Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

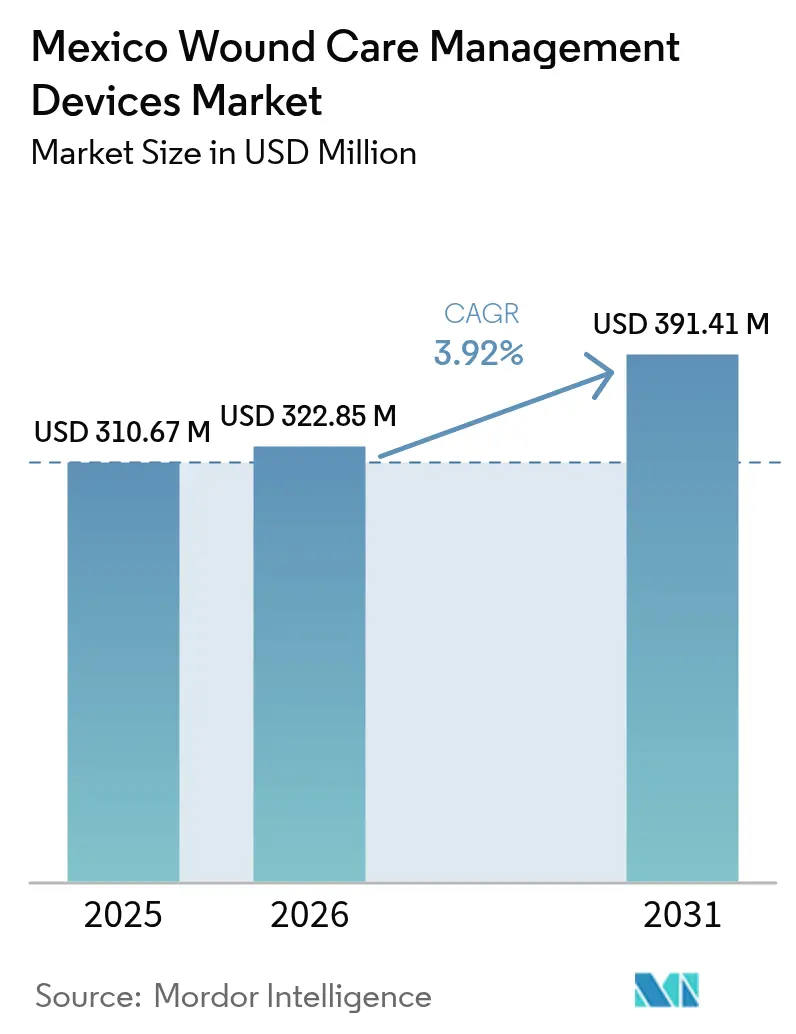

| Base Year Market Size (2025) | USD 310.67 Million |

| Market Size (2026) | USD 322.85 Million |

| Market Size (2031) | USD 391.41 Million |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Wound Care Management Devices Market Analysis by Mordor Intelligence

The Mexico wound care management devices market size was valued at USD 310.67 million in 2025 and estimated to grow from USD 322.85 million in 2026 to reach USD 391.41 million by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). This performance positions the Mexico wound care management devices market as a growing med-tech niche that is gradually reducing import dependence through nearshoring and domestic R&D initiatives. Demand momentum is anchored in Mexico’s diabetes prevalence of 14.7%—well above major regional peers—and the rapid modernization of public healthcare infrastructure under IMSS-BIENESTAR. Parallel investment by global suppliers in advanced therapies, coupled with tariff-driven interest in local manufacturing, underpins technology transfer to Mexican production clusters. Home-based care models, remote monitoring tools, and broader reimbursement coverage act as volume multipliers across both chronic and post-surgical wound applications.

Key Report Takeaways

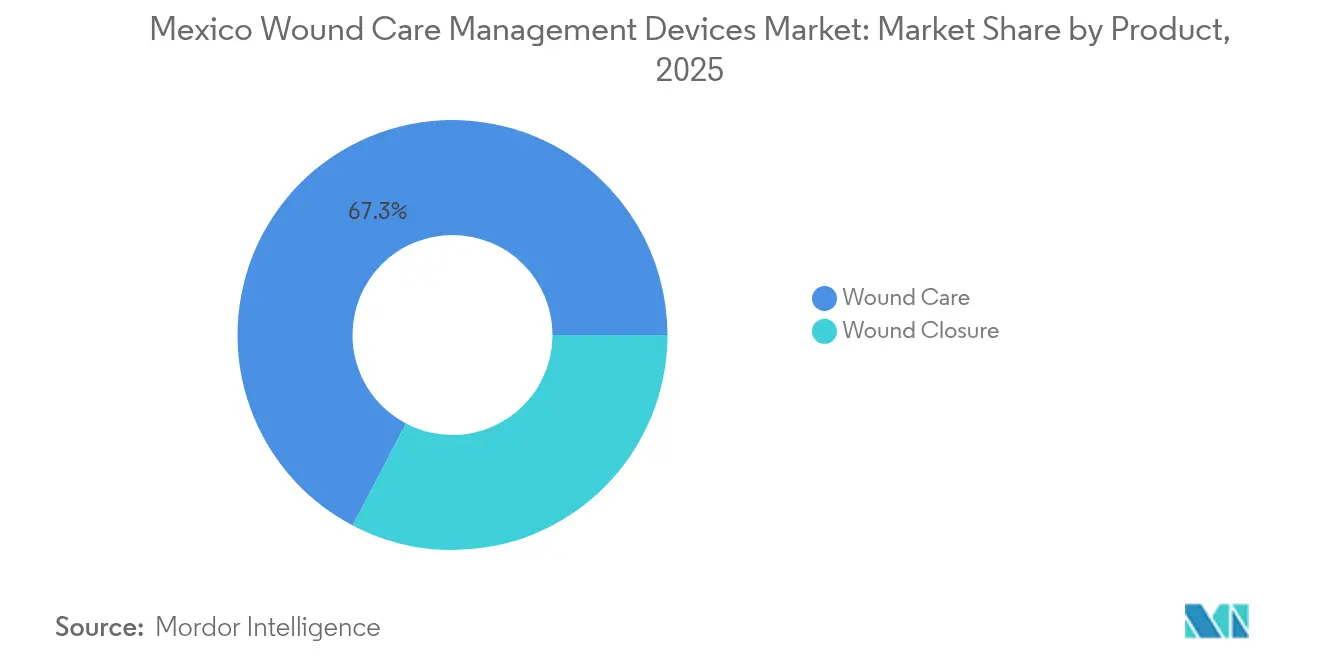

- By product category, Wound Care products led with a 67.31% revenue share of the Mexico wound care management devices market in 2025, while Wound Closure devices are forecast to expand at a 4.71% CAGR through 2031.

- By wound type, Chronic Wounds captured 60.98% of the Mexico wound care management devices market share in 2025; Acute Wounds are projected to grow at a 4.58% CAGR to 2031.

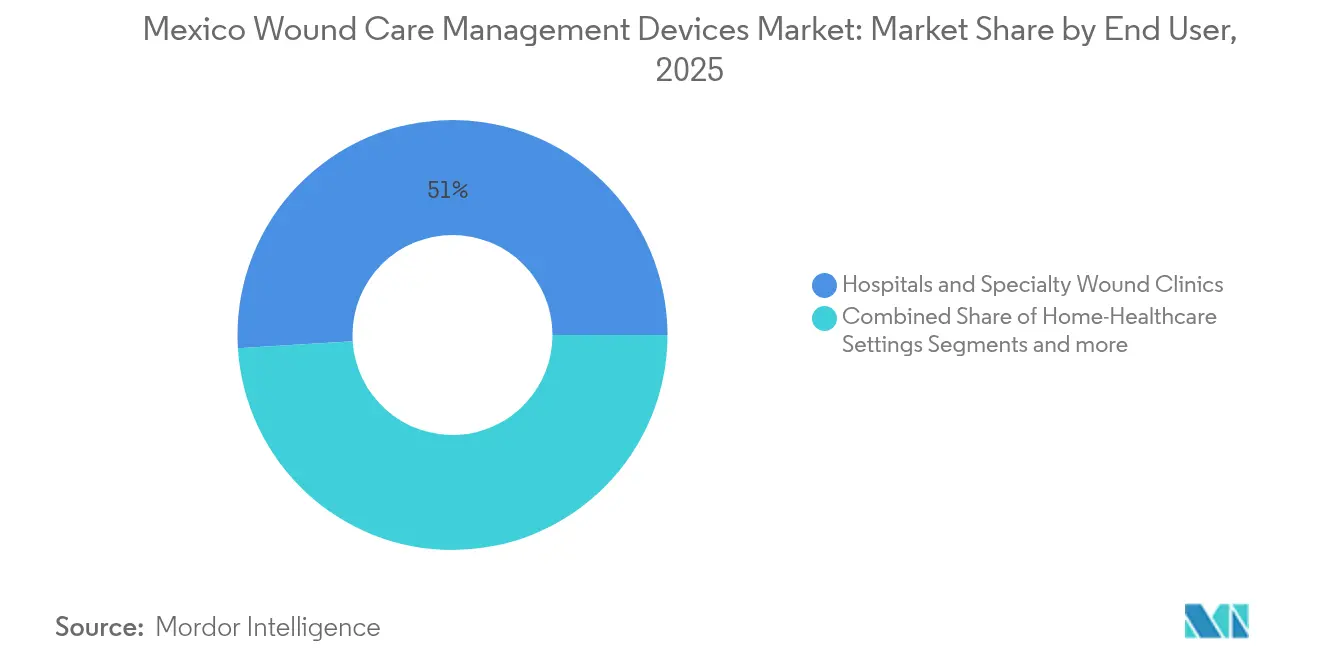

- By end user, Hospitals & Specialty Wound Clinics accounted for 50.98% share of the Mexico wound care management devices market size in 2025, whereas Home-Healthcare Settings are advancing at a 4.79% CAGR through 2031.

- By mode of purchase, Institutional Procurement commanded 67.35% of the Mexico wound care management devices market size in 2025, while the Retail/OTC Channel records the fastest CAGR at 4.68% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing chronic wounds & diabetic ulcers | +1.2% | National, concentrated in Southern states | Long term (≥ 4 years) |

| Rising volume of surgical procedures | +0.8% | Urban centers—Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Rapidly ageing Mexican population | +0.6% | National, accelerated in Northern border states | Long term (≥ 4 years) |

| Increasing advancements in wound care tech | +0.5% | Major metros with tertiary hospitals | Medium term (2-4 years) |

| Wider reimbursement under IMSS-BIENESTAR | +0.7% | Rural and underserved regions | Short term (≤ 2 years) |

| Emergence of domestic bio-based dressings | +0.3% | Research clusters—Mexico City, Guadalajara | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic Wounds & Diabetic Ulcers

Mexico’s diabetes epidemic intensifies the need for wound devices. Southern states, where prevalence reaches 10.2%, register the nation’s highest diabetic foot ulcer risk. IMSS data confirm that diabetic foot complications and kidney failure comprise 78% of preventable diabetic hospitalizations, pushing hospital costs higher even after efficiency gains. Peripheral neuropathy affects 54.5% of type 2 diabetics in Sinaloa, and inpatient diabetic foot therapy can cost MXN 6,457.64 per day, reinforcing the value proposition of advanced dressings. The chronic wound burden therefore sustains the Mexico wound care management devices market through 2030.

Rising Volume of Surgical Procedures

Hip fracture incidence is forecast to reach 155,874 cases by 2050, with an average treatment cost of USD 4,365 per case. Elective surgery capacity is scaling under IMSS-BIENESTAR modernization, while unified national clinical protocols reduce procedural variance across public and private hospitals. The resulting swell in surgical incisions and trauma care accelerates unit demand for sutures, staplers, and tissue adhesives, reinforcing growth in the Mexico wound care management devices market.

Rapidly Ageing Mexican Population

Adults aged ≥65 now represent 8.2% of the national census. Diabetes prevalence doubles within this cohort, elevating the risk of pressure ulcers, which already stand at 28.0% across second-level hospitals. Budget rationalization therefore channels funding toward preventive wound care devices that can reduce hospitalization frequency—a trend benefitting the Mexico wound care management devices market over the long term.

Increasing Advancements in Wound Care Technologies

Machine-learning smart bandages predict healing outcomes with 98% accuracy and reduce closure times to 14 days [1]Ahmad F. Turki, "A Bioelectrically Enabled Smart Bandage for Accelerated Wound Healing and Predictive Monitoring," MDPI, mdpi.com. Domestic laboratories have demonstrated that agave bagasse extracts yield 99.4% closure rates by day 13, outpacing controls [2]Herminia López-Salazar, "The Effect of Agave Bagasse Extract on Wound Healing in a Murine Model," MDPI, mdpi.com. Several tertiary centers are piloting chitosan-metformin formulations and bioelectrical stimulation, signaling faster adoption of premium technologies within the Mexico wound care management devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment & device cost | -0.9% | National, acute in rural areas | Medium term (2-4 years) |

| Limited clinician training on advanced tech | -0.6% | Rural and secondary hospitals | Short term (≤ 2 years) |

| Supply-chain delays due to regulatory gaps | -0.4% | Border manufacturing regions | Short term (≤ 2 years) |

| Counterfeit dressings in informal markets | -0.3% | Urban informal channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment & Device Cost

Daily inpatient therapy for pressure ulcers exceeds MXN 6,400, stretching public budgets. Diabetes complications consumed a large amount in direct and indirect costs. New import tariffs of 4-8% applied in 2025 elevate acquisition costs, leading hospitals to prioritize essential over premium devices.

Limited Clinician Training on Advanced Devices

IMSS treats more than 3.5 million diabetes patients yearly, but specialized wound care training remains limited outside major metros. National diabetic-foot teams are being scaled to close skills gaps. Without structured education, uptake of negative-pressure or bioelectrical systems slows in rural hospitals, softening penetration rates in the Mexico wound care management devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Amid Closure Growth

The Mexico wound care management devices market size analysis shows Wound Care products at a commanding 67.31% share in 2025, powered by chronic wound prevalence and the proven efficacy of advanced dressings. Natural-compound dressings, such as agave-based hydrogels, are gaining preference in tertiary hospitals due to strong clinical outcomes. Negative pressure wound therapy (NPWT) systems are penetrating high-acuity centers, buoyed by multinational investments in local clinical trials. Traditional gauze and tape keep volume leadership in public tenders because of price sensitivity and broad clinician familiarity.

Growth momentum now tilts toward Wound Closure devices, forecast to grow 4.71% CAGR to 2031. Rising orthopedic procedures and trauma cases drive suture and staple usage, while tissue adhesives gain favor for minimally invasive surgeries. Innovations such as silver nanoparticle-infused adhesives are under pre-market review; early data show 37.65% MRSA biofilm inhibition . Electrical stimulation closure tools remain an emerging micro-niche but register pilot adoption in two leading Mexico City teaching hospitals.

By Wound Type: Chronic Wounds Lead Despite Acute Growth

Chronic Wounds hold a 60.98% slice of the Mexico wound care management devices market share thanks to diabetes and pressure-ulcer prevalence. Diabetic foot ulcer management commands the highest spend per episode, reinforced by a 54.5% peripheral neuropathy rate among diagnosed diabetics. Pressure ulcer incidence reaches 28.0% in second-level hospitals, supporting strong baseline demand for advanced foam dressings. Venous leg ulcer incidence rises concurrently with population aging and sedentary lifestyles, stimulating uptake of compression-compatible dressings.

Acute Wounds, while smaller, are on a faster growth curve, pacing at 4.58% CAGR through 2031. Orthopedic, cardiovascular, and bariatric surgeries contribute to higher volumes of clean surgical incisions. Burn management protocols adopt chitosan-metformin biomaterials that shorten healing times in diabetic cohorts. Trauma wound incidence along northern transport corridors also fuels demand for ready-to-deploy closure kits and antimicrobial sprays across emergency units.

By End User: Hospital Dominance Shifts Toward Home Care

Hospitals & Specialty Wound Clinics controlled 50.98% of the Mexico wound care management devices market size in 2025, propelled by IMSS-BIENESTAR centralized procurement and multidisciplinary diabetic-foot units. Large public hospitals favor bulk tenders that bundle basic gauze with selective advanced systems, while private centers differentiate with NPWT and smart bandage technology to compete for affluent patients.

Home-Healthcare Settings offer the fastest expansion trajectory at 4.79% CAGR. Smart dressings with Bluetooth-linked sensors facilitate remote monitoring, reducing readmissions and aligning with post-COVID patient preferences. Telehealth reimbursement policies now allow virtual wound assessments, encouraging early discharge strategies that shift product volumes toward domiciliary channels, further enlarging the Mexico wound care management devices market.

By Mode of Purchase: Institutional Dominance Amid Retail Growth

Institutional Procurement represents 67.35% of 2025 revenues owing to the New Consolidated Procurement Model that channels MXN 130 billion across 26 public entities. The model bundles 4,454 product codes over two years and rewards vendors who meet stringent COFEPRIS documentation and quality testing. Long approval queues incentivize suppliers with prior FDA or Health Canada clearances.

Retail/OTC sales, however, are scaling at a 4.68% CAGR on the back of pharmacy network expansion by chains such as FEMSA Salud. Patient education campaigns on diabetes self-care encourage over-the-counter acquisition of hydrocolloids and antimicrobial sprays. E-commerce penetration extends reach into rural localities, but counterfeit risks in informal markets underscore the need for serialized packaging and consumer training programs.

Geography Analysis

Mexico City, Guadalajara, and Monterrey collectively absorb the largest absolute spend on wound devices, reflecting their concentration of tertiary hospitals and clinical research facilities. These metros also host many early adopters of smart dressings and NPWT, giving suppliers a natural launchpad for new technologies. Federal reimbursement schedules reinforce uptake in these hubs while facilitating reference-site status for nationwide rollouts.

Northern border states—Chihuahua, Nuevo León, and Baja California—exhibit the fastest aging demographics and the densest clusters of foreign-owned device factories. Nearshoring incentives and the presence of 30+ medical-device plants employing 40,000 workers in the El Paso/Juárez borderplex reduce lead times and cushion tariff impacts, bolstering the regional share of the Mexico wound care management devices market. Cross-border patient flows further stimulate high-acuity wound care demand, while import-cost exposure accelerates local sourcing of semi-finished components.

Southern states such as Chiapas and Guerrero carry the highest diabetes prevalence at 10.2% and consequently grapple with severe chronic wound burdens. IMSS-BIENESTAR’s expanded mandate funnels capital into rural clinics, broadening basic wound care access through subsidized dressings and clinician training tours. Telemedicine is pivotal here, enabling remote guidance for complex ulcers via smart phone-compatible imaging systems.

The central plateau encompasses the majority of academic research on natural-compound dressings. Mexico City laboratories spearhead agave-based hydrogel trials, while Guadalajara’s biotech parks focus on chitosan-derivative films. These efforts cultivate a pipeline of cost-effective alternatives that address public-hospital budget constraints and are likely to diffuse nationally by 2028, reshaping competitive dynamics within the Mexico wound care management devices market.

Competitive Landscape

The Mexico wound care management devices market displays moderate consolidation: five multinationals command core advanced-therapy segments, yet domestic startups are unlocking white-space in bio-based dressings and home-care tech. ConvaTec produced 6.7% organic wound-care growth in H1 2024, signaling resilience amid tariff shifts. Smith & Nephew has earmarked USD 1.24 billion for wound investments, notably USD 660 million in skin substitutes that align with diabetic ulcer needs. Mölnlycke, now an AMID member, collaborates with AMCICHAC to promote responsible device usage and clinician education, enhancing its local brand equity.

Domestic innovators leverage Mexico’s biodiversity and cost sensitivities. University spin-offs are patenting agave bagasse hydrogels and silver-nanoparticle adhesives specifically tailored to public-hospital procurement thresholds, challenging import brands on price without sacrificing efficacy. Regulatory familiarity and faster COFEPRIS approvals for devices with prior OECD-nation clearances give seasoned multinationals a defensive edge, but nearshoring output at border plants increases local content thresholds, improving cost competitiveness for both foreign and Mexican firms.

Supply-chain diversification is now a core strategy. New tariffs and 10-18 month registration timelines motivate dual-sourcing models across the United States and the Juárez corridor, ensuring uninterrupted deliveries to institutional buyers. Vendors are also bundling training programs and tele-consultation platforms with devices to mitigate clinician-skill barriers, thereby enhancing stickiness across the Mexico wound care management devices market.

Mexico Wound Care Management Devices Industry Leaders

-

Smith & Nephew

-

Solventum

-

Convatec

-

Smith & Nephew

-

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mölnlycke joined AMID to advocate responsible device use and partnered with AMCICHAC on technology knowledge-sharing initiatives.

- February 2025: New Mexican tariffs of 4-8% on US medical device imports prompted logistics overhauls and compliance software investments across leading suppliers.

- November 2024: The New Consolidated Procurement Model for 2025-2026 earmarked MXN 130 billion to source 4,454 product codes for 26 public institutions, introducing a digital tender platform with elevated transparency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Mexico wound care management devices market as all medical devices placed on or into the wound bed, dressings, negative-pressure systems, closure consumables, oxygen and electrical stimulation platforms, sold for acute or chronic lesion management within hospitals, long-term facilities, and home-care settings.

Scope exclusion: Non-device topical creams, cosmetic scar patches, and veterinary products are outside this scope.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Interviews with procurement heads, wound-clinic nurses, biomedical engineers, and Latin American distributors helped us validate substitution trends, gauge average selling prices, and clarify channel mark-ups across Mexico's six largest metro areas. Follow-up surveys confirmed uptake assumptions for home-health-focused solutions.

Desk Research

Our team began with publicly available macro and clinical datasets from bodies such as Secretaría de Salud admission records, COFEPRIS import manifests, Instituto Nacional de Estadística y Geografía procedure volumes, and International Diabetes Federation prevalence tables, which frame demand fundamentals.

We deepened context with trade association white papers and peer-reviewed journals detailing device usage rates, then screened company filings through D&B Hoovers and news flow in Dow Jones Factiva for pricing shifts and competitive placements.

Additional pointers were taken from hospital procurement portals and tender notices.

The sources noted above illustrate, not limit, the evidence base consulted.

Market-Sizing & Forecasting

We applied a top-down model that starts with national procedure counts and diabetic foot prevalence, multiplies them by clinically accepted device utilization rates, and adjusts for import versus local manufacture before adding retail OTC flow.

Select bottom-up supplier roll-ups on NPWT pump installs and sampled ASP × unit checks served as reality anchors.

Key levers in the model include inpatient surgical volume growth, aging population share, NPWT installed base penetration, hospital bed occupancy, and peso-adjusted import value.

Five-year forecasts deploy multivariate regression blended with an ARIMA overlay, using consensus trend lines gathered during field work.

Gaps in micro-data were bridged by regional averages vetted through analyst peer review.

Data Validation & Update Cycle

Outputs pass three-level variance scans, outlier reviews, and senior analyst sign-off.

We refresh every twelve months and issue interim revisions when regulatory or recall events materially shift demand, ensuring clients always receive the most current baseline.

Why Mordor's Mexico Wound Care Management Baseline Earns Trust

Published estimates often diverge; definitions, device baskets, and refresh cadence explain much of the spread. According to Mordor analysts, clarity on what constitutes a regulated device versus a pharmaceutical aid is the first safeguard.

Typical gap drivers include varying inclusion of stand-alone topical creams, use of list versus blended transaction prices, differing assumptions on NPWT rental cycles, and the timing of exchange-rate conversions that competitors freeze far earlier than our annual refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 310.67 M (2025) | Mordor Intelligence | - |

| USD 355.8 M (2024) | Regional Consultancy A | Includes OTC antiseptic liquids and therapy devices not classified as medical devices in Mexico |

| USD 150 M (2024) | Global Consultancy B | Uses conservative price points and excludes institutional rental revenues |

| USD 1.7 B (2023) | Trade Journal C | Blends biologics and advanced pharmaceuticals into device totals and applies aggressive inflation factors |

The comparison shows that when scope, price realism, and annual updates align, as they do in Mordor's framework, decision makers gain a balanced, transparent baseline they can readily trace back to verifiable variables.

Key Questions Answered in the Report

What is the current size of the Mexico wound care management devices market?

The market is valued at USD 322.85 million in 2026 and is forecast to reach USD 391.41 million by 2031.

Which product category holds the highest Mexico wound care management devices market share?

Wound Care products hold the leading 67.31% share as of 2025.

Which segment is expanding fastest within the Mexico wound care management devices market?

Home-Healthcare Settings are projected to grow at a 4.79% CAGR, outpacing hospital demand.

How do tariffs impact the Mexico wound care management devices industry?

The 2025 tariff increase of 4-8% on US imports raises procurement costs and accelerates nearshoring of manufacturing.

Why are chronic wounds so significant for Mexico?

Diabetes prevalence of 14.7% drives diabetic foot ulcers and pressure ulcers, pushing chronic wounds to 60.98% of market demand.

What technological advances are influencing the Mexico wound care management devices market?

Smart bandages with machine-learning analytics, negative pressure systems, and agave-based bio-dressings are redefining clinical practice.

Page last updated on: