Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

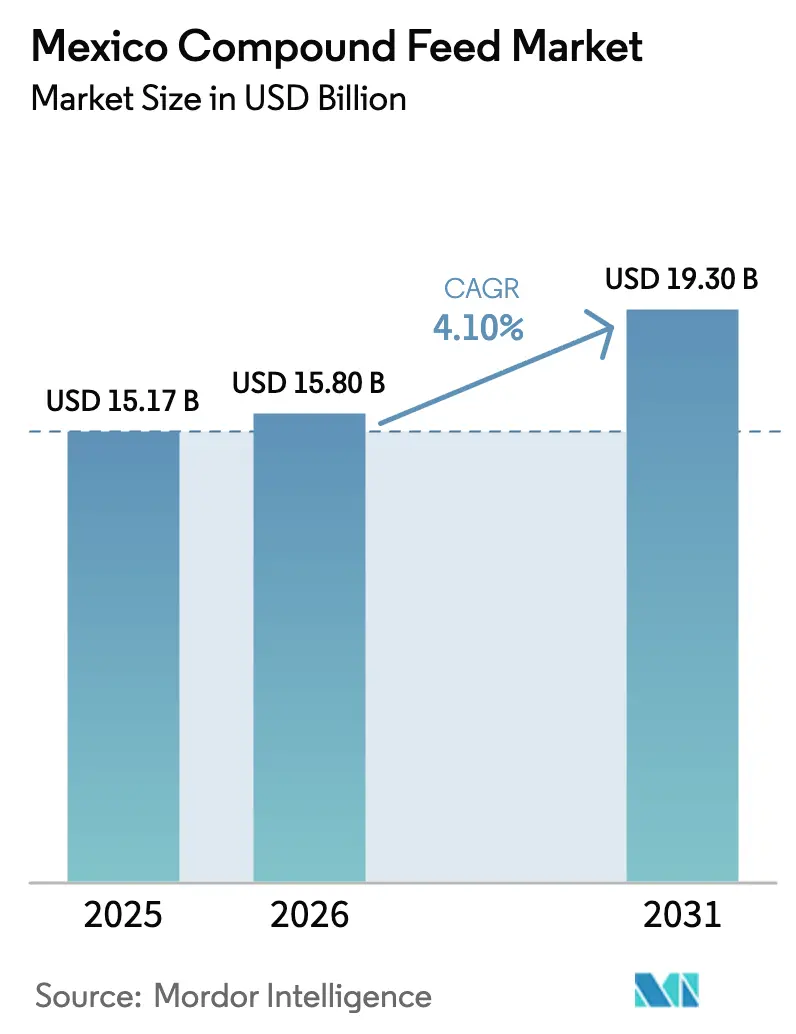

| Base Year Market Size (2025) | USD 15.17 Billion |

| Market Size (2026) | USD 15.80 Billion |

| Market Size (2031) | USD 19.30 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

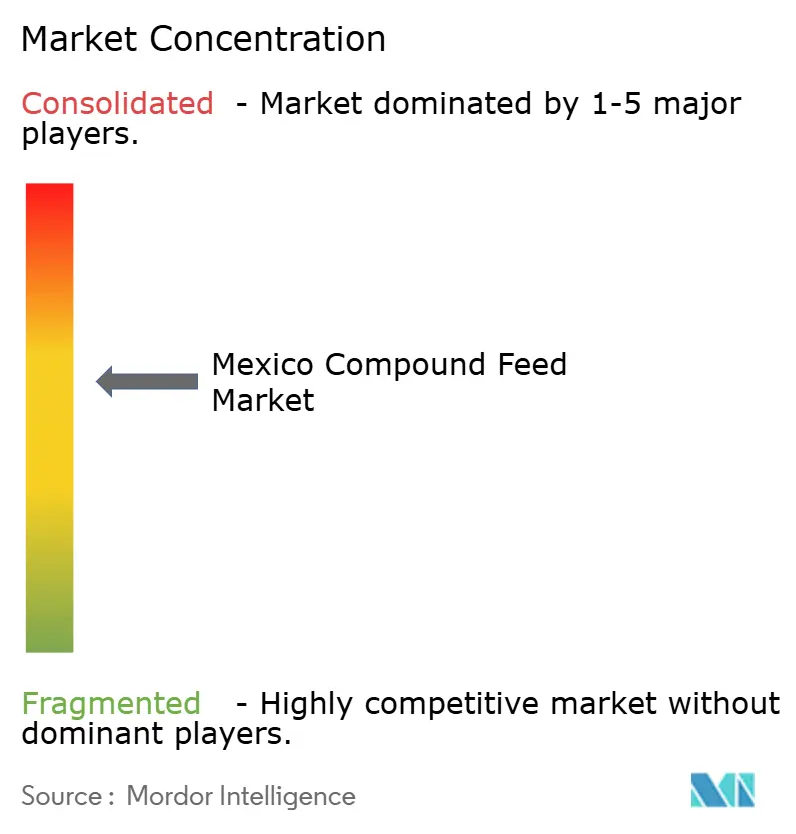

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Compound Feed Market Analysis by Mordor Intelligence

The Mexico compound feed market size is projected to be USD 15.17 billion in 2025, USD 15.80 billion in 2026, and reach USD 19.30 billion by 2031, growing at a CAGR of 4.10% from 2026 to 2031. Volume growth is rooted in Mexico’s status as the world’s fifth-largest feed producer, continued government incentives that reward feed-conversion efficiency, and a nearshoring wave that draws United States meat processors to border states. Tight vertical integration by leading poultry firms links genetics, nutrition, and processing, enabling precision-feeding programs that trim waste and lift margins. Rising aquaculture capacity along both coasts increases demand for specialty extrusion feeds, while digital tools such as Cargill’s Galleon and Evonik’s AMINOSys allow millers to fine-tune formulations in real time. Headline risks include grain-price volatility tied to United States-Mexico-Canada Agreement (USMCA) trade flows, strict mycotoxin rules, and drought-related water caps in northern states.

Key Report Takeaways

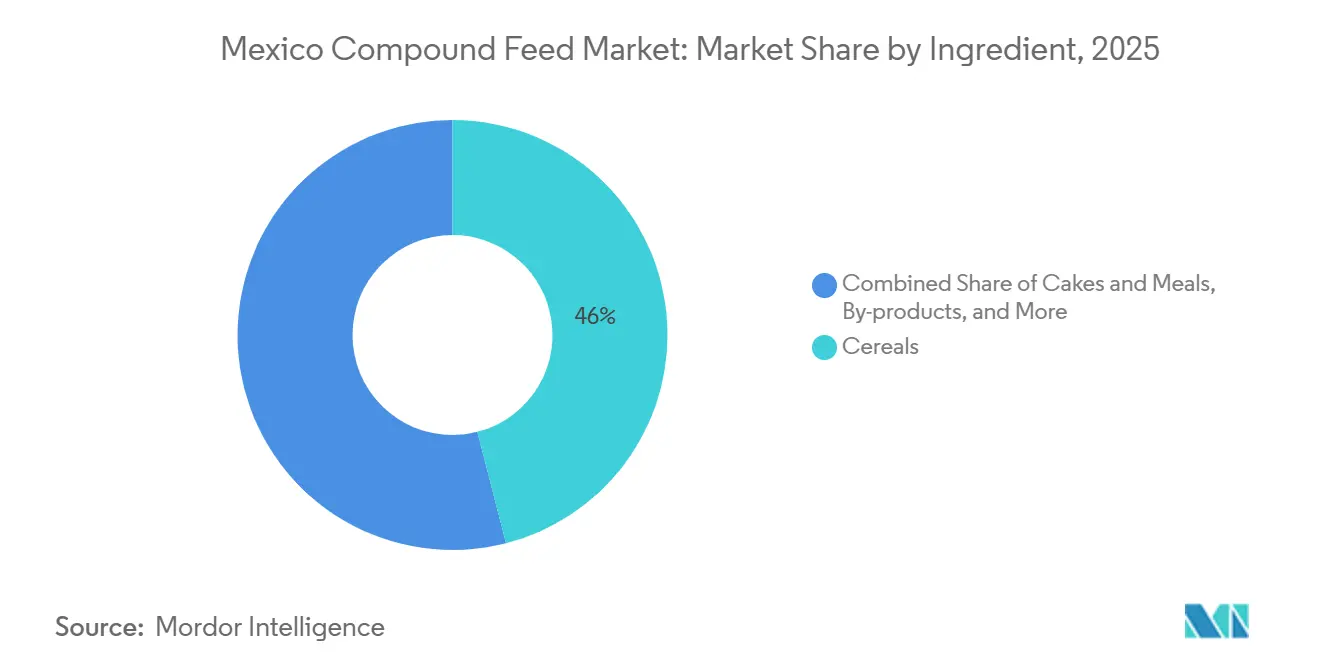

- By ingredient, cereals led with 46.0% revenue share in 2025, while supplements are forecast to expand at a 7.8% CAGR through 2031.

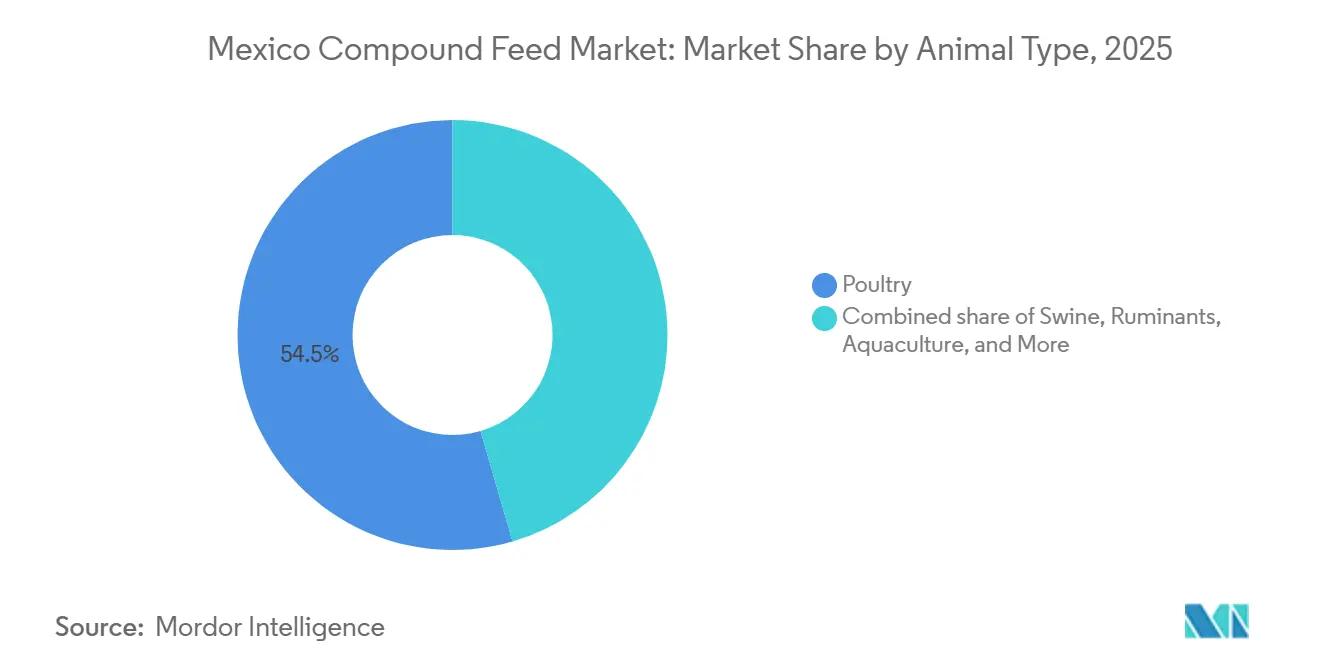

- By animal type, poultry feed captured 54.5% of Mexico compound feed market share in 2025, while aquaculture feed is anticipated to register the fastest growth at an 8.9% CAGR through 2031.

- The five largest suppliers, Cargill, Incorporated, Industrias Bachoco S.A.B. de C.V., Archer Daniels Midland Company, Nutreco N.V. (SHV Holdings N.V.), and Land O’Lakes, Inc., held a majority share in 2025, underscoring a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened demand for value-added animal proteins | +0.8% | National, early gains in Jalisco, Veracruz, Querétaro | Medium term (2-4 years) |

| Expansion of Mexico’s commercial poultry integrators | +1.0% | Jalisco, Veracruz, Aguascalientes, Querétaro | Long term (≥ 4 years) |

| Government's Programa de Fomento a la Productividad Ganadera (PROGAN) - Production subsidies for feed efficiency | +0.5% | Jalisco, Sonora, Puebla, Yucatán | Short term (≤ 2 years) |

| Adoption of precision-feeding and smart-mill technologies | +0.6% | Jalisco, Guanajuato, Querétaro | Medium term (2-4 years) |

| Nearshoring of United States meat processors triggering feed demand | +0.7% | Sonora, Chihuahua, Coahuila, Nuevo León, Tamaulipas | Medium term (2-4 years) |

| Growing aquaculture investments in Pacific and Gulf states | +0.5% | Sinaloa, Sonora, Veracruz, Campeche, Yucatán | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Demand for Value-Added Animal Proteins

Quick-service restaurants and hotels have shifted menus toward higher protein offerings, lifting demand for premium poultry, pork, and seafood. Per-capita meat consumption has shown a significant growth in Mexico, well above the global average and a clear pull for compound feed. Industrias Bachoco’s revenue has recorded a significant growth year on year in 2025, showing how premium meat sales flow back to feed demand. Jalisco, Veracruz, and Querétaro benefit first because dense poultry clusters let millers supply specialized formulas quickly.

Expansion of Mexico’s Commercial Poultry Integrators

Large integrators such as Bachoco run in-house hatcheries, feed mills, and processing plants, locking in margins at every stage. Acquisitions and new breeder farms add capacity, as seen in the MXN 1,100 million (USD 54 million) Yucatán project that cut inter-state egg flows. Scale supports investment in near-infrared analyzers and automated dosing that smaller mills cannot match. Over time, consolidation steers feed demand toward a few well-capitalized buyers.

Government's Programa de Fomento a la Productividad Ganadera (PROGAN)-Production subsidies for feed efficiency

The Programa de Fomento Ganadero (PROGAN) Productivo pays producers who document feed-conversion gains, effectively reducing delivered ration costs[1]Source: Secretaría de Agricultura y Desarrollo Rural, “Programa de Fomento Ganadero 2025,” SAGARPA, gob.mx . In 2025 the Production for Well-Being scheme disbursed MXN 15.2 billion (USD 745 million) for forage and equipment, supporting a shift from pasture to concentrate feeding. Farmers rush to qualify before funds expire, creating seasonal spikes for high-efficiency starter feeds. Uptake is strongest in Jalisco, Sonora, Puebla, and Yucatán, where supplement sales also rise fastest.

Nearshoring of United States Meat Processors Triggering Feed Demand

United States meat companies are shifting slaughter and fabrication lines to Mexican border states to capture lower labor costs and tariff advantages[2]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual: Mexico,” fas.usda.gov . Projects like SuKarne’s USD 580 million Lucero complex in Durango exemplify the scale, feeding 300,000 head daily and requiring 130 metric tons of feed per hour. These plants demand finishing rations that meet United States export rules on antibiotic residues and mycotoxins. Border-state mills gain from shorter grain hauls but must navigate periodic rail congestion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High corn and soybean price volatility post United States–Mexico–Canada Agreement (USMCA) | −0.9% | National, acute in border states | Short term (≤ 2 years) |

| Strict mycotoxin limits in NORMA Oficial Mexicana (NOM) | −0.5% | Sonora, Chihuahua, Sinaloa, Coahuila, Durango | Medium term (2-4 years) |

| Water-use restrictions in drought-prone northern states | −0.4% | National, tighter near export plants | Medium term (2-4 years) |

| Biosecurity gaps raising African Swine Fever (ASF)-related insurance premiums | −0.3% | Jalisco, Sonora, Puebla, Yucatán | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict mycotoxin limits in NORMA Oficial Mexicana (NOM)

Mexico now enforces strict ceilings for aflatoxin and ochratoxin in feed, raising testing and certification costs by about 3% per metric ton [3]Source: Servicio Nacional de Sanidad, Inocuidad y Calidad Agroalimentaria, “Normas Oficiales Mexicanas,”gob.mx. Humid states such as Veracruz see higher rejection rates on local corn, forcing mills to blend imports or add costly binders. Export-oriented integrators demand certified mycotoxin-free rations, splitting the market into premium and commodity tiers. Millers without in-house labs face longer turnaround times and lost orders.

Biosecurity gaps raising African Swine Fever (ASF)-related insurance premiums

African Swine Fever has not entered Mexico, yet insurers lifted swine-sector premiums by up to 25% in dense production zones. Feed mills that serve hog farms must prove pathogen-free supply chains, especially for blood meal and animal proteins banned under NOM-060. Grupo KUO invested in traceability and rendering to lower risk, but independent mills shoulder higher compliance costs. In the short term, added overhead cuts profitability where feed already represents most of swine production cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Cereals Anchor Rations While Supplements Surge

Cereals led the ingredient portfolio with 46.0% Mexico compound feed market share in 2025, anchored by corn that supplies cost-effective metabolizable energy. Supplements posted the fastest growth, advancing at a 7.8% CAGR through 2031 as millers adopt lysine, phytase, and probiotics to meet stricter mycotoxin and antibiotic-free rules. This pivot toward precision nutrition shifts value capture from bulk grains to functional additives and enlarges the Mexico compound feed market size attributed to high-margin inputs. Better feed-conversion ratios and sustainability claims help early adopters justify premium prices to integrated poultry and aquaculture buyers.

Cakes and meals, primarily soybean meal, remain the main protein source but face volatile import costs that squeeze independent mills. Distillers dried grains with solubles gain traction as a lower-priced protein alternative and already absorb 15% of United States DDGS exports to Mexico, signaling further penetration potential. Vitamins, minerals, and toxin binders round out the mix, with sales lifted by tougher enforcement of NOM-187 mycotoxin ceilings. Together, these remaining segments diversify ingredient sourcing and create niche openings for regional premix specialists that tailor formulas to local grain quality.

By Animal Type: Poultry Holds Sway as Aquaculture Accelerates

Poultry feed commanded 54.5% Mexico compound feed market share in 2025, reflecting dense broiler and layer clusters in Jalisco, Veracruz, and Querétaro. Aquaculture feed recorded the quickest expansion, projected to rise at an 8.9% CAGR through 2031 on the back of shrimp farms in Sinaloa and Sonora that produced 273,940 metric tons in 2024. Strong demand for export-grade shrimp drives adoption of enzyme-fortified extruded rations that lift the Mexico compound feed market size for specialty coastal products. The twin pillars of poultry scale and aquaculture momentum underscore a widening gap between commodity and high-specification diets.

Swine feed held a significant share of national demand, anchored by integrated systems in Yucatán and Sonora where biosecurity investments temper African Swine Fever risk. Ruminant diets for dairy and feedlot cattle represent prominent demand and benefit from government forage subsidies that encourage moves from pasture to concentrate finishing. Pet nutrition accounts for a limited share of tonnage yet offers the highest margins, prompting Archer-Daniels-Midland to open a USD 39 million wet pet-food plant in Morelos. These remaining segments add resilience by balancing commodity-heavy poultry volumes with value-added niches that cushion revenue during grain-price swings.

Geography Analysis

Jalisco remained the foremost hub in the Mexican compound feed market share in 2025, supported by dense broiler, layer, and cattle clusters that provide mills with scale advantages. Its proximity to import ports and central highway corridors ensures efficient grain inflows and rapid distribution of finished feed. Pacific and Gulf coastal states, including Sinaloa, Sonora, Veracruz, Campeche, and Yucatán, form the fastest-growing region, with compound feed demand projected to rise through 2031 as shrimp and tilapia farming expand. Aquaculture’s need for high-protein extruded diets lifts margins despite lower overall feed tonnage relative to inland poultry centers.

Durango leverages integrated beef complexes to anchor local feed consumption, while Veracruz and Guanajuato cater to mixed poultry and cattle bases supported by modern milling assets. Northern border states such as Sonora, Chihuahua, and Coahuila capture nearshoring-driven demand from United States meat processors yet contend with drought-linked water caps that slow new plant approvals. Southern interior states including Chiapas and Tabasco remain underpenetrated but attract fresh investment in tilapia feed lines that diversify production footprints. Together, these areas balance commodity poultry volumes with emerging niche species, smoothing national feed demand.

Regional growth now hinges on logistics, environmental constraints, and species specialization rather than sheer population density. Central states exploit rail and highway links that shrink grain hauls and lower inbound costs for imported soybean meal. Coastal zones benefit from export-oriented shrimp operations that justify premium diets, while drought-prone northern territories invest in water recycling to sustain output. These intertwined strengths are expected to keep the Mexico compound feed market on an upward trajectory as diversified regional engines offset localized risks.

Competitive Landscape

The five largest suppliers including Cargill, Incorporated, Industrias Bachoco S.A.B. de C.V., Archer Daniels Midland Company, Nutreco N.V. (SHV Holdings N.V.), and Land O’Lakes, Inc. together controlled a majority of Mexico compound feed revenue in 2025, underscoring a moderately concentrated arena. Cargill, Incorporated leverages its Galleon, CattleView, and Agriness digital suites to offer precision-feeding services that raise client feed-conversion ratios. Industrias Bachoco vertically integrates breeder genetics, feed milling, processing, and branded retail channels, which secures captive demand and smooths raw-material risk. These two leaders use scale and technology to win multi-year contracts with poultry and pork integrators that favor consistent nutrient profiles and documented sustainability claims.

Archer-Daniels-Midland Company expands through specialty additives and a new wet pet-food plant that balances livestock exposure with higher-margin consumer segments. Nutreco N.V. (SHV Holdings N.V.) builds its presence via a fourth Mexican mill in Querétaro and focuses on shrimp and swine premixes that meet export market specifications. Land O’Lakes, Inc. upgrades its Purina Animal Nutrition site in Guanajuato to supply dairy and beef concentrates aligned with rising forage-to-grain feeding systems. Mid-tier regional millers still serve local demand, yet they face competitive pressure as these multinationals roll out precision-nutrition services countrywide.

Growth strategies hinge on functional ingredients, digital platforms, and targeted acquisitions that close geographic or species gaps. Joint ventures such as the 2026 Alltech-Archer-Daniels-Midland alliance signal a shift toward bundled solutions that combine global distribution with natural gut-health additives. Sustainability metrics, including mycotoxin compliance and carbon-reduced amino acids, enable premium pricing that lifts overall market value. As leading firms pair data analytics with specialty inputs, they are expected to accelerate Mexico compound feed adoption among export-oriented integrators and niche producers alike.

Mexico Compound Feed Industry Leaders

Cargill, Incorporated

Industrias Bachoco S.A.B. de C.V.

Nutreco N.V. (SHV Holdings N.V.)

Land O’Lakes, Inc.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alltech and Archer Daniels Midland Company confirmed regulatory clearance for their feed-additive joint venture, slated to begin operations in the first quarter of 2026, focusing on natural gut-health solutions for poultry and swine.

- August 2025: Novus International, Inc. enhanced its operations in Mexico by forming a dedicated team specializing in feed additives, gut health, production management, and sustainability. This team focuses on supporting poultry, swine, and dairy producers by improving feed efficiency and animal health, which are essential aspects of the compound feed industry.

- March 2025: ADM inaugurated a USD 39 million wet pet-food plant in Morelos to support its Ganador and Minino brands with 50% domestic inputs.

Mexico Compound Feed Market Report Scope

Compound feed is a combination of different concentrate feed ingredients in suitable ratios. Frequently used ingredients in compound feed include brans, protein meals/cakes, grains, agro-industrial by-products, minerals, and vitamins. The Mexico Compound Feed Market is segmented By Animal Type (Ruminants, Poultry, Swine, Aquaculture, and Others) and By Ingredients (Cereal, Cakes & Meals, By-Products, and Supplements). The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Ingredient

| Cereals |

| Cakes and Meals |

| By-products |

| Supplements |

By Animal Type

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Other Animal Types |

| By Ingredient | Cereals |

| Cakes and Meals | |

| By-products | |

| Supplements | |

| By Animal Type | Poultry |

| Swine | |

| Ruminants | |

| Aquaculture | |

| Other Animal Types |

Key Questions Answered in the Report

What is the current value of the Mexico compound feed market?

The Mexico compound feed market size stands at USD 15.80 billion in 2026 and is forecast to reach USD 19.30 billion by 2031.

Which ingredient category leads demand?

Cereals, especially corn, hold a 46.0% revenue share in 2025, serving as the primary energy source in broiler, layer, and swine diets.

How fast will aquaculture feed grow?

Aquaculture feed volume is projected to advance at an 8.9% CAGR through 2031, the fastest among all animal types.

Who are the top players in this market?

Cargill, Incorporated, Industrias Bachoco S.A.B. de C.V., Archer-Daniels-Midland Company, Nutreco N.V. (SHV Holdings N.V.), and Land O’Lakes, Inc. collectively capture a majority of sales.

What is the main risk facing millers?

Exposure to corn and soybean price volatility, driven by dependence on United States imports and currency fluctuations, poses the most immediate margin risk.

Page last updated on: