Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

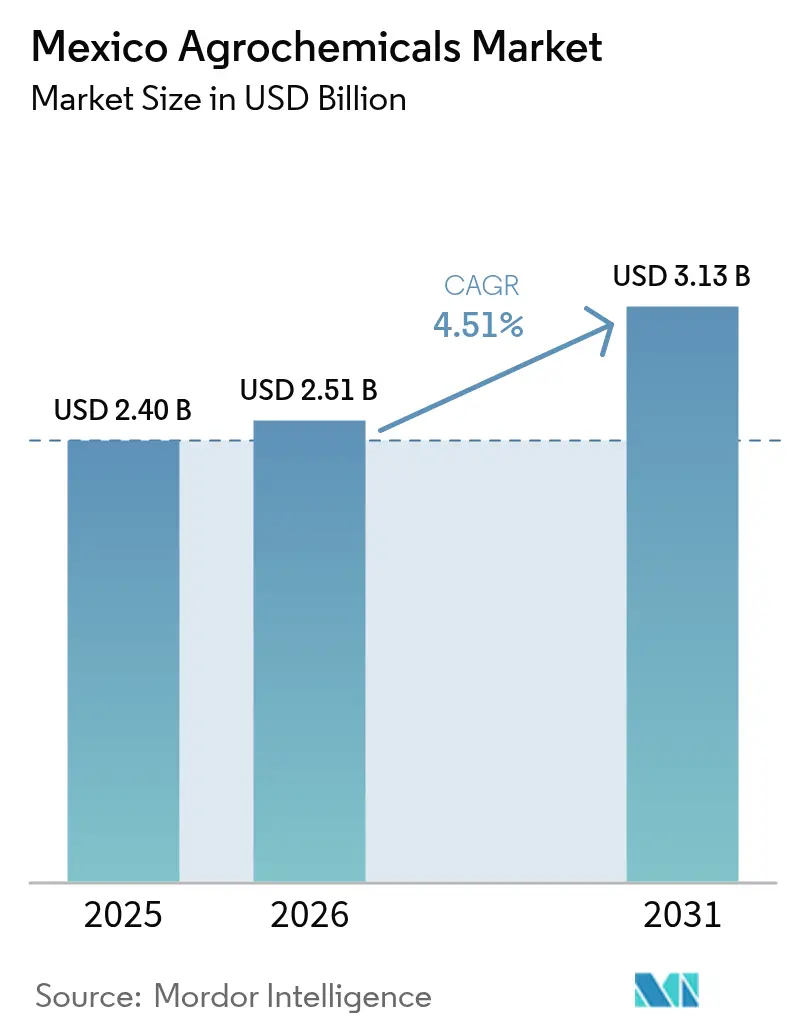

| Base Year Market Size (2025) | USD 2.4 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Agrochemicals Market Analysis by Mordor Intelligence

The Mexico agrochemicals market size was valued at USD 2.4 billion in 2025 and estimated to grow from USD 2.51 billion in 2026 to reach USD 3.13 billion by 2031, at a CAGR of 4.51% during the forecast period (2026-2031). Mexico’s large base of irrigated grains, fast-expanding horticulture exports, and steady government subsidy outlays anchor demand, while tighter active-ingredient rules and global raw-material swings temper the growth curve. Fertilizer vouchers help stabilize smallholder purchases and catalyze the rebound in corn and sorghum acreage following conditions like drought[1]Source: Servicio de Información Agroalimentaria y Pesquera, “Estadísticas de Producción Agrícola,” SIAP, gob.mx. Export-oriented orchards and protected-agriculture clusters are creating specialized niches for micronutrient blends, copper fungicides, and water-soluble formulations that command above-average price points. Competitive intensity remains moderate.

Key Report Takeaways

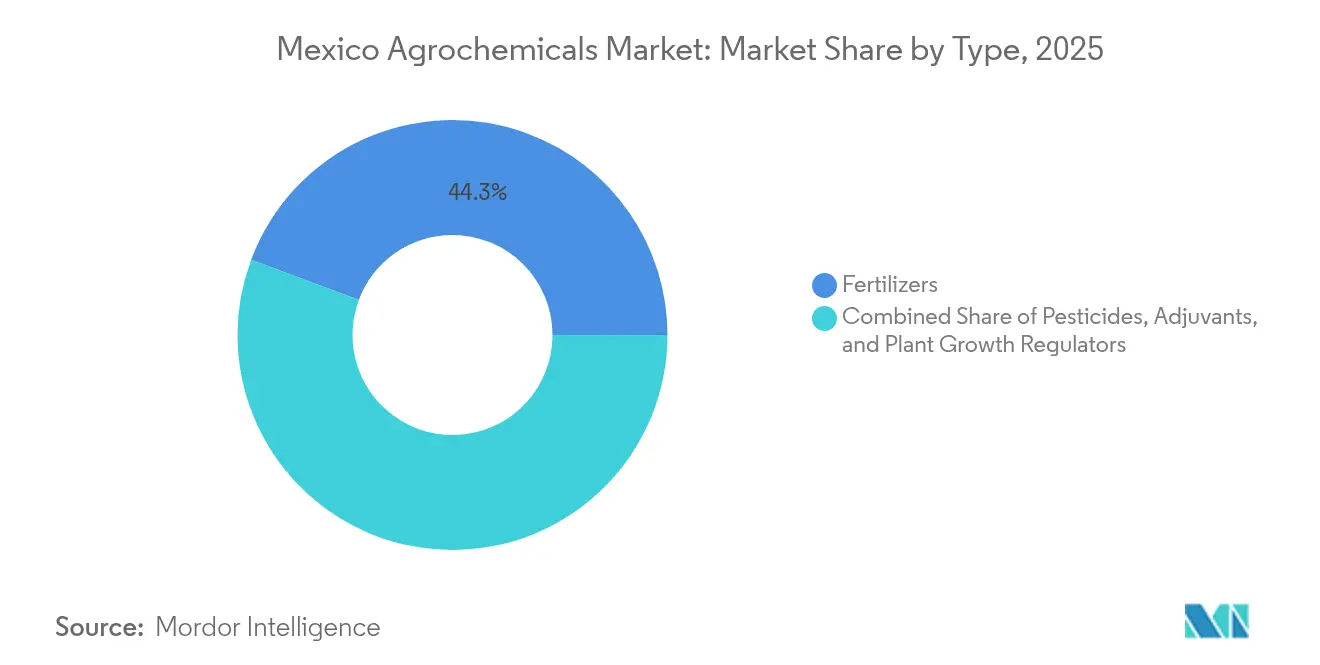

- By product type, fertilizers led with 44.30% revenue share in 2025, while specialty fertilizers are projected to grow at 8.46% CAGR through 2031.

- By application, grains and cereals held 48.80% of the Mexico agrochemicals market share in 2025, and fruits and vegetables are expanding at an 7.94% CAGR through 2031.

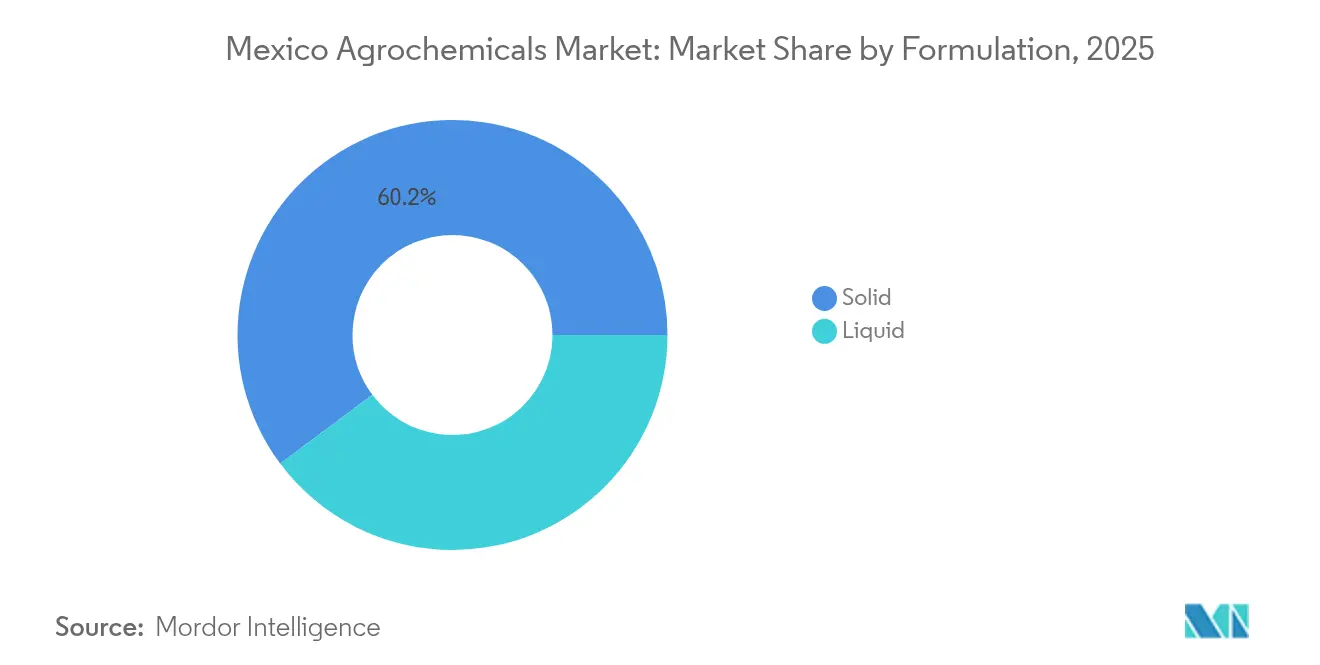

- By formulation, solid formulations accounted for a 60.20% share of the Mexico agrochemicals market size in 2025, whereas liquid formulations are advancing at a 7.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies Drive Fertilizer Demand Across Smallholder Segments | +1.2% | National, strongest in rain-fed smallholder zones | Medium term (2–4 years) |

| Corn and Sorghum Acreage Recovery Boosts Nutrient Consumption | +0.8% | Sinaloa, Sonora, Jalisco | Short term (≤ 2 years) |

| Integrated Pest Management Adoption Transforms Product Mix | +0.7% | Export regions nationwide | Long term (≥ 4 years) |

| Avocado Export Expansion Drives Specialty Input Demand | +0.9% | Michoacán, Jalisco, Nayarit | Medium term (2–4 years) |

| Protected Agriculture Expansion Accelerates Input Intensification | +0.6% | Central Mexico and Baja California | Long term (≥ 4 years) |

| Precision Agriculture Technology Adoption Optimizes Input Efficiency | +0.5% | Commercial farms across Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies Drive Fertilizer Demand Across Smallholder Segments

The SADER (Secretariat of Agriculture and Rural Development) fertilizer program allocated MXN 9 billion (USD 500 million) in 2024, a 15% jump from 2023 [2]Source: Secretaría de Agricultura y Desarrollo Rural, “Programas de Apoyo al Campo,” SADER, gob.mx . Inclusion of specialty blends such as slow-release urea and chelated micronutrients boosted premium uptake, and local formulation lines have been expanded so international suppliers can qualify for the domestic-sourcing rule. Participating growers report yield lifts of 7% to 9% in rain-fed corn, reinforcing the program’s political and agronomic importance. Distributors now bundle mobile advisory apps with voucher redemption, deepening brand loyalty.

Integrated Pest Management Adoption Transforms Product Mix

INIFAP (Instituto Nacional de Investigaciones Forestales, Agrícolas y Pecuarias) field trials show that integrated pest management techniques cut overall pesticide volume by up to 40% without sacrificing yields.[3]Source: Instituto Nacional de Investigaciones Forestales, Agrícolas y Pecuarias, “Investigación y Desarrollo Agrícola,” INIFAP, gob.mx Export producers chasing maximum residue limit compliance now rely on pheromone traps and selective insecticides with precise modes of action. COFEPRIS approved 12 reduced-risk products in 2024, double the previous year’s count. These launches favor suppliers with robust R&D pipelines capable of replacing broad-spectrum actives being phased out, and they stimulate demand for adjuvants that optimize droplet retention and canopy coverage.

Avocado Export Expansion Drives Specialty Input Demand

Mexico shipped 1.4 million tons of avocados in 2024, earning USD 3.2 billion and spurring intensive input regimes across 140,000 hectares in Michoacán plus new acreages in Jalisco. Copper fungicide programs call for eight to twelve sprays per season, and growers increasingly apply foliar zinc, boron, and calcium to achieve U.S. Department of Agriculture Grade 1 fruit. New orchard plantings use soil fumigants and root biostimulants at establishment, further diversifying the addressable product slate. Export protocols mandate residue testing, pushing demand toward shorter pre-harvest-interval formulations.

Protected Agriculture Expansion Accelerates Input Intensification

Year-round tomato and bell-pepper cycles inside greenhouses create non-seasonal purchasing profiles coveted by suppliers. Enclosed environments require selective insecticides that preserve worker air quality and provide other associated benefits, driving demand for new chemical classes and innovative solutions. Government credit incentives covering a significant share of greenhouse capex fuel continued footprint growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility Pressures Import-Dependent Supply Chains | -1.1% | Nationwide import-dependent supply chains | Short term (≤ 2 years) |

| SEMARNAT Regulatory Tightening Reduces Available Active Ingredients | -0.8% | National, with variable state enforcement | Medium term (2–4 years) |

| Water Stress and Soil Salinity Reduce Input Efficiency | -0.6% | Sonora, Sinaloa, Baja California, coastal belts | Long term (≥ 4 years) |

| Counterfeit Products Undermine Market Value and Farmer Confidence | -0.7% | Informal rural channels | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Pressures Import-Dependent Supply Chains

Ammonia, phosphate rock, and potash imports cover 70% of national requirements, so fluctuations that swung urea between USD 300 and USD 650 per ton in 2024 flowed directly into ex-warehouse prices. Domestic ammonia output fell to 60% of capacity because of natural-gas constraints at PEMEX facilities, raising import reliance. Port congestion at Veracruz and Altamira during peak season added USD 15 to USD 25 per ton in demurrage fees, and a 10% peso depreciation typically lifts distributor costs by 7% to 8%. Smallholders who buy at planting have the least ability to hedge, hitting baseline volume during price spikes.

SEMARNAT Regulatory Tightening Reduces Available Active Ingredients

Thirty-five active ingredients have been banned or restricted since 2024, and the glyphosate phase-out slated for 2025 leaves corn growers scrambling for alternatives. Paraquat removal in 2024 eliminated a key desiccant, forcing a switch to more expensive options such as diquat or mechanical harvesting in sorghum. Atrazine limits in groundwater protection zones now cover roughly two million hectares, pressing growers to adopt multi-ingredient herbicide stacks that often double program cost. Regulatory divergence among states complicates logistics as distributors juggle varying compliance rosters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fertilizers Anchor Market and Specialty Fertilizers Lead Growth

By product type, fertilizers led with 44.30% revenue share in 2025. Nitrogenous products account for the bulk, reflecting corn’s heavy demand, while phosphate formulations support root growth in beans and chickpeas. Potash relies on overseas mines, giving domestic blenders latitude to tweak ratios and capture margin. Specialty fertilizers are projected to outpace the broader Mexico agrochemicals market at an 8.46% CAGR to 2031 as coated urea, chelates, and bio-enhanced granules fit precision-agriculture scripts.

Nitrogen efficiency products now sell through every leading distributor, aided by voucher eligibility and greenhouse segment pull. Pesticides occupy the second-largest wallet share, and herbicides lead that subset because 7.1 million hectares of corn rely on weed control. Fungicides are gaining popularity as avocado and berry exporters chase spotless phytosanitary certificates. Adjuvants and plant growth regulators remain smaller, but surfactants that bolster canopy spread are gaining single-digit share as spraying windows narrow under stricter residue cut-offs.

By Application: Grain Volume Steady, Horticulture Value Surging

By application, grains and cereals held 48.80% of the Mexico agrochemicals market share in 2025. Large mechanized holdings deploy pre-emergence herbicide programs that dovetail with minimum-tillage practices. Pulses and oilseeds show incremental growth supported by livestock feed demand, but remain comparatively niche on the revenue ladder.

Fruits and vegetables are forecast to expand at 7.94% CAGR, making them the brightest pocket through 2031. Avocado hectares expand outside Michoacán, requiring intensive copper fungicide sequences and foliar micronutrients. Protected berry operations inside high-roof tunnels use soluble NPK at rates triple those of open-field tomatoes. Export protocols that require zero-tolerance for certain residues are accelerating switches to selective modes of action, thereby raising average selling prices and lifting absolute contribution to the Mexico agrochemicals market.

By Formulation: Solids Dominant Yet Liquids Climb on Technology Uptake

By formulation, solid formulations accounted for a 60.20% share of the Mexico agrochemicals market size in 2025, because granular fertilizers are easy to broadcast with tractor-pulled spreaders common in Sinaloa grain belts. Wettable powders remain cost-effective for basic fungicide needs and tolerate long warehousing cycles in warm rural depots. Granule coating technology that embeds micronutrients is beginning to differentiate price tiers.

Liquid formats are slated to grow 7.28% annually through 2031 as drip fertigation, aerial drone spraying, and variable-rate rigs demand formulations with predictable flow curves. Water-soluble fertilizers already dominate greenhouse pepper and cucumber nutrition schedules, and emulsifiable herbicide concentrates cut rinsing volumes when growers implement tank-mix programs. Suppliers are investing in Lerma and Querétaro plants to onshore liquid blending, shortening delivery lead times when peso exchange rates swing.

Geography Analysis

Northern states such as Sinaloa, Sonora, and Tamaulipas represent a significant block of demand. Mechanization levels enable early adoption of precision applicators that favor coated fertilizers and selective herbicides. Water scarcity pushes the adoption of polymer-based conditioners and salinity-tolerant nutrient packages.

Central Mexico, encompassing Jalisco, Michoacán, and Guanajuato, contributes a modest percentage of sales. Michoacán’s phytosanitary regime mandates copper sprays and micronutrient foliar feeds. The region benefits from dense distributor networks and proximity to research institutions that run demonstration plots promoting integrated management and digital scouting.

Southern and southeastern states, including Chiapas, Oaxaca, and Yucatán, currently make up a less significant contribution to the Mexico agrochemicals market but are logging the fastest expansion as fertilizer voucher penetration widens. Smallholders are switching from saved seed varieties to higher-yield hybrids that need more nutrients per hectare.

Regulatory Landscape

Mexico regulates pesticides and plant nutrients through an inter-agency framework coordinated under CICLOPLAFEST. COFEPRIS leads on health, SEMARNAT covers environmental aspects, and SADER operates through SENASICA for agriculture and phytosanitary control. Product market access depends on registration plus the relevant import and export authorizations, while compliance is anchored in the Ley Federal de Sanidad Vegetal, which requires monitoring and verification of pesticide use to limit contamination and protect plant health.

Labeling and packaging compliance is enforced through mandatory standards such as NOM-232-SSA1-2009 for containers and labels of technical and formulated pesticides. This shapes artwork and traceability information, and it also affects distributor handling practices. Given the inter-agency approval and enforcement process, along with active-ingredient restrictions and phase-outs referenced in the market context (including SEMARNAT and COFEPRIS actions), suppliers need strong dossier readiness, reformulation pipelines, and distributor compliance programs to maintain commercialization permits.

Competitive Landscape

The Mexico agrochemicals market features moderate concentration; the top five suppliers held a major share of 2024 revenue, balancing scale benefits with room for niche innovators. Bayer holds a prominent share by coupling corn hybrids with aligned herbicide tolerance packages, delivering an integrated value proposition that locks in seed and chemistry income streams. Syngenta follows at a significant share, supported by vegetable seed leadership and a broad fungicide line for greenhouse users. UPL is another prominent player with a major share, illustrating the strength of post-patent portfolios when combined with deep rural logistics networks that guarantee in-season stock.

Digital farm advisory tools have become a clear differentiator. Bayer’s FieldView platform covers nearly 500,000 hectares, driving cross-sell of variable-rate fertilizer recommendations. Syngenta’s Cropwise suite offers predictive disease alerts that tie into its newly registered reduced-risk fungicides. Local players leverage WhatsApp groups and in-field demonstration days to build loyalty in remote areas where data connectivity is uneven but peer recommendation carries weight.

Regulatory tightening favors suppliers with robust R&D, as the exit of older high-toxicity molecules opens white space for selective chemistries. BASF’s patent on copper-amino-acid complexes supports a premium line for organic-leaning orchardists. Distributors able to guarantee traceability via QR codes and tamper-evident seals also win share from counterfeit markets. Production localization continues: BASF will invest EUR 50 million (USD 55 million) in Lerma to de-risk port congestion and currency exposure.

Mexico Agrochemicals Industry Leaders

Syngenta Crop Protection AG

UPL Limited

Yara International ASA

BASF SE

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory changes create openings for suppliers that can replace restricted actives with newer reduced-risk chemistries and biologicals, while also supporting better economics for differentiated innovation. In April 2026, a decree amending the Regulations on Pesticides, Plant Nutrients, and Toxic or Hazardous Substances introduced a 10-year data protection period for safety and efficacy data for new products, and it extended registration renewal validity from 5 to 10 years. Together, these provisions favor innovators with registrable dossiers and improve lifecycle planning for branded portfolios. The same reform tightened requirements for generic or me-too applicants by requiring proof of a patent in force in Mexico or an IMPI-recorded license, which reshapes entry strategies for post-patent portfolios.

Demand-side opportunities are concentrated in export-oriented horticulture and orchards, where growers monetize compliance and performance, including water-soluble fertigation products for protected agriculture and micronutrient and copper-based programs for crops such as avocados (1.4 million tons exported in 2024). Volume is also supported by programmatic spend, with SADERs fertilizer support allocating MXN 9 billion in 2024 and voucher eligibility for specialty blends expanding the reachable smallholder basket beyond commodity NPK. On the supply side, localization and service layers can reduce disruption from import dependence and counterfeit leakage, including onshore liquid blending, QR-coded traceability, and digitally supported stewardship aligned to COFEPRIS/SENASICA compliance requirements.

Recent Industry Developments

- July 2026: Syngenta opened a new research laboratory in El Ejido focused on addressing agronomic and technical challenges for growers. The added local R&D and testing capability supports faster adaptation of crop protection and biological solutions to regional pest and disease pressures, tightening the linkage between field validation and commercialization in Mexico.

- May 2025: PepsiCo and Yara expanded their partnership to Latin America, including work with potato growers in Mexico, to advance lower-carbon fertilizer and farming practices across the food value chain. The program strengthens demand for differentiated nutrient products and advisory services that document sustainability outcomes for downstream buyers.

- September 2024: COFEPRIS increased approvals of reduced-risk crop protection products, with the market context noting 12 such products approved in 2024. The higher pace of reduced-risk registrations accelerated portfolio rotation away from older broad-spectrum molecules and expanded options for export growers managing residue-compliance requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Mexico agrochemicals market is the sales value of farm-use input chemicals used in crop production within Mexico, covering fertilizers, pesticides, adjuvants, and plant growth regulators across common crop uses and formulation forms.

Scope exclusions: We exclude bulk purchases that are later resold after value addition to avoid double counting the same product value twice.

Segmentation Overview

- By Type

- Fertilizers

- Nitrogenous Fertilizers

- Phosphatic Fertilizers

- Potash Fertilizers

- Specialty Fertilizers

- Pesticides

- Herbicides

- Insecticides

- Fungicides

- Adjuvants

- Surfactants

- Oils and Concentrates

- Plant Growth Regulators

- Auxins

- Cytokinins

- Gibberellins

- Fertilizers

- By Application

- Grains and Cereals

- Pulses and Oilseeds

- Fruits and Vegetables

- Turf and Ornamentals

- Other Applications

- By Formulation

- Solid

- Liquid

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping Mexico agriculture activity and chemical use context, because demand usually tracks crop area, crop mix, and application intensity. We used public sources such as FAOSTAT, UN Comtrade, and Mexico government statistics (such as SIAP and INEGI) to anchor crop area trends, production signals, and trade movements.

We also reviewed product and regulatory signals that can change demand or pricing, including guidance from agriculture and environmental regulators, association publications, and reputable press coverage. Company filings and investor presentations were used to sense-check business direction, and paid subscriptions for company financials and shipment-level trade data were used selectively to validate the value-pool direction and timing. The sources listed here are illustrative only, and many other public references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm buying patterns and seasonality, and to test assumptions that are hard to infer from public data alone. We spoke with manufacturers, formulators, distributors, agronomy advisers, and farm operators across Mexico so that formulation shifts (solid versus liquid), crop intensity differences, and pricing behavior were represented in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 17% | |

| Mid tier: 58% | Functional/Unit leaders: 35% | |

| Smaller Players: 17% | Managers: 48% |

Market-Sizing & Forecasting

Sizing was anchored using a top-down build that reconstructs the value pool from Mexico crop activity and input-intensity signals, then applies pricing logic by major product group. To keep totals realistic, we corroborated results with selective bottom-up checks, such as sampled price per kilogram or liter multiplied by estimated application volumes for key crops, followed by distributor validation.

Inputs used in the model included planted area and crop mix for major grains and horticulture, import and export trends for key chemical inputs, observed shifts between solid and liquid formulations, seasonality aligned to planting cycles, and mix changes across fertilizers, pesticides, adjuvants, and plant growth regulators. Where direct data points were missing, we handled gaps using conservative interpolation and expert-confirmed ranges so outputs stayed repeatable. Forecasts were developed using scenario analysis supported by a simple multivariate regression view, with area, crop value direction, and input-cost movements as main drivers, then tuned using primary feedback on adoption and pricing.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, where totals were compared against trade movements, crop area trends, and the implied spend per hectare for key crops. If a segment showed an unusual change, we rechecked assumptions, then ran a second analyst review and targeted re-contacts when pricing, product mix, or timing needed clarification.

The study is refreshed annually, and interim updates are made when material events affect fertilizer or pesticide pricing, regulation, or supply availability. Before delivery, an analyst runs a fresh pass across the model and narrative so clients receive an updated view aligned to the latest public statistics and confirmed market feedback.

Mordor Intelligence's Mexico Agrochemicals Market Size Compared With Other Published Estimates

Different published market sizes for Mexico agrochemicals can diverge even when the titles look similar, because the included product basket and pricing basis are not always aligned. The base year selected, how imports are treated, and whether distribution markups are counted can also move the final number.

In practice, the biggest gaps come from whether fertilizers are included alongside crop protection chemicals, and whether adjuvants and plant growth regulators are counted as separate demand or blended into pesticide totals. Another driver is the price basis used for the year, where some estimates use an average across the year while others lean on higher-price months during volatility. The spread below is mainly explained by including fertilizers plus specialty inputs while excluding reseller value-add layers, a scope treatment applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.40 B (2025) | |

| Global Consultancy A | USD 3.12 B (2025) | Uses a broader product basket that appears to weight fertilizers more heavily, and it may apply a different price basis and channel uplift assumptions, which can raise the value versus farm-use consumption. |

| Industry Publisher B | USD 4.61 B (2025) | Likely rolls up fertilizers and pesticides with regional splits and a longer-horizon pricing view, and it is less clear how import values, local formulation, and distribution margins are separated. |

Across the three figures, the higher values are consistent with wider inclusion and different treatments of pricing and channel economics. By tying totals back to crop activity signals and checking implied spend per hectare with market feedback, we keep the final number traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Mexico agrochemicals market?

The Mexico agrochemicals market is valued at USD 2.51 billion in 2026 and is projected to climb to USD 3.13 billion by 2031.

How fast is demand for specialty fertilizers growing in Mexico?

Specialty fertilizers are forecast to expand at an 8.46% CAGR through 2031, outpacing the broader market thanks to precision farming and export-crop quality needs.

Which crop segment drives the largest share of agrochemical consumption?

Grains and cereals, led by corn and sorghum, account for 48.80% of total spending because of their large harvested area and high nutrient requirements.

Which regions offer the fastest growth opportunity for suppliers?

Central Mexico's protected-agriculture corridor and the southern states transitioning to voucher-based fertilizer programs are registering the highest volume growth.

Page last updated on: