Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

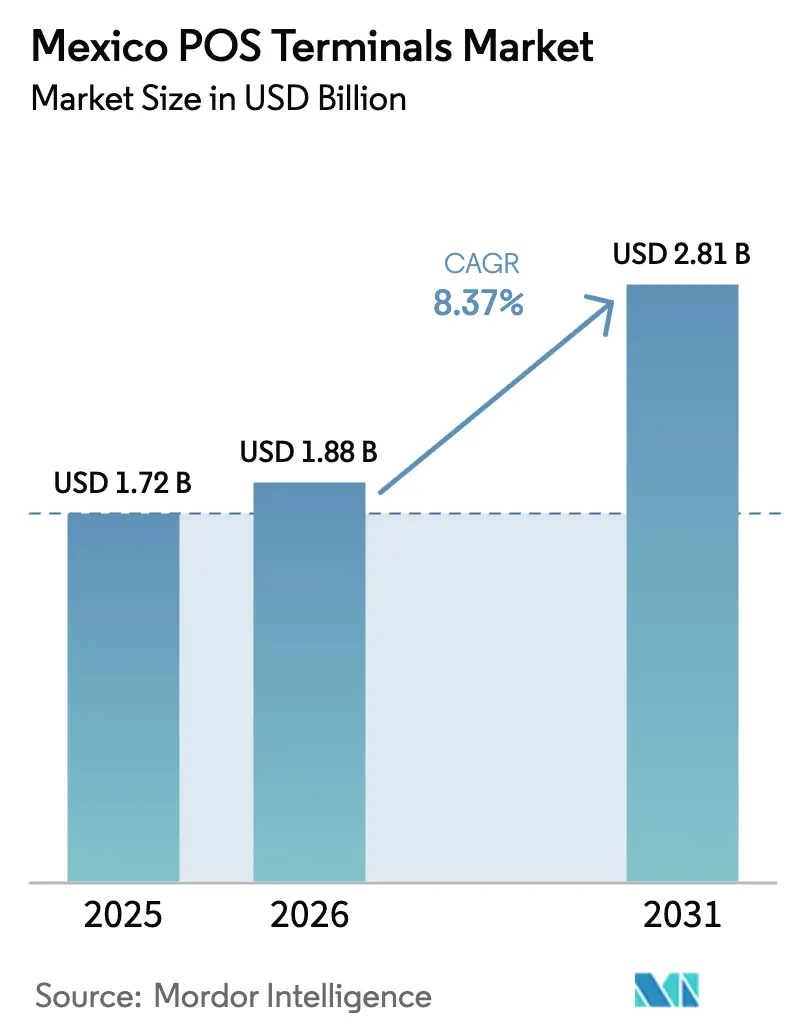

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 8.37% CAGR |

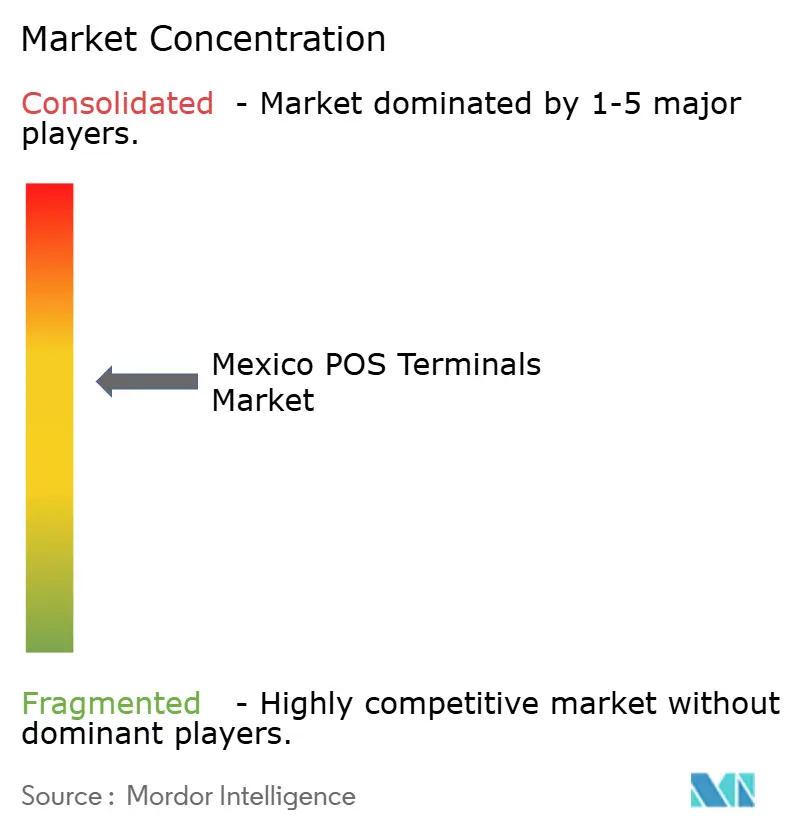

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico POS Terminals Market Analysis by Mordor Intelligence

The Mexico POS terminals market size is projected to expand from USD 1.72 billion in 2025 and USD 1.88 billion in 2026 to USD 2.81 billion by 2031, registering a CAGR of 8.37% between 2026 to 2031. Steady migration away from cash, a dense pipeline of low-cost mobile readers, and pro-competition regulation are widening acceptance, yet informal commerce, network interoperability gaps, and fraud anxiety continue to temper the upside. Contact-based devices still anchor most checkout lanes, but near-field communication rollouts are compressing upgrade cycles, while embedded-financing bundles are tightening aggregator lock-in. Draft interchange caps promise to ease merchant costs, though they also compress acquirer margins and could spark price realignments. Hardware supply chains have largely stabilized ahead of the 2026 FIFA World Cup, easing the execution risk around planned terminal deployments.

Key Report Takeaways

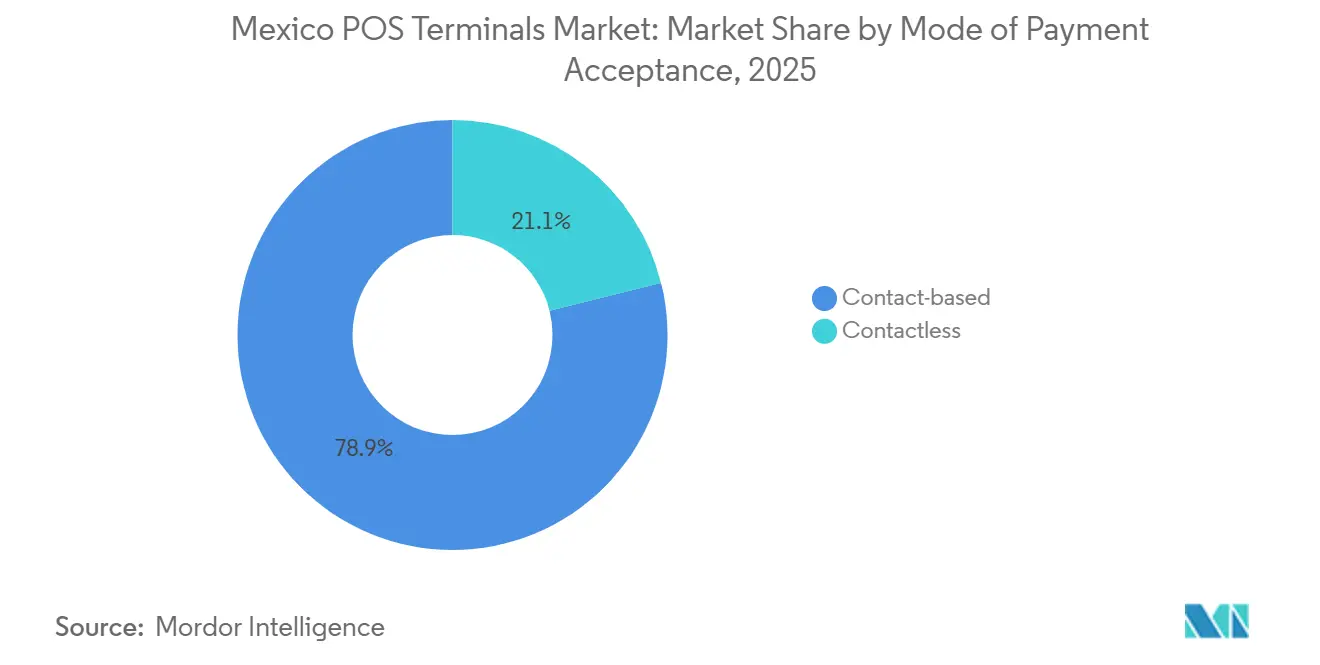

- By mode of payment acceptance, contact-based terminals led with 78.89% of the Mexico POS terminals market share in 2025, whereas contactless systems are projected to advance at a 10.18% CAGR through 2031.

- By POS type, mobile and portable devices accounted for 67.97% of the Mexico POS terminals market size in 2025 and are forecast to grow at a 9.04% CAGR between 2026-2031.

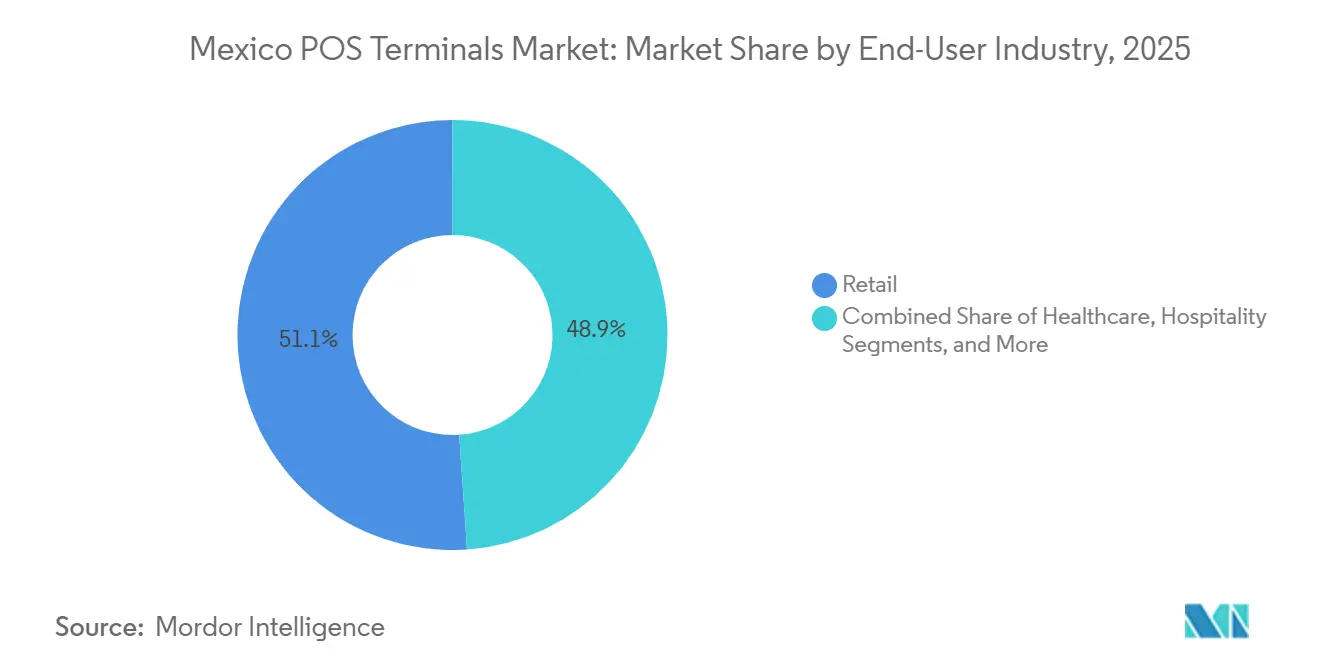

- By end-user industry, retail held 51.07% of demand in 2025, while healthcare is expected to post the fastest expansion at an 11.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Contactless-NFC Transactions | +2.1% | National, Strongest in Mexico City, Guadalajara, Monterrey | Medium Term (2-4 Years) |

| SME Adoption of Mobile POS Aggregators | +1.9% | National, Concentrated in Urban and Peri-Urban Corridors | Short Term (≤ 2 Years) |

| CoDi and DiMo Real-Time Payment Rails | +1.3% | National, Pending Incentives | Long Term (≥ 4 Years) |

| MDR Caps Boost Card Acceptance | +1.5% | National, Acute Among Micro-Merchants | Medium Term (2-4 Years) |

| Embedded Lending and Data-Driven Analytics | +0.9% | National | Medium Term (2-4 Years) |

| Rise of Software-Only SoftPOS Solutions | +0.6% | National, Early Pilots | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Surge in Contactless-NFC Transactions

Contactless payment volume jumped 150% year-over-year in 2024, lifted by BBVA’s rollout of 45,000 NFC-enabled devices across 22,000 OXXO stores and the enablement of tap-to-pay on 70% of its card portfolio.[1]Asociación de Bancos de México, “Contactless Payment Volume Growth in Mexico,” ABM.ORG.MX Mexico City, Guadalajara, and Monterrey together generate a disproportionate share of tap activity as commuters favor speed and hygiene, whereas rural municipalities trail because legacy mag-stripe readers remain serviceable. Acquirers benefit from 15% fewer chargebacks and faster settlement, trimming fraud reserves and float funding costs.[2]Visa, “Unlocking the Benefits of Digital Payments for Micro & Small Businesses: Insights from Mexico,” VISA.COM Vendors are racing for PCI PTS v7 certification, which hard-codes tokenization and secure elements into new hardware, effectively forcing merchants to refresh devices before enforcement deadlines.

SME Adoption of Mobile POS Aggregators

Aggregators operated more than 1 million active terminals by September 2025, with Mercado Pago alone hitting that milestone and Clip serving over 2 million merchants processing 4 million daily transactions.[3]PYMNTS, “Clip, Mercado Pago, and SumUp Market Developments,” PYMNTS.COM Devices priced below MXN 1,000 (USD 54) and instant onboarding contrast sharply with the costly, paperwork-heavy model still common among banks. The Ministry of Economy’s December 2025 program promises zero-cost readers for 1 million MSMEs ahead of the 2026 World Cup, dramatically enlarging the funnel for first-time acceptance.[4]Pérez-Llorca and Aurea Partners, “Fintech 2025: Mexico,” CHAMBERS.COM Embedded loans amplify loyalty, Mercado Pago issued 2.5 million small-ticket credits to 400,000 businesses, turning payment data into underwriting fuel that incumbents struggle to replicate.

CoDi and DiMo Real-Time Payment Rails

CoDi accumulated just 11.9 million transactions through Q1 2024, equating to under 1% of daily payment flows despite fee-free rules. DiMo added 7.5 million users within twelve months, but merchant acceptance remains patchy because user journeys lack receipt flows or refunds. The Federal Economic Competition Commission urged Banco de México to allow third-party overlays that could bundle loyalty or cash-back modules, mirroring Brazil’s Pix success where average merchant cost is 0.22% against 2.2% for cards.[5]Federal Economic Competition Commission, “Study of Competition and Free Market Access in Digital Financial Services,” COFECE.MX If regulators green-light value-added layers and banks commercialize APIs, real-time rails could undercut interchange-based economics and remodel terminal demand.

MDR Caps Boost Card Acceptance

In October 2025, draft rules proposed slashing interchange to 0.3% on debit and 0.6% on credit, down from roughly 1.15% and 1.91% . Lower merchant discount rates should unlock acceptance among taco stands, laundromats, and pharmacies where average tickets have fallen to MXN 580 (USD 31). Aggregators are structurally advantaged because they already monetize thin spreads and upsell credit, whereas traditional acquirers face margin compression. Complementary surcharge bans enacted in April 2024 further neutralized a key merchant objection to taking cards.[6]Banco de México, “Annual Report 2024: Payment Systems and Financial Infrastructure,” BANXICO.ORG.MX

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Cash Preference and Unbanked Base | -1.8% | National, Acute in Rural Municipalities | Long Term (≥ 4 Years) |

| Card-Data Security and Fraud Exposure | -1.2% | National, Concentrated in E-Commerce | Short Term (≤ 2 Years) |

| Terminal Hardware Supply-Chain Volatility | -0.7% | National | Medium Term (2-4 Years) |

| Merchant Friction on DiMo/CoDi Fees and UX | -0.5% | National | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Persistent Cash Preference and Unbanked Base

Nine of every ten adults still rely on cash for day-to-day spending, while 74.5% of households remain cash-exclusive. Half the population is unbanked, and 55% of workers earn income informally, short-circuiting the card issuance loop. Connectivity divides amplify the gap: 19 million adults lack internet, 18 million lack smartphones, and 14 million lack both. Pilot projects show upside, tortillerías using QR and contactless added up to USD 1,912 in monthly revenue, but adoption targets of 40% in year one underscore the gradual cultural shift.

Card-Data Security and Fraud Exposure

Fraud losses hit MXN 11.3 billion (USD 611 million) in 2024, with identity theft up 77% year-over-year and social-engineering scams driving 72% of incidents. Chargeback-prone e-commerce saw acceptance rates dip below 67% by value, eroding merchant confidence. New internal-control rules demand multi-factor authentication and near-real-time monitoring, straining small acquirers. Players with scale, Citibanamex cut fraud 70% via AI and Nu México earmarked USD 100 million for defenses, are fortifying, yet the compliance burden may slow onboarding at the long tail of micro-merchants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contact-Based Dominance, Contactless Momentum

Contact-based terminals captured 78.89% of the Mexico POS terminals market share in 2025, a reflection of legacy mag-stripe and chip-and-PIN estates. Transaction stability caters to high-ticket verticals such as electronics and automotive service where customers still prefer PIN entry. Yet contactless sales grew triple digits in 2024 after BBVA deployed NFC readers chain-wide at OXXO, showing the velocity that subsidy-backed rollouts can reach. Because contactless clears faster and posts roughly 15% fewer chargebacks, supermarkets and quick-service restaurants view upgrades as throughput enhancers.

The Mexico POS terminals market size attributable to contactless devices is expected to expand at a 10.18% CAGR, helped by mandatory PCI PTS v7 compliance and multi-network acceptance rules under the National Banking and Securities Commission. Ingenico’s AXIUM and Verifone’s Victa families both ship with dual-interface antennas, biometric modules, and Android 14 operating systems, future-proofing merchants for loyalty, stablecoin acceptance, and identity verification. As acquirers refresh estates, mixed fleets will persist; the tipping point hinges on device financing programs that alleviate upgrade costs for micro-merchants.

By POS Type: Mobile Systems Shape Merchant Economics

Mobile and portable devices commanded 67.97% of 2025 installations, thanks to aggregator strategies that bundle low-cost card readers with instant KYC and same-day settlement. Clip’s Ultra ruggedized model and Mercado Pago’s smart terminal lineup illustrate the pivot from dongles to app-rich, Android-based hardware capable of inventory control and lending origination. The segment is projected to clock a 9.04% CAGR, outpacing the overall Mexico POS terminals market, as SumUp’s January 2026 entry intensifies price competition yet broadens reach among still-cash-only MSMEs.

Fixed countertop systems held the balance 32.03% share, entrenched in grocery chains, department stores, and gas stations where Ethernet reliability and integrated receipt printers remain non-negotiable. Still, cloud device-management suites such as Ingenico 360 enable remote diagnostics, narrowing the service-level gap with field-upgradable mobiles. SoftPOS solutions, Verifone Tap and the AXIUM software stack, introduce a hardware-less model that could cannibalize low-end mobile readers, though security certification and merchant trust keep widespread adoption a longer-term prospect.

By End-User Industry: Retail Volume, Healthcare Velocity

Retail generated 51.07% of transactions in 2025, buoyed by dense convenience-store networks and nationwide department-store footprints. Banorte, for instance, expanded its acquirer estate 18% year-over-year in underserved municipalities, signaling that even in peri-urban corridors card acceptance lifts basket sizes. Hospitality is adding tap-to-pay ahead of the World Cup, but healthcare is the fastest-growing vertical, set to advance at 11.23% CAGR through 2031 as public clinics digitize billing and private hospitals link POS data to patient records for real-time claims.

The Mexico POS terminals market size tied to healthcare remains smaller today but benefits from mandatory electronic payments for co-pays and prescriptions. Integrated patient-management suites boost revenue-cycle accuracy, trimming reconciliation delays. In parallel, pharmaceutical retail inside hospitals adopts mobile readers to reduce cash-handling, reinforcing hygiene and security imperatives. Regulatory data-privacy mandates elevate hardware requirements, tokenization, end-to-end encryption, raising switching costs and cementing vendor relationships.

Geography Analysis

Greater Mexico City, Guadalajara, and Monterrey host roughly 40% of the installed terminal base despite representing just one-fifth of the population, underscoring the urban skew of the Mexico POS terminals market. Card transactions nationwide totaled 10.662 billion operations valued at MXN 6.2 trillion (USD 335 billion) from July 2024 to June 2025, reflecting 18.4% volume growth and illustrating the widening digital footprint. Yet CoDi accounts for less than 1% of daily flows, emphasizing that infrastructure availability does not guarantee adoption.

Peri-urban belts now receive concentrated investment, with Banorte reporting 73% terminal growth in municipalities previously underserved by banks. Correspondent agents fill branch gaps, but their density is uneven: OXXO alone controls 46% of correspondent points, exposing geographic concentration risk. Southern states, Oaxaca, Chiapas, Guerrero, lag in both device penetration and card issuance, yet they represent the largest untapped pool where zero-fee device programs could unlock millions of merchants. Frontier states facing the United States perform above average, leveraging cross-border commerce and dynamic-currency conversion to attract dollar spend.

Preparations for the 2026 World Cup are catalyzing upgrades in host cities, spurring adoption of multi-wallet acceptance, offline fallback, and EMV QR to serve 5.5 million expected visitors. Whether those investments radiate into outlying boroughs will hinge on connectivity build-outs, as 19 million adults still lack internet, many of them living in high-marginalization zones. Banco de México’s interoperability oversight and the National Banking and Securities Commission’s acquirer licensing standards continue to push the market toward broader, more transparent coverage.

Competitive Landscape

Non-bank institutions operate 78% of the 6.3 million-plus terminals deployed as of December 2024, proving that platform-based models can outpace bank-centred distribution. Commercial banks still clear 91.3% of card value but are ceding hardware ground to aggregators that weave payment acceptance into credit, analytics, and loyalty. Mercado Pago’s estate surpasses 1 million active devices, 60% of which are smart, application-ready units, deepening ecosystem lock-in. Clip, having seeded micro-merchants, is climbing upmarket with API-enabled Pin Pad and rugged Ultra models, courting enterprise chains that demand ERP connectivity.

Global Payments’ July 2025 renewal with Banamex keeps a 900 million-transaction pipeline intact, illustrating that bank partnerships remain relevant where countertop estates and payroll clients converge. Meanwhile, white-space pivots around software-only acceptance: Ingenico’s SoftPOS-ready AXIUM suite and Verifone Tap convert commercial smartphones into terminals, chopping capital costs and potentially recoding economics for small traders. Biometric add-ons, Verifone’s PopID face and palm modules, promise faster checkout and identity assurance, yet certification and privacy hurdles could slow scaling.

PCI PTS v7 and mandatory multi-network acceptance rules create high fixed costs for certification, tilting advantage toward incumbents that can amortize across global volumes. Still, aggregators leverage nimble software stacks to iterate features, installments, pay-by-link, split bills, at speeds legacy acquirers rarely match. The competitive chessboard therefore pivots on ecosystem breadth rather than device counts alone, positioning data-rich platforms to capture the next wave of merchant adoption across the Mexico POS terminals market.

Mexico POS Terminals Industry Leaders

Ingenico Mexico SA De CV

Verifone Systems Inc.

PAX Technology Limited

Diebold Nixdorf Incorporated

BBPOS Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ingenico launched its AXIUM payment-device family and Ingenico 360 cloud platform, delivering Android 14, PCI PTS v7 certification, and SoftPOS capability for large-scale global rollouts.

- January 2026: SumUp began Mexican operations, introducing mobile card readers for micro-merchants still reliant on cash.

- December 2025: The Ministry of Economy, Visa, BBVA, and Santander unveiled “Crece tu mipyme con pagos digitales,” aiming to equip 1 million MSMEs with zero-cost devices before the World Cup.

- December 2025: Spin and Visa extended their alliance for eight years to widen digital-wallet acceptance across OXXO’s network.

Mexico POS Terminals Market Report Scope

A point of sale (POS) terminal is a digital electronic gadget that allows businesses to take payments without directly reading cards through their cash registers. It functions via a mix of hardware and software. Devices are used to accept card/cash payments, manage inventory, print invoices, etc., in various end-use industries, including restaurants, hotels, healthcare, retail, warehouse/distribution, and entertainment. The POS terminal is operated through two types of products: wired or fixed POS terminal and mobile or wireless POS terminal.

The Mexico POS Terminals Market Report is Segmented by Mode of Payment Acceptance (Contact-based, Contactless), POS Type (Fixed Point-of-Sale Systems, Mobile and Portable Point-of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

How large will electronic payment acceptance become in Mexico by 2031?

The Mexico POS terminals market is expected to reach USD 2.81 billion by 2031 on an 8.37% CAGR, reflecting sustained device rollouts and regulatory cost relief.

Which terminal form factor is growing the fastest?

Mobile and portable readers lead growth, projected to expand at a 9.04% CAGR as aggregators push low-priced, Android-based devices to micro-merchants.

What regulations could reshape merchant economics most in the near term?

Draft interchange caps of 0.3% for debit and 0.6% for credit transactions would slash acceptance costs for low-ticket merchants if enacted in 2026.

Why is healthcare poised for rapid terminal adoption?

Public-sector mandates for electronic co-pay collection and private hospitals' drive to integrate payments with patient records support an 11.23% CAGR to 2031.

Are software-only SoftPOS solutions ready to replace hardware readers?

SoftPOS is certified for tap-on-phone in Mexico, but merchant trust and handset fragmentation mean it will complement, not immediately displace, dedicated mobile terminals.

How will the 2026 FIFA World Cup affect deployment?

An influx of 5.5 million visitors is accelerating upgrades in host cities, especially adding contactless and multi-wallet support across retail, hospitality, and transport venues.

Page last updated on: