Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

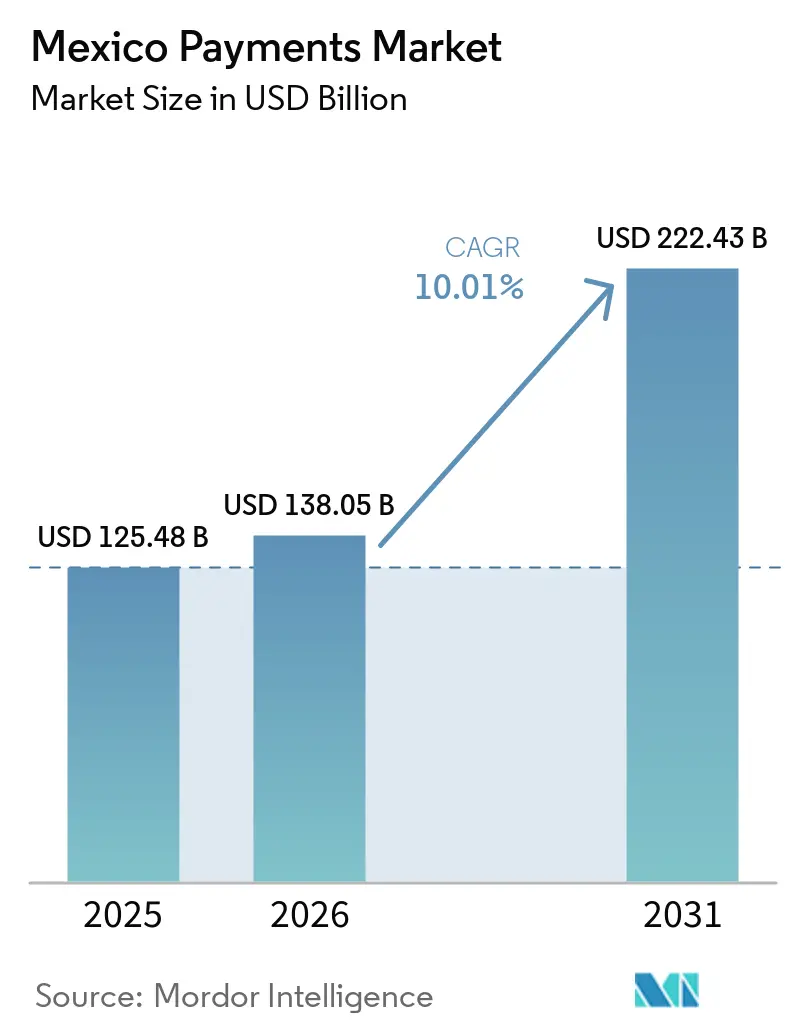

| Base Year Market Size (2025) | USD 125.48 Billion |

| Market Size (2026) | USD 138.05 Billion |

| Market Size (2031) | USD 222.43 Billion |

| Growth Rate (2026 - 2031) | 10.01% CAGR |

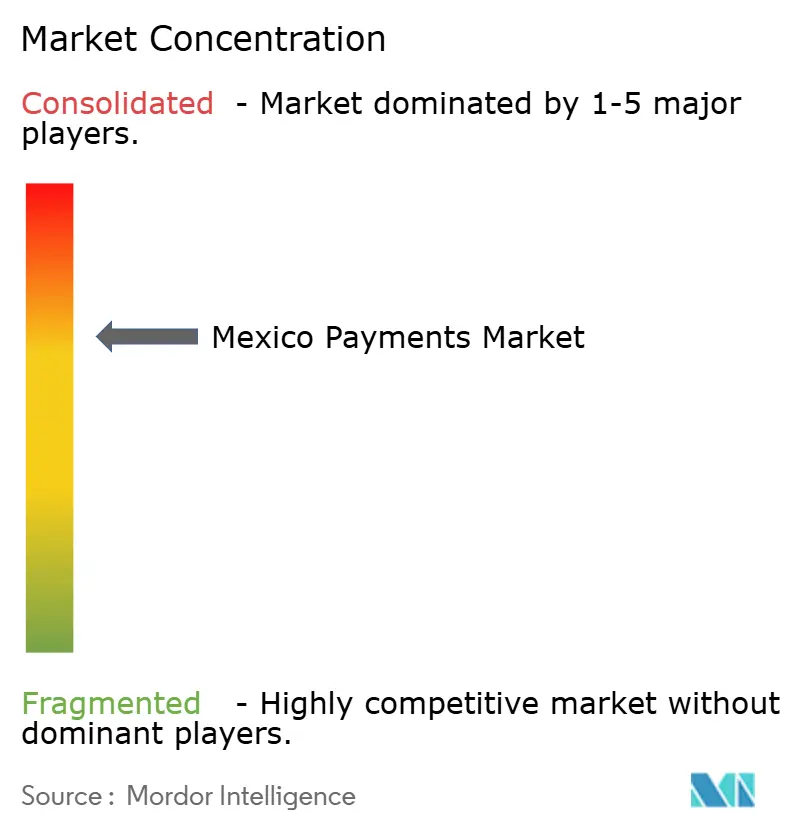

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Payments Market Analysis by Mordor Intelligence

The Mexico payments market size was valued at USD 125.48 billion in 2025 and estimated to grow from USD 138.05 billion in 2026 to reach USD 222.43 billion by 2031, at a CAGR of 10.01% during the forecast period (2026-2031). Expansion rests on regulatory modernization, real-time infrastructure, and a surge in cross-border flows that position the Mexico payments market as a pivotal hub for North American trade. Robust fintech licensing, increasing smartphone penetration, and embedded-finance integrations are widening consumer choice while encouraging merchant acceptance. Rapid e-commerce adoption is pushing the shift toward digital wallets, and government incentives aimed at the unbanked are accelerating formalization. At the same time, the Mexico payments market faces persistent cash preference among micro-merchants, mounting cyber-threats, and interoperability gaps that elevate both risk and opportunity. Heightened competition from nearly 1,000 fintech players keeps fees under pressure while spurring innovation around AI-driven fraud prevention and instant settlement rails.

Key Report Takeaways

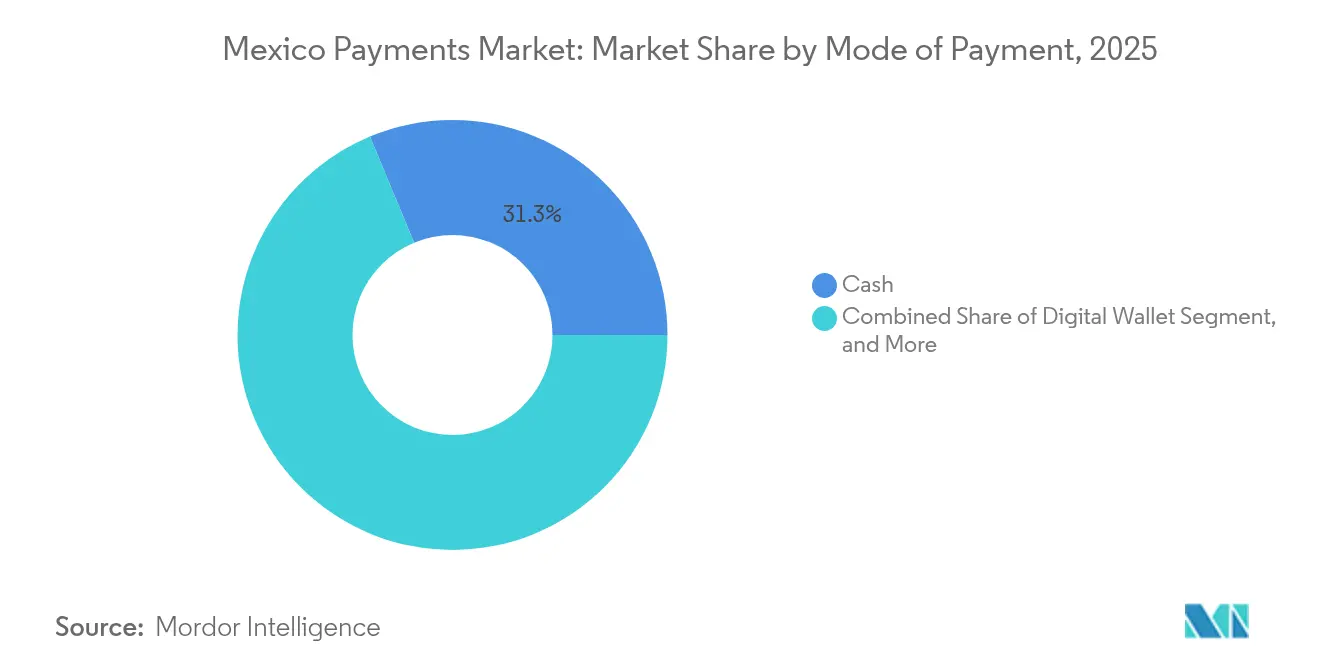

- By mode of payment, cash led with 31.27% of Mexico payments market share in 2025, whereas digital wallets are projected to post a 10.74% CAGR through 2031.

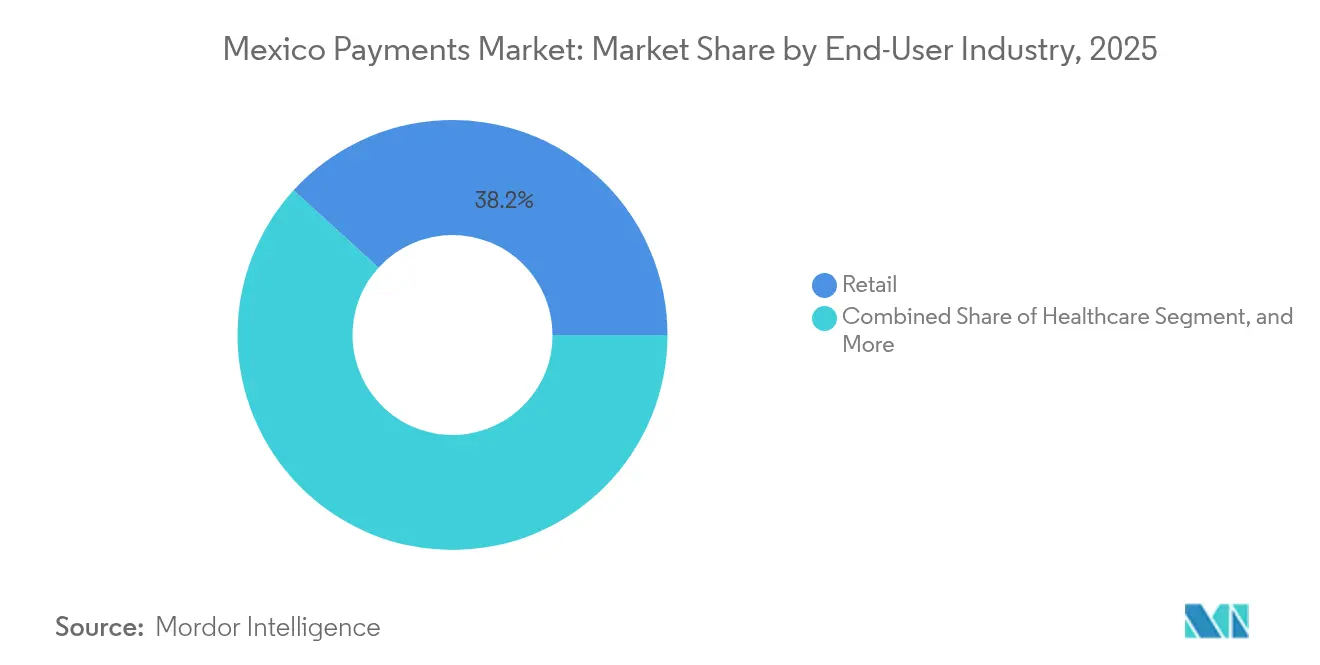

- By end-user industry, retail accounted for 38.24% of the Mexico payments market size in 2025, while healthcare is set to advance at an 11.08% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of CoDi (real-time A2A payments) | +1.8% | National, with early gains in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Expansion of smartphone and internet penetration | +2.1% | National, with spillover to rural areas | Long term (≥ 4 years) |

| Government push for financial inclusion and Fintech Law | +1.5% | National, focused on underbanked regions | Long term (≥ 4 years) |

| Rise of e-commerce and on-demand delivery | +2.3% | Urban centers with expansion to secondary cities | Short term (≤ 2 years) |

| Remittance-linked digital wallets spur formalization | +1.2% | Border states and high-migration regions | Medium term (2-4 years) |

| Retailer-led closed-loop wallets (e.g., OXXO Pay) | +0.9% | National, concentrated in retail-dense areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of CoDi (real-time A2A payments)

Bank of Mexico’s CoDi platform processed 3.894 billion transactions in 2023, underscoring its role as a low-cost backbone for the Mexico payments market. User enrollment climbed to roughly 60 million in 2024, yet peer-to-peer usage trails Brazil’s Pix because many institutions operate closed-loop environments that reduce interoperability.[1]Bank of America, “Digital Payments Growth and Transformation in Latin America,” business.bofa.com Small merchants gain immediate liquidity, but lack of universal QR compatibility still curbs broad uptake. Commercial suppliers increasingly demand instant settlement to optimize working capital, adding pressure on lagging banks. Regulatory adherence to ISO 20022 aligns CoDi for eventual cross-border integration, positioning the Mexico payments market for seamless North American trade.

Expansion of smartphone and internet penetration

Smartphone penetration surpassed 80% of adults in 2025, forming a technology bedrock for the Mexico payments market.[2]BBVA México, “Conoce los medios de pago digital más usados,” bbva.mx Digital payment values topped USD 100 billion in 2024, and mobile channels accounted for nearly 18% of all transactions. Rural gaps persist, prompting investment in 5G and fiber backbones that promise to lift digital wallet usage beyond urban enclaves. Mastercard research highlights that offline-capable solutions and agent networks are vital for remote uptake.[3]Mastercard Center for Inclusive Growth, “Lessons in Expanding Digital Payments to Remote Communities,” mastercardcenter.org Fintech players are therefore optimizing apps for low-bandwidth environments to broaden the Mexico payments market footprint across underserved regions.

Government push for financial inclusion and Fintech Law

Since 2020, CNBV has authorized 84 financial technology institutions, creating a vibrant, competitive field that enlarges the Mexico payments market. Over 56% of adults now own at least one financial product, but rural inclusion gaps remain. The 2018 Fintech Law offers clear licensing tiers, yet delays in open-banking rules slow data portability and limit multi-platform competition. Constitutional reforms in December 2024 eliminated oversight bodies INAI and IFT, injecting uncertainty into data-governance enforcement. Still, mandatory local data storage nurtures domestic cloud-services growth, reinforcing resilience within the Mexico payments market.

Rise of e-commerce and on-demand delivery

Mexican e-commerce exceeded USD 50 billion in 2024, and embedded finance accounted for 70% of online checkout flows. BNPL usage jumped 78% year over year, reaching 10 million users, and could secure an 18–22% share of online payments by 2027. On-demand delivery platforms require instant confirmation, driving real-time settlements and enriching the Mexico payments market. Merchant challenges include reconciling multiple tender types and mitigating fraud, spurring adoption of unified payment gateways. The convergence of logistics, data analytics, and flexible credit unlocks fresh monetization channels for platform operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and fraud concerns | -1.4% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| High cash preference among micro-merchants | -1.8% | National, concentrated in rural and informal sectors | Long term (≥ 4 years) |

| Limited interoperability across fintech rails | -1.1% | National, affecting cross-platform transactions | Medium term (2-4 years) |

| Rural connectivity gaps slowing QR adoption | -0.7% | Rural areas and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and fraud concerns

Mexico recorded 31 million cyberattacks in 2024, a 78% jump that threatens trust in the Mexico payments market. Mobile fraud rose to 61% of all incidents as real-time rails gained popularity. Banks responded with dynamic CVV codes that refresh every five minutes and mandated 3-D Secure on card-not-present transactions, boosting security but increasing user friction. Regulatory requirements for on-shore data storage enlarge compliance costs for smaller fintechs. Investment in AI fraud-detection engines and digital-ID networks is escalating to safeguard transaction growth and bolster confidence in the Mexico payments market

High cash preference among micro-merchants

Cash remains the primary tender for 80% of the population, and 85% of purchases under USD 50 still settle in cash, constraining digital acceleration within the Mexico payments market. Micro-merchants cite fee sensitivity, equipment costs, and limited digital literacy as main hurdles. The informal economy’s scale exacerbates apprehension toward transparent electronic records. Yet targeted onboarding efforts show promise; merchant-service providers that subsidize hardware and offer flat-fee structures are gradually widening acceptance. Long-term conversion will require bundled education, simplified KYC, and demonstrable revenue uplift for small businesses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Sustain Momentum

Cash retained 31.27% of Mexico payments market share in 2025, but digital wallets are forecast to grow at 10.74% CAGR, underlining a behavioral shift away from physical tender. The Mexico payments market size for digital wallets is projected to capture a rising share of transaction value as alliances such as Nu and OXXO add 22,000 cash-withdrawal points that create hybrid experiences. Credit and debit card volumes remain substantial, yet account-to-account rails like CoDi promise fee relief for merchants. Real-time settlement lowers working-capital constraints, providing a competitive edge versus card schemes. However, fragmented QR code standards hamper universal acceptance, slowing the path toward a cash-light economy.

Physical point-of-sale innovation is expanding acceptance lanes across 800,000 small businesses through low-cost readers and contactless NFC. Cash-on-delivery persists in e-commerce segments serving unbanked shoppers, illustrating the multichannel nature of the Mexico payments market. Regulatory oversight by CNBV maintains security benchmarks while opening licensing to niche providers that target specific merchant cohorts. As new entrants deploy AI risk engines at scale, the Mexico payments industry benefits from lower fraud exposure and richer data insights. The medium-term outlook hinges on resolving interoperability gaps that currently dilute the user experience.

By End-User Industry: Healthcare Accelerates Digital Adoption

Retail held 38.24% of Mexico payments market share in 2025, sustaining leadership by embedding payments across grocery, convenience, and department store chains. BNPL penetration within retail is anticipated to lift conversion rates and broaden average ticket sizes, further anchoring the segment in the Mexico payments market. Healthcare, meanwhile, is primed for the fastest 11.08% CAGR as telemedicine platforms integrate automated billing and micro-insurance, unlocking previously unmet demand. Integration of Health Savings Accounts with real-time rails streamlines reimbursements and reduces administrative overhead.

Entertainment and hospitality sectors leverage contactless and mobile payments to quicken service and minimize chargeback risk. Education and government services are rolling out e-wallet tuition and tax portals, reinforcing the Mexico payments market size in non-retail verticals. Cross-industry platform solutions let merchants tap multiple tenders through single APIs, cutting technical complexity. As data analytics matures, sector-specific loyalty programs drive higher engagement and incremental spend. Healthcare’s trajectory exemplifies how specialized workflows and regulatory clarity can unlock latent digital payment volumes across the Mexico payments industry.

Geography Analysis

Major metropolitan zones, Mexico City, Guadalajara, and Monterrey, contribute the bulk of digital transactions thanks to dense merchant networks and superior connectivity. These urban centers anchor the Mexico payments market size and set adoption benchmarks that ripple into secondary cities. Cross-border trade with the United States generated USD 573 billion in annual flows, intensifying demand for low-cost FX conversion and instant settlement. Nearshoring momentum is drawing over 400 manufacturers that require multicurrency payroll and supplier-payment tools, expanding corporate wallet volumes.

Border states capture a significant slice of remittance-linked activity; USD 64.745 billion in remittances arrived in 2024, and 64% of recipients used digital channels to receive funds. High fees and delayed settlements push users toward specialized fintech wallets that offer near-instant disbursement. Rural southern regions grapple with connectivity deficits that slow QR adoption, underscoring the need for offline functionality and agent banking. Regional banks are forming alliances with telcos to roll out cash-in/cash-out nodes, bridging physical and digital ecosystems.

Regulatory uniformity from Banco de México provides a nationwide rulebook, yet local culture and economic profiles shape product design. Indigenous communities require interfaces in native languages and flexible KYC processes to amplify trust. Tourism belts along the Yucatán Peninsula lean on contactless card acceptance to serve international visitors, bolstering seasonal spikes in the Mexico payments market. Overall, geographic diversity demands agile infrastructure capable of handling micro-transactions in remote villages and high-value cross-border B2B payments in industrial corridors.

Competitive Landscape

Traditional banks retain scale advantages, but fintech challengers are capturing niche segments through specialized user journeys and fee transparency. BBVA México commands a broad digital footprint with 12.7 million monthly active users, providing a deep data reservoir for personalized offers. Nearly 1,000 fintechs have secured or are seeking licenses, signaling rising rivalry within the Mexico payments market. Players such as Mercado Pago and Nu Mexico are extending beyond wallets into credit, insurance, and investments to enhance stickiness.

Strategic acquisitions are accelerating capabilities: Klar acquired Tribal to deepen B2B settlement expertise, while Airwallex bought Mexpago to push cross-border services into Mexico. Technology priorities center on AI fraud detection, biometric ID, and ISO 20022 compliance to facilitate real-time messaging. Domestic data-hosting mandates bestow an operational edge on local cloud providers, increasing entry barriers for foreign newcomers. Despite moderate fragmentation, the top five entities collectively manage a majority of electronic transaction value, indicating gradual consolidation trajectory in the Mexico payments market.

White-space opportunities lie in healthcare payments, agricultural supply-chain financing, and rural agent networks. Interoperability initiatives that bridge CoDi, card schemes, and closed-loop wallets promise to unlock network effects. Competitive differentiation will hinge on embedded analytics that convert transaction data into credit-scoring and loyalty insights. As regulations evolve to accommodate open-banking APIs, incumbents and disruptors alike will race to integrate savings, lending, and wealth modules within single-stack ecosystems, reinforcing the breadth of the Mexico payments industry.

Mexico Payments Industry Leaders

Visa Inc.

Mastercard Incorporated

American Express Company

HSBC Holdings plc

Citigroup Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nu Mexico expanded its partnership with OXXO, enabling cash withdrawals at 22,000 stores and lifting its physical touchpoints above 30,000 nationwide.

- January 2025: Creditea partnered with Conekta to embed BNPL across merchant networks, offering four interest-free biweekly installments.

- December 2024: CNBV published the first comprehensive dataset on licensed Financial Technology Institutions, enhancing transparency for investors and consumers.

- November 2024: Paymentology entered a strategic alliance with digital bank albo to support its 2 million users, adding dynamic CVV and 400 new cash top-up points.

Mexico Payments Market Report Scope

Payments are becoming increasingly cashless, and the industry's responsibility to support inclusivity has risen to the top of the agenda. Payments help promote digital economies and encourage innovation while also providing a reliable backbone for the global economy. POS and e-commerce are the two segments of the payments market. Online purchases of both products and services, such as purchases made on e-commerce websites and online travel and hotel bookings, are examples of e-commerce payments. All transactions taking place at a physical point of sale are included in the market's scope when it comes to POS.

The Mexican payments market is segmented by mode of payment (point of sale [card payments, digital wallet, cash, and other points of sale] and online sale [card payments, digital wallets, and other online sales]) and end-user industry (retail, entertainment, healthcare, hospitality, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other Point of Sale Payment Mode | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Mode |

End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Other End-User Industries |

| Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Point of Sale Payment Mode | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Mode | ||

| End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Mexico payments market in 2026?

The Mexico payments market size is USD 138.05 billion in 2026 and is on track to reach USD 222.43 billion by 2031.

What is driving double-digit growth?

Regulatory support, rapid smartphone adoption, and booming e-commerce are propelling a 10.01% CAGR for the Mexico payments market.

Which payment mode is expanding fastest?

Digital wallets lead with a forecast 10.74% CAGR, supported by partnerships that blend online convenience with physical cash-in points.

Which end-user sector shows the highest growth potential?

Healthcare is projected to grow at 11.08% CAGR as telemedicine and micro-insurance integrate real-time payment workflows.

What is the main challenge to full digital adoption?

High cash preference among micro-merchants and escalating cyber-security threats remain key restraints on the Mexico payments market.

Page last updated on: