Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

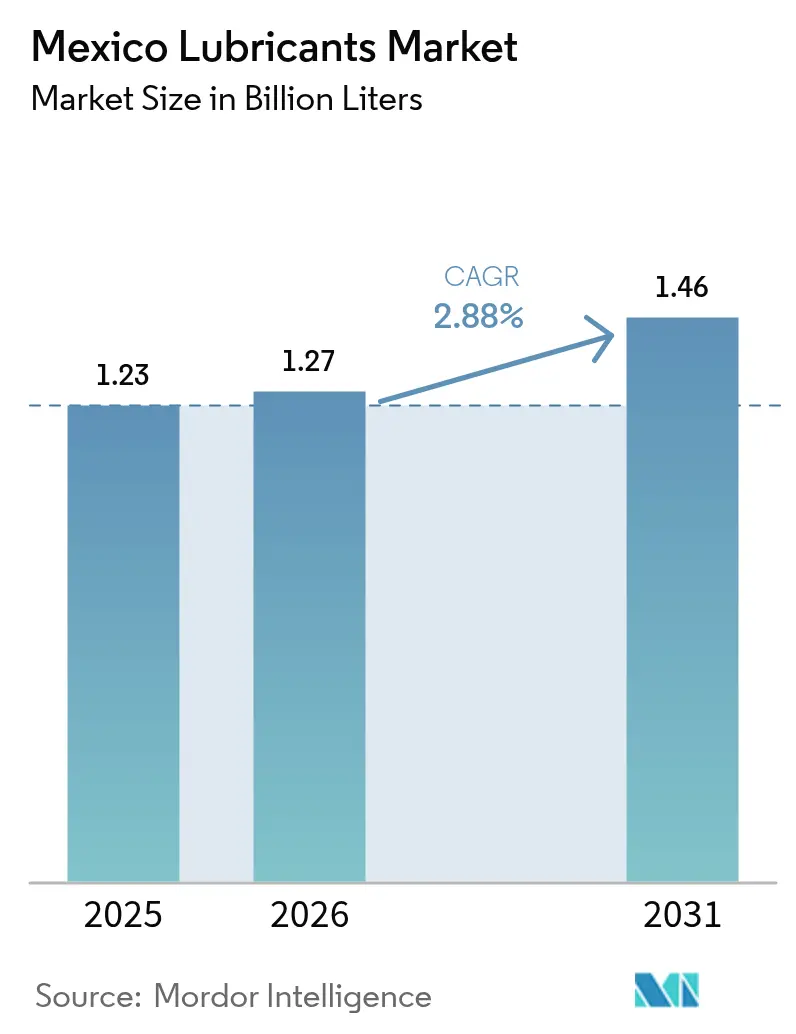

| Base Year Market Size (2025) | 1.23 Billion liters |

| Market Volume (2026) | 1.27 Billion liters |

| Market Volume (2031) | 1.46 Billion liters |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Lubricants Market Analysis by Mordor Intelligence

Mexico Lubricants market size in 2026 is estimated at 1.27 billion liters, growing from 2025 value of 1.23 billion liters with 2031 projections showing 1.46 billion liters, growing at 2.88% CAGR over 2026-2031. Demand is driven by the manufacturing boom created by near-shoring, a surge in vehicle production, and foreign direct investment pledges exceeding USD 45 billion, which reinforce industrial lubricant demand. Engine oil volumes continue to dominate, yet hydraulic and synthetic formulations are gaining ground as equipment technology evolves and Mexico implements Euro VI standards. The Dos Bocas refinery ramp-up strengthens the domestic base-oil supply and reduces import exposure. At the same time, rising electric-vehicle adoption, crude price swings, and new hydrocarbon compliance rules introduce cost and volume headwinds. Suppliers respond with local blending capacity, digital condition-monitoring services, and bio-based portfolios in line with the March 2025 Biofuels Law.

Key Report Takeaways

- By product type, automotive engine oil held 47.62% of the Mexico lubricants market share in 2025, while hydraulic fluids recorded the highest CAGR at 4.19% through 2031.

- By end-user industry, the automotive segment accounted for 60.05% of the Mexican lubricants market size in 2025; the heavy equipment segment is advancing at a 4.41% CAGR to 2031.

- By base stock, mineral oil retained 81.15% share in 2025, whereas bio-based grades are expanding at a 5.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive production boom and vehicle-parc growth | +1.2% | National, concentrated in Bajío and Northern border states | Medium term (2-4 years) |

| Near-shoring-led industrial capacity expansion | +0.8% | National, with early gains in Nuevo León, Querétaro, Guanajuato | Long term (≥ 4 years) |

| Shift toward high-performance synthetic lubricants | +0.4% | National, premium segments in urban centers | Medium term (2-4 years) |

| Industry 4.0 condition-monitoring adoption | +0.3% | Regional, manufacturing hubs in Tijuana, Ciudad Juárez | Long term (≥ 4 years) |

| Dos Bocas refinery ramp-up adding base-oil supply | +0.2% | National, supply chain optimization benefits | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Production Boom and Vehicle-Parc Growth

Mexico's automotive industry increased year-over-year, boosting demand for engine oil and transmission fluid across both OEM fill and aftermarket channels. Passenger-car sales and exports rose, reinforcing the lubricant pull-through in production hubs across Guanajuato and Coahuila. The average fleet age exceeds 17 years, so maintenance frequency stays elevated, especially for synthetic grades that extend service intervals. OEMs such as Tesla and BMW select Mexican sites to optimize USMCA content rules, further lifting factory-fill volumes. As of January 2025, Mexico will enforce Euro VI and EPA 2010 limits, compelling the development of high-performance, low-ash formulations that increase value per liter.

Near-Shoring-Led Industrial Capacity Expansion

FDI commitments of more than USD 45 billion in 2024 target electronics, battery, and precision-machinery clusters that require metalworking, hydraulic, and gear oils for clean-room and high-load environments[1]Tony Payan et al., “The Power Problem: Nearshoring and Mexico's Energy Sector,” Baker Institute, bakerinstitute.org . Guanajuato and Querétaro headline the manufacturing corridor, whereas Nuevo León’s proximity to Texas accelerates maquiladora growth. Power-grid bottlenecks limit factory throughput, prompting the installation of distributed solar and gas-engine systems that require high-temperature turbine and genset lubricants. Wind-turbine buildout in Coahuila and Oaxaca spurs demand for specialty greases resilient to fluctuating climate conditions. As OEM supply chains relocate, long-term industrial lubricant consumption embeds structurally higher baselines.

Shift Toward High-Performance Synthetic Lubricants

Plant managers adopt synthetics to counter unplanned downtime and labor shortages. Automotive OEM specifications favor SAE 0W-16 and 0W-20 formulations that deliver fuel-economy gains and extend oil-change intervals beyond 15,000 km. In the food and pharmaceutical industries, ISO 21469 and NSF H1 standards are expanding the uptake of ester-based fluids that withstand high-temperature wash-downs. Industrial players operating 24/7 machining lines are migrating to polyalphaolefin gear oils that reduce bearing temperature by 8-10 °C, thereby lowering maintenance labor costs. Mexico’s climatic diversity, ranging from 45 °C desert summers to 0 °C high-altitude winters, rewards multigrade synthetics that maintain viscosity within OEM targets across various regions. The wider availability of Group III base oils from Dos Bocas reduces import premiums, thereby narrowing the synthetic price gap.

Industry 4.0 Condition-Monitoring Adoption

Factories in Tijuana and Ciudad Juárez deploy IoT sensors and cloud platforms that trigger oil-change decisions based on in-service oxidation and wear-metal analytics. Early adopters report 20% savings in lubricant volume and 25% longer component life. Data integration drives demand for low-electrical-conductivity turbine oils that are compatible with embedded monitoring probes. Predictive alerts limit downtime in open-pit mines where stoppages can cost USD 50,000 per day. Barriers persist, including sensor retrofit expenses, limited broadband availability in rural sites, and a shortage of reliability engineers. Multinationals, therefore, dominate deployments; however, falling hardware costs will prime medium-term diffusion through tier-two suppliers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV penetration curbing engine-oil volumes | -0.6% | National, accelerated in urban centers | Long term (≥ 4 years) |

| Crude and base-oil price volatility | -0.4% | National, supply chain cost pressures | Short term (≤ 2 years) |

| New Hydrocarbon Sector Law raises compliance costs | -0.3% | National, regulatory framework changes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EV Penetration Curbing Engine-Oil Volumes

Electric-vehicle registrations surged in 2024, boosting the EV share of new-car sales and reducing the per-vehicle lubricant needs. OEMs retool for battery-electric output, while Mexico City and Monterrey offer charging tax credits that push fleet operators to electrify vans. Engine oil demand erosion accelerates after 2027 as larger parcels of Mexico’s aging fleet retire. Countermeasures include thermal-management fluids for lithium-ion packs and e-drive greases with dielectric properties. Development timelines and small volumes temper revenue substitution in the forecast window.

Crude and Base-Oil Price Volatility

Brent prices oscillated in 2024, squeezing blender margins and complicating inventory planning for small distributors lacking hedging lines. PEMEX satisfied only 30% of domestic base-oil demand ahead of the Dos Bocas ramp-up, so importers were exposed to freight spikes and peso moves. The September 2024 decree, which tightened import documentation, increased lead times and working capital needs. Although Dos Bocas adds Group II capacity, operational learning curves may constrain near-term output consistency. Volatility, therefore, remains a planning variable through 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Retain Lead While Hydraulic Fluids Accelerate

In 2025, automotive engine oils captured 47.62% of the Mexico lubricants market share as assembled vehicles required both factory-fill and dealership after-sales support. Hydraulic fluids, however, register the highest 4.19% CAGR, driven by demand for construction equipment and mining shovels linked to infrastructure programs. Metalworking fluids increase in volume in machining plants that produce EV battery casings and aerospace components, while turbine oils benefit from 19 GW of renewable energy build-out through 2030.

Technological differentiation deepens across sub-categories. Low-viscosity SAE 0W multigrade engine oils can improve fuel economy, a key selling point as automakers strive to meet CAFE standards. Hybrid vehicles spur growth in specialized transmission fluids with high dielectric strength. Gear oil volumes trail new quarry operations in Sonora and Zacatecas, where demand for open-gear greases supporting 10-meter ball mills rises sharply. Oil off-take processes track tire production along Puebla’s rubber corridor, while transformer oil consumption increases with grid modernization spending that targets 75% capacity additions by 2037.

By End-User Industry: Automotive Still Dominant but Heavy Equipment Gains Momentum

The automotive sector accounted for 60.05% of Mexico's lubricants market size in 2025 as OEMs maintained three-shift schedules to meet North American demand. Passenger-vehicle maintenance, dealership service contracts, and extended warranties tie lubricant brands into OEM-approved supply chains. Heavy equipment lubricants are projected to post a 4.41% CAGR as the Tren Maya railway, highway concessions, and open-pit lithium projects in Sonora stimulate excavator and haul-truck fleets.

Marine consumption tracks port expansion projects in Altamira and Veracruz, which handle petrochemical and LNG cargoes, driving demand for cylinder oil and hydraulic fluid for container cranes. Aerospace clusters in Baja California utilize synthetic lubricants that conform to AS5780 standards for component machining. Industrial sectors ranging from steelmaking in Nuevo León to food processing in Jalisco increase demand for high-temperature grease and food-grade compressor oil. Power generation, especially combined-cycle gas plants, requires low-ash turbine oils that resist varnish formation under Mexico’s high ambient temperatures.

By Base Stock Type: Mineral Leads but Bio-Based Sets the Growth Pace

Mineral-oil volumes commanded an 81.15% share in 2025 because Group I and Group II supplies enjoy cost advantages from PEMEX and U.S. Gulf Coast imports. The Mexico lubricants market size for mineral oils is expected to increase even as synthetic oil adoption rises. Synthetic-grade demand is projected to be driven by OEM specifications and high-temperature industrial applications. Semi-synthetic adoption expands in the commercial vehicle fleet, where operators balance price and drain interval gains.

Bio-based lubricants register a 5.22% CAGR, the highest across base stocks, under Mexico’s March 2025 Biofuels Law that encourages renewable-feedstock uptake. Applications include NSF H1-approved hydraulic oil for beverage firms and biodegradable chainsaw oils for forestry in Durango. Despite cost premiums, CSR targets and export audits from U.S. customers support adoption. Waste-oil re-refining capacity led by Bravo Energy reaches 100 million liters per year, feeding circular-economy loops that supply base-oil Group II+ cuts for fleet trials.

Geography Analysis

Regional demand mirrors industrial clusters. The demand in the Bajío corridor of Guanajuato, Querétaro, and San Luis Potosí is driven by the dense automotive output and ancillary plastic-molding plants. Fuchs invested in a USD 15 million blending plant in San Luis Potosí, which reduces delivery lead times to OEM lines. Monterrey houses Mexico’s largest steelworks, boosting demand for high-temperature roller-bearing greases.

Central Mexico, centered on Mexico City and the State of Mexico, retains the largest aftermarket pool, owing to a passenger-car parc exceeding 5 million units that average 17 years in age. Stringent emissions inspections push garages toward low-sulfur synthetics. The region hosts petrochemical clusters in Tula and Altamira that require compressor and gear oils for ethylene and propylene trains. Coastal demand stems from marine bunkering and refinery maintenance along the Gulf. Mining clusters in Chiapas and Guerrero add grease and hydraulic-fluid volume. Distribution challenges persist due to limited road infrastructure, yet e-commerce auto-parts platforms improve last-mile lubricant access for independent workshops.

Competitive Landscape

The Mexico lubricants market is moderately consolidated. Shell leverages its global brand and exclusive agreements with OEM dealerships. Domestic champion Mexicana de Lubricantes commands loyalty through nationwide convenience-store availability, whereas Lubricantes de América excels in private-label blending for industrial distributors. Competitive strategy increasingly depends on technical services such as fluid condition monitoring, AI-driven pricing engines, and training programs that build stickiness beyond commodity pricing. Sustainability credentials also matter, prompting suppliers to launch bio-based lines and publish carbon-footprint disclosures. New entrants face capital-intensive quality-assurance requirements under SENER oversight, yet niche opportunities exist in EV fluids, food-grade lubricants, and military-spec formulations. Strategic partnerships between global additive houses and local formulators help bridge technology gaps and ensure compliance with OEM and ASTM standards. Overall, product innovation and customer-centric services outweigh pure scale in defining long-term winners within the Mexico lubricants market.

Mexico Lubricants Industry Leaders

Exxon Mobil Corporation

Shell Plc

Roshfrans

Raloy

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. initiated a strategic review of its Castrol unit, valued near USD 10 billion, potentially reshaping competitive dynamics.

- December 2024: FUCHS has finalized a land agreement for its second lubricant plant in Villa de Reyes, San Luis Potosi, Mexico. This new facility, representing a USD 15 million investment, will span 51,000 square meters at World Trade Center San Luis Potosi 2. It will serve as a key hub for FUCH's next phase of expansion, with operations expected to begin in 2026.

- January 2024: Petrofer has successfully expanded its production plant by doubling the floor space, significantly enhancing production capacities to meet growing demand. This strategic expansion is poised to strengthen Petrofer's competitive edge and drive growth in the lubricant market.

Mexico Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How big is the Mexico lubricants market in 2026?

The market is expected to reach 1.27 billion liters in 2026 and is projected to grow at a 2.88% CAGR through 2031.

Which product type leads demand?

Automotive engine oil holds a 47.62% share, reflecting Mexico’s vehicle production base.

What is the fastest-growing end-user segment?

Heavy equipment lubricants are projected to post a 4.41% CAGR as construction and mining fleets expand.

Why are synthetic lubricants gaining share?

OEM fuel-economy targets, higher drain intervals, and Mexico’s wide climate range favor synthetics for both automotive and industrial applications.

How will electric vehicles affect lubricant demand?

EV penetration reduces per-vehicle lubricant consumption, pressuring long-term engine oil volumes but opening niches in thermal management fluids.

Page last updated on: