Meta-Xylene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

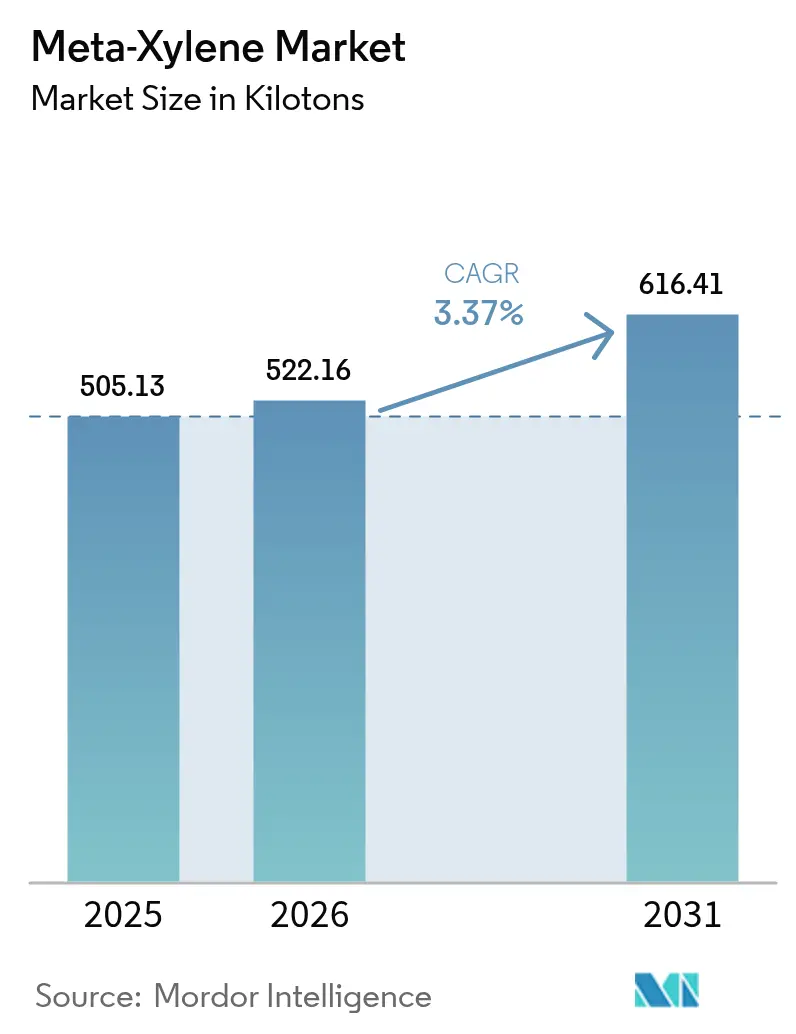

| Market Volume (2026) | 522.16 kilotons |

| Market Volume (2031) | 616.41 kilotons |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

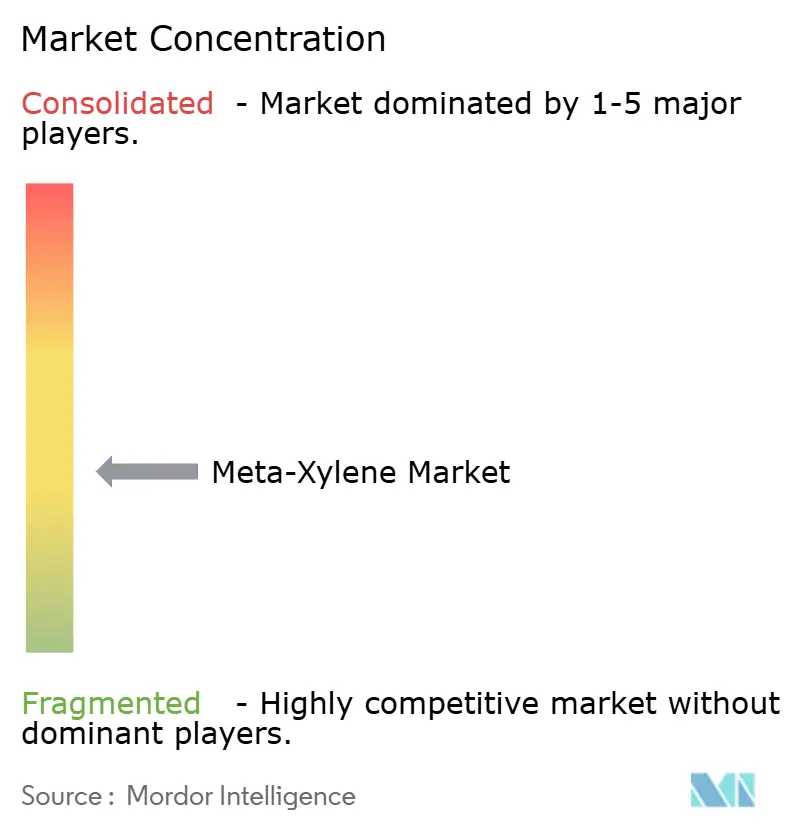

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meta-Xylene Market Analysis by Mordor Intelligence

The Meta-Xylene market size is expected to grow from 505.13 kilotons in 2025 to 522.16 kilotons in 2026 and is forecast to reach 616.41 kilotons by 2031 at 3.37% CAGR over 2026-2031. Sustained PET and unsaturated polyester resin (UPR) consumption, together with a shift toward low-VOC and bio-based coating ingredients, underpins volume growth as producers leverage meta-xylene’s role as the sole feedstock for isophthalic acid. Capacity additions inside integrated aromatics complexes across China, India, and the Middle East keep supply aligned with demand, while advanced extraction technologies lower unit costs and improve purity thresholds. On the demand side, regulatory pressure to curb solvent emissions is simultaneously reducing overall solvent volumes yet elevating the value of meta-xylene’s balanced evaporation rate in premium, high-solids paints. As crude price volatility continues to influence aromatics spreads, the evolving dynamics among multinational energy-chemical giants and regional champions are reshaping the competitive landscape.

Key Report Takeaways

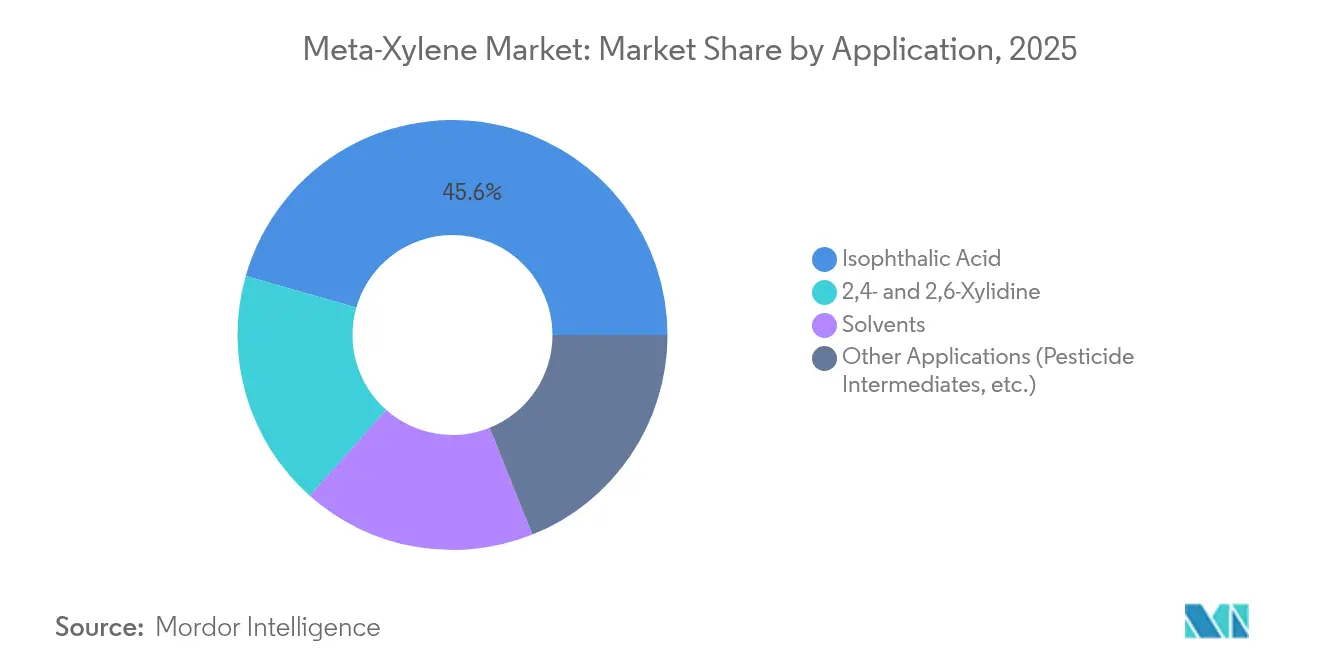

- By application, isophthalic acid commanded 45.58% of meta-xylene market share in 2025, whereas bio-based isophthalic acid is expected to register the fastest 6.72% CAGR through 2031.

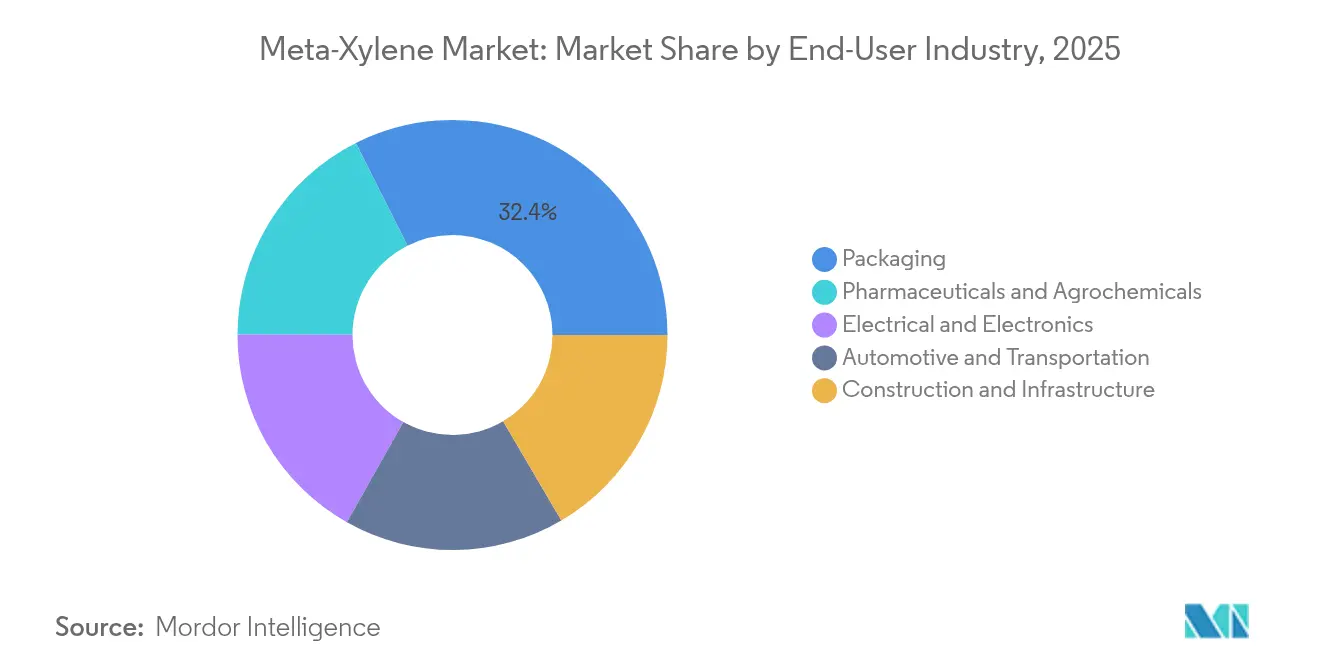

- By end-user industry, the packaging sector led with 32.42% revenue share in 2025; pharmaceuticals and agrochemicals are forecast to expand at the highest 5.62% CAGR to 2031.

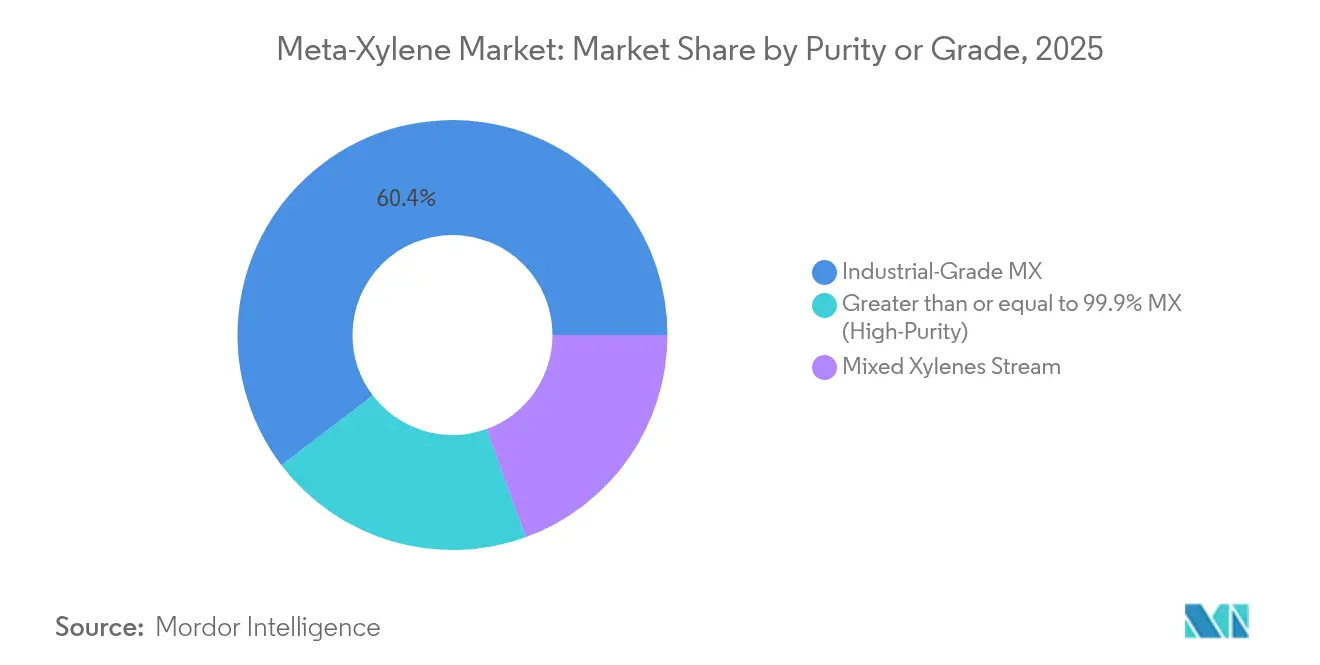

- By purity/grade, industrial grade held 60.35% of the meta-xylene market size in 2025, while greater than or equal to 99.9% high-purity grades are poised for a 6.95% CAGR between 2026-2031.

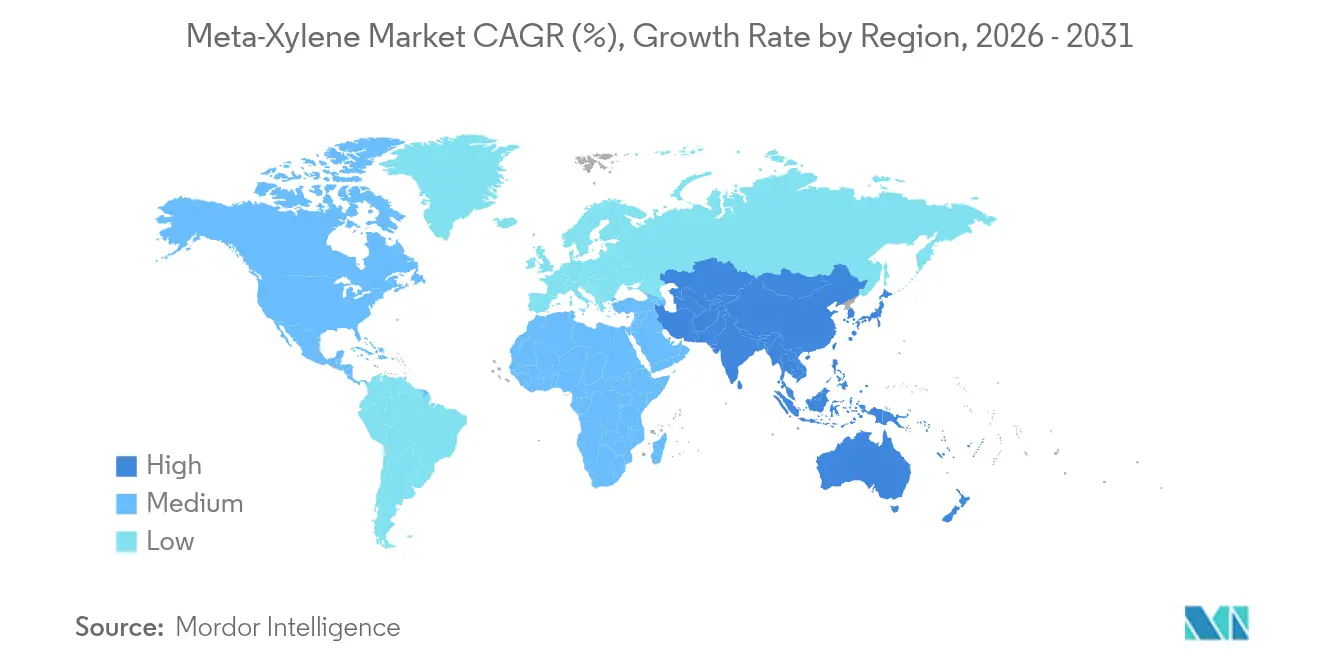

- By region, Asia-Pacific contributed 52.98% of global volume in 2025, and the region is projected to grow at a 5.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meta-Xylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for isophthalic acid in PET & UPR production | +1.20% | Global, Asia-Pacific core | Medium term (2-4 years) |

| Shift toward high-solids/low-VOC industrial coatings | +0.80% | North America & EU, spill-over to APAC | Long term (≥4 years) |

| Capacity expansions in integrated PX-MX aromatics complexes | +1.00% | APAC core, spill-over to MEA | Short term (≤2 years) |

| Increasing demand from paints and coatings sector | +0.60% | Global | Medium term (2-4 years) |

| Expansion of the automotive sector | +0.40% | Global, early gains in China & India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Isophthalic Acid in PET & UPR Production

Isophthalic acid enhances thermal stability and gas-barrier performance in modified PET, making it indispensable for premium bottles, films and industrial fibers. Automotive and electronics manufacturers specify isophthalic acid-modified PET when temperatures exceed standard PET thresholds, reinforcing pull-through demand for meta-xylene. Innovation pipelines increasingly rely on renewable feedstocks such as 5-hydroxymethylfurfural (HMF); once commercial scale is reached, bio-based routes are expected to capture share within the next decade as brand owners pursue carbon-reduction goals. In UPR, isophthalic acid delivers higher corrosion resistance in wind‐turbine nacelles and marine composites, supporting structural applications growth across Asia-Pacific shipyards and European offshore installations. The dual demand from PET and UPR accordingly registers the strongest positive impact on the meta-xylene market trajectory.

Shift Toward High-Solids/Low-VOC Industrial Coatings

The United States Environmental Protection Agency’s 2024 Hazard Communication Standard update tightened labeling norms for xylene derivatives, pushing formulators toward higher-solids systems that still rely on meta-xylene for effective viscosity control[1]United States OSHA, “Hazard Communication Standard Final Rule,” osha.gov . Europe’s decarbonization roadmap similarly incentivizes low-VOC coatings, driving substitution of lighter, faster-evaporating solvents in favor of meta-xylene’s more moderate evaporation profile. Although waterborne paints reduce aggregate solvent volumes, premium architectural and industrial maintenance products continue to incorporate meta-xylene as a coalescent aid, preserving demand through the forecast period.

Capacity Expansions in Integrated PX-MX Aromatics Complexes

Mega-complexes such as Zhejiang Petroleum & Chemical’s 11.8 million t/y aromatics hub in Zhoushan optimize para-xylene and meta-xylene output through advanced extractive distillation, cutting unit energy use by up to 20% versus legacy plants. Honeywell UOP’s Eluxyl technology further reduces capital intensity, enabling financially competitive projects in the Middle East and Southeast Asia. Integration into steam crackers and downstream PTA, resin, and fiber lines locks in captive demand and protects margins—even during crude price downturns—thereby supporting construction of additional capacity across India’s USD 87 billion petrochemical pipeline.

Increasing Demand from Paints and Coatings Sector

Automotive refinishing, heavy-duty marine coatings and infrastructure refurbishment all require solvents with balanced dissolution power and evaporation rates. Meta-xylene meets these specifications, ensuring consistent film build and leveling. Powder-coating adoption reduces solvent use overall, yet primer and adhesion-promoter niches preserve sizable volume opportunities, particularly as emerging economies widen their vehicle fleets. Smart-coating formulations that embed nanoparticles or corrosion sensors benefit from the chemical compatibility meta-xylene offers with advanced additive systems, keeping the solvent integral to specialty product chemistries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicological & flammability profile driving stricter exposure limits | -0.40% | Global, early implementation in EU & North America | Short term (≤2 years) |

| Crude-oil price volatility cascading to aromatics spreads | -0.60% | Global | Short term (≤2 years) |

| Capital-intensive isomer separation technology deterring newcomers | -0.30% | Global, with higher barriers in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicological & Flammability Profile Driving Stricter Exposure Limits

The Agency for Toxic Substances and Disease Registry (ATSDR) underscores neurological concerns linked to chronic xylene exposure, prompting European regulators to contemplate lowering the 8-hour TWA occupational limit[2]ATSDR, “Toxicological Profile for Xylene,” atsdr.cdc.gov . Implementing enhanced ventilation, spark-proof handling systems, and personal protective equipment raises production costs, especially for small or standalone facilities. Where viable, coatings producers experiment with alternative solvents, yet meta-xylene’s unique solvency and processing characteristics hinder full substitution, tempering but not eliminating demand.

Crude-Oil Price Volatility Cascading to Aromatics Spreads

Geopolitical supply disruptions and OPEC+ output decisions accentuated crude price swings in early 2025, compressing margins for non-integrated aromatics producers. South Korean petrochemical firms reported double-digit profit contractions in 2024 as feedstock costs climbed and regional oversupply intensified competition. Integration with upstream refining and diversified downstream outlets, therefore, remains critical for sustaining profitability, and cash-negative assets face rationalization or consolidation in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bio-Based Routes Challenge Traditional Pathways

Isophthalic acid production accounted for the largest share of the meta-xylene market size, at 45.58% in 2025, underscoring the segment’s entrenched role in high-performance PET bottles and corrosion-resistant UPR laminates. The progressive switch toward bio-based isophthalic acid, projected to grow at 6.72% CAGR to 2031, signals a structural realignment in feedstock sourcing as renewable chemistries enter commercial deployment. Early adopters in Europe and Japan already certify mass-balance routines to capture brandowner premiums, while Asian producers erect greenfield units adjacent to biomass supply corridors.

Over the medium term, pesticide and pharmaceutical intermediates derived from 2,4- and 2,6-xylidine will preserve niche demand despite regulatory concerns around toxicology. Solvent applications shrink in absolute tonnage but exhibit value resilience where specialty electronics and pharmaceutical cleaning require meta-xylene’s narrow boiling range. Taken together, the application mix is migrating from bulk solvent dependency toward higher-margin resin and specialty chemical use, elevating overall profitability despite moderate headline growth.

By End-User Industry: Pharmaceuticals Drive Premium Demand

Packaging held a 32.42% share of the meta-xylene market in 2025, reflecting its central place in food-contact bottles and flexible films that rely on modified PET for enhanced gas barrier properties. Pharmaceuticals and agrochemicals are anticipated to expand at the fastest 5.62% CAGR, propelled by surging generic drug output in India and ASEAN and by stringent purity specifications that favor greater than or equal to 99.9% grades.

Construction coatings, civil infrastructure sealants, and pipe relining compounds absorb considerable industrial-grade volumes, yet growth correlates with national infrastructure budgets and remains cyclical. Automotive OEM and refinish lines sustain steady demand as rising vehicle production combines with stricter durability standards. The electronics sector, meanwhile, underpins premium demand for ultra-pure meta-xylene used in semiconductor wafer cleaning, where sub-ppm impurities can compromise device yield.

By Purity/Grade: High-Purity Grades Capture Value Premium

Industrial grade continues to dominate with 60.35% of meta-xylene market share in 2025, supplying bulk solvents, resin intermediates, and gasoline blending streams. Advanced grades at greater than or equal to 99.9% purity are projected to register the strongest 6.95% CAGR, illustrating buyers’ willingness to pay for specification consistency in pharmaceuticals, microelectronics, and photo-initiator synthesis.

Molecular-sieve adsorption, simulated moving bed (SMB), and extractive distillation technologies enable producers to achieve these purity levels, but capital intensity bars smaller players from entry. Investment, therefore, clusters among integrated majors and technology licensors, reinforcing the market’s gradual bifurcation into commodity and specialty tiers. The margin delta between grades compensates investors for higher operating costs while meeting end-user quality mandates.

Geography Analysis

Asia-Pacific captured 52.98% of global volumes in 2025 and is forecast to clock a 5.32% CAGR through 2031, driven by vertically integrated complexes across China and India that harness feedstock flexibility and scale economics. China’s Zhoushan aromatics hub and Guangdong CNOOC-Shell joint venture each broaden regional self-sufficiency, curbing import requirements from the United States and Europe. India’s USD 87 billion petrochemical blueprint seeks to raise domestic xylene capacity to 5.5 million t by 2035, securing raw material availability for downstream polyester, coatings, and pharma corridors. Japan and South Korea confront structural margin pressure as Chinese exports intensify competition, spurring these economies to pivot toward high-purity specialties and differentiated formulations.

North America retains strategic significance through superior separation technologies, abundant shale-derived naphtha and proximity to a vast coatings customer base. However, upward pressure on energy costs and tightening environmental compliance increase operating expenditure. Chevron’s potential USD 15 billion acquisition of Phillips 66’s CPChem stake underscores the region’s consolidation trajectory as companies chase scale and feedstock integration benefits. Mexico’s emerging automotive value chain stimulates solvent and resin demand but relies heavily on United States imports, illustrating the importance of the USMCA’s tariff stability.

Europe confronts the steepest operating challenges, with high utility costs and stringent carbon policies discouraging fresh investment in commodity aromatics. The European Green Deal’s evolving carbon-border adjustment mechanism may partially shield domestic output yet adds administrative complexity. Shell’s announcement to exit base chemicals by 2030 typifies how international energy majors reallocate capital toward LNG and renewables. Remaining European producers emphasize bio-based isophthalic acid and circular PET feedstocks, capitalizing on regulatory incentives for climate-neutral materials.

Value Chain Analysis

Meta-xylene supply is anchored in the C8 aromatics chain, starting with crude oil and natural gas liquids that move through refining and steam cracking to generate reformate and pyrolysis gasoline streams containing mixed xylenes. Producers recover mixed xylenes via fractionation, then separate meta-xylene using capital-intensive isomer separation steps such as selective adsorption (for example, Sorbex-type systems) or crystallization, often coupled with isomerization to manage equilibrium constraints and maximize target isomer yields. This structure favors integrated refinery-petrochemical sites and technology-enabled operators that can consistently meet industrial and >=99.9% purity specifications.

Downstream, the largest pull-through route remains conversion of meta-xylene into isophthalic acid for modified PET, unsaturated polyester resins, and specialty coatings, with additional demand from xylidine-based intermediates and solvent use. Distribution typically runs from integrated producers and regional aromatics traders to isophthalic acid manufacturers and specialty chemical formulators, with handling requirements shaped by flammability and exposure controls that add logistics and compliance costs. Mitsubishi Gas Chemical Company is a named producer with meta-xylene production at its Mizushima Plant, illustrating how supply participation clusters among established chemical manufacturers with integrated assets and quality systems.

Competitive Landscape

The meta-xylene market is moderately fragmented, anchored by integrated oil-to-aromatics conglomerates that leverage scale and captive feedstocks. Strategic transactions accelerate as majors refine portfolios: Chevron’s interest in CPRing CPChem strengthens its resin and specialty chemicals footprint, while Shell’s pivot away from base chemicals frees capital for LNG and power. Technology providers such as Honeywell UOP, Axens, and GTC Technology license extractive distillation and SMB solutions, enabling licensees to reach cost-effective purity thresholds and shortening time-to-market. Mitsubishi Chemical Group’s KAITEKI Vision 35 highlights an organizational shift toward green specialty materials, including high-purity aromatics for electronics.

White-space opportunities exist in bio-based production, where start-ups leverage fermentation or catalytic oxidation of renewable feedstocks to yield isophthalic acid and eventually meta-xylene itself. While current capacities remain pilot-scale, brandowner ESG commitments and potential carbon pricing differentials could make these routes cost-competitive within the decade. Success hinges on intellectual property, selective hydrogenation catalysts, and the ability to secure offtake agreements with consumer-product multinationals.

Meta-Xylene Industry Leaders

Exxon Mobil Corporation

Honeywell International Inc.

MITSUBISHI GAS CHEMICAL COMPANY, INC.

Chevron Phillips Chemical Company LLC

Moeve

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity area sits in higher-purity meta-xylene value pools, where >=99.9% grades support pharmaceuticals, agrochemicals, and electronics applications that require tighter impurity control than bulk solvent markets. This connects to the market mix shift described in the report, where industrial grade still dominates volume but premium grades capture incremental value, supporting demand for adsorption and extractive-distillation upgrades within integrated aromatics complexes rather than standalone commodity capacity.

Sustainability-linked differentiation is also creating whitespace around certified, lower-carbon feedstock claims in the aromatics chain. Mitsubishi Gas Chemical Company obtaining ISCC PLUS certification for meta-xylene produced at its Mizushima Plant (September 2024) provides an anchor for mass-balance positioning, with downstream isophthalic acid and PET users able to document renewable-content claims. In Asia-Pacific, ongoing integration and self-sufficiency efforts, including large-scale aromatics hubs in China (for example, Zhoushan) and India’s stated petrochemical blueprint to lift xylene capacity to 5.5 million t by 2035, are reshaping trade flows and creating procurement opportunities for downstream resin and coating producers located near C8 aromatics supply.

Recent Industry Developments

- June 2026: US isophthalic acid pricing softened as feedstock xylene costs moved lower and buying activity weakened. The episode highlighted how aromatics cost swings transmit into the largest meta-xylene derivative chain, tightening the link between integrated supply economics and downstream resin and packaging margins.

- January 2025: OPEC+ output decisions and geopolitically driven disruptions amplified crude volatility into early 2025, pressuring naphtha-to-aromatics spreads for non-integrated producers. Integrated refining-aromatics operators gained a relative advantage by balancing reformate and C8 aromatic optimization against fuel blending alternatives.

- September 2024: Mitsubishi Gas Chemical Company obtained ISCC PLUS certification for meta-xylene produced at its Mizushima Plant under a mass-balance approach. The certification enabled renewable-content claims for buyers in isophthalic acid, coatings, and other specialty chains that increasingly require auditable sustainability documentation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers meta xylene volumes supplied to end users for use as a chemical feedstock and solvent, measured in kilotons at the global level across major consuming regions.

Scope exclusions: We exclude internal transfers that do not translate into marketable volumes, and we also exclude value-added downstream derivatives such as isophthalic acid and finished resins.

Segmentation Overview

- By Application

- Isophthalic Acid

- 2,4- and 2,6-Xylidine

- Solvents

- Other Applications (Pesticide Intermediates, etc.)

- By End-user Industry

- Construction and Infrastructure

- Packaging

- Automotive and Transportation

- Pharmaceuticals and Agrochemicals

- Electrical and Electronics

- By Purity/Grade

- Greater than or equal to 99.9 % MX (High-Purity)

- Industrial-Grade MX

- Mixed Xylenes Stream

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set industry boundaries and to build the first pass of the supply and demand picture. We referred to public chemical and energy statistics and trade flows to understand how aromatics move through refineries and petrochemical chains, then checked how much of the xylene pool is typically routed toward meta xylene.

Sources included non-paywalled materials such as national customs and statistics portals, energy and petrochemical publications from intergovernment bodies, environmental agency releases on VOC rules, and peer-reviewed chemistry and process journals that describe separation routes and purity requirements. We also reviewed company filings, investor presentations, and association websites to align operating-rate commentary with market direction, and we used a paid subscription focused on company financials and intelligence plus a patent database to cross-check capacity announcements and process changes. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around real operating rates, purity mix, and how contract versus spot availability shifts by region. We spoke with a mix of producers, distributors, and downstream buyers so that volume allocations by application could be corrected where published splits were too broad, and we ensured coverage across Asia, Europe, and the Americas to avoid a single-region view driving the global total.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 43% | EMEA: 31% |

| Smaller Players: 21% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of the global meta xylene pool, where aromatics production indicators and trade balances are used to infer the available xylene stream and the share separated into meta xylene. Once that pool is built, it is allocated to applications using a mix of secondary splits and what we heard in interviews, which are then reconciled against downstream demand signals.

To keep the model practical, inputs focus on a small set of trackable variables such as aromatics and mixed xylene output trends, regional import and export movements, announced and effective operating rates at separation units, typical purity or grade requirements by end use, and demand pull from isophthalic acid and solvent use patterns. After the top-down pass, selective bottom-up approximations were used as checks, including sampled capacity to utilization rollups and sanity checks of implied consumption versus trade availability in key regions. Where bottom-up detail was missing, we filled gaps with conservative utilization bands and then revalidated them through channel feedback.

Forecasting relied on scenario analysis supported by simple time-series smoothing, where expected changes in operating rates, trade direction, and downstream demand were applied as the main levers. Assumptions were kept consistent across regions, and only adjusted when primary inputs indicated a structural change such as a capacity addition, shutdown, or a sustained logistics constraint.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, and then variances were investigated before finalizing numbers. Our team compared implied consumption against trade and production indicators, and outliers were reviewed region by region so that one abnormal datapoint did not distort the global line.

If a variance could not be explained with public evidence, respondents were re-contacted to confirm whether the issue was timing, purity mix, or a temporary operating disruption. A separate analyst review is completed before sign-off, followed by an annual refresh cycle with interim updates when material events occur, and a final pre-delivery review is done so clients receive the latest updated view.

Mordor Intelligence's Meta Xylene Market Size Versus Other Published Estimates

Published market sizes for meta xylene can look far apart because the market is sometimes expressed in value versus volume, and because the boundary between mixed xylene, meta xylene, and downstream derivatives is not always handled the same way. Timing also matters, since some sources use older base years and do not fully adjust for shifts in trade flows or short-term operating rate changes.

By tracking operating rates, trade balances, and separation yield assumptions and then refreshing the boundary rules, Mordor Intelligence keeps the estimate tied to marketable meta xylene volumes in kilotons rather than folding in downstream derivative revenue. In a chemicals chain like this, a common gap driver is whether solvent-grade material is counted alongside high-purity volumes, and whether the model allocates demand based on end-use consumption signals versus announced capacity alone.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 505.13 M (2025) | |

| Trade Publisher A | USD 1.41 B (2024) | Reported in revenue terms and may include broader pricing and value-chain assumptions, which can also pull in value from downstream derivatives rather than isolating traded meta xylene volumes. |

| Industry Report B | USD 1.50 B (2024) | Uses a revenue model with a different base year and longer forecast window, and the scope often blends technology routes and end-use buckets that can expand what is counted under meta xylene. |

The spread in the table is mainly explained by unit choice and boundary setting, since a volume-based view in kilotons will not line up with revenue totals that depend on ASP paths and what parts of the chain are included. Our approach stays repeatable by tying each step back to observable production, trade, and operating signals, and then cross-checking those totals with application allocations validated through interviews.

Key Questions Answered in the Report

What is the current size of the meta-xylene market?

The meta-xylene market stands at 522.16 kilotons in 2026 and is forecast to rise to 616.41 kilotons by 2031 at a 3.37% CAGR.

Which application segment dominates meta-xylene demand?

Isophthalic acid production commands 45.58% share, making it the leading application segment.

Why is Asia-Pacific the largest regional market for meta-xylene?

Asia-Pacific hosts integrated aromatics complexes in China and India, securing 52.98% of global volumes and recording the fastest 5.32% CAGR.

How are sustainability trends influencing the meta-xylene market?

Bio-based isophthalic acid is growing at 6.72% CAGR as producers adopt renewable feedstocks to meet brand-owner carbon targets, while high-solids coatings bolster demand for meta-xylene’s balanced solvency.

What purity grades of meta-xylene are gaining traction?

Greater than or equal to 99.9% high-purity grades are projected to post a 6.95% CAGR through 2031, driven by electronics and pharmaceutical uses that demand ultra-low impurity levels.

How do crude oil price fluctuations affect meta-xylene producers?

Volatile crude prices squeeze naphtha-to-aromatics spreads, pressuring margins for non-integrated producers and accelerating consolidation toward players with refining integration and advanced separation technologies.

Page last updated on: