Metal Oxide Nanoparticles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Oxide Nanoparticles Market Analysis by Mordor Intelligence

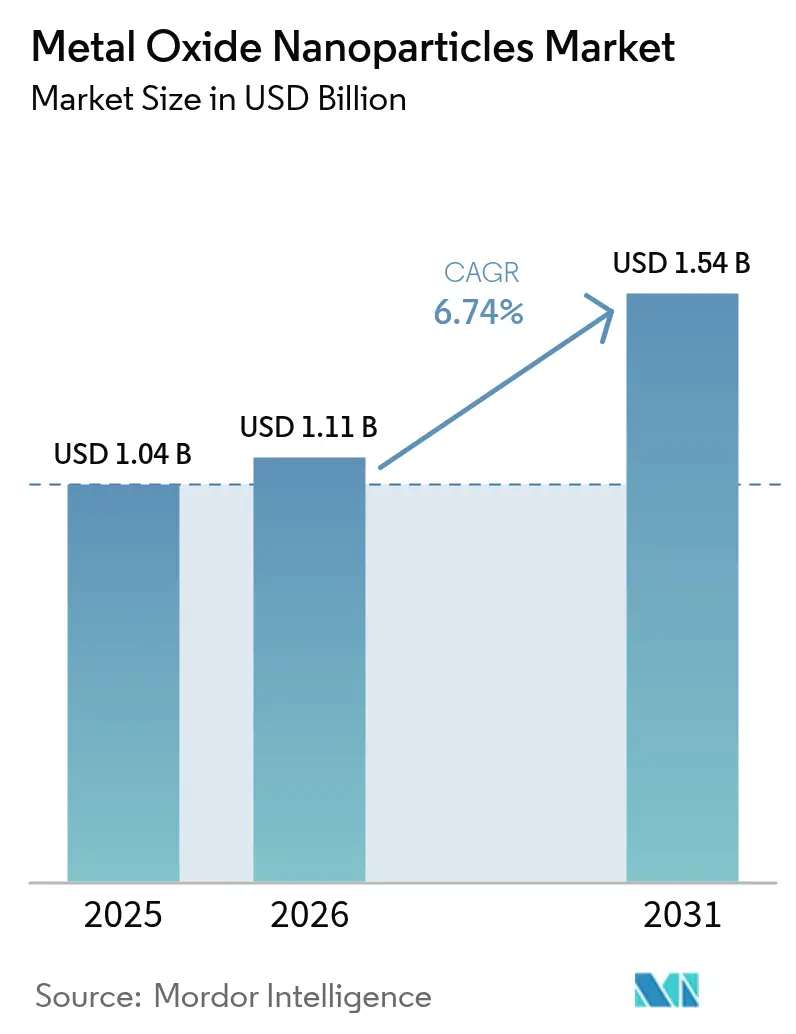

The Metal Oxide Nanoparticles Market size market is expected to grow from USD 1.04 billion in 2025 to USD 1.11 billion in 2026 and is forecast to reach USD 1.54 billion by 2031 at 6.74% CAGR over 2026-2031. Robust demand from semiconductor fabs, electric-vehicle battery makers and high-performance coating formulators underpins this outlook. Advanced node logic below 5 nm, solid-state electrolyte prototypes and antimicrobial surface treatments all rely on metal oxides whose surface-to-volume ratios deliver properties unavailable in bulk equivalents. Supply chains remain regionally concentrated, yet bio-based synthesis pilots are lowering environmental footprints while meeting electronics-grade purity thresholds. Regulatory momentum around nanomaterial stewardship, especially in the European Union and North America, is steering procurement toward greener production routes, favouring suppliers that disclose full life-cycle data.

Key Report Takeaways

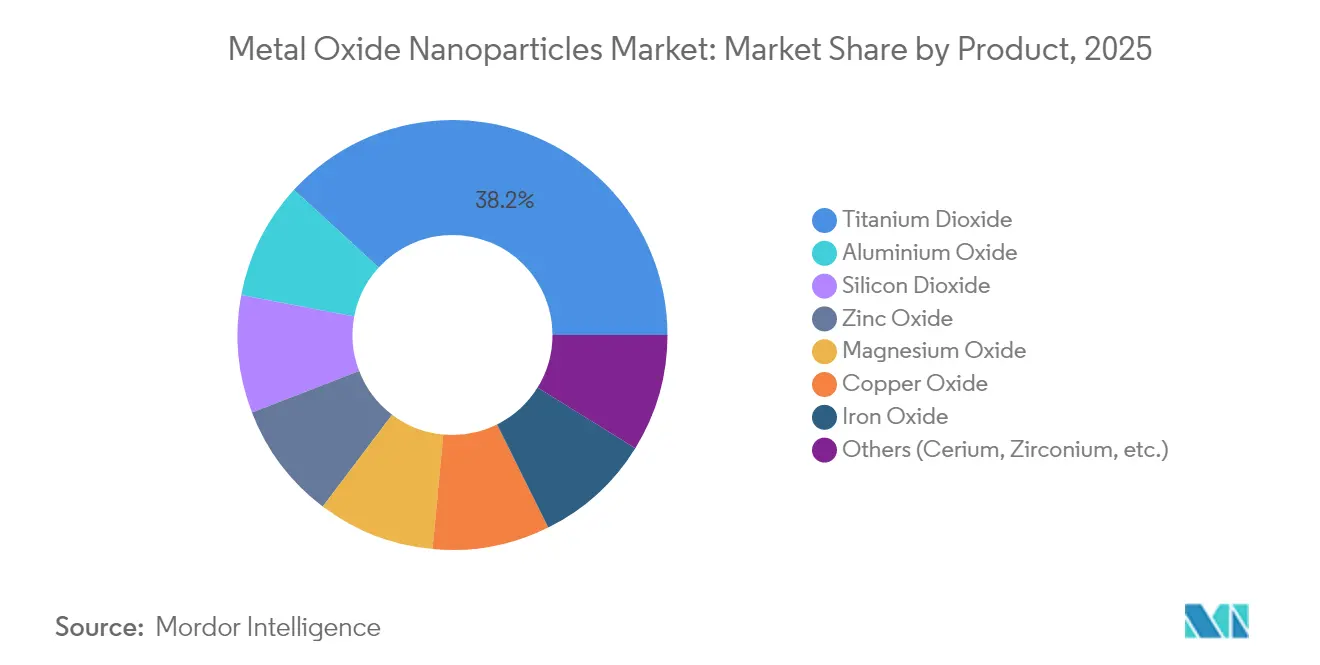

- By product type, Titanium Dioxide led with 38.20% of the Metal oxide nanoparticles market share in 2025.

- By synthesis method, chemical routes held 62.55% share of the Metal oxide nanoparticles market size in 2025, while bio-based synthesis is projected to expand at 7.89% CAGR through 2031.

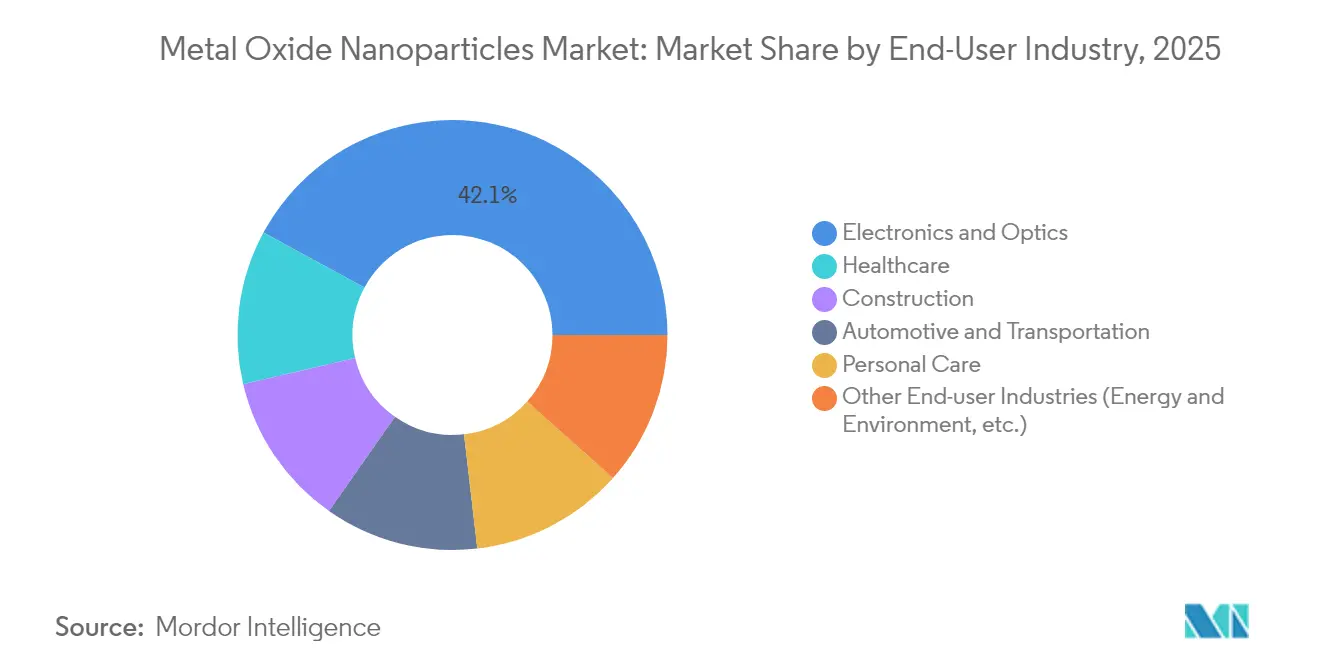

- By end-user industry, electronics and optics commanded 42.10% share of the Metal oxide nanoparticles market size in 2025; energy & environment is forecast to advance at an 8.32% CAGR to 2031.

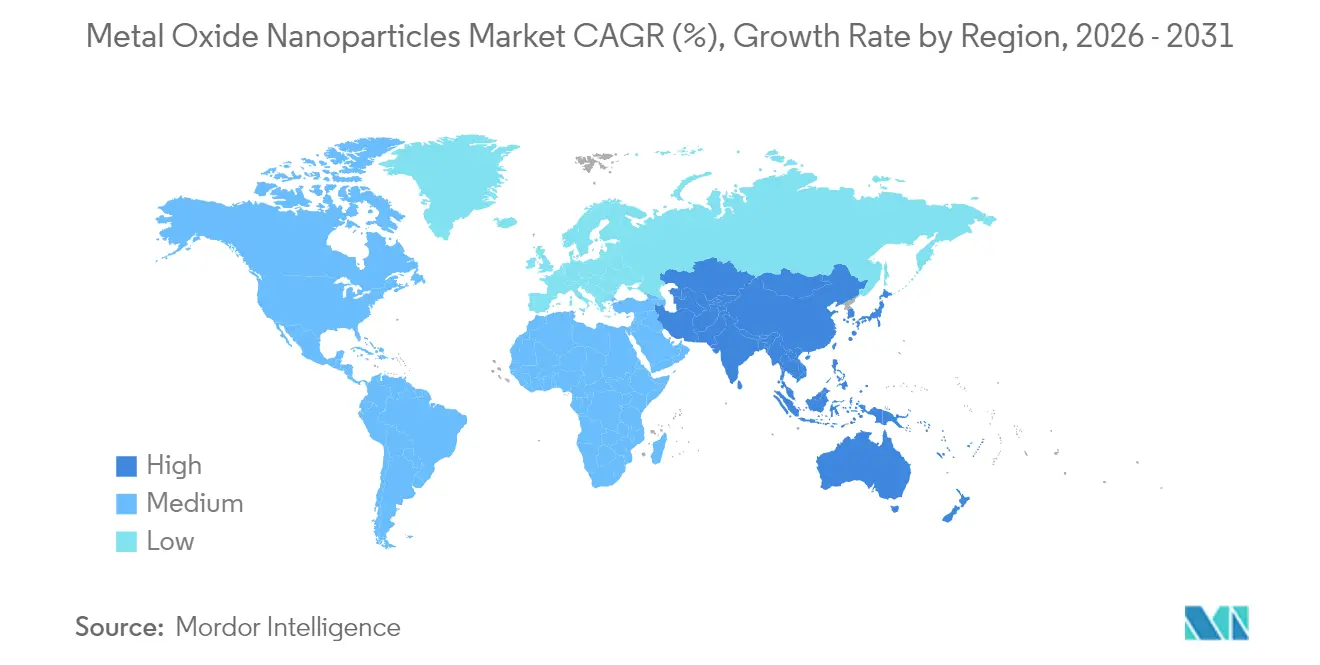

- By geography, Asia-Pacific accounted for 47.40% of the Metal oxide nanoparticles market share in 2025 and is set to grow at 7.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metal Oxide Nanoparticles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing electronics demand for high-k dielectric & transparent conductive films | +1.8% | Global, concentrated in APAC semiconductor hubs | Medium term (2-4 years) |

| Rising use as antibacterial agents in personal care & coatings | +1.2% | Global, with regulatory leadership in EU and North America | Short term (≤ 2 years) |

| Surge in Li-ion battery cathode & solid-state electrolyte R&D | +1.5% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Transition to green synthesis routes enhancing regulatory acceptance | +0.9% | EU and North America leading, APAC following | Long term (≥ 4 years) |

| Demand for UV-blocking additives in 3D-printing photopolymers | +0.7% | North America and EU, early adoption in APAC | Medium term (2-4 years) |

| Government incentives for semiconductor fabs needing high-purity oxide nanopowders | +1.1% | United States, South Korea, Japan, Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing electronics demand for high-k dielectric & transparent conductive films

Advanced node logic chips below 5 nm require ultrathin gate stacks made from titanium dioxide and hafnium oxide nanoparticles that minimize leakage currents while preserving capacitance. United States incentives total USD 1.4 billion for advanced packaging, with funds supporting materials down-selection that depends on semiconductor-grade oxides[1]U.S. Department of Commerce, “CHIPS for America: Funding Opportunity,” commerce.gov. Touchscreens and flexible OLED displays rely on indium tin oxide and zinc oxide nanoparticle films that remain conductive under repeated bending cycles. AI accelerators positioned at the edge drive higher operating temperatures, compelling designers to specify dielectric layers able to withstand thermal spikes without drifting electrical constants. HP’s USD 50 million Oregon expansion aims to scale microfluidic MEMS technologies that incorporate oxide thin films for nozzle and channel insulation. These converging trends sustain a high-purity materials pipeline that anchors the Metal oxide nanoparticles market.

Rising use as antibacterial agents in personal care & coatings

Zinc oxide and copper oxide nanoparticles deactivate 99.9% of bacteria within 10 minutes by releasing reactive oxygen species, offering an alternative to conventional preservatives. Pandemic-era building retrofits accelerated orders for antimicrobial wall paints and HVAC filters embedding these oxides. European regulators formalised nano-specific safety dossiers for TiO₂ and ZnO in cosmetics, signalling likely adoption in other jurisdictions and giving compliant producers first-mover advantage. Construction specifications increasingly embed antimicrobial coatings to extend maintenance intervals, while smart-textile manufacturers incorporate nanoparticle finishes that survive 50+ wash cycles. The breadth of applications continues to pull new volumes into the Metal oxide nanoparticles market.

Surge in Li-ion battery cathode & solid-state electrolyte R&D

Battery developers engineer lithium nickel manganese cobalt oxide and lithium iron phosphate cathodes with nanoscale morphology control to shorten diffusion paths. Evonik’s Yokkaichi fumed alumina plant, opening 2025, will supply separator coatings demanding 99.99% purity grades. Ceramic solid-state electrolytes formulated with zirconia and alumina nanoparticles now achieve ionic conductivities of 10^-3 S/cm at room temperature. American Elements expanded its portfolio to include silicon nanoparticles coated with metal oxides that mitigate volumetric expansion in high-capacity anodes[2]American Elements, “Battery-Grade Metal Oxide Nanoparticles Portfolio,” americanelements.com . With automakers committing to multi-gigawatt-hour cell factories, stable upstream supply strengthens the Metal oxide nanoparticles market.

Transition to green synthesis routes enhancing regulatory acceptance

Plant-extract and microbial processes cut energy input by up to 60% versus conventional sol-gel methods while sidestepping toxic solvents. Proof-of-concept lines converting agricultural waste into ZnO and TiO₂ feedstocks are reaching kilogram-per-hour output, matching semiconductor purity after post-synthesis calcination. European buyers evaluating cradle-to-gate emissions now treat bio-based nanoparticles as a differentiator in supplier scorecards. Harmonised protocols for biologically derived powders support regulatory filings, smoothing commercial rollout. These developments position sustainable processes as a core growth lever inside the Metal oxide nanoparticles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity and environmental persistence prompting stricter regulations | -1.4% | Global, with EU and North America leading regulatory stringency | Medium term (2-4 years) |

| Lack of standardized nano-scale metrology across supply chains | -0.8% | Global, particularly affecting cross-border trade | Short term (≤ 2 years) |

| Price volatility of rare-earth precursors for complex oxides | -0.6% | Global, with supply concentration in China creating vulnerabilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Toxicity and environmental persistence prompting stricter regulations

Tokyo University of Science revealed that ultra-small silica nanoparticles alter protein secondary structures, increasing β-sheet content linked to neurodegeneration. Water-treatment plants struggle to capture sub-50 nm particles, leading to accumulation in aquatic ecosystems. The European Union broadened REACH to mandate full life-cycle safety files for nanomaterials, stretching product qualification timelines and raising compliance costs. Manufacturers unable to furnish chronic toxicity data risk delayed market entry, tempering near-term expansion of the Metal oxide nanoparticles market.

Lack of standardized nano-scale metrology across supply chains

Inter-laboratory tests show particle-size readings can diverge by 20% despite identical instrumentation, underscoring the need for certified reference materials. Non-uniform reporting complicates regulatory reviews and forces buyers to pad specifications, increasing scrap risk. NIST is developing calibration artefacts and best-practice guides to close these gaps. Until adoption becomes widespread, measurement uncertainty will continue to challenge just-in-time delivery models in the Metal oxide nanoparticles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Titanium Dioxide anchors electronics demand

Titanium Dioxide retained a 38.20% stake in the Metal oxide nanoparticles market in 2025, buoyed by dual roles in UV-blocking sunscreens and 5 nm gate dielectrics. Over 98% visible-light transmission photoresists rely on TiO₂’s high refractive index, keeping defect densities below 0.3 cm^-2 in extreme-ultraviolet lithography. Magnesium Oxide posts the fastest CAGR at 7.78% through 2031, propelled by its ability to stabilise ceramic electrolytes at 300 °C. Silicon Dioxide broadens its reach into additive manufacturing powders, while Zinc Oxide expands inside antimicrobial polymer films. These shifts keep product differentiation high and support value capture inside the Metal oxide nanoparticles market.

Japanese plasma-spray breakthroughs now deliver TiO₂ nanoparticles averaging 40 nm at 12.3 g/min throughput, closing the scale gap between pilot and mass production. Aluminum Oxide’s presence in separator coatings and ceramic substrates further entrenches its role, especially following Evonik’s capacity build-out. Copper and Iron Oxides occupy catalysis and magnetic-storage niches, and ceria or zirconia oxides serve fuel cell and high-temperature turbine markets. The resulting portfolio complexity encourages strategic sourcing programs that balance cost, purity and functional performance, bolstering resilience across the Metal oxide nanoparticles industry.

By Synthesis Method: Chemical routes dominate, bio-based gains pace

Chemical processes constitute 62.55% of 2025 production as sol-gel, precipitation and CVD lines guarantee parts-per-billion impurity control. These mature platforms underpin semiconductor node migrations, anchoring the Metal oxide nanoparticles market. Yet bio-based synthesis is set for 7.89% CAGR, catalysed by policy incentives and early adopter demand from personal-care brands seeking eco-labels. Pilot units using citrus peel extracts now produce ZnO nanorods with 30 nm mean diameters and consistent aspect ratios below 2.5, matching optoelectronic grade standards.

Hybrid workflows that blend biological templates with downstream chemical calcination offer tunable surface functionalisation useful in targeted drug delivery. Physical techniques such as mechanical milling or pulsed-laser vaporisation keep a foothold where unique morphologies are needed, for instance in thermally conductive fillers. As metrology protocols converge, parity in specification language between green and conventional powders will expand purchasing options, intensifying competition inside the Metal oxide nanoparticles market.

By End-User Industry: Electronics leads while energy accelerates

Electronics and optics applications captured 42.10% of the Metal oxide nanoparticles market size in 2025. Multi-chiplet packaging architectures hinge on ultra-pure oxide layers that isolate heat-generating dies, and display makers deploy nanoparticle inks for bendable touch sensors. Government allocations of USD 1.7 billion for semiconductor materials in North America directly boost procurement.

Energy & environment is the fastest riser at 8.32% CAGR. Lithium-ion cell makers coat separators with alumina nanosheets only 30 nm thick, reducing thermal runaway by 60%. Solid-state electrolyte prototypes featuring sulfide-stabilised zirconia nanoparticles hit cycle lives beyond 1,000 charges at 25 °C. Healthcare gains from metal-oxide-mediated photodynamic therapies, while construction adopts nanoparticle-enhanced cement that extends service life in coastal infrastructure. This diversified pull cements long-term relevance for the Metal oxide nanoparticles industry.

Geography Analysis

Asia-Pacific held 47.40% of the Metal oxide nanoparticles market in 2025 and is poised for 7.55% CAGR through 2031. China’s titanium dioxide capacity nears 7 million tons following multi-province expansions, yet anti-dumping actions by the EU and Brazil tighten margins. Japan’s universities pioneer magnetic nanoparticle therapies for cancer and improve defect detection in powder batches, reinforcing domestic high-value demand. South Korea and Taiwan leverage oxide purity to sustain foundry competitiveness, and India grows output for sunscreens and architectural coatings. End-to-end electronics ecosystems and targeted subsidies preserve the region’s primacy within the Metal oxide nanoparticles market.

North America benefits from CHIPS Act funding that underwrites polysilicon and substrate projects, pulling local oxides into advanced-packaging supply chains. Hemlock Semiconductor’s USD 325 million Michigan investment will ship 59,000 metric tons of hyper-pure polysilicon annually, each ingot doped with metal oxide trace additives. Extensive R&D activity translates to early adoption of bio-based synthesis, while aerospace primes demand for radiation-hard oxides. Cross-border integration with Canada’s mining and Mexico’s assembly plants underpins a resilient regional Metal oxide nanoparticles market.

Europe prioritises sustainability and compliance. REACH nano-amendments motivate automakers to source low-carbon alumina for clear-coat formulations, and aerospace primes ceramic-matrix composite investments that rely on yttria-stabilised zirconia nanopowders. Germany leads industrial throughput, while Nordic nations incubate circular-economy pilots reclaiming oxides from end-of-life batteries. Middle East and Africa build construction and solar projects that integrate nanoparticle additives for heat-reflective paints. South America deploys oxides to enhance ore beneficiation and fertiliser efficiency, adding incremental volumes to the Metal oxide nanoparticles market.

Competitive Landscape

The Metal oxide nanoparticles market remains moderately fragmented. Large integrated players such as Evonik, Sumitomo Chemical and American Elements leverage controlled precursor chains to guarantee semiconductor-grade purity, while niche specialists like SkySpring Nanomaterials tailor coatings for magnetic data storage. Consolidation prospects increase as OEMs simplify approved-vendor lists, valuing suppliers able to cover multiple oxide families under uniform quality systems.

Process innovation serves as a strategic differentiator. Evonik’s fumed alumina line in Japan exemplifies CAPEX directed at fast-growing battery segments, while American Elements expands IP around oxide-coated silicon anodes. Patent filings in pulse-modulated plasma synthesis and bio-templated routes underscore active R&D rivalry.

Metal Oxide Nanoparticles Industry Leaders

American Elements

Nanoshell LLC

Meliorum Technologies, Inc.

Evonik Industries AG

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: A research group from the Hefei Institutes of Physical Science, part of the Chinese Academy of Sciences, has made strides in enhancing localized surface plasmon resonance (LSPR). Their study focused on Cu₂O₁₋ₓ superlattices with oxygen vacancies, shedding light on the nuances of vacancy doping in semiconductors and the induction of LSPR in metal oxide nanoparticles.

- February 2025: Matexcel, a prominent player in material science solutions, has broadened its product portfolio, now offering a wider array of metal oxide nanoparticles. This move underscores Matexcel's dedication to providing top-tier, advanced materials, bolstering sectors like electronics, energy, catalysis, and biomedicine.

Global Metal Oxide Nanoparticles Market Report Scope

The metal oxide nanoparticles market report includes:

| Aluminium Oxide |

| Titanium Dioxide |

| Silicon Dioxide |

| Zinc Oxide |

| Magnesium Oxide |

| Copper Oxide |

| Iron Oxide |

| Others (Cerium, Zirconium, etc.) |

| Physical (Mechanical Milling, Vapor Deposition) |

| Chemical (Sol-Gel, Precipitation) |

| Green / Bio-based |

| Electronics and Optics |

| Healthcare |

| Construction |

| Automotive and Transportation |

| Personal Care |

| Other End-user Industries (Energy and Environment, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product | Aluminium Oxide | |

| Titanium Dioxide | ||

| Silicon Dioxide | ||

| Zinc Oxide | ||

| Magnesium Oxide | ||

| Copper Oxide | ||

| Iron Oxide | ||

| Others (Cerium, Zirconium, etc.) | ||

| By Synthesis Method | Physical (Mechanical Milling, Vapor Deposition) | |

| Chemical (Sol-Gel, Precipitation) | ||

| Green / Bio-based | ||

| By End-User Industry | Electronics and Optics | |

| Healthcare | ||

| Construction | ||

| Automotive and Transportation | ||

| Personal Care | ||

| Other End-user Industries (Energy and Environment, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current Metal Oxide Nanoparticles Market size?

The Metal Oxide Nanoparticles Market stands at USD 1.11 billion in 2026 and is projected to reach USD 1.54 billion by 2031 at a 6.74% CAGR.

Which product segment dominates the Metal oxide nanoparticles market?

Titanium Dioxide leads, holding 38.20% share in 2025.

Which region shows fastest growth in the Metal oxide nanoparticles market?

Asia-Pacific grows at 7.55% CAGR due to concentrated semiconductor fabrication and supportive government incentives.

How do metal oxide nanoparticles enhance lithium-ion batteries?

They improve cathode conductivity, stabilise solid-state electrolytes and mitigate anode volume expansion, boosting safety and energy density.

Page last updated on: