Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

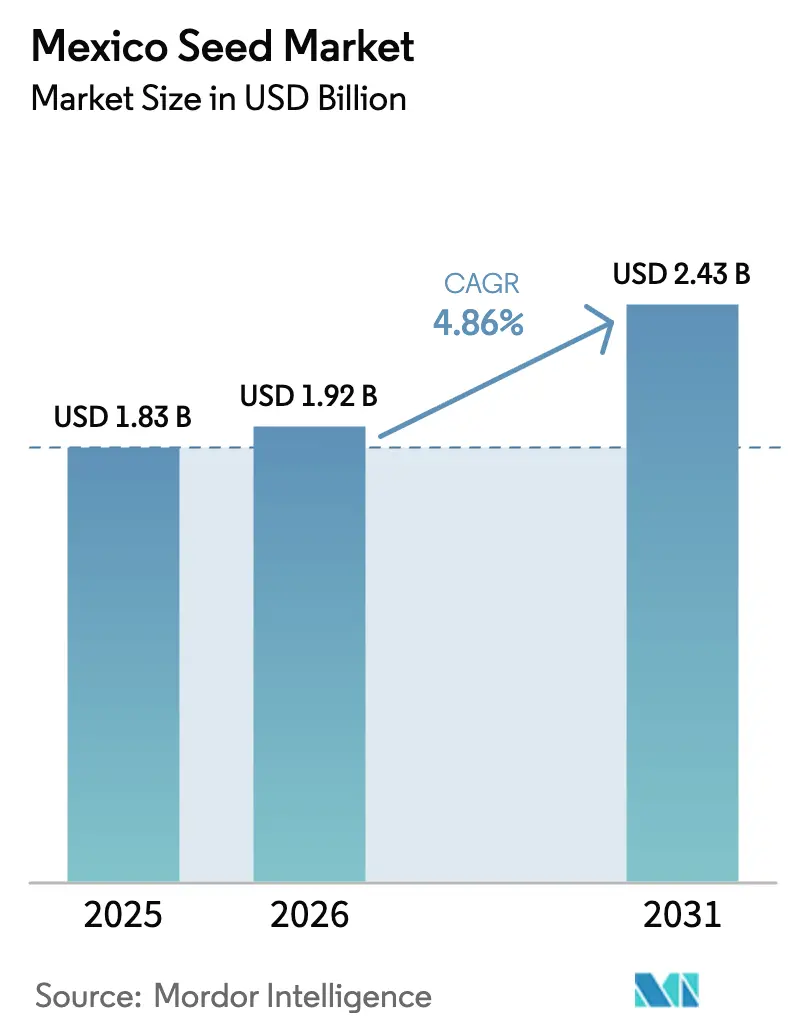

| Base Year Market Size (2025) | USD 1.83 Billion |

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Seed Market Analysis by Mordor Intelligence

The Mexico seed market size was valued at USD 1.83 billion in 2025 and estimated to grow from USD 1.92 billion in 2026 to reach USD 2.43 billion by 2031, at a CAGR of 4.86% during the forecast period (2026-2031). Strong public investment, rising adoption of drought-tolerant hybrids, and the country’s push for agricultural self-sufficiency continue to underpin demand. Regulatory uncertainty surrounding genetically modified corn is simultaneously spurring interest in non-GMO hybrids and accelerating breeding work on climate-resilient traits. Rapid greenhouse expansion in northern states is opening a premium niche for protected-cultivation seed lines, while booming chili exports keep vegetable breeders focused on yield, flavor, and longer shelf life. Together, these factors illustrate how grower economics, policy, and climate risk converge to shape the trajectory of the Mexico seed market.

Key Report Takeaways

- By breeding technology, hybrids led with a 76.20% Mexico seed market share in 2025 and are projected to compound at a 5.12% CAGR through 2031.

- By cultivation mechanism, open-field systems captured 97.10% of the Mexico seed market in 2025, whereas protected cultivation is forecast to expand at a 6.62% CAGR to 2031.

- By crop type, row crops accounted for 79.35% of the Mexico seed market size in 2025; vegetables hold the fastest-growth slot with a 5.44% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government pushes for domestic corn seed self-sufficiency | +1.2% | National, concentrated in Jalisco, Michoacán, and Guerrero | Medium term (2-4 years) |

| Growing adoption of drought-tolerant hybrids among irrigated farms | +0.8% | Northern states (Sinaloa, Sonora, and Chihuahua) | Short term (≤ 2 years) |

| Expansion of protected-cultivation acreage | +0.6% | Sinaloa, Sonora, and Baja California | Long term (≥ 4 years) |

| Rising export demand for Mexican hot-pepper hybrids | +0.5% | Sinaloa, Chihuahua, and Zacatecas | Medium term (2-4 years) |

| Wider e-commerce distribution of hobby-garden seed packs | +0.3% | Urban centers (Mexico City, Guadalajara, and Monterrey) | Short term (≤ 2 years) |

| Corporate venture capital funding in ag-biotech start-ups | +0.4% | National, with concentration in Nuevo León and Jalisco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for Domestic Corn Seed Self-Sufficiency

PROSEBIEN’s program, launched in April 2025, positions the state as both regulator and commercial player. The initiative prioritizes native open-pollinated maize and bean lines, aiming to shave 15–20% off corn imports by 2030. New traceability rules under SENASICA’s SICEFI platform provide local breeders an advantage because compliance costs remain lower for domestic operators. Private seed firms now seek licensing partnerships that keep them inside supply contracts while avoiding direct competition with subsidized public varieties. For growers, subsidized seed access could lift adoption rates of certified lots, provided distribution bottlenecks are resolved. Overall, the program accelerates demand for locally adapted, high-quality seed along with testing services that verify genetic purity.

Growing Adoption of Drought-Tolerant Hybrids

The 2023-2024 drought demolished domestic corn output, pushing irrigated growers toward premium hybrids promising water savings. Bayer’s VITALA package pairs short-stature corn with in-field digital tools that claim yield gains and water reduction. Adoption is most visible in Sinaloa and Sonora, where irrigation districts invest in modernizing canals. Early users report 15–20% higher margins even after paying a seed premium. As Mexico becomes the world’s largest corn importer with arrivals topping growers chasing yields per cubic meter of water, view drought-tolerant corn as insurance. Seed companies able to demonstrate verifiable water-efficiency metrics therefore hold a compelling value proposition.

Expansion of Protected-Cultivation Acreage

Greenhouse permits surged year over year in 2025, driven by export contracts demanding consistent quality and by state incentives covering up to 25% of construction costs[1]Source: World Agri-Tech. "World Agri‑Tech Mexico 2025." www.worldagritechmexico.com. Breeders must tailor genetics for tighter spacing, diffuse light, and strict phytosanitary regimes common under glass. KWS’s Navolato site now screens tomato and pepper lines under variable CO₂ and humidity to match northern Mexico’s desert climate. Seed purchases for protected systems carry a price premium over open-field equivalents, yet growers accept the markup given the higher pack-out rates. The protected wave could lift vegetable seed volume for greenhouses by 8% annually through 2030, though adoption hinges on reliable energy and water access.

Rising Export Demand for Mexican Hot-Pepper Hybrids

Mexico shipped a good amount of green chilies in 2024, anchoring its leadership in the global chili trade. Export buyers seek uniform pungency and longer shelf life, compelling breeders to stack disease resistance with precise Scoville ratings. A Chiapas program now releases hybrids after a decade-long pipeline that integrates pest resistance and flavor profiles specific to U.S. and European palates[2]Source: Jiménez, Gerardo. "En Chiapas, producen semillas híbridas resistentes a las plagas; se exportan a EU y Europa." www.prensa.com. Premium seed pricing rewards intellectual property protection, encouraging companies to deploy trait-tracking QR codes. Concentration of pepper farming in Sinaloa, Chihuahua, and Zacatecas speeds varietal turnover because local distributors can service large greenhouse clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain timeline for GMO corn import ban implementation | -0.9% | National, with the highest impact in border states | Medium term (2-4 years) |

| Chronic water-scarcity limiting summer sowing windows | -0.7% | Northern and Central Mexico (Sonora, Chihuahua, Guanajuato) | Long term (≥ 4 years) |

| Gray-market seed sales eroding branded players' share | -0.5% | National, concentrated in smallholder regions | Short term (≤ 2 years) |

| Limited cold-chain for high-value vegetable seed logistics | -0.3% | Rural distribution networks nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uncertain Timeline for GMO Corn Import Ban Implementation

A December 2024 T-MEC panel deemed Mexico’s GMO rules non-compliant, casting a cloud over biotech approvals. Multinationals weighing trait launches face the risk of retroactive bans that could strand inventory and R&D investments. Farmers delay seed purchases while awaiting policy direction, a drag on early-booking volumes that typically finance local production plots. Industry group AMSAC now lobbies for CRISPR-friendly statutes, yet resolution may stretch into the 2027 elections. Investment freeze in transgenic pipelines restricts technology renewal cycles and crimps potential yield gains.

Chronic Water Scarcity Limiting Summer Sowing Windows

Reservoir levels in northern basins fell below capacity for two consecutive seasons, forcing federal authorities to ration allocations. Summer maize and sorghum sowings slid in 2024 as growers postponed planting until rainfall recovered. Reduced area lowers total seed demand, especially for open-pollinated lines in subsistence systems. Without large-scale irrigation upgrades, cyclical droughts will keep volumes volatile and push insurers to tighten coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Sustain Premium Momentum

Hybrids captured 76.20% Mexico seed market share in 2025, and their dominance is set to continue with a 5.12% CAGR through 2031. The superiority of heterosis in corn and vegetables secures higher yields that justify premium pricing among commercial farms. Mexico’s regulatory preference for non-GMO traits channels R&D toward conventional hybrids, reinforcing the position of seed firms with strong back-cross programs.

Seed demand from smallholders remains elastic; open-pollinated varieties retain footholds where farmers save grain for replanting. PROSEBIEN’s subsidized distribution of native germplasm could slow hybrid share expansion in select zones, yet rising export expectations for uniform produce keep commercial growers aligned with hybrid purchases. The Mexico seed market consistently rewards lines delivering both drought tolerance and standability, attributes more effectively stacked in hybrid pedigrees.

By Cultivation Mechanism: Protected Systems Scale from Low Base

Open-field acreage commands 97.10% of national seed use, reflecting centuries-old rain-fed practices. Yet protected cultivation is the fastest mover, growing at 6.62% CAGR as greenhouse clusters spread across Sinaloa and Sonora. High tunnel and glasshouse operators demand seed tailored to controlled variables, prompting breeders to adjust leaf architecture and internode length for vertical production systems.

Up-front capital remains the barrier; the cost per hectare for modern glasshouses tops limiting entry to export-oriented producers. Nonetheless, climate volatility accelerates the shift because protected units ensure year-round harvests. As power and water tariffs stabilize under new state policies, protected growers project payback periods under five years, strengthening seed demand for specialized determinate lines.

By Crop Type: Vegetables Carve a Rapid-Growth Niche

Row crops maintained a 79.35% share of the Mexico seed market in 2025, owing to corn’s strategic role in food security and feed. Large-scale procurement under PROSEBIEN locks in baseline volumes for maize and beans, ensuring steady demand for certified seed. Sorghum and cotton segments grow modestly but face trait-approval constraints.

Vegetables register the quickest climb at 5.44% CAGR, driven by greenhouse peppers and tomatoes serving North American off-season demand. Export buyers pay premiums for uniformity and Brix levels, encouraging seed suppliers to invest in post-harvest quality traits. Biological seed coatings that extend seedling vigor enter trials at UPL’s Ramos Arizpe center, signaling rising R&D spend targeting the vegetable niche.

Geography Analysis

Northern Mexico, led by Sinaloa, Sonora, and Chihuahua, anchors the commercial heart of the Mexico seed market. Proximity to the United States border, robust irrigation grids, and export-ready logistics support concentrated greenhouse investment, translating into strong uptake of premium drought-tolerant hybrids. KWS’s Navolato breeding hub amplifies local R&D, while pepper growers in Sinaloa lean on controlled-environment lines that out-yield open-field peers.

Central states such as Jalisco, Michoacán, and Guanajuato form the traditional corn and bean belt. Government seed subsidies under PROSEBIEN target cooperatives here, intentionally bridging productivity gaps between subsistence and commercial farms. Precision-agriculture demonstrations, though less dense than in the north, encourage gradual movement toward certified hybrid seed. Intermittent water stress during summer months makes early-maturing maize hybrids attractive, nudging adoption upward each season.

Southern Mexico, including Chiapas, Oaxaca, and Veracruz, presents a mosaic of indigenous farming systems. Limited mechanization constrains hybrid penetration, yet select exporters in Chiapas run advanced pepper breeding plots funded by a 10-year project financing. Biodiversity in this region yields genetic resources valuable to national breeders seeking resilience traits. Logistics hurdles and price sensitivity keep gray-market seed prevalent, challenging branded players trying to expand distribution deeper into the isthmus.

Competitive Landscape

Mexico Seed Market concentration is high. Global majors BASF SE, Bayer AG, Syngenta Group, Land O’Lakes Inc., and Corteva Inc. retain scale advantages through national dealer networks and multi-crop portfolios. High market concentration invites rivalry from midsize Europeans such as KWS and South American innovators like Bioceres. KWS invested in a Navolato R&D station to tailor greenhouse tomatoes and peppers for local climates, shortening release cycles by two years. UPL’s Ramos Arizpe center prioritizes biological coatings projected to grow annually, reflecting a broader industry pivot toward sustainable inputs.

Regulatory volatility after the T-MEC ruling spurs strategic flexibility. Multinationals hedge by expanding non-GMO hybrid lines while lobbying for gene-editing acceptance. Domestic startups, buoyed by venture capital, explore microbial inoculants that reduce synthetic fertilizer loads, a complement to premium seed. Gray-market trade remains the wild card; AMSAC’s roll-out of holographic tags on certified sacks aims to curb counterfeit penetration.

Partnerships define competitive tactics. Corteva’s USD 25 million alliance with Pairwise grants access to Fulcrum CRISPR tools, positioning it ahead should gene-edited crops secure approval. Bioceres leverages its HB4 drought-tolerance trait, already cleared in Argentina and the U.S., to negotiate potential test plots pending Mexican regulatory clarity. Collectively, these moves underscore a landscape where adaptability, local R&D, and IP enforcement dictate share gains in the Mexico seed market.

Mexico Seed Industry Leaders

-

BASF SE

-

Bayer AG

-

Land O’Lakes Inc.

-

Syngenta Group

-

Corteva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mexico launched PROSEBIEN, a state-owned seed enterprise funded to pursue self-sufficiency goals targeting increased beans and rice production by 2030.

- March 2025: Chiapas breeders unveiled export-ready pepper and cucumber hybrids in Mexico, developed over 10 years, integrating solar-powered greenhouses that cut emissions annually.

Mexico Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Row Crops, Vegetables are covered as segments by Crop Type.

Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Crop Type

| Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | ||

| Forage Crops | Alfalfa | |

| Forage Corn | ||

| Forage Sorghum | ||

| Other Forage Crops | ||

| Grains and Cereals | Corn | |

| Rice | ||

| Sorghum | ||

| Wheat | ||

| Other Grains and Cereals | ||

| Oilseeds | Canola, Rapeseed and Mustard | |

| Soybean | ||

| Sunflower | ||

| Other Oilseeds | ||

| Pulses | ||

| Vegetables | Brassicas | Cabbage |

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Lettuce | ||

| Okra | ||

| Peas | ||

| Spinach | ||

| Other Unclassified Vegetables | ||

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| Crop Type | Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | |||

| Forage Crops | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

| Grains and Cereals | Corn | ||

| Rice | |||

| Sorghum | |||

| Wheat | |||

| Other Grains and Cereals | |||

| Oilseeds | Canola, Rapeseed and Mustard | ||

| Soybean | |||

| Sunflower | |||

| Other Oilseeds | |||

| Pulses | |||

| Vegetables | Brassicas | Cabbage | |

| Cauliflower and Broccoli | |||

| Other Brassicas | |||

| Cucurbits | Cucumber and Gherkin | ||

| Pumpkin and Squash | |||

| Other Cucurbits | |||

| Roots and Bulbs | Garlic | ||

| Onion | |||

| Potato | |||

| Other Roots and Bulbs | |||

| Solanaceae | Chilli | ||

| Eggplant | |||

| Tomato | |||

| Other Solanaceae | |||

| Unclassified Vegetables | Asparagus | ||

| Lettuce | |||

| Okra | |||

| Peas | |||

| Spinach | |||

| Other Unclassified Vegetables | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms