Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

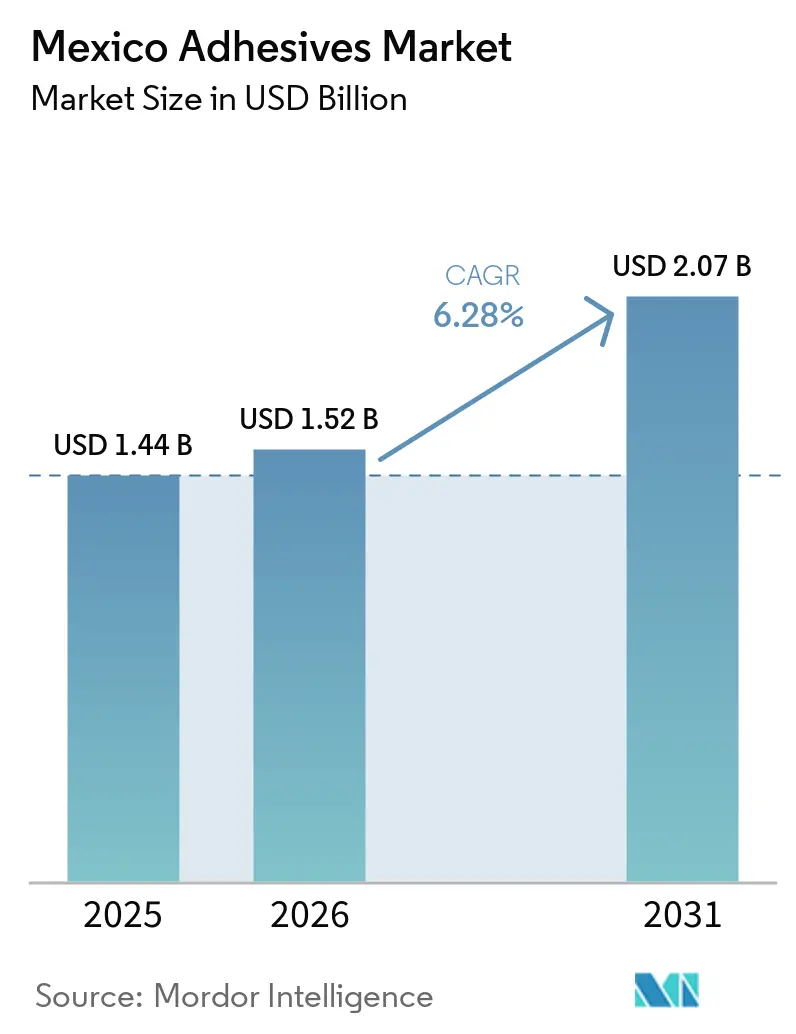

| Base Year Market Size (2025) | USD 1.44 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Adhesives Market Analysis by Mordor Intelligence

The Mexico Adhesives Market size is expected to increase from USD 1.44 billion in 2025 to USD 1.52 billion in 2026 and reach USD 2.07 billion by 2031, growing at a CAGR of 6.28% over 2026-2031. The nearshoring of electronics and electric-vehicle (EV) manufacturing is redefining demand for high-performance chemistries. Epoxies and polyurethanes, which are replacing traditional mechanical fasteners in lightweight platforms, are driving this trend. In the packaging sector, converters increasingly favor rapid-cure hot-melts, driven by the demands of e-commerce fulfillment. Meanwhile, stringent NOM-121-SEMARNAT regulations are encouraging investments in low-VOC water-borne systems. Multinational formulators are consolidating their technical centers near Guanajuato and Nuevo León, accelerating prototype iterations for OEM qualifications. However, the industry faces challenges, including corrugated-board down-gauging and fluctuations in methyl-methacrylate (MMA) prices, which are squeezing gross margins. As a result, suppliers must balance portfolio upgrades with cost optimization.

Key Report Takeaways

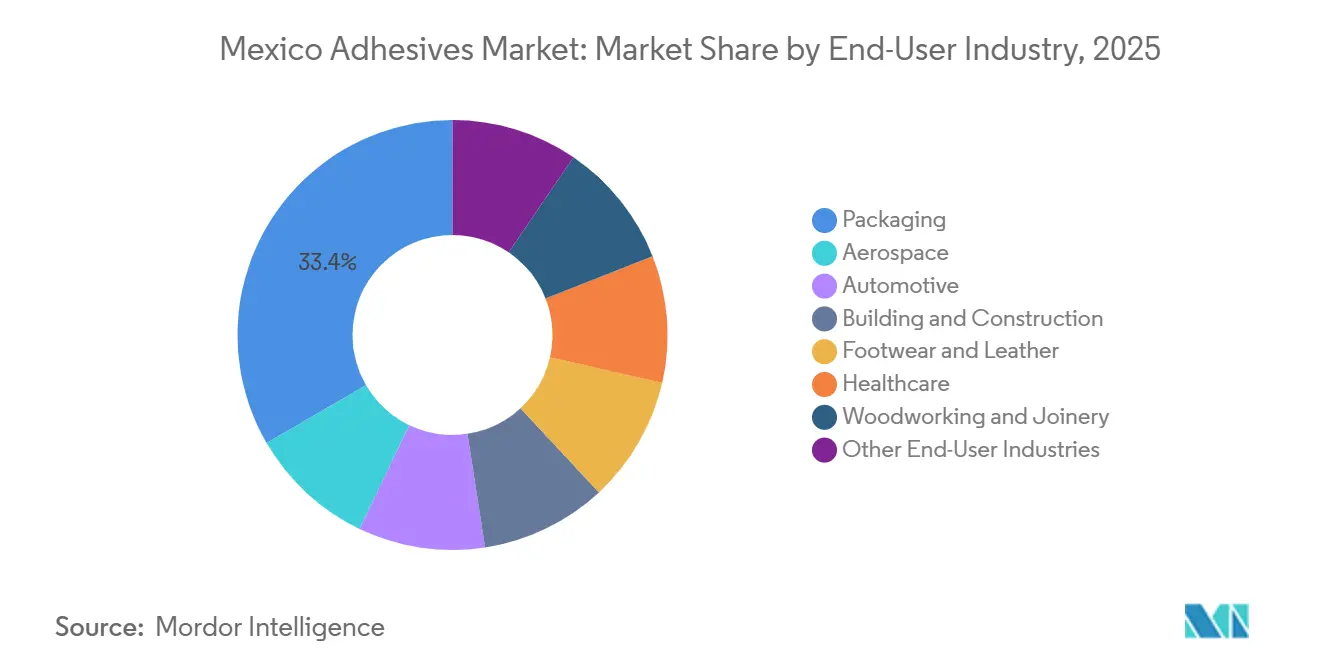

- By end-user industry, packaging led with 33.37% of the Mexico adhesives market share in 2025; automotive applications are advancing at a 6.90% CAGR in the forecast period of 2026-2031.

- By technology, water-borne systems accounted for 42.15% of the Mexico adhesives market size in 2025, while reactive chemistries are projected to expand at a 6.34% CAGR in the forecast period of 2026-2031.

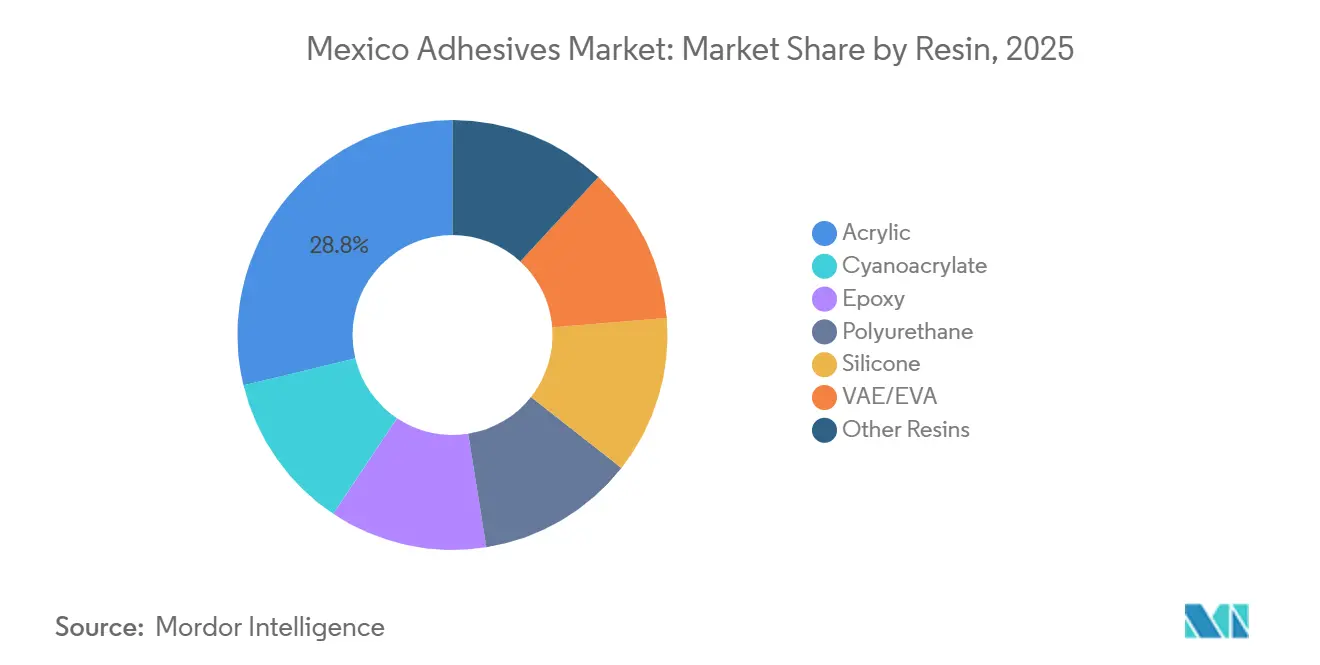

- By resin, acrylic formulations held 28.76% of the Mexico adhesives market share in 2025; epoxy solutions are advancing at the fastest trajectory at 6.42% CAGR in the forecast period of 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-driven lightweighting requirement | +1.8% | National, concentrated in Guanajuato, Nuevo León, San Luis Potosí automotive corridors | Medium term (2-4 years) |

| OEM near-shoring of electronics assembly | +1.4% | National, with early gains in Monterrey metropolitan area and Baja California tech clusters | Short term (≤ 2 years) |

| Surging flexible-packaging demand from e-commerce | +1.2% | National, urban fulfillment hubs in Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Growth of modular construction systems | +0.9% | National, accelerated adoption in northern border states and Yucatán Peninsula tourism projects | Medium term (2-4 years) |

| Packaging tax incentives for recyclability-enhancing adhesives | +0.6% | National, regulatory influence from SEMARNAT environmental standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Lightweighting Requirement

Battery-electric architectures are increasingly adopting structural epoxies and polyurethanes, leading to weight reductions compared to traditional welded steel. In response to the rising demand for thermal-interface and encapsulation adhesives, BMW has allocated a substantial portion of its San Luis Potosí expansion for battery-pack operations[1]BMW Group, “BMW Group Invests 800 Million Euros in San Luis Potosí Plant for NEUE KLASSE Production,” PRESS.BMWGROUP.COM. The push for lightweighting is further highlighted by the adoption of composite body panels and aluminum cargo boxes in commercial EV fleets. However, a notable gap exists: many tier-2 suppliers lack automated dispensing cells capable of micron-level bead control. This deficiency opens doors for potential integrators and service partnerships. As the industry progresses, so do the standards: OEMs are now demanding comprehensive data packages on fatigue, crash performance, and thermal cycling, moving beyond traditional lap-shear tests.

OEM Near-Shoring of Electronics Assembly

As electronics manufacturing shifts from Asia to Mexico, there is a growing demand for underfill epoxies, thermally conductive silicones, and UV-cured acrylics, all customized for the local humidity. General Motors has announced a significant investment, highlighting the increasing integration of electronics in vehicles. Monterrey's aerospace and medical-device talent pool provides the region with a distinct competitive advantage. Formulators establishing laboratories near these plants have reduced qualification cycles from 18 months to approximately 12 months, enabling them to secure design-in positions ahead of competitors in the tendering process.

Surging Flexible-Packaging Demand from E-Commerce

Fulfillment hubs require hot-melt and pressure-sensitive adhesives that bond at line speeds exceeding 60 cartons per minute and can withstand temperature fluctuations. In an effort to reduce energy consumption and prevent scorching of recycled paperboard, Mexican converters are experimenting with lower-temperature hot-melts, specifically those below 150 °C. The rise of direct-to-consumer shipping has increased the use of small-format pouches sealed with repositionable adhesives. This trend complicates inventory planning, particularly as brands frequently refresh designs to enhance consumer appeal. The proximity to U.S. distribution channels enables Mexico to serve as a packaging hub, but the high volatility of SKUs presents suppliers with the challenge of potential raw-material obsolescence.

Growth of Modular Construction Systems

Prefabricated modules now come equipped with insulation, vapor barriers, and structural skins, all bonded using either polyurethane or epoxy. In response to labor shortages, the tourism projects in the Yucatán Peninsula and the factories close to the border are increasingly adopting panelized systems. Adhesives are required to meet stringent fire and moisture criteria, often necessitating third-party certifications. Disparities in building codes across states can lead to delays in project approvals, potentially dampening short-term volumes. However, suppliers offering fire-rated formulations and on-site technical assistance are well-positioned to secure early-stage specifications as regulations gradually converge.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile methyl-methacrylate (MMA) prices | -0.8% | National, affecting reactive and acrylic adhesive producers | Short term (≤ 2 years) |

| Skilled-labor shortages in automated dispensing | -0.6% | National, acute in Guanajuato, Nuevo León automotive clusters | Medium term (2-4 years) |

| Down-gauging of corrugated board reducing adhesive lay-down | -0.5% | National, concentrated in packaging-intensive consumer goods sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Methyl-Methacrylate Prices

MMA plays a pivotal role in the raw material costs of acrylic and reactive systems. Tightened supply can lead to sharp spikes in spot prices, jeopardizing profit margins. Mexican formulators, typically too small to negotiate multi-year offtake agreements, are at the mercy of the quarterly price resets. Such price volatility not only stifles capacity expansions but also shifts research and development focus toward epoxy and polyurethane chemistries, which boast more stable feedstock prices.

Skilled-Labor Shortages in Automated Dispensing

Technicians skilled in programming, vision alignment, and statistical process control are in high demand for robotic bead applications. However, the lack of a robust training pipeline is causing delays in qualifying EV battery-pack lines, subsequently hindering revenue realization. While multinationals have begun placing application engineers directly at OEM sites, this approach proves resource-intensive, posing challenges for regional suppliers who depend on distributors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Packaging Anchors Share, Automotive Drives Value

In 2025, packaging accounted for 33.37% of Mexico's adhesives market revenue, underscoring the dominance of hot-melts in corrugated case sealing and the growing trend of pressure-sensitive labels. With box lines operating at speeds exceeding 60 units per minute, the need for quick-setting adhesives solidified hot-melt's leading position. Additionally, converters in flexible packaging broadened the demand for polyurethane laminating systems, especially those capable of handling retort processing.

Though automotive adhesives represented a smaller segment of Mexico's adhesives market, they were projected to expand at a 6.90% CAGR through 2031, driven by battery pack encapsulation and composite panel bonding. Structural epoxies and polyurethanes replaced traditional spot welds, enhancing both crash and fatigue performance. Furthermore, in response to occupant air quality mandates, interior trim laminations transitioned to low-VOC water-borne systems.

While the building and construction sector consumed significant amounts of tile-setting and flooring adhesives, its price sensitivity limited a shift toward premium chemistries. In Guanajuato, the footwear production industry sustained the demand for polyurethane solvents. Meanwhile, aerospace hubs in Querétaro required specialized high-temperature epoxies, which commanded a premium price.

By Technology: Water-Borne Leads Share, Reactive Gains Momentum

In 2025, water-borne adhesives captured 42.15% of Mexico's adhesive market, primarily driven by VAE and acrylic emulsions used in carton sealing and woodworking. While their low-VOC profile meets the standards of NOM-121-SEMARNAT, these adhesives do face challenges: heightened humidity can extend their curing time.

Reactive systems, encompassing epoxies, polyurethanes, and cyanoacrylates, were forecast to grow at a 6.34% CAGR. This growth was largely attributed to their application in EV battery packs and electronics assemblies, where chemical curing ensures superior structural integrity. Meanwhile, hot-melts, vital for high-speed packaging lines, are being reformulated. Responding to energy-reduction goals, formulators are now crafting grades that achieve bonding at temperatures between 120 and 140 °C.

Solvent-borne adhesives continue to dominate in footwear and trim applications, where their instant tack boosts production speed. However, with tightening VOC regulations, a shift is becoming evident. On the other hand, UV-cured products, though occupying niche markets like optical assemblies, offer the advantage of immediate fixture without the risk of thermal stress.

By Resin: Acrylics Dominate, Epoxy Surges in High-Performance Niches

In 2025, Mexico's adhesive demand saw acrylics claiming a 28.76% share, largely due to their adaptability in pressure-sensitive and water-borne applications. While polyurethanes provided flexibility for footwear and packaging, they faced challenges stemming from MDI/TDI price fluctuations. Epoxies, though accounting for a smaller share, experienced rapid growth at a 6.42% CAGR during the forecast period of 2026–2031, driven by their pivotal roles in EV structural bonding and wind-turbine blade assembly, both requiring high modulus and chemical resistance.

Silicones addressed high-temperature needs in automotive under-hood applications and solar module sealing. However, their slower curing rates limited broader adoption. VAE/EVA copolymers led the market in commodity carton sealing, valued for their cost-effectiveness. Nevertheless, this lack of differentiation intensified price competition. Cyanoacrylates played a vital role in electronics for quick fixes, but their inherent brittleness restricted their use to non-structural joints.

Geography Analysis

Northern industrial corridors exhibit the highest adhesive intensity. The Bajío region, which includes Guanajuato, Querétaro, and Aguascalientes, hosts electric vehicle (EV) and internal combustion assembly operations, supported by the expansion of BMW’s plant in San Luis Potosí. In this region, demand is primarily directed toward structural epoxies and polyurethanes, which are integrated into automated dispensing cells.

In Monterrey, the aerospace and medical device sectors are driving increased demand for thermally conductive silicones, underfill epoxies, and UV-cured systems. The city's proximity to research universities fosters a skilled labor pool, positioning Monterrey as a testing ground for innovative chemistries. Meanwhile, Baja California, Chihuahua, and Tamaulipas, leveraging their maquiladora status, consume hot-melts and pressure-sensitive adhesives, primarily for electronics and packaging destined for the United States.

Mexico City and its surrounding areas represent the largest hub for packaging and consumer goods. In this region, there is a strong preference for water-borne carton adhesives and construction sealants. Modular tourism projects along the Yucatán Peninsula are gradually incorporating polyurethane panel adhesives; however, the shares remain modest. In the southern states, where agriculture and services dominate, adhesive demand is limited, except for localized increases in footwear clusters.

Competitive Landscape

The Mexico adhesives market is moderately consolidated. Multinationals are investing heavily in application labs and robotic dispensing integrations, aiming to capture the specifications of EVs and electronics. In Q1 2025, Henkel's Mobility & Electronics unit recorded robust sales growth in Latin America. However, this growth softened in Q3, which demonstrates the cyclicality of OEM production[2]Henkel, “Financial Reports – Quarterly Results 2025,” HENKEL.COM . Meanwhile, regional suppliers are carving out their niches in commodities by cutting overhead costs and speeding up delivery times. While sustainability is paving the way for opportunities in bio-based polyurethanes and recyclable hot-melts, start-ups still face challenges such as scaling up and obtaining automotive-grade validation. Certifications like ISO 9001 and IATF 16949 act as gatekeepers, funneling the volume of structural adhesives to established players. In commodity segments like corrugated packaging, frequent dual sourcing limits pricing power. However, suppliers who collaborate on automated dispensing and sustainability initiatives are best positioned to achieve profit margin expansion.

Mexico Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

3M

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Henkel introduced Loctite MS 9650, a silane-modified polymer adhesive that bonds metals, plastics, and glass while offering improved UV resistance for automotive applications.

- November 2025: BioBond Adhesives, Inc. introduced a three-layer antimicrobial coating system in Mexico. This system is applicable to concrete, ceramic, wood, and metal surfaces and was designed for use in commercial, residential, industrial, and government facilities in partnership with Insumos Maez S.A. DE C.V.

Mexico Adhesives Market Report Scope

Adhesives are chemical substances that bond substrates by providing surface attachment and cohesion, ensuring high performance, lightweighting, and structural integrity in sectors such as aerospace, automotive, construction, and packaging.

The adhesives market is segmented by end-user industry, technology, and resin type. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. By technology, the market is segmented into hot-melt, reactive, solvent-borne, UV-cured, and water-borne. By resin type, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. For each segment, the market sizing and forecasts are done based on value (USD).

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-User Industries |

By Technology

| Hot-Melt |

| Reactive |

| Solvent-borne |

| UV-Cured |

| Water-borne |

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-User Industries | |

| By Technology | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| UV-Cured | |

| Water-borne | |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms