Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

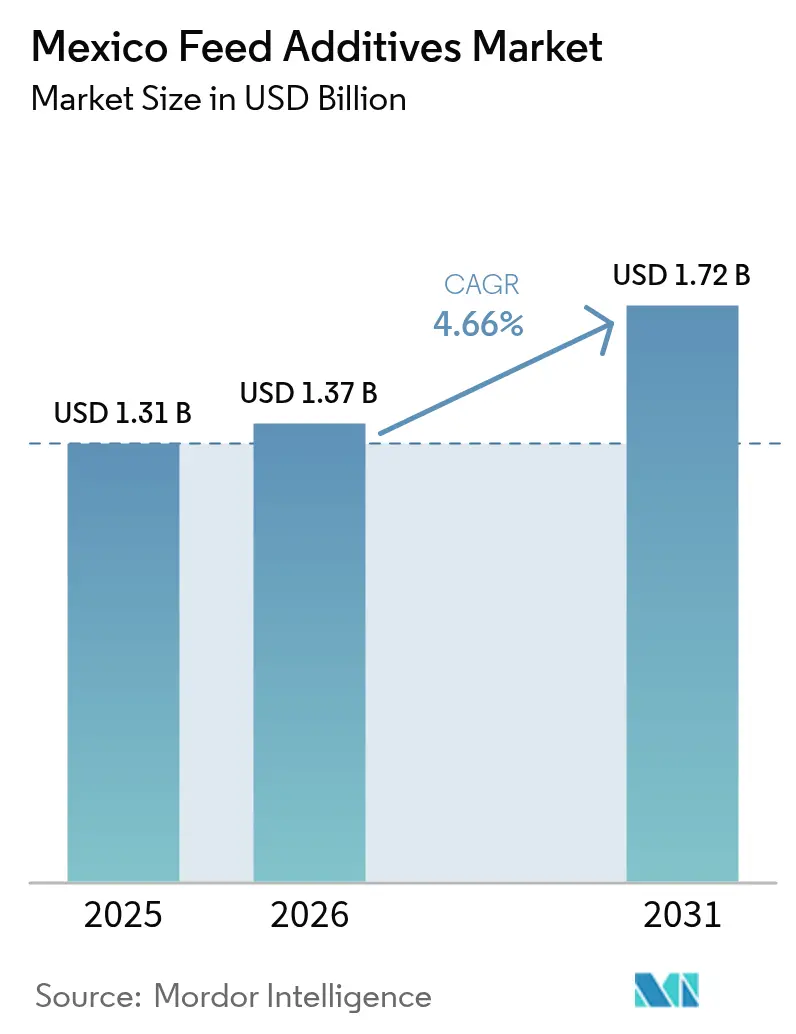

| Base Year Market Size (2025) | USD 1.31 Billion |

| Market Size (2026) | USD 1.37 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

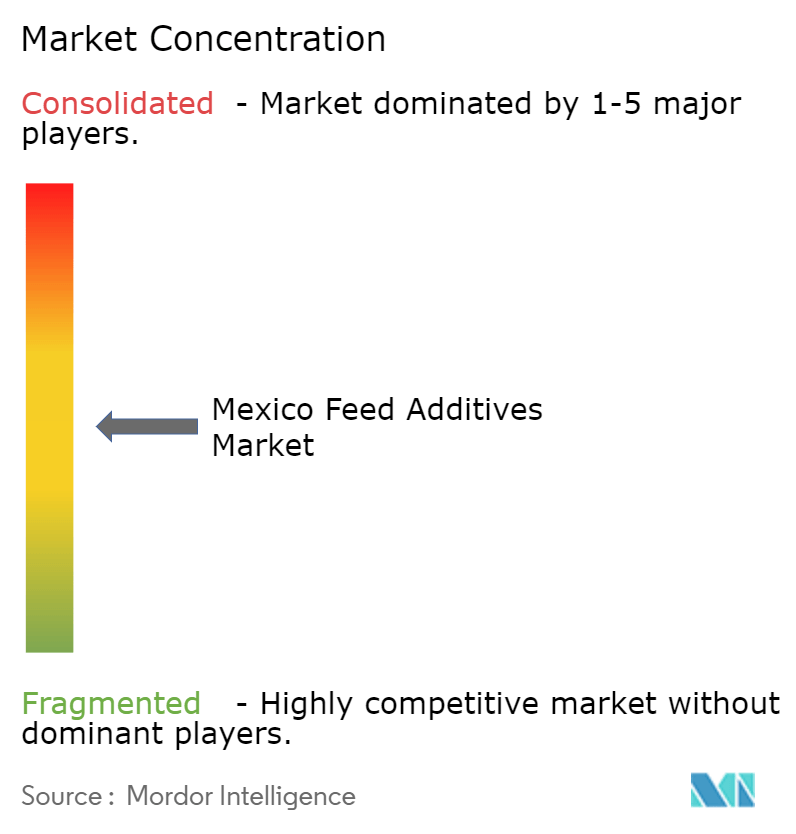

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Feed Additives Market Analysis by Mordor Intelligence

The Mexico feed additives market size is expected to grow from USD 1.31 billion in 2025 to USD 1.37 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at 4.66% CAGR over 2026-2031. Mexico's position as the sixth-largest poultry producer globally, along with its 620 feed mills processing 41.4 million metric tons of compound feed annually in 2024, contributes to the market growth, according to the National Feed Council (Conafab). The increasing consumer demand for affordable animal protein further supports market expansion. With feed costs representing 60-75% of poultry production expenses, producers are adopting additives to improve feed conversion efficiency and reduce disease risks. The implementation of NOM-012-SAG/ZOO-2020 regulations has increased the demand for scientifically validated formulations by mandating traceability and quality controls. International suppliers benefit from Mexico's proximity to North American grain supplies, offering technical support, local manufacturing, and nutrition services. The market growth is further supported by government initiatives through Trust Funds for Rural Development and tax incentives for sustainable inputs, which encourage investment in automated mills and micro-dosing equipment, despite fluctuating raw material prices.

Key Report Takeaways

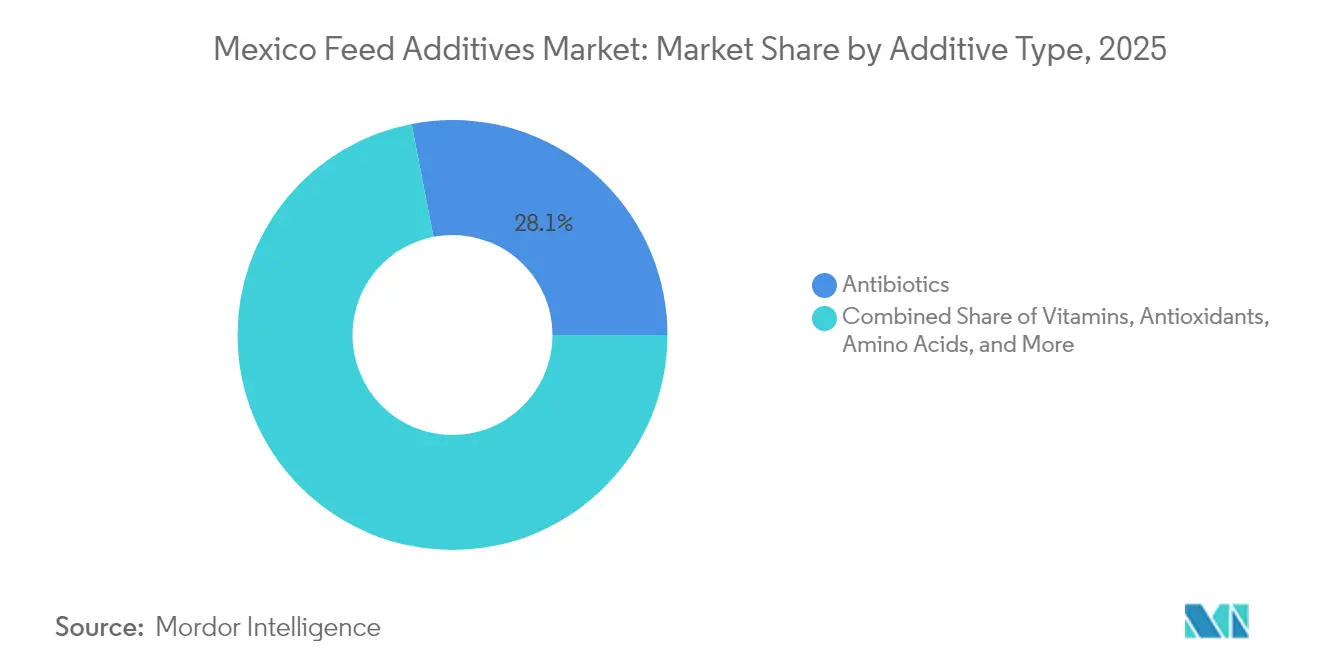

- By additive type, antibiotics led with 28.05% of the Mexico feed additives market share in 2025, while probiotics are forecast to expand at a 7.18% CAGR to 2031.

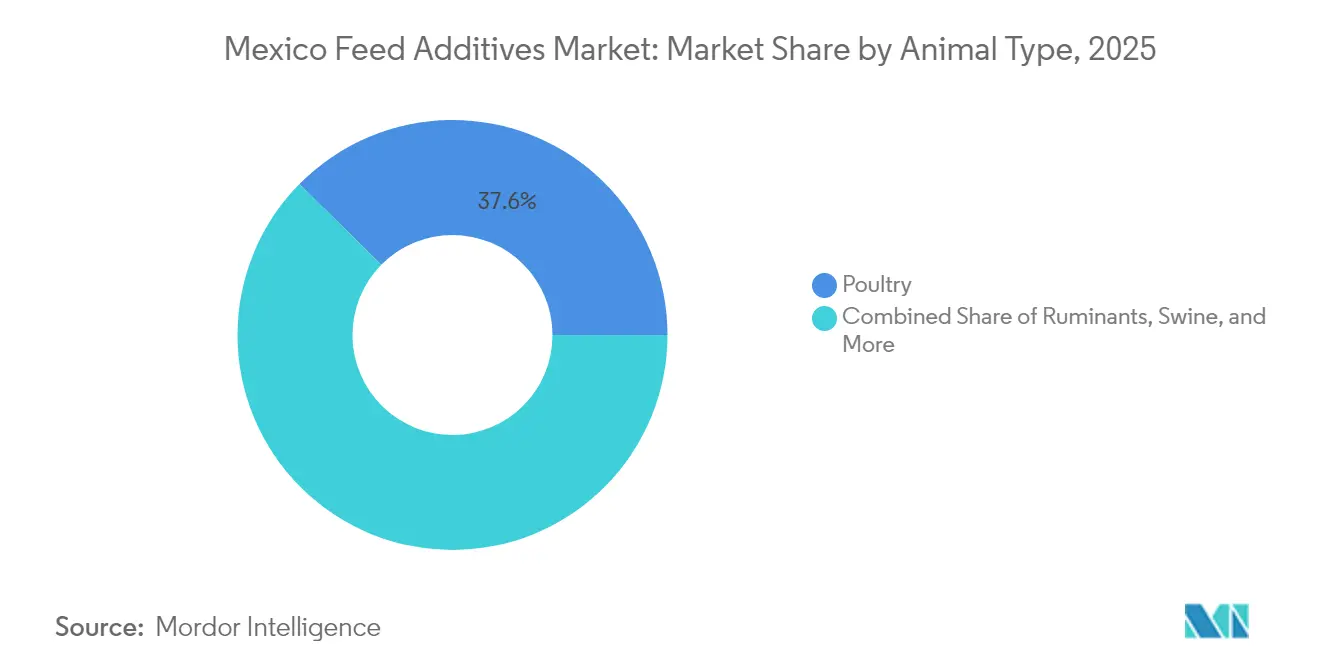

- By animal type, poultry accounted for 37.62% of the Mexico feed additives market size in 2025, and aquaculture is advancing at an 8.49% CAGR through 2031.

- The market is moderately fragmented, with the top five companies, Cargill, Incorporated, DSM-Firmenich AG, ADM (Archer Daniels Midland Company), BASF SE, and Evonik Industries AG collectively holding the majority of the market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Feed Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Industrial livestock and compound-feed output | +1.1% | Jalisco, Sonora, and Veracruz | Medium term (2–4 years) |

| Expanding commercial poultry integration footprint | +0.7% | Jalisco, Puebla, and Yucatan | Short term (≤ 2 years) |

| Rising consumer preference for high-protein diets | +0.6% | Urban centers nationwide | Long term (≥ 4 years) |

| Feed-mill automation and precision-nutrition adoption | +0.5% | Major mills in Jalisco and Estado de Mexico | Medium term (2–4 years) |

| Government tax incentives for sustainable feed inputs | +0.2% | Drought-affected regions nationwide | Long term (≥ 4 years) |

| Blockchain-based supply-chain traceability mandates | +0.1% | Export-oriented operations nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Industrial Livestock and Compound-Feed Output

Mexico's cattle population is projected to reach 8.7 million heads by 2025, while poultry production is projected to achieve 4.1 million metric tons[1]Source: USDA Foreign Agricultural Service, “Livestock and Poultry: World Markets and Trade,” usda.gov. Large-scale confined operations focus on feed efficiency to address increasing grain prices, which drives demand for amino acids, enzymes, and gut-health additives. The Service for National Health, Food Safety, and Food Quality (SENASICA) has implemented stricter oversight and blockchain traceability requirements, compelling producers to adopt branded, data-validated products that ensure regulatory compliance and export market access. Multinational suppliers with established technical support and analytics capabilities are well-positioned to capitalize on this industry transformation.

Expanding Commercial Poultry Integration Footprint

Vertical integrators such as Granjas Carroll generate annual economic impacts of MXN 1.325 billion (USD 66 million) in Veracruz in 2024. The integrated model enables standardized nutrition across farms, creating consistent demand for feed additives, including vitamins, enzymes, and probiotics. The adoption of automated micro-dosing systems reduces waste and tracks feed conversion improvements, enabling premium pricing for additives and facilitating antibiotic-replacement programs. Export-focused integrators prioritize food safety additives to comply with international market standards. The regional clusters in Jalisco, Puebla, and Yucatan leverage shared infrastructure and technical knowledge to increase innovation adoption.

Rising Consumer Preference for High-Protein Diets

Mexico's total meat consumption is anticipated to reach 82.5 kg per capita by 2033, with poultry and pork leading this growth[2]Source: USDA Economic Research Service, “Meat Consumption in Mexico,” ers.usda.gov. Middle-class consumers are willing to pay higher prices for antibiotic-free chicken and traceable seafood. This consumer preference has encouraged producers to implement probiotic blends, phytogenics, and mycotoxin detoxifiers to support clean-label products. Aquaculture has become an important protein source, particularly shrimp production in Sonora and Sinaloa states, which requires specific additives for marine conditions. The increasing demand for organic and antibiotic-free products has created market opportunities for alternative feed additives, including probiotics, prebiotics, and plant-based ingredients.

Feed-Mill Automation and Precision-Nutrition Adoption

Grupo Nutec's premix plant near Querétaro demonstrates modern feed manufacturing capabilities with its 2 million metric tons annual capacity, utilizing automated dosing and near-infrared spectroscopy. The facility implements data-driven ration design to customize micronutrient profiles according to species and lifecycle requirements, enhancing the absorption of high-potency vitamin packs and specialty enzymes that reduce phosphorus excretion. Quality control and batch consistency are improved through near-infrared spectroscopy and automated sampling systems. The implementation of IoT sensors and data analytics platforms enables continuous monitoring of feed performance through measurable biomarkers. To maintain competitiveness, smaller mills are increasingly outsourcing formulation services or establishing partnerships with feed additives suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw material prices | −0.9% | Import-dependent regions nationwide | Short term (≤ 2 years) |

| Challenging government regulations | −0.6% | Export zones with strict inspection regimes | Medium term (2–4 years) |

| Limited cold-chain logistics for liquid additives | −0.4% | Rural and remote areas | Long term (≥ 4 years) |

| High capital costs for on-farm micro-dosing equipment | −0.3% | Small and mid-scale operations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

Mexico's corn imports are projected to reach 22 million metric tons in 2024-2025, exposing feed mills to international price variations and currency exchange risks[3]Source: USDA Foreign Agricultural Service, “Mexico: Grain and Feed Annual,” fas.usda.gov. The limited profit margins restrict spending on premium additives, leading buyers to seek volume discounts or postpone new product adoption. With drought affecting the majority of municipalities, domestic grain production faces constraints, increasing vulnerability to external market forces. The peso-dollar exchange rate volatility creates additional cost uncertainties for companies importing additives. In response, feed mills prioritize additives that demonstrate clear financial benefits through enhanced feed conversion ratios or lower veterinary expenses.

Challenging Government Regulations

The implementation of NOM-012-SAG/ZOO-2020 in May 2024 introduced registration and traceability requirements for feed additives, creating compliance costs and market entry barriers. The Service for the National Health for Food Safety and Food Quality's import consultation modules require documentation for each additive category, extending approval timelines and increasing administrative burden. Small Mexican firms face challenges with documentation requirements, leading to market consolidation favoring large multinational companies. Export-oriented producers must comply with both the United States and European regulations, increasing the cost of maintaining additive production lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Antibiotics Sustain Leadership and Probiotics Set the Pace

Antibiotics hold 28.05% of the Mexico feed additives market share in 2025, maintaining their significant role in therapeutic programs despite increasing regulatory oversight. Large-scale poultry and swine operations continue to use preventive treatments for necrotic enteritis and respiratory infections. Stricter withdrawal requirements and consumer concerns are driving formulators to optimize dosage protocols and incorporate enzymes or organic acids to decrease antibiotic usage. Vitamins, amino acids, and enzymes show consistent growth as automated feed mills enable precise dosing, while mycotoxin detoxifiers remain crucial for feed preservation in Mexico's humid storage conditions.

Probiotics emerge as the fastest-growing segment with a 7.18% CAGR through 2031, supported by proven Bacillus subtilis strains that improve gut health in poultry, swine, and shrimp. In 2024, partnerships with the Center for Scientific Research and Higher Education (CICESE) and the Autonomous University of Nuevo León (UANL) developed region-specific strains for high-salinity aquaculture and high-density broiler production. Combined enzyme-probiotic products gain market acceptance as integrated solutions that enhance digestibility, reduce pathogens, and support antibiotic-free production claims. The demand for carotenoids and phytogenic pigments increases in shrimp hatcheries targeting export markets, indicating growth opportunities in feed additives.

By Animal Type: Poultry Dominance Meets Aquaculture Innovation

Poultry accounts for 37.62% of the Mexico feed additives market in 2025. Mexico's status as the world's sixth-largest poultry producer and the projected consumption increase to 43.8 kilograms per capita by 2033 support this dominance. The segment's growth stems from vertical integration and export market expansion, increasing the demand for additives that enhance feed conversion ratios. The swine segment holds the second-largest market share, with production primarily in regions including Veracruz, where integrated operations maximize additive usage throughout production cycles.

The aquaculture segment is projected to grow at 8.49% CAGR through 2031, with major operations in Sonora and Sinaloa states producing 177,000 metric tons of shrimp annually. The ruminant segment maintains a consistent demand for feed additives focused on methane reduction and milk production enhancement. The other animal types segment, comprising pets and equine, represents a smaller market share but shows growth through premium product adoption and specific nutritional needs.

Geography Analysis

Jalisco leads Mexico's feed additives market through its concentrated poultry integration, modern feed-mill infrastructure, and strategic location near Guadalajara's logistics corridors. The region's network of over 80 commercial mills facilitates the quick implementation of new additive technologies, supported by nutritionists and diagnostic laboratories. The area's academic institutions provide a skilled workforce and research partnerships, establishing Jalisco as the primary innovation center for poultry nutrition solutions that improve feed conversion and decrease antibiotic usage. Its central location to major consumption areas reduces transportation costs, enabling broader adoption of specialty products.

Sonora and Sinaloa generate the majority of Mexico's shrimp production, driving the demand for aquaculture-specific additives. The coastal hatcheries require specialized probiotic formulations that function in 35-40 ppt salinity conditions and carotenoids for color enhancement. Biofloc systems require immune modulators to minimize antibiotic use. The cold-chain transport infrastructure from Guaymas and Mazatlán ports supports temperature-controlled additive distribution, though remote pond locations face distribution challenges for liquid feed additives.

Veracruz, Estado de Mexico, and northern border states complete the market landscape. Veracruz's high humidity increases mycotoxin risks, necessitating antioxidant and detoxifier use despite moderate market growth. Feed mills in the Estado de Mexico utilize highway and rail connections to Mexico City's consumer market, enabling efficient additive delivery to intensive layer and broiler operations. In Chihuahua and other northern states, government subsidies for concentrate feed encourage small-scale cattle and goat farmers to adopt balanced mineral and vitamin supplements for improved weight gain during dry seasons.

Regulatory Landscape

Mexico regulates feed additives under the Federal Animal Health Law (Ley Federal de Sanidad Animal), with SADER overseeing implementation through SENASICA. In practice, market entry and day-to-day commercialization depend on SENASICA registration or authorization, dossier-based verification (including chemical and microbiological specifications), and compliance with official traceability and quality-control expectations for products intended for animal use or consumption.

NOM-012-SAG/ZOO-2020 is the key anchor, as it replaced NOM-012-ZOO-1993 and entered into full force on May 4, 2024. The regulation sets technical specifications for production, storage, distribution, marketing, and quality control, with additional provisions linked to updated labeling requirements scheduled for November 2025. Imports also require meeting SENASICA zoosanitary requirement sheets (HRZ) through the agency import consultation module, while related standards such as NOM-060-SAG/ZOO-2020 govern zoosanitary specifications for animal by-products used in feed. SENASICA residue-control oversight further shapes additive selection and documentation across livestock value chains.

Competitive Landscape

The Mexico feed additives market shows moderate fragmentation, with five major companies - Cargill, Incorporated, DSM-Firmenich AG, ADM (Archer Daniels Midland Company), BASF SE, and Evonik Industries AG holding the majority market share in 2024. Cargill operates 27 facilities across 13 states and integrates digital nutrition platforms to benchmark live performance data. ADM operates a USD 39 million wet pet food plant in Morelos, demonstrating its specialty ingredient capabilities across livestock segments.

BASF maintains six production sites in Mexico, reducing lead times for organic acids, carotenoids, and surfactants. This infrastructure positions BASF SE as a reliable partner for mills requiring domestic inventory during freight disruptions. In 2024, Novonesis, formed through the merger of Novozymes and Chr. Hansen has expanded its presence in enzymes and probiotics, intensifying competition in digestive efficiency and gut health products.

Local companies, including PiSA Farmacéutica and Grupo Nutec, have established market positions through extensive distribution networks and customized premix solutions that address regional preferences and environmental challenges. Companies now compete by offering integrated services that combine additive supply with feed formulation software, on-farm diagnostics, and blockchain compliance systems.

Mexico Feed Additives Industry Leaders

Cargill, Incorporated

DSM-Firmenich AG

ADM (Archer Daniels Midland Company)

BASF SE

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In Mexico, the clearest near-term opportunity in feed additives is tied to capacity additions in feed and premix that prioritize automation and tighter inclusion control. That shift tends to raise demand for standardized, scientifically validated additive programs that align with NOM-012-SAG/ZOO-2020. Trouw Nutrition’s February 2025 inauguration of the Aguila Project in Colon, Queretaro, is a tangible example, as it launched an automated premix and young animal feed plant supported by an approximately MXN 1 billion investment, which supports local supply and shortens technical-service cycles for vitamins, amino acids, enzymes, and gut-health solutions.

Integrator-led expansion also creates pull-through for performance and biosecurity-focused additive bundles, including enzymes, probiotics, organic acids, mycotoxin management, and hygiene-related solutions, especially where traceability and verification are active operational requirements. In January 2026, Pilgrim’s Pride announced a multi-year USD 1.3 billion investment plan in Mexico for 2026-2030 covering feed-plant and hatchery expansion, reinforcing the role of high-throughput mills as demand hubs for additives. At the industry level, participation channels through bodies such as CONAFAB (including its Grupo Premezclas, Aditivos y Microingredientes), ANFACA, and AMENA support dissemination of formulation practices and compliance know-how, which typically favors suppliers that combine products with documentation, analytics, and on-farm troubleshooting in poultry-dense regions. This is also visible in aquaculture clusters, notably shrimp operations in Sonora and Sinaloa, where sourcing needs include specialized probiotic and pigment solutions.

Recent Industry Developments

- July 2026: ADM received the Hecho en Mexico certification from the Secretariat of Economy for pet food produced at its facilities in Morelos and Guadalajara. The certification supports a localized supply posture for animal nutrition products and related inputs, reinforcing domestic manufacturing credentials in Mexico alongside broader portfolio commercialization efforts.

- February 2026: ADM highlighted its SINCRO intelligent nutrition ecosystem and animal nutrition portfolio for the Mexican market at IPPE. The emphasis on connected nutrition tools signals stronger demand from integrators and feed mills for additive programs that can be validated with performance data and aligned with traceability and quality-control requirements.

- April 2024: Phibro Animal Health signed an agreement to acquire Zoetis' feed additive portfolio, water-soluble products, and related assets for USD 350 million, subject to closing adjustments. The transaction expands Phibro's position in animal health and nutrition, broadening supplier options for feed mills and integrators seeking consolidated additive portfolios and technical support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is the value of feed additives sold for use in animal feed in Mexico, covering the mix of nutrition, performance, and health additives used by feed manufacturers and farms.

Scope exclusions: We exclude on-farm feed raw materials and the broader compound feed value, and we also exclude vitamins or minerals sold for human use.

Segmentation Overview

- By Additive Type

- Antibiotics

- Vitamins

- Antioxidants

- Amino Acids

- Enzymes

- Mycotoxin Detoxifiers

- Prebiotics

- Probiotics

- Flavors and Sweeteners

- Pigments

- Binders

- Minerals

- Other Feed Additives

- By Animal Type

- Ruminants

- Swine

- Poultry

- Aquaculture

- Other Animal Types (pets, Equine, Camel, etc.)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base on livestock output, feed use patterns, and the regulatory and trade setting that influences additive demand in Mexico. We referenced public sources such as FAOSTAT, UN Comtrade, the USDA (including GAIN notes where relevant), and publications from Mexico government bodies such as SIAP and INEGI for production and macro indicators.

To convert these signals into market inputs, we reviewed peer-reviewed animal nutrition journals, customs and tariff schedules, association websites related to feed and livestock, and public company filings and investor materials that explain category trends. In addition, paid subscriptions that support company financials and intelligence, patent landscapes, and shipment-level import and export reads were used selectively to cross-check directional movements and fill gaps. These desk research sources are illustrative only, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the Mexico demand pool and the pricing logic behind key additive groups, since list prices and actual realized prices can differ by channel and species. We interviewed and surveyed stakeholders such as additive suppliers, premix blenders, feed manufacturers, large integrators, distributors, and nutrition professionals. We then re-checked assumptions where interview feedback pointed to a different inclusion of antibiotics alternatives, toxin binders, and biotics.

To capture Mexico-specific formulation behavior, discussions were balanced across poultry, swine, and ruminant feed use so the final numbers reflect where additives are actually consumed, and where inclusion levels are changing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 36% | |

| Smaller Players: 20% | Managers: 50% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where livestock production and feed demand signals are translated into additive consumption pools by species, then mapped to additive intensity levels that were validated through interviews. After the core demand pool is established, pricing is applied using a blended ASP approach that reflects typical product mixes, imported versus locally supplied shares, and the timing of currency conversion used in traded inputs.

To keep totals realistic, results are corroborated with selective bottom-up checks, including sampled supplier revenue bands, channel checks with distributors, and volume x ASP sense checks for high-visibility categories like amino acids, enzymes, and mycotoxin detoxifiers. Key inputs include poultry and swine output trends, compound feed production direction, additive inclusion rates in key rations, imported additive volumes from trade statistics, and observable shifts from antibiotic growth promoters to alternatives. For forecasting, scenario analysis is used so short-term feed cycles and cost shocks can be reflected, followed by expert-led assumptions on adoption rates and price normalization that are applied to the 2026-2031 window.

Data Validation & Update Cycle

Outputs are checked through multiple passes, starting with internal consistency tests across species totals, additive mixes, and implied per-ton usage levels. We then compare the final market value against independent signals such as trade movement, livestock production direction, and known formulation shifts, and we flag any large variance for re-work.

Before sign-off, anomalies are reviewed by another analyst, and follow-up calls are triggered when primary feedback contradicts an assumption that materially changes the value. Reports are refreshed annually, with interim updates when major events occur, and a final pre-delivery review is done so clients receive the latest view available.

Mordor Intelligence's Mexico Feed Additives Market Market Estimate Compared With Other Published Estimates

Published market sizes for Mexico feed additives often look far apart because the term can be interpreted differently across reports, and because pricing and inclusion rules are not always stated clearly. The biggest differences usually come from what is counted as an additive versus a feed ingredient, the year used for currency conversion, and whether the value represents manufacturer-level sales or downstream channel markups.

The main gap comes from whether premixes and adjacent nutrition chemical baskets are rolled into the total. Mordor Intelligence counts only additive categories sold for feed use in Mexico and keeps the value at the additive market level rather than inflating it with full premix and feed value. Differences also appear when one estimate uses aggressive adoption assumptions for biotics and antibiotic alternatives, or when trade-based checks are not used to test whether implied volumes are plausible for Mexico.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.31 B (2025) | |

| Industry Publisher A | USD 0.52 B (2025) | This estimate appears to apply a narrower value scope, which can happen when only selected additive groups are counted or when pricing is taken at a lower ex-factory level without reconciling the full additive mix used across poultry, swine, and ruminants. |

| Consultancy B | USD 0.85 B (2024) | The year difference and the likely treatment of channel margins and category mapping can shift the total, especially if some premix value or broader animal nutrition chemicals are included, and if FX timing is not aligned to the market year. |

Looking across the figures, the spread is best explained by scope and price-building choices rather than by a true disagreement on Mexico livestock demand. By keeping variables traceable to production signals, additive inclusion logic, and repeatable pricing checks, the market size becomes easier to audit and update when conditions change.

Key Questions Answered in the Report

How large is the Mexico feed additives market in 2026?

The Mexico feed additives market size reached USD 1.37 billion in 2026 and is forecast to grow at a 4.66% CAGR through 2031.

Which additive segment leads sales?

Antibiotics hold the largest share at 28.05% of revenue in 2025, driven by their continued therapeutic role despite regulatory tightening.

Which segment is growing fastest?

Probiotics post the quickest growth at a 7.18% CAGR to 2031, supported by clean-label demand and validated Bacillus strains for poultry and aquaculture.

What region drives demand most strongly?

Jalisco dominates due to its dense poultry integration, modern feed-mill network, and proximity to consumption centers.

How are regulations affecting suppliers?

NOM-012-SAG/ZOO-2020 imposes detailed traceability and safety documentation, favoring suppliers with comprehensive dossiers and local technical support.

Page last updated on: