Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

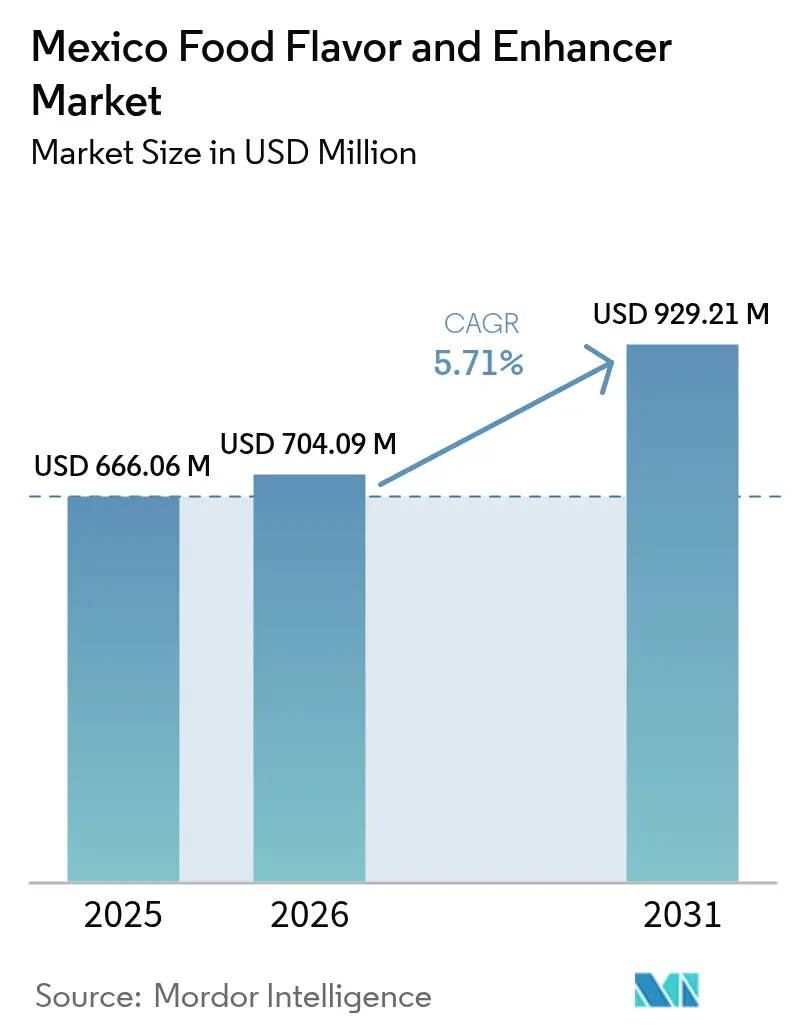

| Base Year Market Size (2025) | USD 666.06 Million |

| Market Size (2026) | USD 704.09 Million |

| Market Size (2031) | USD 929.21 Million |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Food Flavors And Enhancers Market Analysis by Mordor Intelligence

The Mexico Food Flavors And Enhancers Market size was valued at USD 666.06 million in 2025 and estimated to grow from USD 704.09 million in 2026 to reach USD 929.21 million by 2031, at a CAGR of 5.71% during the forecast period (2026-2031). This market evolution reflects the successful fusion of modern processing techniques with Mexico's rich culinary heritage, encouraging manufacturers to invest in sophisticated technologies that preserve traditional flavor profiles while ensuring regulatory compliance. In the market segments, beverages maintained their dominant position with the largest share in 2024, while the dynamic savory snacks category emerged as the fastest-growing segment. This growth is particularly driven by innovative flavor combinations, such as chili-fruit and sweet-heat profiles, which strongly resonate with the younger consumer demographic. The implementation of NOM-051 front-of-pack labeling requirements has fundamentally transformed product formulations, with manufacturers increasingly incorporating natural ingredients, including plant-based enhancers and botanical extracts, as part of their strategic initiatives to develop products with reduced salt, sugar, and fat content [1]Source: International Trade Administration, “Mexico Front of Package Labeling,” trade.gov.

Key Report Takeaways

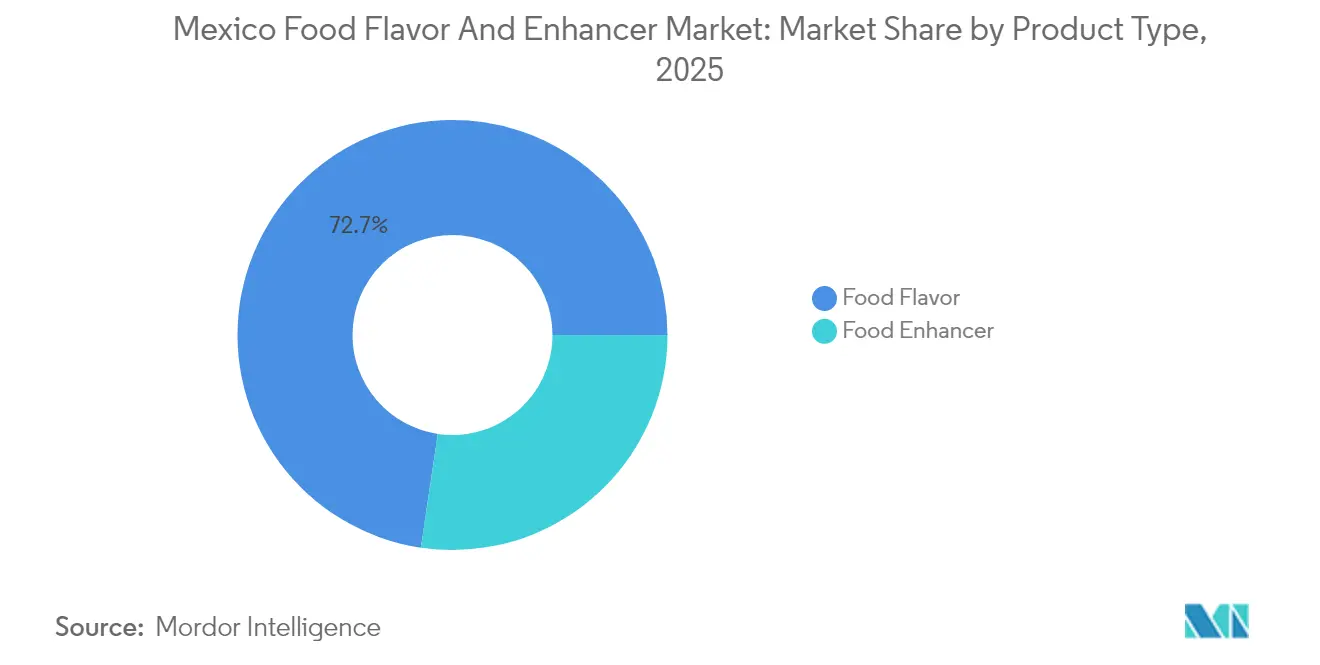

- By product type, food flavors captured 72.65% of the Mexico Food Flavors And Enhancers Market share in 2025.Food enhancers are forecast to post the fastest 6.66% CAGR through 2031.

- By type, synthetic solutions retained 56.70% share of the Mexico Food Flavors And Enhancers Market size in 2025, while natural variants are poised to advance at a 6.37% CAGR.

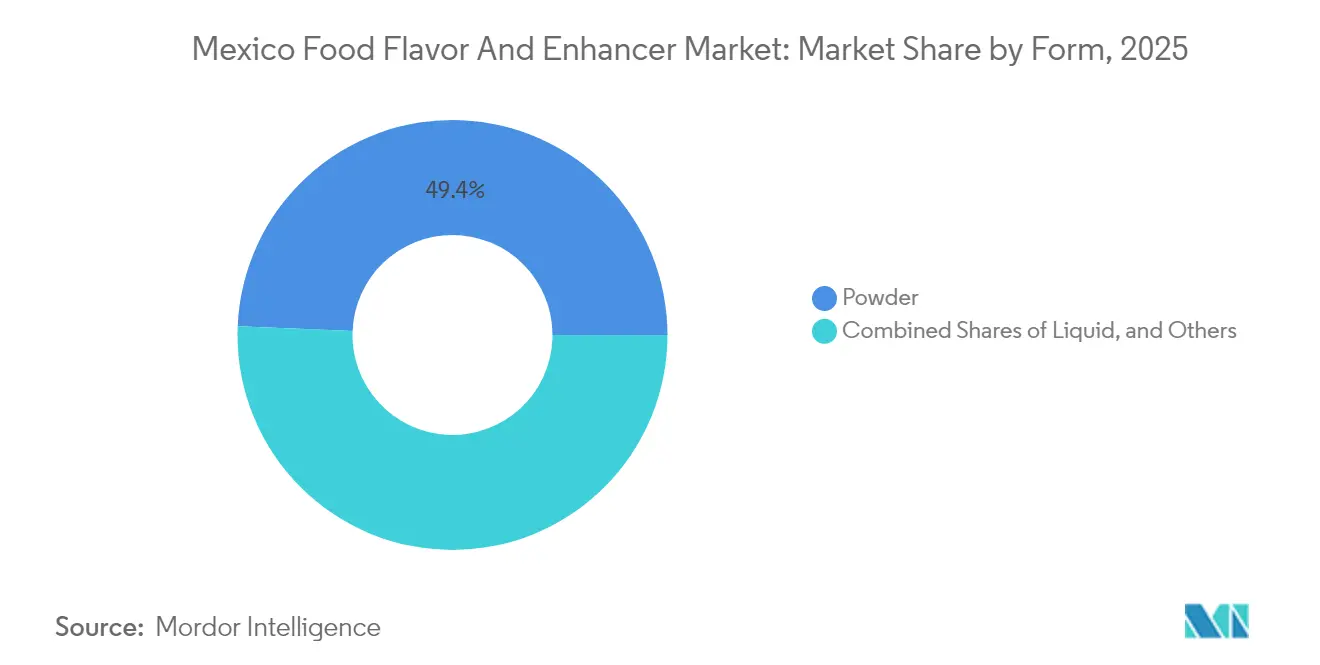

- By form, powders dominated with 49.35% share of the Mexico Food Flavors And Enhancers Market size in 2025; liquids will expand at a 6.55% CAGR to 2031.

- By application, beverages led with 42.90% revenue share in 2025, whereas savory snacks are projected to grow at a 6.62% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Food Flavors And Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in processed and convenience food consumption | +1.8% | National; urban centers | Medium term (2-4 years) |

| Rising consumer preference for clean-label and natural ingredients | +1.5% | National; high-income metros | Long term (≥ 4 years) |

| Expansion of premium and gourmet food products | +1.2% | Mexico City, Guadalajara, tourist corridors | Medium term (2-4 years) |

| Growing demand for plant-based and functional flavors | +1.0% | Urban centers; secondary cities | Long term (≥ 4 years) |

| Development of ethnic and international fusion flavors | +0.8% | National; border states | Short term (≤ 2 years) |

| Increasing interest in sustainability and sustainable sourcing | +0.6% | National; multinational manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Processed and Convenience Food Consumption

The Mexican processed food industry is undergoing significant transformation as urban consumers increasingly seek convenient food options. With more than 80% of the population living in urban areas, the market has experienced substantial growth in ready-to-eat meals, packaged snacks, and shelf-stable products, creating a robust demand for sophisticated flavor systems. This market evolution has attracted major investments from global food manufacturers, with Nestlé investing USD 1 billion in four Mexican facilities to create an export hub, while Unilever commits USD 1.5 billion to a new Nuevo León facility for beauty and personal care products with food applications potential. Combined with PepsiCo's contribution, total planned investments exceed USD 2.5 billion through 2027. The industry operates under COFEPRIS regulations, specifically NOM-251-SSA1-2009 hygiene standards, which maintain quality while facilitating growth. As Latin America's second-largest food processing market, Mexico imported USD 51 billion in food ingredients in 2023, with 63% from the U.S., spanning processed meat, dairy, baking, and confectionery sectors. The market also reflects growing consumer interest in healthier options, including plant-based, protein-rich, and fortified products [2]Source: United States Department of Agriculture, “Mexico: Food Processing Ingredients Annual,” fas.usda.gov.

Rising Consumer Preference for Clean-Label and Natural Ingredients

Mexican consumers have shown a significant shift toward products with transparent labeling and natural formulations, primarily influenced by growing health awareness and the implementation of NOM-051 front-of-pack warning labels in October 2020. Under these regulations, manufacturers must display prominent black octagonal warning stamps on products that exceed established thresholds for calories, added sugars, sodium, trans fats, and saturated fats. This regulatory framework has created substantial market opportunities for natural flavor enhancers, salt-reduction technologies, and sugar-masking solutions. Recognizing this market evolution, Bell Flavors & Fragrances strategically acquired EIGSA in Guadalajara to better serve Mexican consumers' increasing demand for natural ingredients. In a parallel development, Symrise has responded to the market needs by expanding its flavor enhancer portfolio, with particular emphasis on sweetener enhancement and fat-reduction technologies, enabling manufacturers to meet their product reformulation requirements.

Expansion of Premium and Gourmet Food Products

Mexico's expanding middle class and rising disposable income in urban areas drive premium product trends across food categories. The country's position as a major producer of agave and specialty crops enables flavor innovation opportunities, with traditional ingredients like hibiscus, tamarind, and various chili varieties gaining global recognition. Kerry Group's 2025 Taste Charts identify Mexican flavor profiles, including adobo-smoke combinations and regional spice applications, as emerging trends for premium product development. Givaudan's November 2024 expansion of its Pedro Escobedo facility, which doubled its encapsulation technology capacity, enables the company to serve premium applications requiring advanced delivery systems. Mexican traditional foods, including concha (sweet bread), café de olla (spiced coffee), and salsa negra, are moving from foodservice to retail applications, creating opportunities for flavor systems that deliver authentic taste profiles in packaged formats.

Growing Demand for Plant-Based and Functional Flavors

The Mexican plant-based market continues to experience significant growth, driven by increasing consumer awareness of health benefits and environmental impact. Recent market analysis reveals a substantial shift in consumer behavior, with 54% of Mexican consumers actively incorporating plant-based alternatives into their diets as replacements for animal protein. At the forefront of this transformation is NotCo, whose Mexico headquarters houses the innovative AI platform Giuseppe. This advanced system performs detailed molecular analysis and precise plant ingredient matching to enhance the sensory attributes of plant-based products. The company's successful integration into mainstream food service is evidenced by its strategic partnerships with major restaurant chains including Chili's, Starbucks, and Papa John's. The market's evolution is further supported by the incorporation of traditional Mexican ingredients, such as agave fructans, nopal mucilage, and fermented corn-based matrices. These ingredients serve multiple functions, offering prebiotic benefits, improved texture characteristics, and natural preservation capabilities that align with the growing demand for clean-label products. The development and implementation of these functional ingredients strictly follow NOM-251-SSA1-2009 hygiene standards, ensuring the highest levels of product safety and quality in the Mexican market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.8% | National, with concentrated enforcement in major manufacturing hubs | Short term (≤ 2 years) |

| Supply chain disruptions related to seasonal and geopolitical factors | -1.2% | National, with particular impact on border states and agricultural regions | Medium term (2-4 years) |

| Health concerns related to certain flavor enhancer | -0.6% | National, with heightened scrutiny in urban consumer markets | Long term (≥ 4 years) |

| Trade restrictions and tariffs impacting import/export of ingredients | -0.9% | Border states and major ports, affecting cross-border supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety and Labeling Regulations

Mexico's regulatory framework, primarily through COFEPRIS, establishes strict compliance requirements for flavor and enhancer suppliers. The NOM-251-SSA1-2009 regulation requires extensive documentation, traceability systems, and facility standards, necessitating substantial investments in quality management systems. NOM-051's front-of-pack warning label requirements affect product formulations, as items exceeding specified nutrient thresholds face marketing limitations and potential consumer resistance. Import regulations require specific certifications and documentation, with COFEPRIS retaining the authority to conduct compliance sampling and verification, which can result in delays and additional costs. The control of drug precursors has affected the import of certain flavor production raw materials, extending lead times and increasing compliance expenses. These regulations provide competitive advantages to established suppliers with comprehensive quality systems and may encourage market consolidation toward larger companies capable of meeting regulatory requirements.

Supply Chain Disruptions Related to Seasonal and Geopolitical Factors

Mexico's agricultural supply chains experience persistent challenges that affect raw material availability for flavor and enhancer production. These challenges include weather volatility, cross-border logistics constraints, and commodity price fluctuations. The 2023 drought conditions reduced bean production by 56%, necessitating record imports and demonstrating the vulnerability to climate variations. Rail permit suspensions and congestion have disrupted Mexico-US agricultural trade, with monthly grain shipment reductions exceeding 1.188 million tonnes, affecting feedstock availability for corn-derived ingredients and starches used in flavor applications. The country's annual yellow corn imports of 14-16 million tonnes create dependence on US suppliers, while transportation bottlenecks and trade policy uncertainties introduce supply risks for corn-based flavor carriers and sweeteners. The implementation of USMCA and potential trade disputes over GMO corn policies create regulatory uncertainty, affecting long-term supply planning and ingredient sourcing strategies [3]Source: The National Agricultural Law Center “U.S.-Mexico Trade Dispute,” nationalaglawcenter.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Flavors Dominate Despite Enhancer Growth Acceleration

Mexico's food processing industry continues to rely heavily on food flavors, which currently account for 72.65% of the market share in 2025. These flavors play a vital role across various product categories, including beverages, bakery items, confectionery, and savory foods. The segment's strength comes from its well-established relationships with major manufacturers and the deep application knowledge built over many years in the market.

Food enhancers are emerging as a significant growth segment, with a projected CAGR of 6.66% through 2031. This growth is driven by the industry's need to comply with NOM-051 labeling requirements and increasing consumer demand for reduced sugar, salt, and fat content. Companies like Symrise have responded by expanding their enhancer portfolios to include sweetener and salt-reduction solutions. The segment is particularly important in the plant-based market, where manufacturers need effective taste masking and texture modification solutions. While traditional food categories maintain their reliance on conventional flavors, the industry is steadily moving toward enhancers for functional foods and clean-label reformulations, reflecting Mexico's evolving food processing landscape.

By Type: Synthetic Solutions Lead While Natural Variants Accelerate

The Mexican food flavors market is experiencing a significant shift in dynamics, with synthetic flavors commanding a substantial 56.70% market share in 2025. This dominance is underpinned by their practical advantages, including lower production costs, reliable supply chains, and well-established regulatory frameworks that enable efficient large-scale food manufacturing. The stability, precise dosage control, and concentrated flavor profiles of synthetic ingredients make them particularly valuable for Mexico's extensive food processing industry, where major companies like Nestlé, PepsiCo, and Unilever depend on them for operational efficiency.

In contrast, the natural flavors segment is emerging as a dynamic force in the market, achieving a notable growth rate of 6.37% CAGR. This growth is primarily fueled by evolving consumer preferences, as more shoppers actively seek products with recognizable, natural ingredients. Additionally, the implementation of front-of-pack warning label regulations has created a stronger incentive for manufacturers to enhance their ingredient transparency, further supporting the expansion of natural flavor applications in the Mexican market.

By Form: Powder Applications Dominate Despite Liquid Innovation

Mexico's flavor market shows a clear preference for powder forms, which currently command a 49.35% market share in 2025. This dominance stems from practical advantages that resonate with manufacturers - better storage stability, cost-effective transportation, and adaptability across various food applications. Food producers particularly value powder flavors for their dry mix products, including seasonings, snack coatings, and instant beverages, which cater to both domestic consumption and export opportunities.

The liquid flavor segment is experiencing robust growth at 6.55% CAGR, primarily fueled by Mexico's thriving beverage industry. This growth has prompted strategic investments, as evidenced by Givaudan's recent expansion at their Pedro Escobedo facility. By doubling their encapsulation technology capacity, the company has positioned itself to meet the increasing demand from beverage manufacturers while strengthening its export capabilities. The stability of powder forms proves especially valuable given Mexico's diverse climate conditions and logistical challenges, offering manufacturers tangible benefits through reduced shipping costs and extended product shelf life.

By Application: Beverages Lead While Savory Snacks Drive Growth

Mexico's beverage sector dominates the market with a 42.90% share in 2025, highlighting the country's strength as a manufacturing powerhouse for both domestic consumption and exports. The industry thrives on robust infrastructure, with companies like Coca-Cola FEMSA operating extensively alongside a flourishing craft beverage market and traditional drink categories such as aguas frescas and flavored waters, all requiring sophisticated flavor solutions.

The market presents substantial opportunities for flavor suppliers across various beverage categories, particularly with major manufacturers increasing their investments. Nestlé's USD 1 billion expansion program exemplifies this trend, creating demand across carbonated soft drinks, juices, energy drinks, and functional beverages. In parallel, the savory snacks segment shows remarkable potential with a 6.62% CAGR, as urban consumers embrace new consumption patterns and manufacturers innovate with traditional Mexican flavors in modern snack formats.

Competitive Landscape

The Mexico Food Flavors And Enhancers Market demonstrates moderate concentration, characterized by a balanced competitive landscape between established global entities and specialized regional suppliers. The market's leading segment comprises companies with robust local manufacturing capabilities, comprehensive regulatory expertise, and sophisticated application development resources specifically tailored to Mexican consumer preferences. Major international players including Givaudan, IFF, Kerry Group, and Symrise have established dominant positions through strategic direct operations, targeted acquisitions, and substantial technology investments, showcasing their long-term commitment to the Mexican market.

The fastest-growing segment in the market centers around companies pursuing aggressive vertical integration strategies, expanding local production facilities, and implementing technology-driven differentiation to address evolving regulatory requirements and consumer trends. This growth is exemplified by Givaudan's significant expansion of its Pedro Escobedo facility, which doubled encapsulation technology capacity while maintaining 40% of global delivery systems production at the Mexican site. Similarly, Bell Flavors & Fragrances' strategic acquisition of EIGSA in Guadalajara and Symrise's substantial investment in its Querétaro plant demonstrate the increasing importance of local production capabilities and technical expertise.

Other market segments present diverse opportunities, particularly in specialized applications such as plant-based flavor systems, traditional Mexican ingredient development, and sustainable sourcing programs. These segments align closely with multinational manufacturers' ESG requirements and evolving consumer preferences. The expanding plant-based market, reaching USD 389.1 million in 2025, has created substantial demand for innovative taste masking and texture modification technologies. Additionally, traditional ingredients, including agave derivatives, nopal extracts, and fermented corn-based systems, offer significant differentiation potential for companies focusing on authentic Mexican flavor profiles.

Mexico Food Flavors And Enhancers Industry Leaders

Givaudan

DSM-Firmenich

International Flavors & Fragrances (IFF)

Kerry Group

Archer Daniels Midland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: IFF announced USD 70 million expansion of Cedar Rapids, Iowa facility to produce TAURA fruit-based ingredients for healthy snacks market, expected fully operational H2 2026, creating supply chain implications for Mexican food manufacturers importing clean-label fruit ingredients.

- January 2025: Kerry Group launched 2025 Taste Charts featuring Mexico-specific flavor filters and regional trend analysis, highlighting adobo-smoke fusion concepts and traditional Mexican flavor applications for product development and market positioning strategies.

- November 2024: Givaudan inaugurated expanded production facility in Pedro Escobedo, Mexico, doubling encapsulation technology capacity to represent 40% of global delivery systems production, supporting growing Latin American demand and reinforcing operational excellence in fragrance and beauty applications with potential food crossover technologies.

Mexico Food Flavors And Enhancers Market Report Scope

Mexico Food Flavors And Enhancers Market is segmented by type that includes flavors and flavor enhancers. The flavor section is further segmented into natural flavors, synthetic flavors and nature identical flavors. Based on Application, the market is segmented into bakery, confectionery, dairy, beverages, processed food, and others.

By Product Type

| Food Flavor |

| Food Enhancer |

By Type

| Natural |

| Synthetic |

| Nature Identical |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

| By Product Type | Food Flavor |

| Food Enhancer | |

| By Type | Natural |

| Synthetic | |

| Nature Identical | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snack | |

| Meat | |

| Beverage | |

| Other Applications |

Key Questions Answered in the Report

How large is the Mexico Food Flavors And Enhancers Market in 2026?

Market size is USD 704.09 million in 2026, projected to hit USD 929.21 million by 2031.

Which application consumes the most flavors in Mexico?

Beverages lead with 42.90% revenue share in 2025.

What is driving natural flavor demand?

NOM-051 warning labels and consumer preference for clean-label products propel natural variants at a 6.37% CAGR.

Which segment is growing fastest?

Savory snacks show the highest 6.62% CAGR, fueled by chili-fruit fusion profiles.

Who are key players in the market?

Givaudan, IFF, Kerry Group, Symrise, and Bell Flavors & Fragrances hold the largest shares.

Page last updated on: