Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

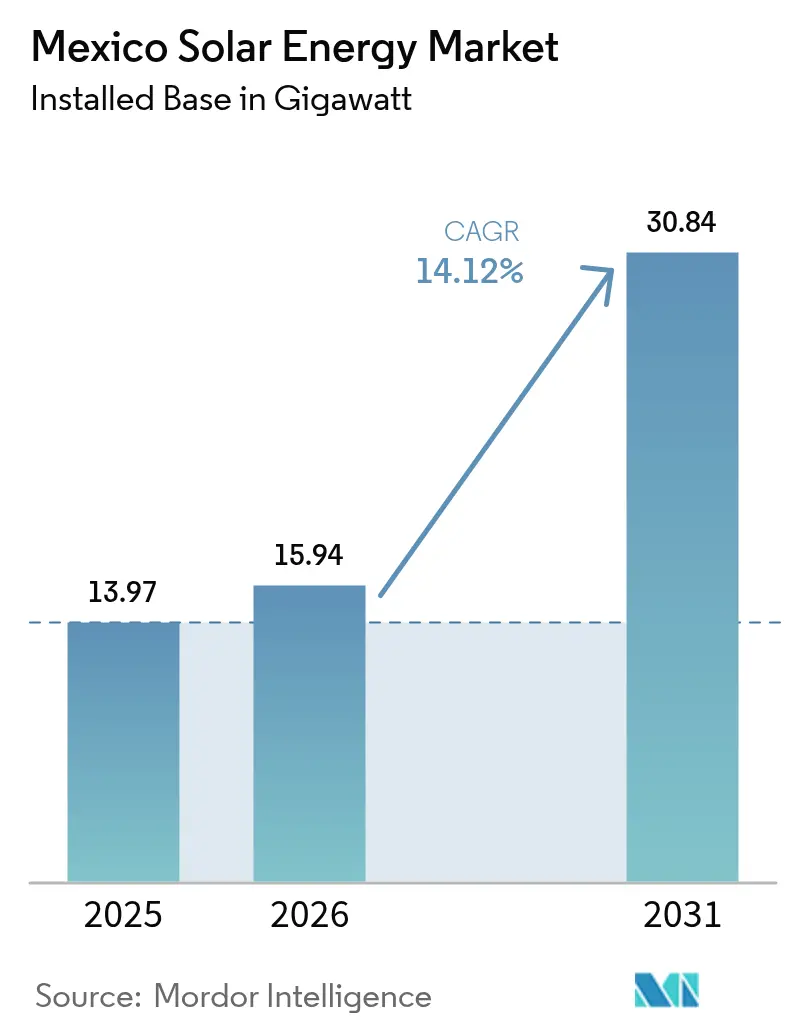

| Base Year Market Size (2025) | 13.97 gigawatt |

| Market Volume (2026) | 15.94 gigawatt |

| Market Volume (2031) | 30.84 gigawatt |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

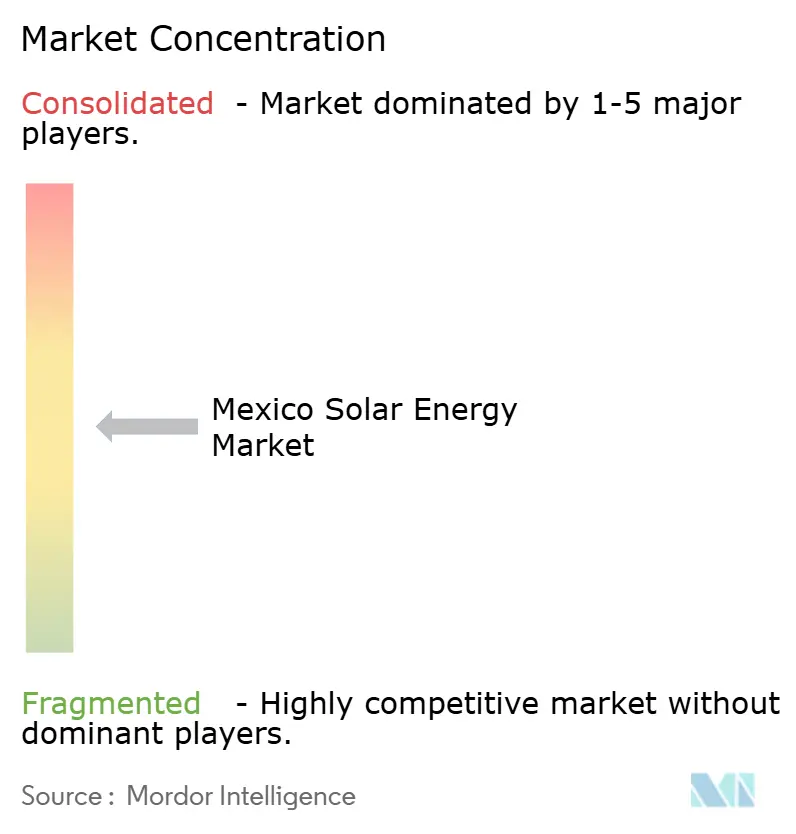

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Solar Energy Market Analysis by Mordor Intelligence

The Mexico Solar Energy Market size is expected to grow from 13.97 gigawatt in 2025 to 15.94 gigawatt in 2026 and is forecast to reach 30.84 gigawatt by 2031 at 14.12% CAGR over 2026-2031.

Rising deployment is anchored in President Claudia Sheinbaum’s 45% clean-power goal for 2030, abundant irradiance over 85% of national territory, and a regulatory regime that retains private-sector pathways even as Comisión Federal de Electricidad (CFE) safeguards a 54% generation quota. Utility-scale plants dominate capacity additions, yet residential and commercial distributed generation is accelerating as equipment prices fall and green financing scales up. Nearshoring pressures from United States manufacturers add new corporate-PPA demand, while a US-Mexico-Canada Agreement sustainability clause tightens the link between trade and renewable sourcing. Planned transmission upgrades, battery manufacturing incentives under the USD 7 billion Plan Sonora, and CFE’s USD 23.4 billion investment plan further support growth even as policy shifts and permitting bottlenecks inject near-term uncertainty.

Key Report Takeaways

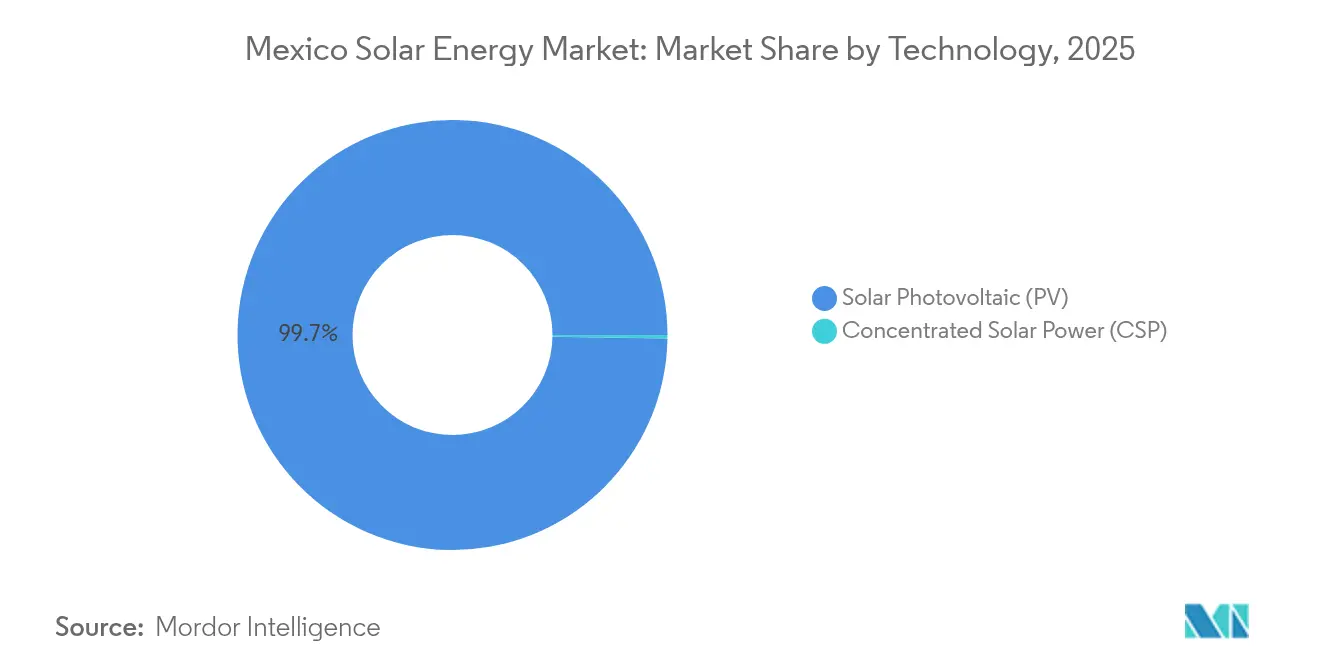

- By 2025, photovoltaic systems held 99.74% of the Mexican solar energy market share, while solar thermal systems for industrial heat are projected to rise at a 36.83% CAGR through 2031.

- By grid type, on-grid systems accounted for 94.85% of the Mexico solar energy market size in 2025, whereas off-grid solutions are forecast to progress at a 20.65% CAGR through 2031.

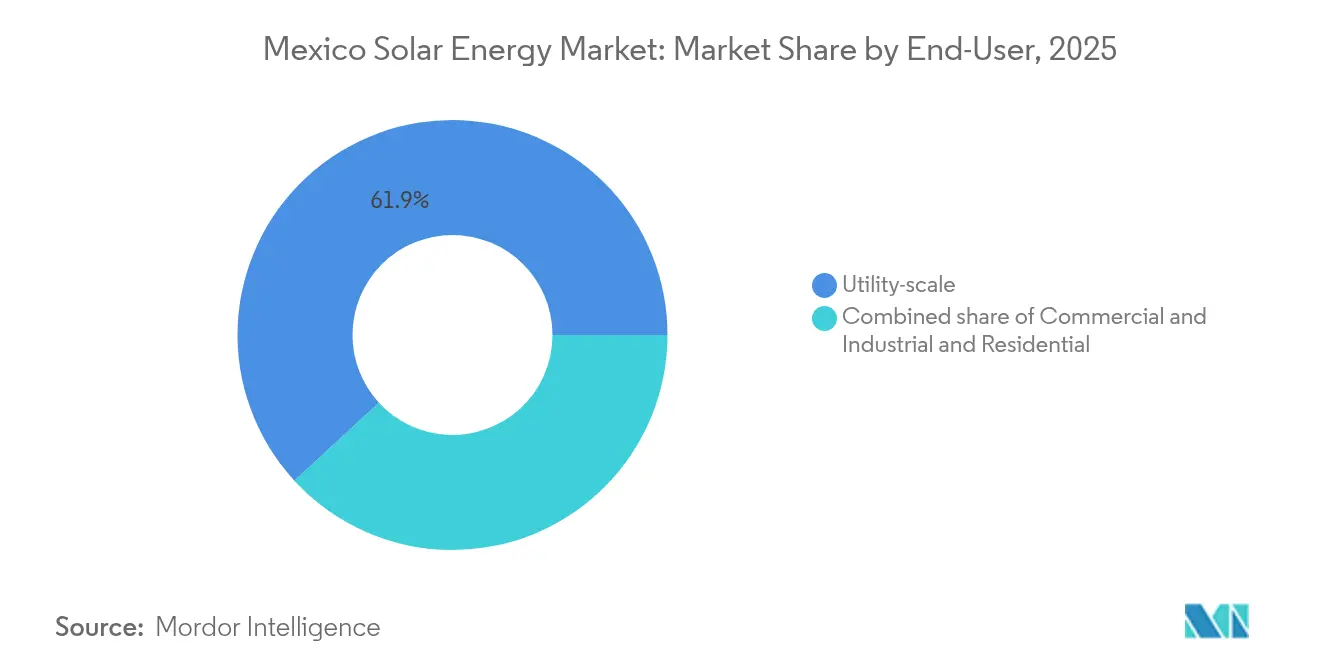

- By end-user, the utility-scale segment captured 61.85% of the Mexican solar energy market size in 2025, while the residential sector is set to grow at an 18.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant solar irradiance across 85% of the country | 3.20% | North and Central regions | Long term (≥ 4 years) |

| Government clean-energy targets to 45% by 2030 | 4.10% | National with focus on Sonora and Coahuila | Medium term (2-4 years) |

| Falling PV capex and new rooftop financing | 2.80% | Urban and peri-urban locations | Short term (≤ 2 years) |

| Powershoring demand for low-carbon supply chains | 3.50% | Border states and manufacturing corridors | Medium term (2-4 years) |

| Smart-grid and storage upgrades | 1.90% | Metropolitan and industrial zones | Long term (≥ 4 years) |

| Corporate-PPA momentum under USMCA clauses | 2.70% | Export-oriented hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Solar Irradiance Drives Geographic Advantage

Mexico achieves irradiation levels above 2,000 kWh/m²/year in its northern deserts and still exceeds 1,600 kWh/m²/year in the south, yielding capacity factors of 25-30% that outperform European benchmarks.[1]Intersolar Mexico, “Mexico’s Solar Resource Potential,” intersolar.mx Seasonally consistent radiation enables developers to diversify their portfolios, smoothing output and reducing project risk. Studies estimate the technical potential at nearly 24,918 GW, which is many times the current installations, positioning the Mexican solar energy market as a future regional powerhouse.[2]Mexico Energy Partners, “Technical Solar Potential Study,” mexicoenergypartners.com

Government Clean-Energy Targets Reshape Investment Landscape

The National Strategy for the Electric Sector 2024-2030 allocates USD 12.3 billion to new generation, increasing the limits on distributed-generation projects to 0.7 MW and streamlining permit requirements to 20 MW. CFE issued USD 1.5 billion of sustainable bonds in 2024 to finance assets, including the 1,000 MW Puerto Peñasco project. Mixed public-private development models now balance state oversight with private capital, sustaining the Mexico solar energy market despite CFE dominance.

Falling PV Costs Enable Distributed Generation Boom

Auction clearing prices slid from USD 50/MWh to USD 20/MWh, outpacing rising retail tariffs that hit 151.60 USD/MWh in 2023.[3]Global Climatescope, “Mexico Power Market Tariff Tracker,” global-climatescope.org More than 450,000 net-metered contracts, mainly residential, already total nearly 4 GW. Green mortgages and Fondo de Servicio Universal Eléctrico widen access, while lighter Comisión Reguladora de Energía rules lower soft costs. Analysts expect 600,000 solar rooftops by 2026, reshaping consumption profiles in the Mexico solar energy market.

Powershoring Amplifies Industrial Solar Demand

US manufacturers relocating facilities under near-shoring strategies insist on renewable energy. Microsoft’s USD 1.1 billion data center commitment in Querétaro illustrates the clean power pull that accelerates corporate PPAs. Border states Nuevo León and Chihuahua have seen manufacturers purchase dedicated plants to secure a solar supply, thereby embedding demand directly into industrial growth trajectories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy uncertainty & permitting delays under energy-sector reforms | -2.3% | National, particularly affecting private developers and foreign investors | Short term (≤ 2 years) |

| Dominance of CFE limiting private-grid access | -1.9% | National, concentrated in transmission-dependent regions and utility-scale projects | Medium term (2-4 years) |

| Land-use & social-license conflicts in desert utility-scale zones | -1.4% | North region desert areas, particularly Sonora and Chihuahua | Medium term (2-4 years) |

| Grid-congestion & curtailment risk in high-DG regions | -1.2% | North region and metropolitan areas with high solar penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Policy Uncertainty Creates Investment Hesitation

The transfer of CRE and CNH duties to a new National Energy Commission resulted in a 75% decline in clean-energy investment, dropping to USD 302 million in 2023. Secondary legislation due by September 2025 lengthens the clarity gap, raising financiers’ risk perception and slowing project pipelines.[4]White & Case, “Mexico Energy Reform: Legal Outlook,” whitecase.com

CFE Market Dominance Constrains Grid Access

The statutory 54% generation share reserved for CFE grants the utility key control of transmission planning. Developers report curtailment in Sonora because surplus mid-day output cannot reach distant demand centers, and dispatch priority often favors CFE gas assets over lower-cost solar. These conditions temper the private sector's appetite, especially for large solar parks that rely on grid evacuation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic Dominance Faces CSP Renaissance

Photovoltaic systems captured 99.74% of the Mexico solar energy market share in 2025, reflecting entrenched cost advantages and a mature supply chain that spans residential rooftops through multi-gigawatt parks. Concentrated Solar Power, however, is projected to expand at a 36.83% CAGR to 2031 as policymakers seek dispatchable renewable capacity that pairs thermal storage with Mexico’s world-class direct normal irradiance in desert states such as Sonora and Chihuahua.

The technology mix is evolving from pure cost optimization toward achieving grid stability and energy security goals. CFE’s hybrid geothermal–solar plan at Cerro Prieto and the Puerto Libertad steam project illustrate institutional support for thermal technologies beyond PV. Mexico’s leadership in industrial solar-thermal installations underpins a forecast 7.25 million m² of hybrid collectors by 2030, a build-out that could cut Food and Beverage sector emissions by 51.7%. As a result, the Mexico solar energy market size attributed to CSP and advanced thermal solutions is expected to expand steadily, even as PV remains the cornerstone of capacity.

By Grid Type: On-Grid Supremacy Meets Off-Grid Innovation

On-grid projects accounted for 94.85% of the Mexico solar energy market size in 2025, supported by net-metering rules and the reach of the National Electric System. Off-grid and hybrid systems, though smaller in absolute terms, are growing at a 20.65% CAGR through 2031 as remote mines, farms, and island communities adopt storage-backed arrays that bypass transmission bottlenecks.

Battery prices below USD 100/kWh and new market rules that let storage earn capacity payments now tilt project economics toward energy independence. Plan Sonora’s USD 7 billion battery cluster will shorten supply lines for domestic integrators, enabling off-grid solutions to deliver 24/7 reliability that rivals grid-connected service during peak-load curtailments. Agro-voltaic pilots in Yucatán and Chiapas confirm that stand-alone solar can power irrigation while shielding crops, a dual-benefit model expected to lift the off-grid slice of the Mexico solar energy market by decade-end

By End-User: Utility-Scale Leadership Challenged by Residential Surge

Utility-scale plants held 61.85% of the Mexico solar energy market share in 2025, anchored by projects such as the 1,089 MW Villanueva park and CFE’s 1,000 MW Puerto Peñasco venture. Residential arrays, however, are advancing at an 18.21% CAGR to 2031 as household economics improve; average retail tariffs reached 151.60 USD/MWh in 2023, while module prices slid to historical lows.

More than 450,000 interconnection contracts—75% of which are residential—already total nearly 4 GW, underscoring the consumer appetite for self-generation. Green mortgages and the Fondo de Servicio Universal Eléctrico extend financing to lower-income households, boosting inclusion without sacrificing technical standards. Corporates such as Grupo Bachoco demonstrate the middle-ground appeal of distributed portfolios, having installed 26 MW across 19 states to hedge tariff risk and accelerate ESG compliance. Looking forward, hybrid solar-plus-storage configurations are becoming standard at both residential and utility scales, positioning dispatchability—not just cost—as the decisive differentiator in the Mexico solar energy market.

Geography Analysis

The North region dominates the current capacity in the Mexican solar energy market due to its superior irradiance, industrial demand, and shorter routes to the United States' off-takers. Sonora’s Plan Sonora integrates lithium mining and battery cell production, fostering a localized value chain that informs project finance models and labor demand. However, congestion on the existing 400 kV lines curtails midday PV exports, prompting calls for HVDC links to central load hubs.

Central Mexico, encompassing Mexico City and the State of Mexico, balances high demand with rooftop potential. Steep retail tariffs and dense urban real estate encourage the installation of solar canopies and commercial warehouses. Municipal green-bond frameworks support schools and hospitals in adopting distributed arrays, establishing a replicable model for other metropolitan areas in the Mexico solar energy market.

The South & Peninsula exhibits the quickest installation pace as tourism and near-coastal manufacturing amplify load growth. Microgrids powered by hybrid solar-storage systems lower reliance on diesel and fortify resilience to tropical storm outages, particularly in Quintana Roo. Agro-voltaic pilots in Yucatán demonstrate the benefits of co-location, where shading improves crop yields and diversifies farmer income, underscoring the inclusivity potential of the Mexican solar energy market.

Competitive Landscape

International developers continue to dominate the utility-scale tier. Enel Green Power operates 2.98 GW across 19 Mexican plants, combining solar, wind, and hydro for portfolio hedging. Iberdrola, Acciona, Engie, and Sonnedix follow with multi-GW pipelines. Canadian Solar, Jinko, Trina, and LONGi supply modules, while First Solar’s thin-film technology finds niche demand in high-temperature desert operations.

Supply-chain localization gains momentum. A USD 198 million cell and module plant in Durango enhances regional content ratios, enabling developers to manage import tariffs introduced by the United States in 2025. Rafiqui’s recycling complex adds circular-economy credentials, and Chinese inverter firms expand assembly within Mexico to sidestep duties.

Strategic differentiation is increasingly centered on storage integration, hybrid plant optimization, and financial innovation, rather than headline-per-watt pricing. Players able to bundle software, asset management, and capital-market access will outpace pure-play EPCs. Market consolidation is expected as smaller installers face balance-sheet pressure, tilting the Mexico solar energy market toward mid- and large-cap firms proficient in policy navigation and risk management.

Mexico Solar Energy Industry Leaders

Enel Green Power México

Iberdrola México

Engie México

Canadian Solar

Acciona Energía

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: President Sheinbaum signed reforms that elevate the National Energy Commission and retain CFE’s 54% generation share while outlining six private development models.

- March 2025: New electricity laws dissolved CRE and CNH, consolidating oversight under the Ministry of Energy with secondary rules due by September 2025.

- February 2025: CFE unveiled a USD 22.3 billion system strengthening plan, which includes 9 solar PV plants totaling 673 MW and 22,674 MW of overall additions.

- February 2025: The United States imposed tariffs on solar imports from Mexico, influencing module sourcing and project economics.

Mexico Solar Energy Market Report Scope

The scope of the Mexican solar energy market report includes:

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What is the current Mexico solar energy market size?

The installed base stands at 15.94 GW in 2026 and is set to rise to 30.84 GW by 2031.

How fast is the Mexico solar energy market growing?

Capacity is increasing at a 14.12% compound annual rate through 2031.

Which segment is expanding quickest?

Residential distributed generation leads with an 18.21% CAGR owing to lower module prices and green financing programs.

How will new Mexican energy laws affect investors?

The laws elevate CFE’s role but keep private participation open under six models, so bankable projects will rely on clear interconnection rights and long-term PPAs.

What role will storage play in future growth?

Hybrid solar-plus-battery systems are projected to grow at 21.55% CAGR as battery prices fall and new market rules allow revenue stacking.

Page last updated on: