Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

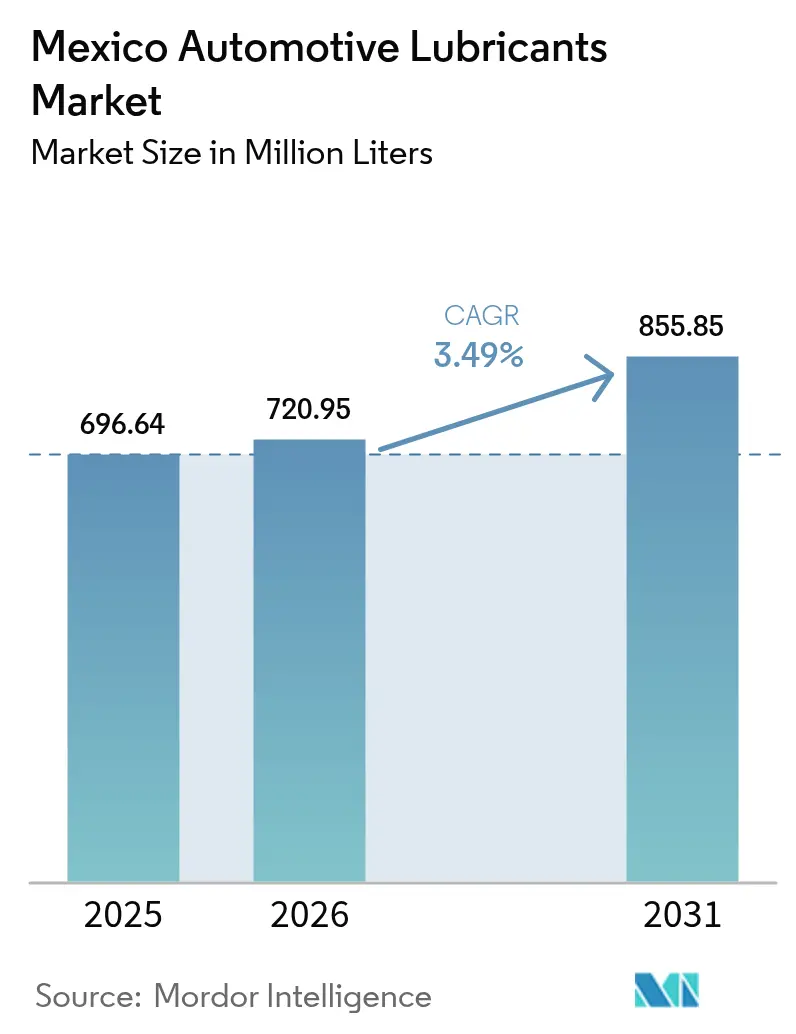

| Base Year Market Size (2025) | 696.64 Million liters |

| Market Volume (2026) | 720.95 Million liters |

| Market Volume (2031) | 855.85 Million liters |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Automotive Lubricants Market Analysis by Mordor Intelligence

The Mexico Automotive Lubricants Market size is projected to be 696.64 million liters in 2025, 720.95 million liters in 2026, and reach 855.85 million liters by 2031, growing at a CAGR of 3.49% from 2026 to 2031. Two distinct forces shape near-term growth. Light-truck output bound for the United States keeps factory fill steady in the Bajío and northern corridors, yet extended drain intervals on those same trucks flatten retail volume. Synthetic adoption is rising because OEMs require low-viscosity 0W-20 and 5W-30 grades to comply with NOM-044 emissions limits, pulling value up even as liters per vehicle decline. Counterfeit crackdowns that lengthened import-permit approvals from 15 to 32 days in December 2025 briefly exposed the fragility of just-in-time supply lines, but they also nudged buyers toward traceable brands and digitally verified packaging. E-commerce still represents under 5% of lubricant sales, yet its double-digit trajectory is forcing distributors to publish transparent prices, eroding the information advantage independent mechanics once held. Finally, Industry 4.0 automation inside assembly plants is lifting demand for specialty greases that feed automated lubrication systems, creating fresh, high-margin micro-segments.

Key Report Takeaways

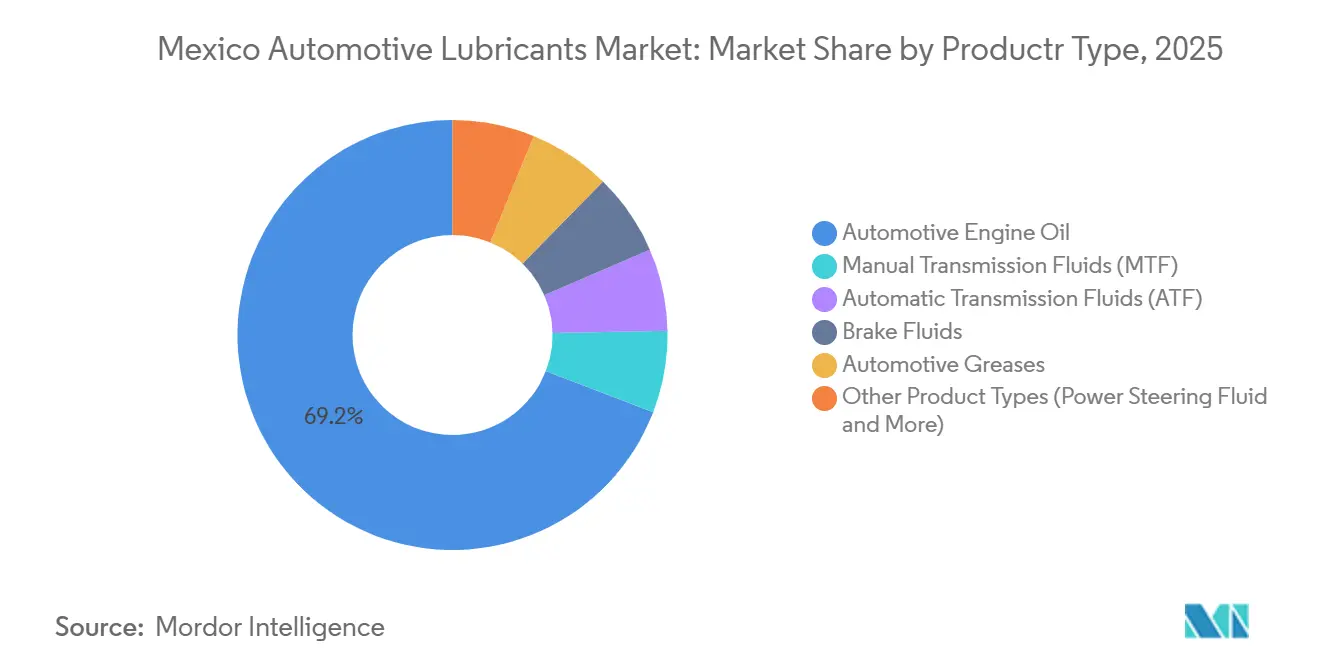

- By product type, automotive engine oil accounted for 69.15% of the Mexico Automotive Lubricants market share in 2025, while automatic transmission fluids (ATF) are forecast to register the highest CAGR of 4.33% during the forecast period (2026-2031).

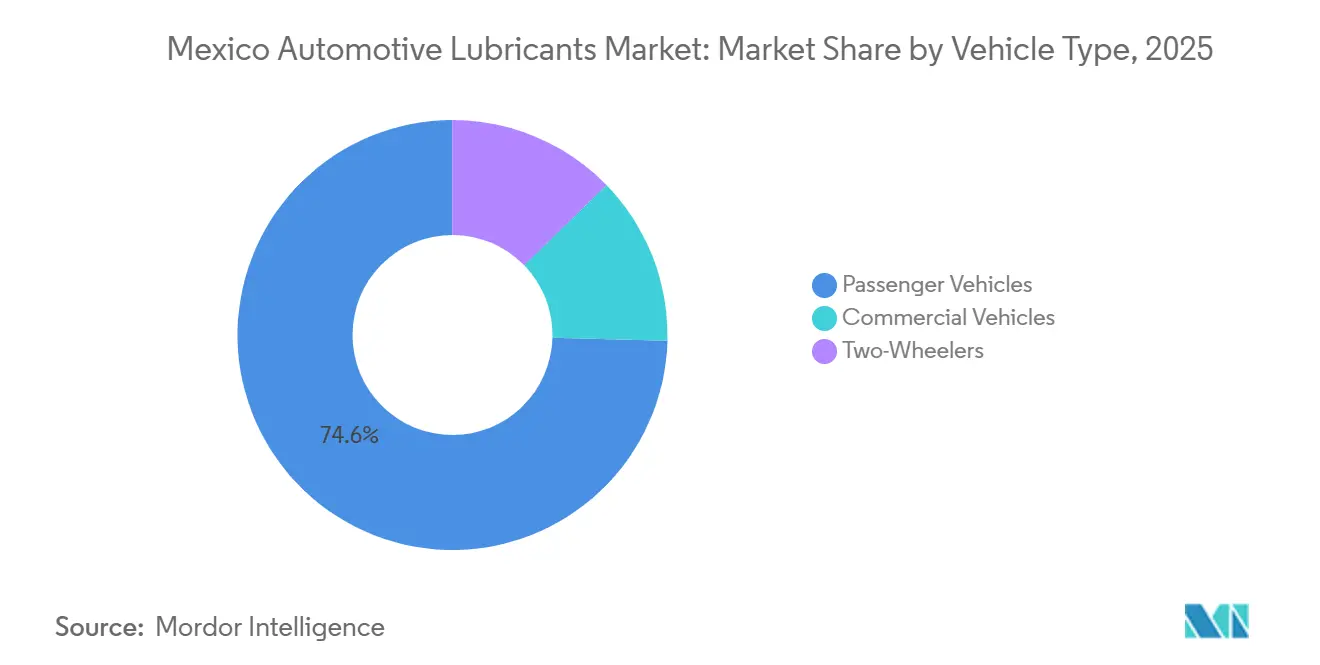

- By vehicle type, passenger vehicles accounted for 74.57% of the Mexico Automotive Lubricants market size in 2025 and are expected to expand at a 3.95% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of domestic auto production and exports | +1.2% | Bajío (Guanajuato, Querétaro) and North (Nuevo León, Coahuila, Chihuahua) | Medium term (2-4 years) |

| Penetration of synthetic and low-viscosity lubricants | +0.8% | Global, with early gains in Bajío OEM clusters | Long term (≥ 4 years) |

| Growth of quick-lube and e-commerce aftermarket channels | +0.6% | National, concentrated in Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Industry 4.0 uptake of automated lubrication systems | +0.5% | Bajío and North manufacturing corridors | Medium term (2-4 years) |

| Fleet-digitization driving predictive-maintenance oil demand | +0.4% | National, with early adoption in logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic Auto Production and Exports

Mexico assembled 3.95 million vehicles in 2025, shipping 78% to the United States under USMCA rules that favor parts made in the region[1]Asociación Mexicana de la Industria Automotriz, “Producción y Exportación de Vehículos Ligeros,” amia.com.mx. Light trucks and SUVs represented close to four-fifths of that output, each unit carrying 8-10 quart sumps that sustain the Mexico Automotive Lubricants market even as sedans shrink. January 2026 retail sales climbed 8.7% year on year to 131,472 units, signaling healthy replacement demand despite a brief production dip tied to inventory rebalancing. Assembly capacity is clustered in Guanajuato, Querétaro, Nuevo León, Coahuila, and Chihuahua, creating dense aftermarket networks where quick-lube chains fight dealer workshops for service revenue. ExxonMobil’s new lubricant-analysis laboratory, launched in January 2026, processes 90,000 samples a year within 48 hours, anchoring predictive-maintenance contracts for Tier 1 suppliers and locking fleet customers deeper into premium synthetics.

Penetration of Synthetic and Low-Viscosity Lubricants

Synthetic formulations now represent about 55% of gasoline-engine oil volume, propelled by OEM mandates for 0W-20, 5W-20, and 5W-30 grades that trim friction losses and satisfy strict emissions limits. Toyota pioneered 10,000-mile drain intervals in Mexico and the United States back in 2010, halving lifetime oil demand per vehicle while boosting ticket value per change because synthetics sell at 40-60% premiums. Home-grown blender Raloy supplies more than half of Mexico’s synthetic gasoline-engine oils and performs over 100 ASTM tests at its accredited laboratory, enabling rapid tweaks when OEM specs evolve. Low-viscosity fluids cut fuel use by 1-2%, a gain that resonates with fleet operators paying diesel prices above USD 1.00 per liter. However, longer drain intervals stretch replacement cycles, meaning volume growth in the Mexico Automotive Lubricants market lags value growth.

Growth of Quick-Lube and E-Commerce Aftermarket Channels

Quick-service chains and digital marketplaces are redrawing aftermarket distribution maps. Bardahl de México runs 52 branches and 80,000 points of sale, and in March 2026, it opened a new Toluca plant certified as “Industria Limpia,” positioning the brand to service retail chains that demand environmental credentials. ExxonMobil expanded its Mobil Fleet Pro digital platform to 22 states in December 2025, offering fleets real-time inventory visibility and automated re-order triggers that bypass traditional distributors. E-commerce penetration sits below 5% but is climbing at double-digit rates as MercadoLibre and Amazon Mexico list OEM-approved bottles with home delivery, allowing price comparisons that squeeze margins for unbranded oils. Valvoline’s March 2026 agreement with logistics firm RIMSA covers six states and focuses on the Restore & Protect line for high-mileage vehicles, a segment that holds more than 60% of Mexico’s 49.6 million vehicle parc.

Industry 4.0 Uptake of Automated Lubrication Systems

Industrial-robot imports grew 23% between 2017 and 2022, and 70% of those units landed in automotive plants that rely on centralized lubrication to keep presses, CNC machines, and robotic welders humming. FUCHS invested MXN 300 million (USD 15 million) in a San Luis Potosí plant that opened in January 2026, complete with rail sidings that cut delivery times to Bajío customers from one week to two days. A June 2025 warehouse expansion in Querétaro doubled storage capacity, allowing 2-3 day service to border cities that tolerate zero downtime. Shell’s Expo Manufactura case study showed automated systems running up to 62,000 hours, shaving 23,500 liters of lubricant use and 65 tonnes of CO₂-equivalent emissions, evidence that synthetic greases can cut both maintenance bills and carbon footprints[2]Shell Global, “Case Study: Optimized Industrial Lubrication,” shell.com. Specialty greases such as polyurea and calcium sulfonate command 30-50% premiums, giving suppliers a margin hedge against slowing engine-oil volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV adoption reducing ICE oil volumes | -0.4% | National, with early gains in Mexico City, Monterrey | Long term (≥ 4 years) |

| Proliferation of counterfeit / low-quality products | -0.3% | National, concentrated in informal retail channels | Short term (≤ 2 years) |

| OEM-driven extended drain-intervals | -0.2% | Global, with early adoption in OEM dealer networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Adoption Reducing ICE Oil Volumes

Battery-electric and hybrid models captured 9.5% of new-vehicle sales in 2025, up from near zero five years earlier, and require little to no engine oil while using a fraction of conventional transmission fluid. Domestic EV output reached 169,929 units in 2024, mostly premium crossovers built for export, yet component suppliers tied to internal-combustion engines reported 35-45% order declines and face USD 2.5 billion in retooling costs. Hybrid powertrains soften the blow because they still employ engines, but regenerative braking and stop-start systems stretch service intervals by roughly 20%, trimming retail oil demand further. Mexico offers no broad consumer purchase incentives, so mass adoption hinges on battery cost curves and OEM product planning, indicating the sharpest demand erosion for the Mexico Automotive Lubricants market likely arrives after 2030 rather than during the forecast window.

Proliferation of Counterfeit and Low-Quality Products

Counterfeit lubricants hold an estimated 20% global share and an even higher slice of informal Mexican retail, where stolen fuel, known as “huachicol,” often masquerades as engine oil to dodge taxes. December 2025 rules that stretched import-permit approval to 32 days sought to improve traceability but temporarily halted one auto plant and almost stopped three more, spotlighting supply-chain fragility. Bardahl earned “Industria Limpia” certification in March 2026 to reassure buyers of product integrity, while TotalEnergies rolled out holographic ValiGate labels worldwide, although Mexican adoption details remain undisclosed. Organized networks sell counterfeit oil 30-50% below branded prices, eroding brand loyalty and pushing legitimate suppliers to spend more on packaging security and distributor audits, costs ultimately borne by consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Volume, ATF Leads Growth

Automotive engine oil controlled 69.15% of the Mexico Automotive Lubricants market share in 2025. Yet its growth trails the broader Mexico Automotive Lubricants market size because extended drain intervals and rising EV penetration cut per-vehicle demand in half on many late-model cars. Within the segment, low-viscosity 0W-20 and 5W-30 synthetics are displacing legacy 15W-40 and 20W-50 grades, favoring multinational blenders with Group III base-oil access. Manual transmission fluids and automotive greases continue to grow in line with vehicle-parc expansion, but neither commands more than a mid-single-digit volume share.

Automatic transmission fluids are the fastest-growing product line, advancing at a 4.33% CAGR through 2031 and lifting their slice of the Mexico Automotive Lubricants market size every year. Eight-speed and CVT gearboxes in light trucks require fully synthetic DEXRON VI or MERCON LV fluids that last 80,000-160,000 kilometers, doubling ticket value per service. Demand for brake fluids, coolants, and specialty greases rides the upgrade cycle for turbocharged engines and automated manufacturing, creating a rich long-tail of small but high-margin sub-segments.

By Vehicle Type: Passenger Cars Dominate, Fleet Behavior Alters Volume

Passenger cars held 74.57% of 2025 lubricant liters and will expand at a 3.95% CAGR to 2031 as crossover and SUV registrations climb and older sedans remain on the road. Vehicles older than 10 years, more than 60% of the parc, leak and burn oil, pulling conventional 10W-30 and 20W-50 grades through informal channels. By contrast, late-model SUVs use synthetic 0W-20 oils with twice-as-long intervals, shrinking liters sold per service but doubling revenue per change, a value migration that reshapes channel economics in the Mexico Automotive Lubricants market.

Commercial vehicles command a mid-teens share of volume yet underpin the Mexico automotive lubricants market size in revenue terms because CK-4 synthetics carry price premiums of 60-80%. Extended drain programs stretch oil changes to 40,000-60,000 kilometers, curbing volume growth to roughly 3% but boosting demand for oil analysis kits and telematics services that only a handful of suppliers can bundle. Two-wheelers occupy a low-single-digit slice and grow with GDP in large cities, yet rampant counterfeit sales keep margins razor-thin.

Geography Analysis

The Bajío, Guanajuato, Querétaro, Aguascalientes, and San Luis Potosí, and the northern corridor of Nuevo León, Coahuila, and Chihuahua host 70% of national light-vehicle assembly, concentrating factory fill and first-service demand within 200 kilometers of the plants. FUCHS’ USD 15 million San Luis Potosí plant, opened in January 2026, uses rail links to cut inbound mineral-oil costs and outward delivery times, a sign that suppliers now design logistics around this geography.

Mexico City and Estado de México own the largest single consumption cluster because eight million vehicles clog their roads; however, counterfeit penetration reaches up to 70% of roadside sales, forcing premium brands to invest in serialized labels and formal dealer networks that raise distribution costs by 10-15%. Shell and partner CISA are investing up to USD 35 million to lift Naucalpan blending capacity by roughly 50%, targeting central-state demand that still rises on the back of aging cars.

Jalisco and Puebla act as secondary hubs where automotive stamping and truck fleets create a balanced mix of engine oils, hydraulic fluids, and greases. Valvoline’s partnership extension with RIMSA covers Veracruz and Chiapas, betting that port expansion and logistic-corridor growth will lift high-mileage vehicle counts and favor Restore & Protect synthetics. Southern and Gulf states such as Oaxaca, Yucatán, and Campeche display lower per-capita lubricant use but faster percentage growth, supported by tourism fleets and infrastructure projects that add diesel trucks to local roads.

Competitive Landscape

The Mexico Automotive Lubricants market is moderately consolidated. White-space growth lies in FA-4 ultra-low-viscosity diesel oils for long-haul fleets and in 0W-8 synthetics for next-generation hybrid engines. Shell’s Expo Manufactura case study quantified USD 1.1 million in savings and 23,500 liters of reduction at one plant, framing premium lubricants as cost-avoidance tools rather than consumables. Compliance complexity under NOM-116, which mandates Spanish labels, batch tracking, and two-year certification, also raises the barrier to entry, helping entrenched brands defend margins against informal blenders.

Mexico Automotive Lubricants Industry Leaders

ExxonMobil Corporation

Shell PLC

BP Plc (Castrol)

Roshfrans

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Valvoline Global Operations has partnered with RIMSA, a leading automotive distributor in Mexico, to expand its reach across six key states. Starting March 1, 2025, the partnership will enhance access to Valvoline's premium products, including the "Restore and Protect Premium Full Synthetic" motor oil, transmission fluids, and gear oils.

- March 2025: BASF announced to invest in its manufacturing site in Puebla, Mexico, to increase the capacity of aminic antioxidants for lubricants. This expansion will address the growing demand for antioxidant additives and help the Mexican automotive lubricants market.

Mexico Automotive Lubricants Market Report Scope

Automotive lubricants, encompassing engine oils, gear oils, and greases, play a pivotal role in reducing friction, wear, and heat among moving parts. This not only boosts engine performance and efficiency but also extends its lifespan. These lubricants, made from a combination of base oils and additives, serve multiple functions: they clean, cool, and guard against corrosion.

The Mexico Automotive Lubricants market report is segmented by product type (automotive engine oil, manual transmission fluids, automatic transmission fluids, brake fluids, automotive greases, and other product types (power steering fluid and more)) and vehicle type (passenger vehicles, commercial vehicles, and two-wheelers). The market forecasts are provided in terms of volume (liters).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large will automotive lubricant demand be in Mexico by 2031?

It is forecast to reach 855.85 million liters, expanding at a 3.49% CAGR from 2026 to 2031.

Which product line grows the fastest?

Automatic transmission fluids are projected to post a 4.33% CAGR through 2031 as 8-9-speed and CVT gearboxes spread across light trucks.

What share do passenger vehicles hold today?

Passenger cars represent 74.57% of 2025 lubricant liters the Mexico automotive lubricants market.

How serious is counterfeiting in Mexican lubricants?

Counterfeit and adulterated oils account for roughly 20% of total volume and up to 70% of roadside sales in parts of Mexico City.

Are synthetics now the majority of engine-oil sales?

Yes, synthetics constitute around 55% of gasoline-engine oil liters, driven by OEM mandates for 0W-20 and 5W-30 grades.

Page last updated on: