Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

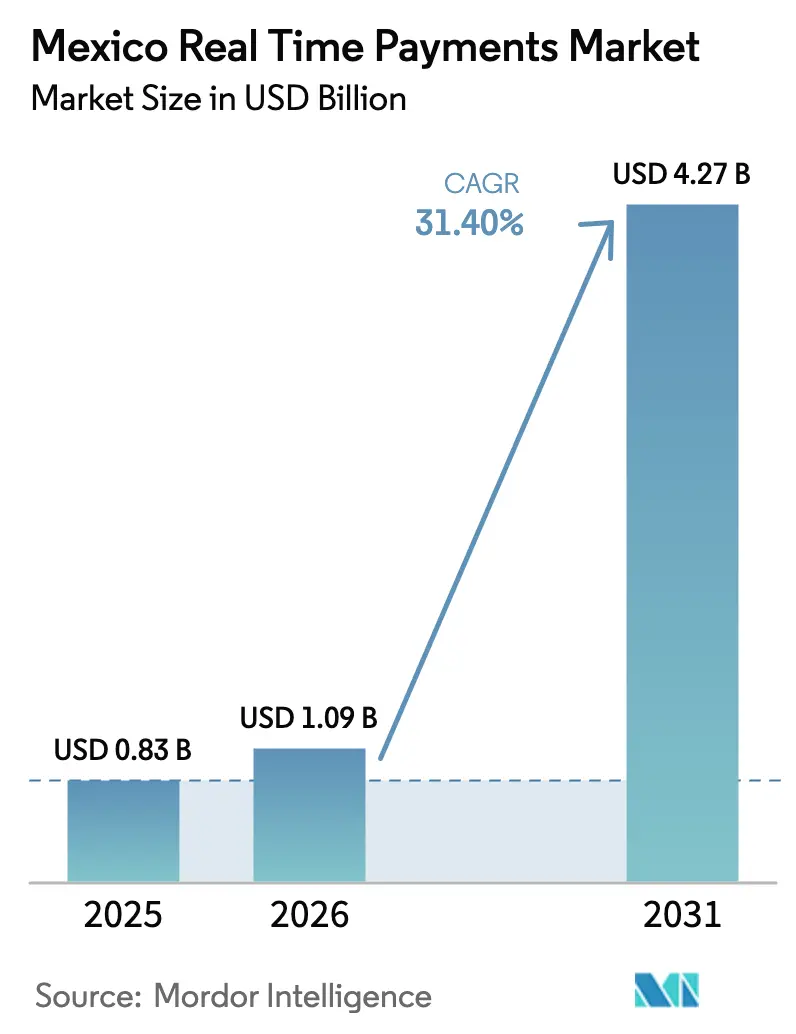

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 31.40% CAGR |

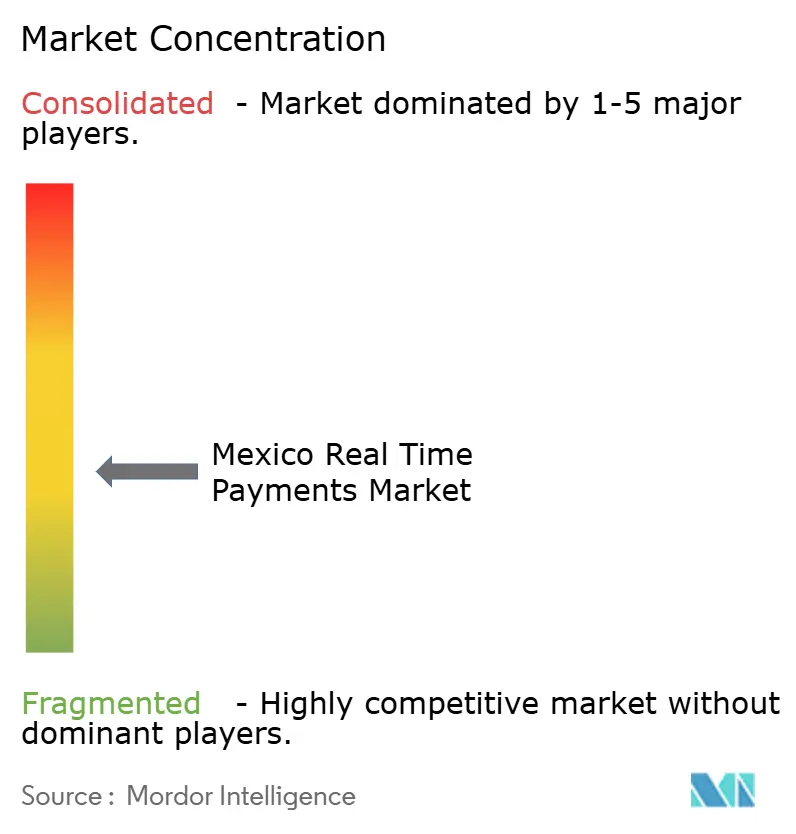

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Real Time Payments Market Analysis by Mordor Intelligence

The Mexico real-time payment market size is expected to grow from USD 0.83 billion in 2025 to USD 1.09 billion in 2026 and is forecast to reach USD 4.27 billion by 2031 at 31.4% CAGR over 2026-2031.[1]Banco de México, “Financial Stability Report – December 2024,” banxico.org.mx Rising smartphone penetration, government-backed financial-inclusion mandates, and continuous upgrades to the SPEI–CoDi rails are redefining how consumers and businesses settle transactions in seconds rather than days. As overlay services such as DiMo expand QR-code reach, peer-to-business adoption accelerates, and cloud migration lowers entry barriers for small firms, competitive dynamics are tilting toward agile fintechs that can plug specialized use cases onto central infrastructure. Meanwhile, the nearshoring wave is amplifying cross-border needs, prompting both banks and payment tech suppliers to prioritise interoperability, 24/7 uptime, and richer data standards under ISO 20022. Large enterprises continue to anchor volumes, yet the faster uptake among SMEs signals a widening addressable base and growing monetisation opportunities across value-added services.

Key Report Takeaways

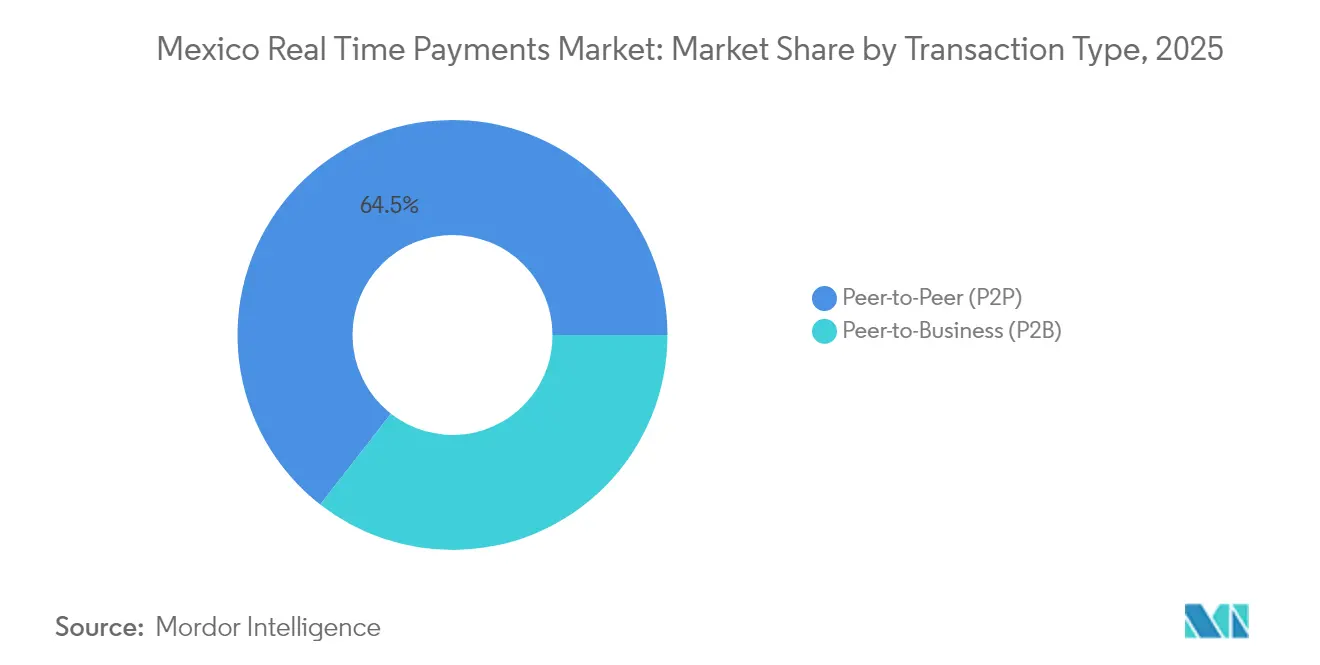

- By transaction type, Peer-to-Peer transfers led with 64.45% of the Mexico real-time payment market share in 2025, while Peer-to-Business flows are projected to expand at a 34.1% CAGR through 2031.

- By component, solutions platforms commanded 72.90% share of the Mexico real-time payment market size in 2025; the services segment is expected to grow the fastest at 28.3% CAGR over 2026-2031.

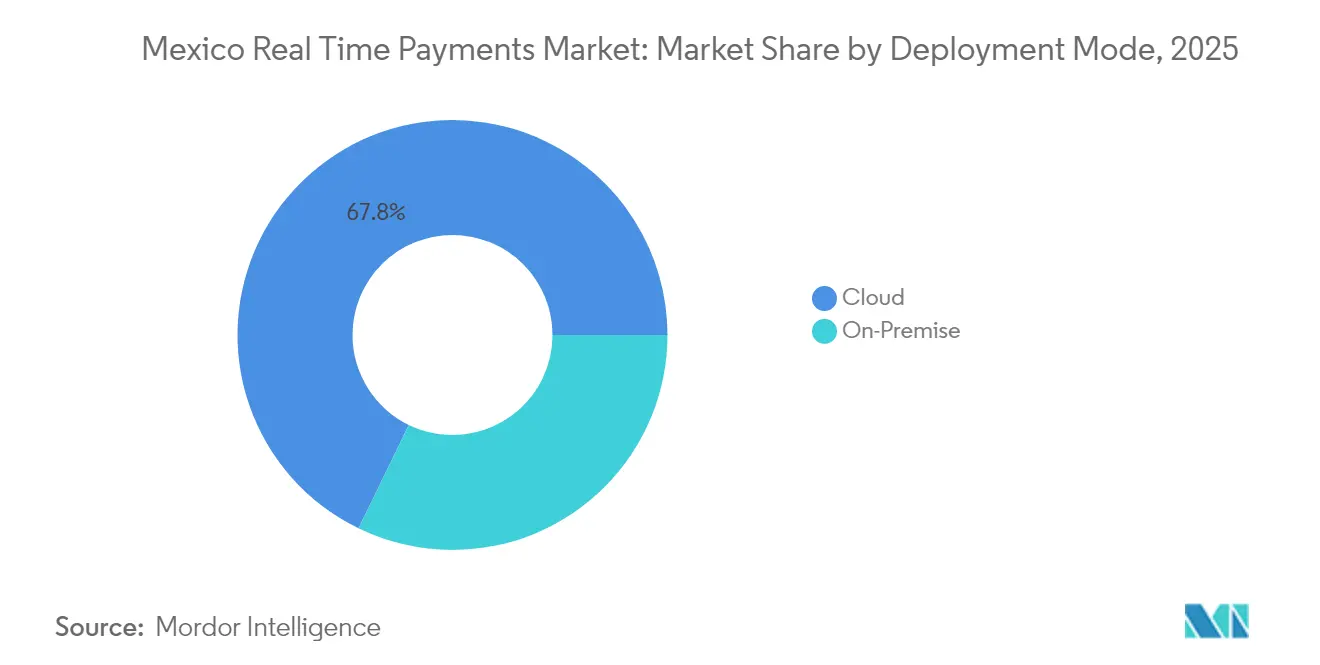

- By deployment mode, cloud captured 67.80% of the Mexico real-time payment market share in 2025 and is poised to rise at a 33.2% CAGR during the forecast period.

- By enterprise size, large enterprises held 63.70% of the Mexico real-time payment market share in 2025, whereas SMEs are forecast to record a 31.9% CAGR to 2031.

- By end-user industry, retail & e-commerce accounted for a 37.90% share of the Mexico real-time payment market size in 2025, while BFSI is advancing at a 30.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mexico's SPEI-CoDi Mandate Unlocking Instant Low-Value Transfers | + 7.2% | National, with concentration in urban centers | Medium term (2-4 years) |

| Surging FinTech Lending Apps Driving In-App RTP Adoption | + 8.5% | National, with higher impact in major cities | Short term (≤ 2 years) |

| QR-Code Interoperability Standards (CoDi, DiMo) Accelerating Merchant On-Boarding | + 6.3% | National, with early gains in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Retailers' Cash-to-Digital Conversion Campaigns in Northern States | + 5.1% | Northern states, with spillover to central regions | Medium term (2-4 years) |

| Rising Remittance-to-Wallet Programs Targeting US–MX Corridor | + 9.4% | Border states and high-migration regions | Short term (≤ 2 years) |

| Increasing Payroll-on-Demand Use-Cases Among Maquiladoras | + 4.8% | Manufacturing hubs in northern and central Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mexico's SPEI-CoDi mandate unlocking instant low-value transfers

Regulatory compulsion around CoDi usage has normalised QR-based micro-payments for day-to-day spending, cutting fees that previously deterred digital adoption and adding 18.4 million validated CoDi accounts by 2024. Continuous cryptographic upgrades by Banco de México have strengthened system resilience, safeguarding consumer trust and encouraging merchants to embed instant pay buttons within checkout flows. These measures are widening the Mexico real-time payment market reach into mass-transit, public-utility, and neighbourhood retail contexts that were historically cash dependent.

Surging fintech lending apps driving in-app RTP adoption

With more than 773 domestic and 217 foreign fintechs active in 2025, digital lenders such as Konfío and Clara use real-time rails to disburse approved funds and collect repayments in minutes, turning every borrower into a frequent instant-payments user. The frictionless loop between credit decisioning and settlement reduces default risk, shrinks cost-of-funds, and creates a spill-over effect: borrowers begin to demand the same immediacy for payroll, supplier, and personal transfers, accelerating overall network volumes.

QR-code interoperability standards accelerating merchant on-boarding

Unified QR protocols under CoDi and DiMo remove format fragmentation, trimming POS integration costs for micro-merchants by up to half and enabling single-scanner acceptance across banks and wallets. This simplicity is particularly valuable for the informal sector, which contributes roughly 22% of GDP and now gains a straightforward path to formal digital commerce. As more small stores switch stickers from static cash-only to dynamic QR, the Mexico real-time payment market gains breadth and transaction density.

Retailers' cash-to-digital conversion campaigns in northern states

Large chains such as Walmart and Soriana incentivise app-based checkouts with targeted discounts, loyalty points, and on-site staff training. Northern border locations act as proving grounds where consumer adoption is tracking 15% above the national mean, then cascades southward as store networks replicate playbooks. Retailers simultaneously lower cash-handling costs and gather SKU-level data, proving the commercial upside of aligning promotions with instant settlements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Trust in Digital Authentication Outside Tier-1 Cities | -4.2% | Secondary cities and rural areas | Medium term (2-4 years) |

| Fragmented Acquirer Connectivity for Small-Ticket Merchants | -3.8% | National, with higher impact in smaller cities | Short term (≤ 2 years) |

| High MDR Perception vs. Cash Among Informal Vendors | -5.1% | National, particularly in markets and informal retail | Medium term (2-4 years) |

| Legacy Core-Bank Batch Systems Limiting 24/7 RTP Capability | -3.5% | National, affecting all regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low trust in digital authentication outside tier-1 cities

Security scepticism persists, with only 17.6% of smartphone owners in smaller towns using mobile banking due to fraud fears. Mobile operators have introduced SIM-swap detection via the GSMA Open Gateway initiative to reassure users.[2]GSMA, “Mexico’s Mobile Industry Joins Forces to Simplify the Development of Applications Through GSMA Open Gateway,” newswire.ca Yet sustained grassroots education and demonstration of transaction-level protections remain essential to close the adoption gap and unlock incremental volumes in the Mexico real-time payment industry.

Fragmented acquirer connectivity for small-ticket merchants

Micro-retailers juggling multiple processors face costly, complex integrations that erode the economics of accepting instant payments. Payment-orchestration platforms such as Payabli promise unified APIs, but market penetration is limited. Unless streamlined onboarding becomes ubiquitous, a large portion of corner stores and street vendors will remain cash-centric, limiting Mexico real-time payment market depth despite consumer willingness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2P remains dominant while P2B accelerates

Peer-to-Peer transfers accounted for 64.45% of 2025 volume, capturing the early-mover advantage as friends and families embraced mobile banking apps for quick repayments. This segment’s entrenched behaviour sustains resilient baseline traffic that underpins liquidity across the Mexico real-time payment market. Merchants are now leveraging the same QR rails to accept account-to-account payments at checkout, a shift that is narrowing the historical divide between personal and commercial use cases.

The P2B segment, although smaller today, is forecast to grow at 34.1% CAGR. As QR scanners become standard at physical tills and e-commerce checkouts display CoDi prompts, merchants enjoy zero interchange, instant settlement, and lower fraud risk. Integration through SPEI alias functionality further disintermediates card schemes, positioning P2B to command a larger slice of the Mexico real-time payment market size for day-to-day retail interactions.

By Component: Platforms dominate, services gather momentum

Solutions platforms represented 72.90% of market revenue in 2025, reflecting heavy investment by banks and processors in ISO 20022-compliant routing, alias lookup, and request-to-pay modules. These core capabilities are non-negotiable foundations that enable overlay services and analytics. An expanding vendor ecosystem led by ACI Worldwide and Mexipay supplies turnkey hubs that custodians can deploy rapidly.

Professional and managed services are now entering a high-growth phase, advancing at a 28.3% CAGR as institutions seek external expertise for system integration, cloud migration, and fraud-detection upgrades. Cybersecurity audits, data-analytics consulting, and compliance validation are in growing demand, especially among mid-tier banks and fintechs that lack deep in-house engineering resources. These support layers unlock further utilisation, widening overall participation in the Mexico real-time payment market.

By Deployment Mode: Cloud leads and continues to accelerate

Cloud-hosted platforms captured 67.80% of deployment share in 2025, underlining the preference for elastic scalability and reduced capex. Providers such as MongoDB Atlas have expanded local availability zones so financial data remains in-country, satisfying regulatory data-sovereignty requirements. Elastic compute lets operators accommodate peak events such as payroll runs without over-provisioning hardware.

On-premise estates still handle high-sensitivity workloads at top-tier banks, yet even these incumbents are piloting hybrid configurations to tap containerised microservices and real-time analytics. As latency-sensitive applications—like fraud scoring and dynamic limit management—move cloud-native, the Mexico real-time payment market is expected to converge on predominantly cloud or hybrid deployments that exploit continuous integration pipelines for rapid feature rollouts.

By Enterprise Size: Large enterprises lead, SMEs close the gap

Large corporates retained a 63.70% share in 2025, harnessing economies of scale to integrate real-time disbursements into payroll, supplier settlements, and consumer payouts. Banks including BBVA México have launched instant bulk-payment suites that compress processing windows from hours to seconds, delivering working-capital visibility to treasurers.

SMEs are the fastest-growing cohort at 31.9% CAGR thanks to zero-fee CoDi acceptance, low-touch cloud onboarding, and orchestration tools that abstract technical complexity. As these businesses move beyond cash box reconciliations to real-time cash-flow dashboards, they unlock new credit-scoring data, reinforcing a virtuous cycle that expands adoption and enriches the Mexico real-time payment market.

By End-User Industry: Retail leads while BFSI accelerates

Retail & e-commerce held a 37.90% share in 2025, driven by online shopping above USD 53 billion that demands frictionless checkout and reduced cart abandonment. Chain retailers blend instant payments with loyalty redemption at POS, creating omnichannel consistency that boosts conversion. Fulfillment efficiency strengthens as stock-replenishment orders trigger automatically upon payment confirmation.

The BFSI segment is projected to post the fastest 30.4% CAGR. Banks use instant rails to settle investment redemptions, insurance claims, and micro-loan disbursements, strengthening customer stickiness through immediacy. Fintech entrants push incumbents to modernise back ends, while insurers pilot straight-through processing for small claims, collectively deepening the functional breadth of the Mexico real-time payment market.

Geography Analysis

Mexico City, Guadalajara, and Monterrey together account for roughly 65% of transaction volume, benefiting from dense financial infrastructure, higher smartphone adoption, and bank headquarters that pioneer digital initiatives. Corporate payroll batches, e-commerce fulfilment hubs, and metro transit systems create fertile test beds for new overlay features, which then radiate outward through national networks.

Northern border states experience disproportionate growth as nearshoring brings factories and logistics operators that demand 24/7 cross-border clearing. Remittance-to-wallet schemes along the US corridor funnel USD 64.7 billion annually into digital accounts, acting as an on-ramp for families who later use the same wallets for domestic spending. Cloud regions in Monterrey and Querétaro minimise latency for industrial ERP integrations, further catalysing uptake among suppliers.

Southern and rural regions lag on penetration yet represent untapped upside. Infrastructure upgrades, government social-benefit digitisation, and operator-led security APIs are gradually eroding reliance on cash. As financial literacy programmes scale and smartphone coverage nears parity, these areas could record above-average growth, helping broaden the Mexico real-time payment market footprint beyond metro economies.

Competitive Landscape

Mexico’s instant-payments arena is moderately concentrated, anchored by universal banks—BBVA México, Citibanamex, Banco Santander México, and Banco Azteca—that leverage established client bases and sizable IT budgets to roll out feature-rich mobile apps. Global processors such as ACI Worldwide, Fiserv, and Mastercard supply ISO 20022-compliant switching, alias resolution, and risk-scoring engines that underpin daily operations.

Competitive intensity has risen as more than 773 local fintechs and 217 foreign entrants chase niche opportunities, from gig-worker payouts to embedded finance for online marketplaces. To scale quickly, incumbents and newcomers alike harness partnerships: Visa acquired a majority stake in Prosa, which handles 10 billion annual transactions, to embed tokenised security and broaden cloud capabilities. ACI Worldwide teamed with Mexipay to embed request-to-pay and alias modules, reinforcing coverage for micro-merchants.

White-space remains across cross-border RTP, SME working-capital platforms, and data-driven loyalty engines. Disruptors such as Albo collaborate with Paymentology to bundle payroll, expense cards, and credit scoring targeted at underserved businesses. The strategic landscape therefore rewards modular technology stacks, collaborative go-to-market models, and proactive compliance readiness, all of which amplify differentiation in the Mexico real-time payment market.

Mexico Real Time Payments Industry Leaders

ACI Worldwide, Inc

Mastercard, Inc

PayPal Holdings, Inc

Visa Inc

Fiserve

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Banco de México upgraded SPEI cryptography and messaging formats to strengthen cybersecurity, a move that safeguards rising volumes and reinforces systemic confidence needed for further scale. Strategic rationale: ensuring resilience reduces downtime risk, encouraging merchants to rely on instant settlement for mission-critical flows.

- May 2025: Altán Redes, América Móvil, AT&T Mexico, and Telefónica Mexico opened network APIs under the GSMA Open Gateway, enabling fraud-mitigation functions such as SIM-swap detection that enhance payment security. Strategy: lowering authentication friction in rural regions broadens addressable user segments.

- March 2025: MongoDB launched local Atlas clusters on AWS, Google Cloud, and Microsoft Azure to support in-country data residency for regulated financial workloads. Strategy: removing latency and compliance barriers accelerates migration of core payment workloads to cloud.

- February 2025: Wise entered Mexico’s USD 60 billion remittance corridor, linking US senders to pesos wallets through instant settlement. Strategy: competing on speed and transparency, Wise positions itself as a cross-border layer atop domestic real-time rails.

Mexico Real Time Payments Market Report Scope

Real-time payments or RTP are payments that are begun and settled nearly immediately. It is the digital infrastructure that facilitates real-time payments. Ideally, real-time payment networks provide 24x7x365 access, which means they are always online to process transfers at any given day or time.

The Mexico Real Time Payments Market is segmented By Type of payment (P2P and P2B).

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-user Industries |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-user Industries |

Key Questions Answered in the Report

What is driving the rapid growth of the Mexico real-time payment market?

Smartphone ubiquity, regulatory mandates such as CoDi, and cloud-based infrastructure that lowers onboarding costs are propelling a projected 31.40% CAGR to 2031.

How large will the Mexico real-time payment market size be by 2031?

Industry estimates place the value at USD 4.27 billion, up from USD 0.83 billion in 2025.

Which segment is expanding fastest within the Mexico real-time payment market?

Peer-to-Business transactions are growing at a 34.1% CAGR, fuelled by QR acceptance at retail and e-commerce checkouts.

Why are cloud deployments preferred for real-time payment systems in Mexico?

Cloud offers elastic scaling, faster rollout, and compliant in-country data hosting, securing 67.80% deployment share in 2025 and a 33.2% CAGR.

How are SMEs benefiting from real-time payments?

Reduced transaction fees, improved cash-flow visibility, and simple API integrations enable SMEs to grow adoption at a 31.9% CAGR through 2031.

What role do remittances play in the Mexico real-time payment industry?

Remittance-to-wallet programmes convert cross-border inflows worth USD 64.7 billion into instant pesos credits, onboarding new users and boosting domestic RTP volumes.

Page last updated on: