Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

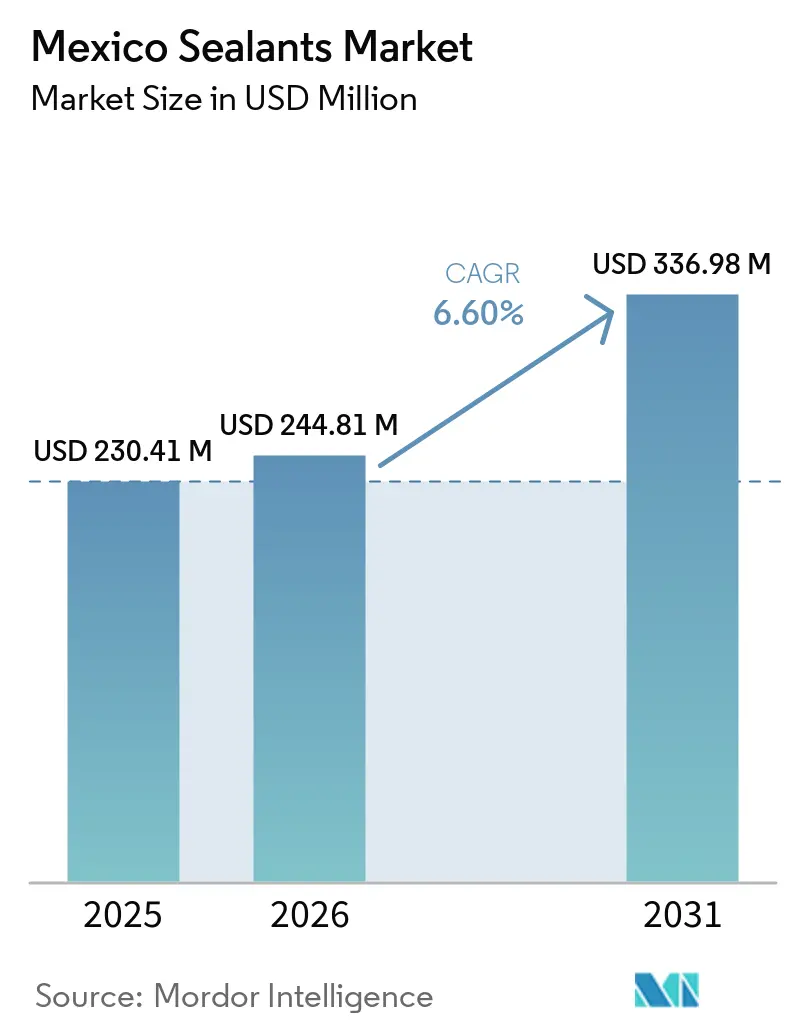

| Base Year Market Size (2025) | USD 230.41 Million |

| Market Size (2026) | USD 244.81 Million |

| Market Size (2031) | USD 336.98 Million |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

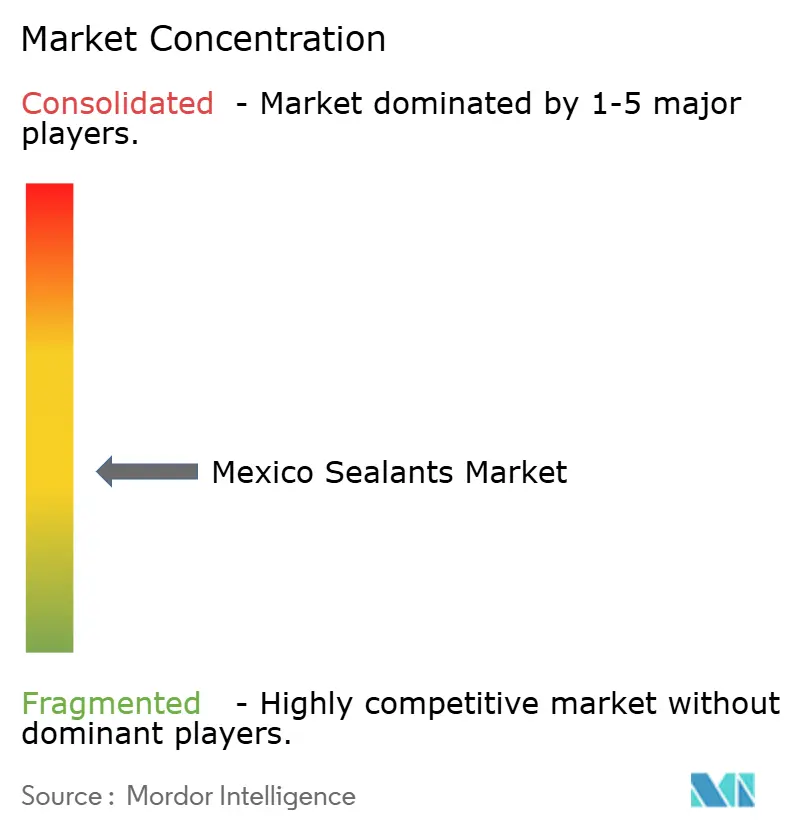

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Sealants Market Analysis by Mordor Intelligence

The Mexico Sealants Market size is expected to grow from USD 230.41 million in 2025 to USD 244.81 million in 2026 and is forecast to reach USD 336.98 million by 2031 at 6.60% CAGR over 2026-2031. Surging federal housing programs, a rebound in light-vehicle manufacturing, and a USD 40.9 billion near-shoring inflow have synchronized to push demand for silicone, polyurethane, and hybrid chemistries beyond normal construction-cycle pacing. Supply chains are being rewired around low-VOC rules, prompting backward integration into resins and accelerating the shift from solvent-based to water-borne or moisture-cure products. Specialty-grade volumes are rising in aerospace clusters that already exported USD 10.7 billion in 2024, while modular construction is amplifying linear-joint meters per dwelling. Together, these vectors raise the strategic importance of the Mexico sealants market for global producers looking to balance North-American capacity with tariff-resilient access.

Key Report Takeaways

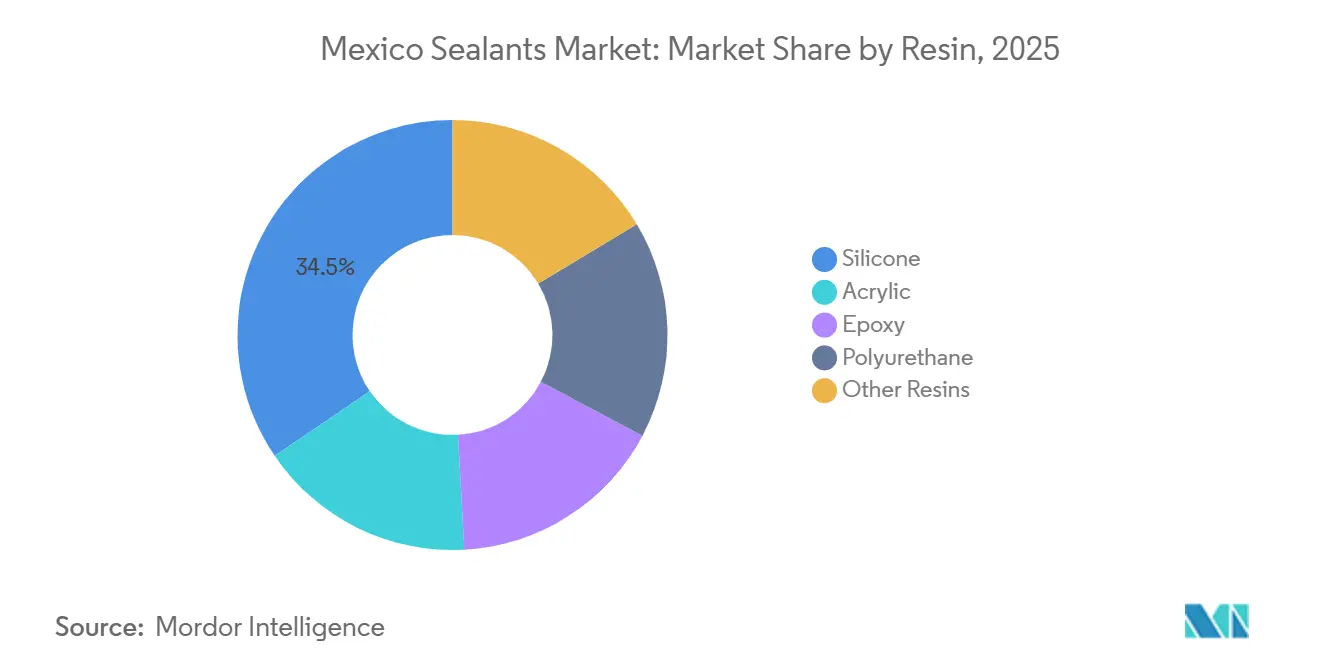

- By resin, silicone commanded 34.50% of the Mexico sealants market share in 2025, while polyurethane is forecast to post the fastest growth at a 7.26% CAGR to 2031.

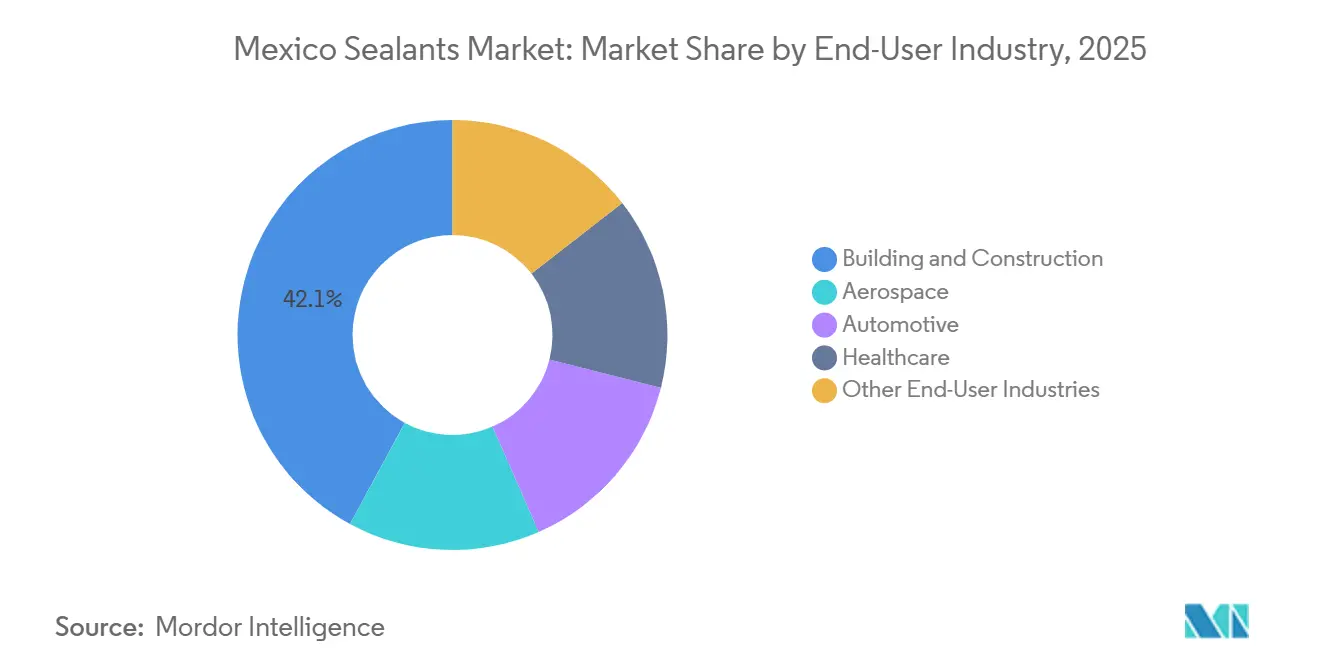

- By end-user, building and construction held 42.10% of value in 2025; automotive is projected to expand at 7.6% CAGR through 2031, outpacing every other sector

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Sealants Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and infrastructure boom supported by government programmes | +2.1% | National, with concentration in Tamaulipas, Coahuila, Nuevo León, Yucatán, Puebla, Veracruz | Medium term (2-4 years) |

| Resurgent automotive manufacturing and export volumes under USMCA | +1.6% | Northern states: Coahuila, Nuevo León, Guanajuato, Aguascalientes, San Luis Potosí, Querétaro | Short term (≤ 2 years) |

| Accelerating near-shoring wave bringing new industrial facilities | +1.8% | National, with early gains in Nuevo León, Querétaro, Jalisco, Bajío region | Medium term (2-4 years) |

| Prefabricated / modular construction driving fast-curing sealant demand | +0.9% | Urban centers: Mexico City, Guadalajara, Monterrey, Querétaro, Puebla | Short term (≤ 2 years) |

| Growth of aerospace clusters boosting specialty sealants | +0.6% | Querétaro, Sonora, Baja California, Chihuahua, Nuevo León | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction And Infrastructure Boom Supported By Government Programs

Federal housing initiatives targeting 1.8 million new homes by 2030 are already advancing more than 390,000 subscriptions, channeling acrylic and silicone volumes into window glazing, bathroom waterproofing, and façade joints[1]Comisión Nacional de Vivienda, “Programa de Vivienda para el Bienestar 2025 Update,” gob.mx. Early-stage completions cluster in northern states before February 2026, giving inventory advantages to distributors holding stock near the border. Beyond housing, the Plan México program allocates MXN 5.6 trillion to rail corridors, energy, and water projects, each requiring specialized tunnel and station sealants that must satisfy environmental-compliance clauses. Procurement rules now favor low-VOC formulations, accelerating market migration toward water-based chemistries even ahead of mandatory cut-over dates. Suppliers with pre-certified products, therefore, secure first-call status for bulk federal bids.

Resurgent Automotive Manufacturing And Export Volumes Under USMCA

Light-vehicle output recovered to 3.95 million units in 2025, with 3.38 million exported to the United States, re-establishing Mexico as North America’s assembly hub. GM’s USD 1 billion reinvestment through 2026 and rising hybrid penetration are enlarging polyurethane demand per vehicle for battery packs and windshield bonding. Hybrid layouts introduce extra sealing nodes for thermal management, raising per-unit material intensity even if total builds plateau. Sealant suppliers co-locate mixing plants next to Coahuila and Guanajuato assembly lines to honor just-in-sequence logistics windows measured in hours. USMCA review uncertainty delays some expansion, but the treaty’s regional-content rules embed Mexico in the long-term supply calculus, buffering the Mexico sealants market from short-term tariff noise.

Accelerating Near-Shoring Wave Bringing New Industrial Facilities

Foreign investors poured USD 40.9 billion into Mexico in 2025, with industrial parks absorbing USD 4.1 billion for electronics, medical devices, and logistics hubs. Build schedules compressed to 12-18 months, pushing contractors toward single-component polyurethane and hybrid polymers that cure in under six hours and slash labor. Investment Zones offering 100% income-tax credits through year three are funneling projects into Nuevo León, Puebla, and the AIFA-Tula corridor, creating localized order spikes. Early movers in the Mexico sealants market that pre-stage warehouses inside these zones are locking multi-year master-supply agreements that include escalation clauses tied to petrochemical indices, securing both volume and margin.

Prefabricated / Modular Construction Driving Fast-Curing Sealant Demand

Twenty percent of Mexico City’s 20,000-unit affordable-rental target now uses factory-built floor and bathroom pods. Each modular home carries 30% more linear-joint meters than cast-in-place builds, offsetting any labor savings and lifting aggregate consumption. Moisture-cure polyurethane and silyl-modified hybrids deliver handling strength within hours, keeping assembly lines moving. Indoor air-quality certifications mandate low-VOC products, nudging contractors away from legacy solvent-based lines still common in informal retail outlets. Suppliers offering paintable, low-odor options, therefore, command premium shelf space at big-box retailers serving self-build volume.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical feedstock prices pressuring margins | -0.8% | National, with acute impact on formulators in Estado de México, Jalisco, Nuevo León | Short term (≤ 2 years) |

| Tightening VOC regulations on solvent-based chemistries | -0.5% | National, with stricter enforcement in Mexico City, Guadalajara, Monterrey metropolitan areas | Medium term (2-4 years) |

| Import dependence for specialty resins causing supply bottlenecks | -0.3% | National, affecting aerospace and healthcare end users in Querétaro, Sonora, Baja California | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Prices Pressuring Margins

Pemex output collapsed to 4,000 tons of polyethylene in 2025 from 252,000 tons in 2020, forcing more than half of resin inputs to be imported at prices that swung 27% during the year. Smaller Mexican formulators lack hedging tools, so quarterly repricing can wipe out project gross profit. Pemex has earmarked USD 4.2 billion to revive ethylene capacity by 2030, but the five-year lag cements feedstock security as a moat for majors owning captive resin plants. PPG’s 2025 low-emission expansion in Tepexpan and BASF’s antioxidants line in Puebla (complete end-2026) illustrate how integration shields EBITDA and gives marketing leverage on sustainability score.

Tightening VOC Regulations On Solvent-Based Chemistries

A draft rule floated in July 2023 layers stricter VOC caps atop NOM-123-SEMARNAT-1998, with enforcement pilots already active in the three largest metros. Contractors face 15%-25% cost premiums for compliant products and must retrain applicators to manage humidity sensitivity. Public tenders increasingly require ISO 14001 credentials, quietly sidelining non-compliant suppliers from billion-dollar housing and rail budgets. The Mexico sealants market, therefore, bifurcates: accredited players compete for institutional projects, while cash-strapped builders gravitate toward lower-priced solvent lines in the informal channel, complicating demand forecasts for every resin class.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Gains As Automotive And Modular Construction Converge

Silicone captured 34.5% of the Mexico sealants market share in 2025 for its dominance in aerospace fuel-tank sealing and long-life façade joints. Polyurethane is on track for a 7.26% CAGR through 2031, powered by structural glazing in vehicles and six-hour cure cycles in panelized housing. The Mexico sealants market size tied to epoxy remains confined to industrial floors and composite bonding but commands premium pricing. Acrylic retains carpenter loyalty for interior trim, yet hybrid silyl-modified polymers are eroding its base by combining paintability with 25% joint movement capability.

Rising hybrid-vehicle output elevates polyurethane kilos per car, while modular construction magnifies linear meters per dwelling, together lifting polyurethane tonnage faster than headline demand. Silicone continues to grow in absolute volume but will cede small share to hybrids tailored for mixed-climate durability and quick paint-over. Resin supply chains are diverging: aerospace and automotive draw from ISO-certified plants with multi-batch QC, whereas residential acrylic remains a price fight in informal retail outlets. Suppliers able to flex across both regimes secure broader wallet share.

By End-User Industry: Automotive Overtakes Construction In Growth Velocity

Building and construction absorbed 42.1% of the value in 2025 as federal housing outlays surpassed MXN 513 billion. Yet automotive will add the most marginal pesos, advancing at 7.6% CAGR to 2031, as battery enclosures, hybrid cooling loops, and lightweight bonding push sealant spend per vehicle up by double digits. The Mexico sealants market size attached to aerospace sits below 10% of the total, but its high unit prices and AS9100 lock-in deliver an outsized margin. Healthcare, though still nascent, is climbing on the back of medical-device near-shoring, such as Domico Med-Device’s Celaya launch.

Construction demand is cyclical and project-dependent, but automotive orders arrive in level-loaded weekly buckets, smoothing factory utilization for polyurethane and silicone lines. Aerospace sales, in contrast, follow long-horizon MRO schedules and tight batch-traceability queues, making capacity planning a high-value puzzle. Suppliers balancing these rhythms with dedicated small-batch reactors and high-throughput mixers maximize both plant uptime and portfolio margin.

Geography Analysis

Northern border states commanded largest market in 2025, leveraging proximity to U.S. customers and housing 26% of the national automotive capacity. Nuevo León’s Monterrey axis alone hosts USD 4.1 billion in active industrial-park builds, consuming epoxy floor sealants during fit-out and polyurethane glazing in curtain walls. Coahuila’s Ramos Arizpe and Derramadero corridors anchor GM and Stellantis volumes, pulling polyurethane windshield beads in just-in-time cadence. Chihuahua’s MXN 16.961 billion aerospace output makes it the top buyer of MIL-PRF silicones.

The Central Mexico sealants market demand is led by Guanajuato, Querétaro, and San Luis Potosí within the Bajío auto belt. Querétaro’s Aerocluster funnels specialty sealant demand into NADCAP-certified channels and supports SME tier-2 suppliers adopting robotic extrusion. Guadalajara’s smart-city retrofits emphasize low-VOC acrylics and hybrids for LEED targets. Central geography lets distributors trans-ship both north to export-oriented factories and south to resort construction, creating scale in third-party logistics contracts.

Southern and coastal states are witnessing rising market growth with Yucatán and Quintana Roo rallying behind tourism and affordable-rental pipelines. Prefab pilot projects in Mérida demand fast-cure hybrids, while hotel builds in Cancún specify salt-spray-resistant silicones. Puebla gains strategic weight from BASF’s upcoming antioxidants plant, which will seed an integrated supply hub for polyurethane pre-polymers serving both automotive and white-goods clusters.

Competitive Landscape

The Mexico sealants market is moderately fragmented. Strategic plays center on low-VOC lines, captive resin, and robotics-ready rheology. PPG doubled powder-coating capacity at San Juan del Río in January 2026 to service auto and general industry needs, embedding low-emission technologies ahead of metro compliance deadlines[2]PPG Industries, “Press Release: San Juan del Río Expansion,” ppg.com. BASF’s antioxidants expansion in Puebla, due by the end of 2026, shores up urethane additive supply and reduces import risk. H.B. Fuller’s 2025 portfolio pruning eliminates commodity flooring adhesives, freeing capex to chase high-margin aerospace and medical sealants.

Emerging disruptors push bio-based polymers that meet LEED credit paths and sell private-label SKUs through constructors’ merchants. Certification remains the moat: AS9100, ISO 13485, and SCAQMD Rule 1168 compliance barriers dampen new-entrant momentum. Consequently, competition tilts toward supply-chain resilience, guaranteed stock, 24-hour technical visits, and flexible MOQs, over price alone, positioning agile mid-caps to nibble share from multinational giants burdened by global re-tooling cycles.

Mexico Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

RPM International Inc.

Sika AG

DOW

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PPG completed an USD 11 million expansion at its San Juan del Río plant, doubling powder-coating capacity and adding low-emission resin lines aligned with upcoming VOC mandates.

- March 2025: BASF announced extra aminic antioxidants capacity in Puebla, with start-up slated for end-2026, to shorten supply chains for polyurethane and epoxy formulators.

Mexico Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Mexico sealants market is segmented by resin and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-User Industries |

| By Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-User Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms