (2-4 years) |

| Automotive OEM and aftermarket expansion in Morocco and Egypt | +0.9% | Morocco, Egypt, with exports to EU and sub-Saharan Africa | Medium term (2-4 years) |

| Modular construction uptake in East Africa | +0.6% | Kenya, Ethiopia, Tanzania | Long term (≥ 4 years) |

| Gulf localisation mandates for hygiene-product adhesives | +0.5% | Saudi Arabia, UAE, Bahrain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction Mega-Projects Under Saudi Vision 2030

The Public Investment Fund deployed USD 40 billion in 2025 into anchor projects such as NEOM, Qiddiya, and King Salman Park[1]Public Investment Fund, “Annual Report 2025,” pif.gov.sa. Curtain-wall glazing at NEOM’s linear city uses structural silicone sealants formulated with UV-blocking additives to withstand 12 hours of daily sun exposure. Marine villas in the Red Sea Development rely on polyurethane adhesives able to resist 3,000-hour salt-fog cycles, prompting new one-component systems from Sika and Wacker Chemie. Fast-cure epoxies on precast panels accelerate schedules by 40%, reducing labor on mega sites. Similar specifications extend to Lusail City Phase II in Qatar, where reactive polyurethane sealants bond composite cladding on high-rise towers.

E-Commerce–Led Packaging Boom Across GCC and Egypt

United Arab Emirates e-commerce gross merchandise value reached USD 9.2 billion in 2025, boosting corrugated-box demand 18% year on year and pushing uptake of water-borne starch adhesives that satisfy food-contact regulations. Egyptian paperboard output climbed to 1.8 million metric tons in 2025 as Amazon and Noon scaled fulfillment hubs, driving hot-melt adhesive usage on 60-carton-per-minute lines. H.B. Fuller’s 2025 polyolefin hot-melt bonds recycled kraft liner at 15 °C lower temperatures, cutting converter energy use by 12%. Saudi e-commerce penetration doubled to 14% of retail sales, prompting Jowat to open a Riyadh technical center for tamper-evident tape formulations. Reactive polyurethane laminating adhesives are also displacing acrylic emulsions in retort pouches that survive 121 °C sterilization.

Automotive OEM and Aftermarket Expansion in Morocco and Egypt

Morocco built 535,000 vehicles in 2025, making it Africa’s top exporter, with 4,200 metric tons of structural adhesives consumed in body-in-white bonding and battery-tray assembly[2]Automotive World, “Morocco Vehicle Assembly Statistics 2025,” automotiveworld.com. BYD announced a 150,000-unit EV plant in Tangier that will rely on conductive adhesives for lithium-iron-phosphate cell interconnects, a niche Henkel targets with its Loctite ECI 1020 series. Egypt granted golden licenses in 2025, allowing Volkswagen to produce 50,000 units yearly, using hot-melt adhesives for headliners and polyurethanes for windshield bonding. The aftermarket absorbs cyanoacrylate adhesives for mirror reattachment and acrylic tapes for emblem replacement, distributed through Petromin and TotalEnergies channels. Moroccan parts exports hit EUR 12 billion in 2025, with tier-1 suppliers meeting ISO 9001 and IATF 16949 via epoxy adhesives on airbag modules.

Modular Construction Uptake in East Africa

Kenya’s affordable-housing effort delivered 42,000 modular units in 2025, each using polyurethane adhesives to bond EPS-steel sandwich panels, enabling three-day on-site assembly. Ethiopia’s Hawassa and Mekelle industrial parks adopted precast concrete modules joined with epoxy adhesives that meet Ethiopian seismic code ES 8-2015. Tanzania’s construction sector grew 7.8% in 2025, with bus rapid-transit stations using structural acrylic adhesives that cure in humid conditions without primer, sourced from regional distributors. The East African Community’s Vision 2050 earmarks USD 100 billion for cross-border rail and port projects, specifying adhesive-bonded composites to lower maintenance. Despite progress, only 18% of Mombasa-Kampala freight routes offered refrigerated containers in 2025, limiting water-borne adhesive penetration.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC regulations and green-building codes | -0.7% | UAE, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Petrochemical feedstock price volatility | -0.9% | Global, with acute impact on GCC solvent-borne producers | Short term (≤ 2 years) |

| Limited cold-chain logistics for water-borne chemistries | -0.4% | East Africa (Kenya, Ethiopia, Tanzania) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Regulations and Green-Building Codes

Dubai’s Green Building Regulations cap interior adhesive VOC content at 50 g/L and exterior at 100 g/L, steering formulators toward water-borne systems. South Africa’s Green Star rating introduced a 30 g/L incentive threshold that just 12% of imported products met in 2025. Saudi Arabia adopted GSO 2756 in 2024, mirroring EU limits and extending product-launch cycles by six weeks due to third-party tests. Reformulation costs reach up to USD 150,000 per product, deterring smaller players and consolidating share among multinationals with dedicated R&D budgets. Egypt deferred its proposed VOC law to 2027, injecting uncertainty into planned water-borne investment.

Petrochemical Feedstock Price Volatility

Propylene traded between USD 950 and USD 1,150 per metric ton in 2025 following outages at the Ras Tanura cracker, pressuring solvent-borne margins. Benzene averaged USD 1,020 per metric ton in Q4 2025, 18% above Q1, inflating costs for styrene-based adhesives. Dow’s SADARA venture moved to quarterly price resets that passed through 70% of volatility, squeezing smaller converters without hedging tools. Egyptian formulators faced additional foreign-exchange risk when the pound weakened 12% versus the U.S. dollar, lifting isocyanate import costs and causing six-week production pauses. Transport premiums from Rotterdam to Casablanca climbed USD 120 per metric ton after Red Sea shipping diversions, pushing Moroccan blenders to renegotiate feedstock contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesives Resin: Acrylics Anchor Packaging, Polyurethanes Accelerate

Acrylic adhesives held 29.46% of 2025 demand, the highest share within the Middle East and Africa adhesives and sealants market, owing to their fast-tack performance in pressure-sensitive tapes used for e-commerce parcels. Polyurethane grades are forecast to expand at a 6.24% CAGR, outpacing all other chemistries as automotive windshield bonding in Morocco and structural glazing in Saudi Arabia demand elongation-at-break above 400%. Epoxy systems are witnessing increased demand from wind-turbine blade and precast-concrete bonding, yet their two-hour pot life constrains uptake on rapid site schedules. Silicone adhesives find their applications mainly in high-temperature automotive and wearable-sensor applications where ISO 10993 biocompatibility is mandatory.

Wider substitution trends favor acrylics in packaging laminates for snack foods, while polyurethanes gain in modular-construction panel assembly. Cyanoacrylates remain niche in aftermarket repair, and VAE/EVA hot-melts dominate carton sealing with Jowat and H.B. Fuller controlling 60% regional supply. Phenolic and polyamide adhesives stay stable in brake-lining and textile lamination. As infrastructure megaprojects advance, the Middle East and Africa adhesives and sealants market size linked to polyurethane formulations is projected to rise disproportionately within overall growth, reinforcing supplier investments in local pre-polymer synthesis.

By Adhesives Technology: Water-Borne Formulations Lead Compliance Shift

Water-borne chemistries accounted for 37.28% of 2025 demand following Dubai’s 50 g/L VOC ceiling, the largest technology share across the Middle East and Africa adhesives and sealants market. Reactive systems, including two-component epoxies and moisture-cure polyurethanes, are projected to grow at a 6.31% CAGR through 2031 as battery-pack assembly and composite panel bonding prioritize high strength with rapid cure. Hot-melts are used in high-speed packaging lines, where polyolefin bases reduce energy use by 12% over EVA options.

Solvent-borne grades face incremental regulation that restricts their expansion. UV-cured adhesives are witnessing rising demand after Sika introduced a silicone sealant that cures in eight seconds under LED lamps, halving automotive glass line dwell time. As compliance deadlines tighten, the Middle East and Africa adhesives and sealants market share of water-borne and UV platforms will rise, compelling legacy solvent formulators to retool or exit low-margin segments.

By Sealants Resin: Polyurethane Dominates, Silicone Surges in Facades

Polyurethane sealants held a commanding 41.37% share in 2025, securing the highest stake in sealant demand within the Middle East and Africa adhesives and sealants market. Superior joint movement and paintability make them standard in Saudi expansion joints and Egyptian residential builds. Silicone sealants are predicted to grow at a 6.18% CAGR on the strength of curtain-wall glazing in UAE towers and solar-panel edge sealing in Morocco’s Noor complex, where −40 °C to 150 °C tolerance is essential. Acrylic sealants serve kitchens and bathrooms that value low odor but accept limited movement capability.

Epoxy sealants dominate industrial flooring and marine decks, where diesel and saltwater resistance offset their higher cost. Polysulfides fulfill niche aviation demand given MIL-S-8802 compliance. Wacker’s silane-terminated polyether range gains traction in bus and truck manufacturing, reflecting growing hybrid polymer interest. As façade area per building rises, the Middle East and Africa adhesives and sealants market size allocated to silicone systems is poised to widen, challenging polyurethane incumbency on life-cycle costs.

By End-User Industry: Construction Leads, Healthcare Accelerates

Building and construction consumed 39.52% of 2025 demand, driven by Saudi Vision 2030 sites that specify structural silicones for glass facades and polyurethanes for insulated panels.

Automotive consumption in the region is centered on Morocco and Egypt, where structural bonding trims vehicle weight by up to 12 kg. The woodworking industry in the region mainly demands polyvinyl acetate emulsions, prominent in furniture manufacturing across South Africa and Saudi Arabia. Footwear and leather captured a considerable share, still solvent-intensive despite rising VOC scrutiny. Aerospace and other segments demand flame-smoke-toxicity-compliant adhesives used in cabin interiors. Shifting demographics and regulatory mandates will keep construction dominant, yet the healthcare slice of the Middle East and Africa adhesives and sealants market share will climb fastest through the forecast period.

Geography Analysis

Saudi Arabia commanded 34.48% of 2025 revenue, the largest portion of the Middle East and Africa adhesives and sealants market, energized by USD 40 billion in annual Vision 2030 disbursements for projects such as Trojena ski resort and King Salman Park. The United Arab Emirates is on track for a 6.12% CAGR to 2031 as Expo City pavilions and Masdar City Phase III embed low-VOC mandates favoring water-borne adhesives. Dubai’s Green Building Regulations, Masdar clean-energy targets, and a resurgent hospitality pipeline sustain broad adoption of water-borne acrylics and low-modulus silicones. Abu Dhabi’s industrial strategy now extends incentives to battery materials, opening fresh use cases for one-component moisture-cure adhesives. Free-zone duty exemptions lower landed raw-material costs, further boosting competitiveness.

South Africa, Egypt, and Morocco contribute diverse but smaller revenue blocks. South Africa couples infrastructure refurbishment with automotive glass encapsulation that uses UV-cured silicones. Egypt benefits from e-commerce packaging and new vehicle assembly, yet currency devaluation widens working-capital demands. Morocco’s automotive corridor draws conductive and structural epoxies into EV battery lines. East African markets offer modular housing as the main vector, although logistics hurdles cap water-borne growth. Collectively these patterns highlight how local regulations, currency dynamics, and industrial policy shape the trajectory of the Middle East and Africa adhesives and sealants market.

Competitive Landscape

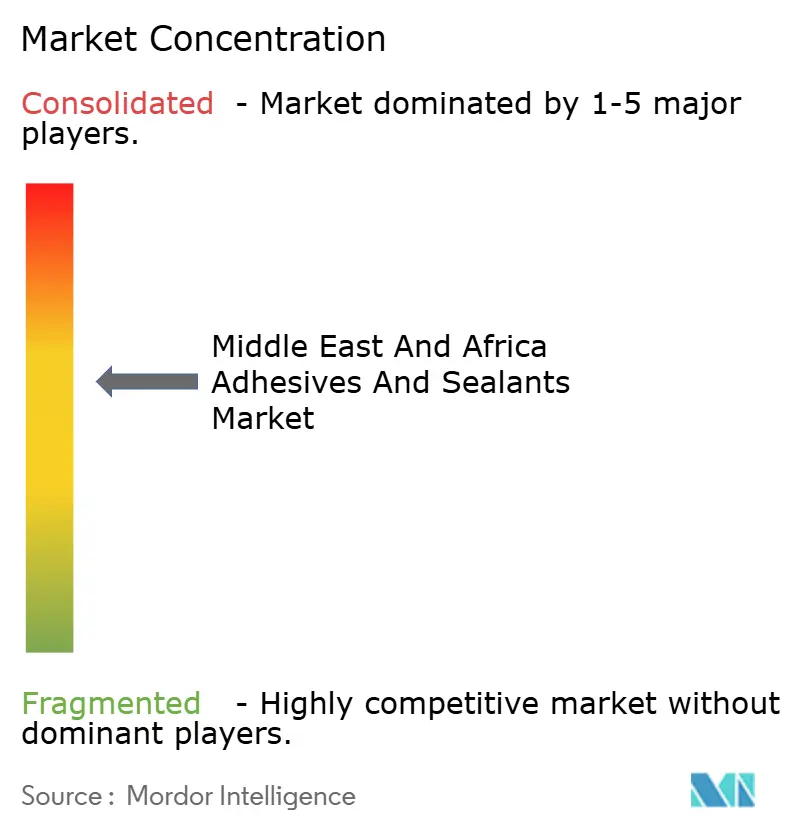

The Middle East and Africa adhesives and sealants market is moderately consolidated, with the top five holding a significant market size. Each leading player operates blending or compounding plants inside the region to reduce shipping lead times and tailor formulations to desert climates. Henkel’s 12,000-metric-ton hot-melt line in Jubail Industrial City came online in January 2025 to serve hygiene-product makers and meet Gulf localization quotas. Regional specialists, notably Permoseal in South Africa and The Industrial Group in Saudi Arabia, are delivering niche marine-grade and high-temperature gasket solutions with rapid on-site support. Technology differentiation leans on VOC compliance and cure-speed gains. Smaller players struggle with feedstock volatility after propylene price swings of 21% in 2025 forced three Egyptian blenders offline for six weeks. White-space opportunities span healthcare adhesives for wearable sensors and reactive polyurethanes for EV battery encapsulation, areas where regulatory approval paths are still forming.

Middle East And Africa Adhesives And Sealants Industry Leaders

Henkel AG & Co. KGaA

Sika AG

Dow

Arkema

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: H.B. Fuller introduced a polyolefin hot-melt in Egypt that bonds recycled kraft at 15 °C lower temperatures, saving converters 12% in energy.

- March 2025: Sika acquired a 60% stake in a Moroccan distributor, gaining 42 service centers across Casablanca, Tangier, and Marrakech.

- January 2025: Henkel began commercial production on a 12,000-metric-ton hot-melt line in Jubail Industrial City, trimming Gulf hygiene-adhesive lead times to 10 days.

Middle East And Africa Adhesives And Sealants Market Report Scope

Adhesives are made from a combination of resins, additives, and solvents. Adhesives are substances that bond different substrates and provide high shear strength, withstand severe peel forces, and provide superior chemical resistance. Sealants are substances primarily used to block or seal the gap between two surfaces. It provides excellent flexibility, corrosion resistance, and strength.

The market is segmented by adhesives resin, technology, sealants resin, end-user industry, and geography. By adhesives resin, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into hot melt, reactive, solvent-borne, UV-cured, and waterborne. By sealant resin, the market is segmented into polyurethane, epoxy, acrylic, silicone, polysulfide, and other resins. By end-user industry, the market is divided into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. The report also covers market estimates and forecasts for adhesives and sealants for 6 major countries in the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

By Adhesives Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Adhesives Technology

| Hot-Melt |

| Reactive |

| Solvent-Borne |

| UV-Cured |

| Water-Borne |

By Sealants Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Polysulfide |

| Other Resins |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

By Geography

| Saudi Arabia |

| South Africa |

| United Arab Emirates |

| Qatar |

| Bahrain |

| Egypt |

| Rest of Middle-East and Africa |

| By Adhesives Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Adhesives Technology | Hot-Melt |

| Reactive | |

| Solvent-Borne | |

| UV-Cured | |

| Water-Borne | |

| By Sealants Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Polysulfide | |

| Other Resins | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Qatar | |

| Bahrain | |

| Egypt | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

How fast is demand expected to grow for adhesives and sealants across the Middle East and Africa?

The Middle East and Africa adhesives and sealants market is forecast to expand at 5.98% CAGR from 2026 to 2031, lifting value from USD 1.52 billion to USD 2.03 billion.

Which country contributes the largest revenue to regional consumption?

Saudi Arabia generated 34.48% of 2025 revenue, buoyed by Vision 2030 mega-projects that specify high-performance silicones and polyurethanes.

What resin type shows the quickest growth outlook?

Polyurethane adhesives lead growth with a 6.24% CAGR thanks to their expanding use in automotive bonding and structural glazing.

How are VOC rules shaping technology choices?

UAE, Saudi Arabia, and South Africa now restrict interior VOC content to as low as 30–50 g/L, accelerating the switch to water-borne and UV-cured technologies.

Which end-user vertical is advancing the fastest?

Healthcare applications—especially wearable sensors and medical-device assembly—are projected to post a 6.27% CAGR through 2031.

What tactics are suppliers using to protect margins amid feedstock swings?

Multinationals operate regional blending plants, lock long-term propylene contracts, and introduce low-temperature cure chemistries that cut customer energy costs.

Page last updated on: