Mental Health Apps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

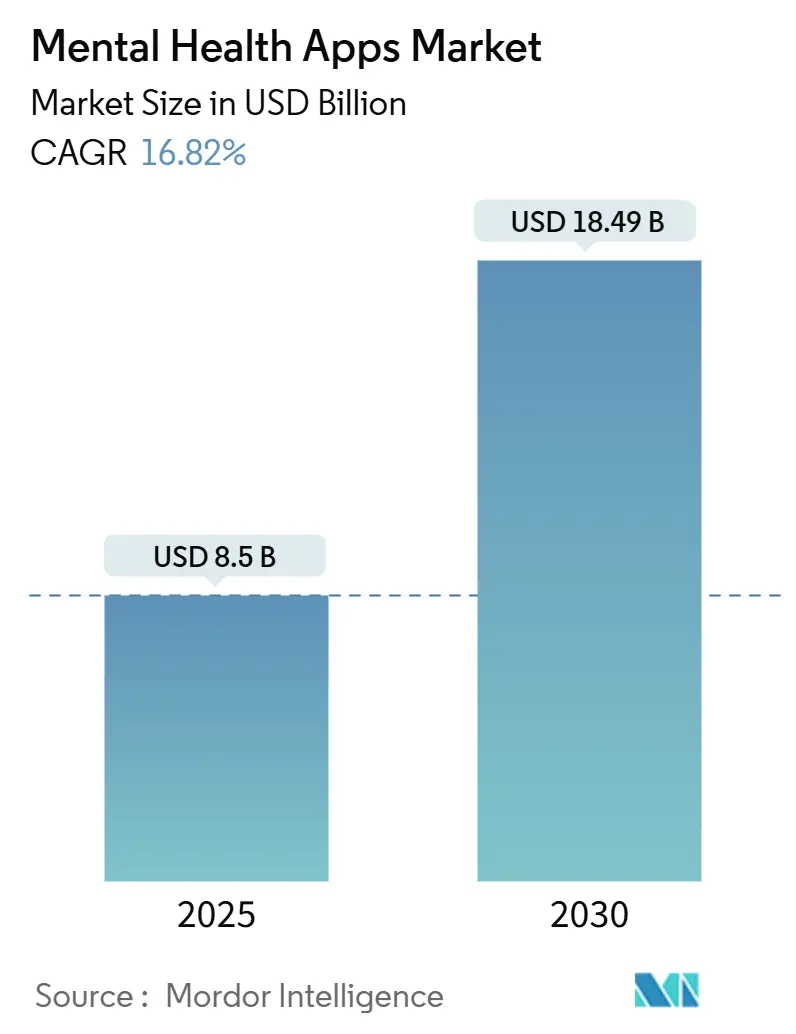

| Market Size (2025) | USD 8.5 Billion |

| Market Size (2030) | USD 18.49 Billion |

| Growth Rate (2025 - 2030) | 16.82% CAGR |

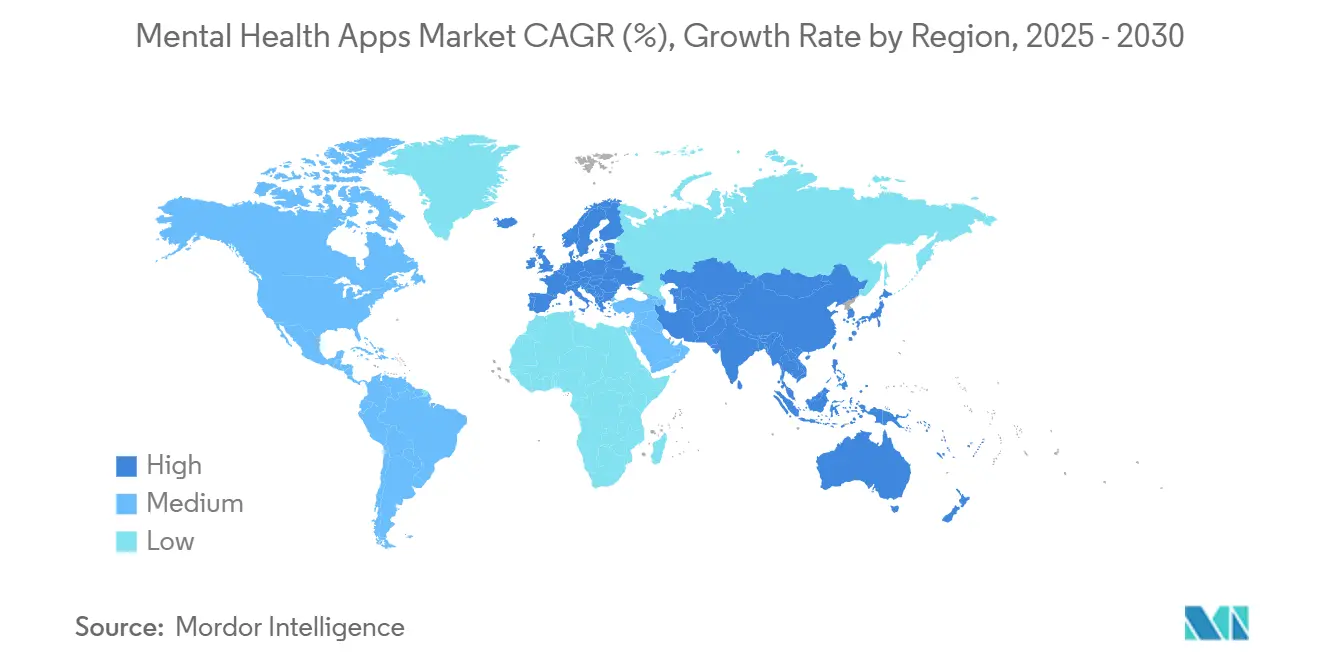

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

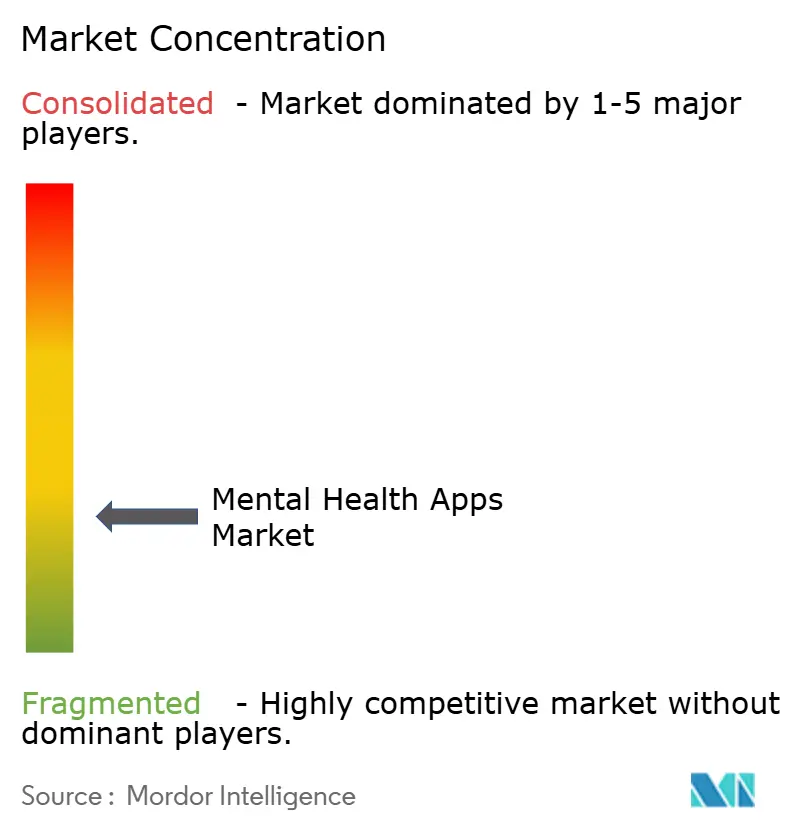

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mental Health Apps Market Analysis by Mordor Intelligence

The mental health apps market size is estimated at USD 8.50 billion in 2025, and is expected to reach USD 18.49 billion by 2030, at a CAGR of 16.82% during the forecast period (2025-2030). Momentum is building as smartphones place clinical-grade tools in pockets, employers link psychological safety to productivity, and payers broaden reimbursement for virtual care. Venture funding continues to flow into digital therapeutics that marry artificial intelligence with cognitive-behavioral protocols, while 5G networks cut latency for video counseling and biometric streaming. Regulatory attention around data protection is accelerating product design improvements, and evidence-based solutions are starting to displace gamified wellness apps that lack clinical rigor. Competitive intensity is rising as consumer brands, tele-psychiatry networks, and start-ups converge on the same user base, prompting differentiation through clinical validation, language localization, and integration with electronic health records.

Key Report Takeaways

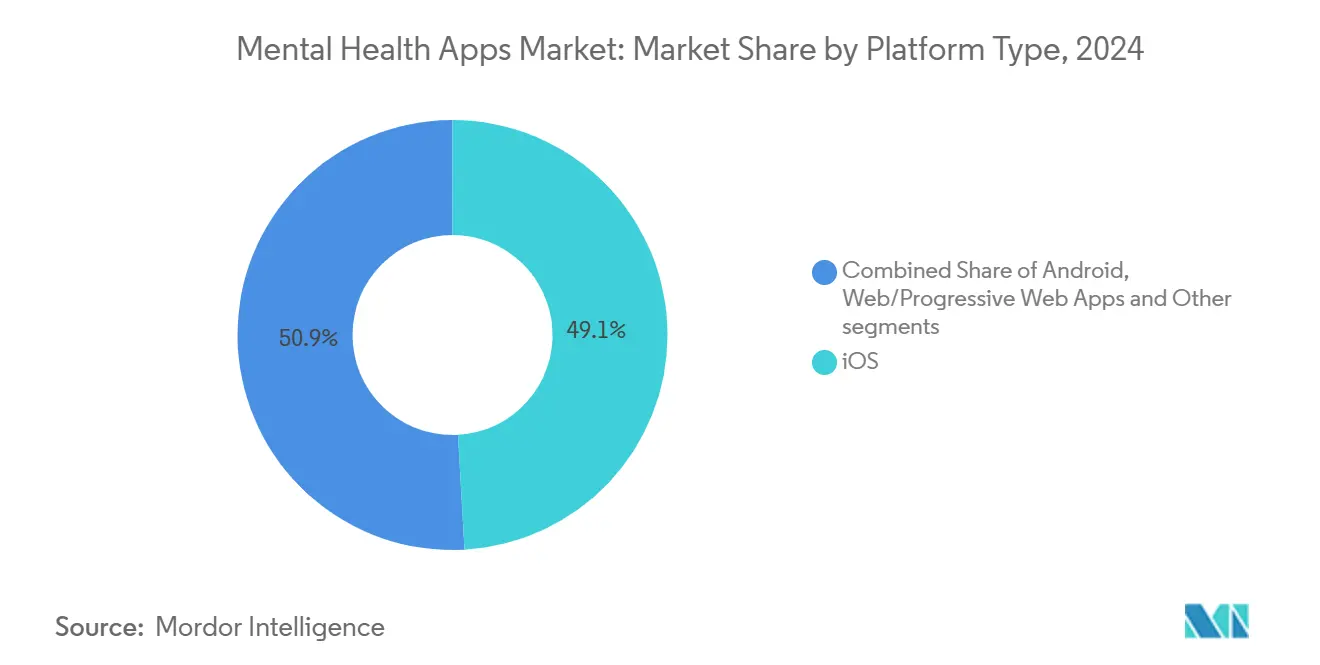

- By platform type, iOS led with 49.12% revenue share in 2024; Android is forecasted to expand at an 18.94% CAGR to 2030.

- By application, depression and anxiety management captured 30.78% of the mental health apps market share in 2024, while stress management is advancing at an 18.53% CAGR to 2030.

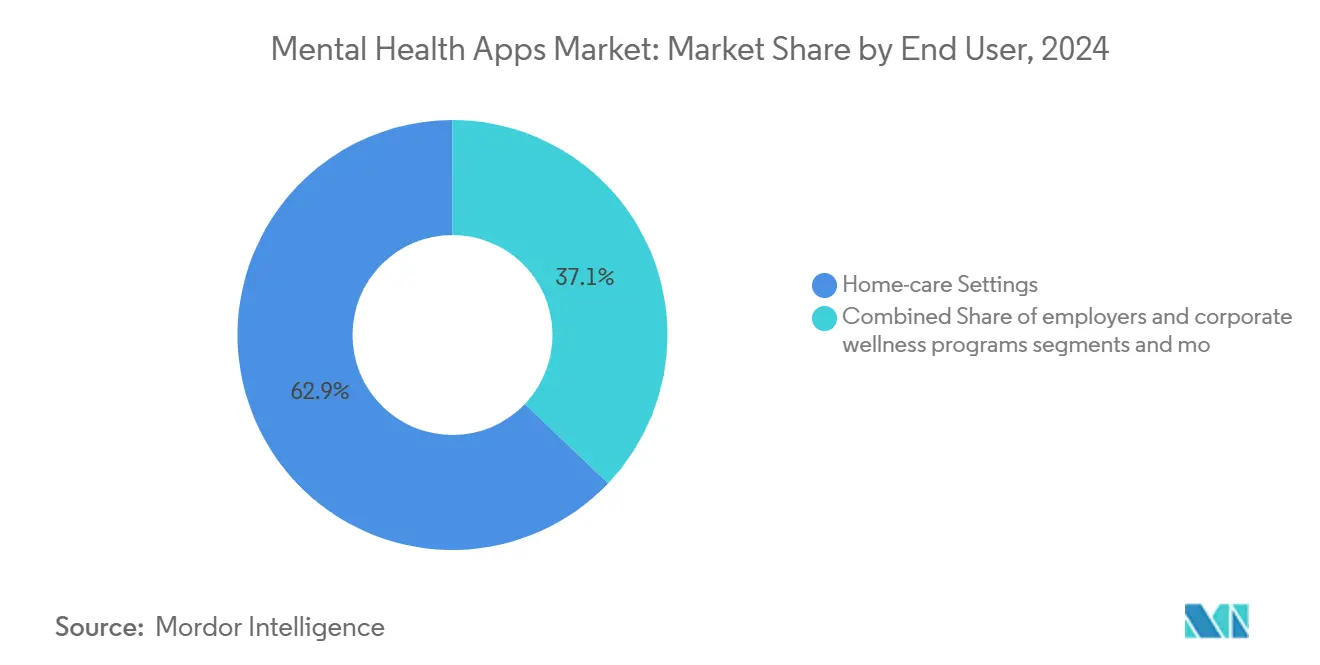

- By end user, home-care settings held 62.86% of the mental health apps market size in 2024; employers and corporate wellness programs record the fastest projected CAGR at 17.68% to 2030.

- By age group, adults (18-64 yrs) accounted for 67.11% share in 2024, whereas children and adolescents (≤17 yrs) represent the fastest-growing cohort at 17.88% CAGR.

- By region, North America dominated with 37.65% share in 2024, and Asia-Pacific is poised to grow at an 18.15% CAGR through 2030.

Global Mental Health Apps Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of anxiety, depression, and stress disorders | +4.2% | Global; stronger in North America and Europe | Short term (≤ 2 years |

| Smartphone penetration and 5G connectivity | +3.8% | Global; peak effect in Asia-Pacific | Medium term (2-4 years) |

| Clinical and payer acceptance of tele-mental-health | +3.1% | North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Awareness of mental health importance | +2.9% | Global | Short term (≤ 2 years |

| Corporate wellness and insurance reimbursement | +2.8% | North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Technological advancements and AI Integration | +3.5% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising Global Prevalence of Anxiety, Depression & Stress Disorders

Mental health conditions now contribute more to global disability than any other illness, prompting a marked shift toward on-demand digital support. Workplace surveys show that 77% of staff reported job-related stress in 2024, a signal that employers can no longer frame wellbeing as a fringe perk.[1]Source: U.S. Department of Health and Human Services, “Social Media and Youth Mental Health: The U.S. Surgeon General’s Advisory,” hhs.gov Mental health apps offer discreet, always-available coaching that dovetails with traditional therapy and, when evidence-based, can shorten time to care. The U.S. Surgeon General has emphasized the need for digital interventions backed by peer-reviewed research, encouraging health systems to integrate validated apps as step-care options. Growing comfort with self-help technology among young adults is extending the addressable market beyond clinical populations into prevention and performance optimization.

Surge in Smartphone Penetration & 5G Connectivity Enabling On-Demand Care

Smartphone subscriptions exceed global population estimates, and 5G coverage already reaches more than half of urban residents. Lower latency lets counseling platforms deliver crisp video sessions and collect sensor data for real-time mood analytics. Rural users who once faced multi-hour travel to clinics can now join cognitive-behavioral groups from home, a change that is especially transformative in large countries across Asia-Pacific. Device makers continue to open health application programming interfaces, giving app developers secure access to motion and sleep metrics that can trigger just-in-time interventions for panic attacks or insomnia.

Growing Clinical & Payer Acceptance of Tele-Mental-Health Solutions

Clinical endorsement climbed in 2024 when 43% of mental health professionals reported using artificial-intelligence tools for rapid screening or homework support.[2]Source: Shane Cross et al., “Use of AI in Mental Health Care,” JMIR Mental Health, mental.jmir.org Payers followed, with 72% of large United States employers adding virtual behavioral health to benefit menus, often bundling meditation, therapy matching, and medication management into one platform.[3]Source: Jennifer Croft and John Fisher, “Why Workplace Well-Being Programs Don’t Achieve Better Outcomes,” Harvard Business Review, hbr.org These contracts are shifting revenue models from direct-to-consumer subscriptions to enterprise licensing, stabilizing cash flow and funding further product validation studies.

Expanding Corporate Wellness and Insurance Reimbursement Programs

Nearly 90% of large United States employers now operate structured wellness programs that include digital mental health tools, benefitting about 63 million. Corporate buyers demand rigorous outcomes data that link app use to absenteeism cuts, nudging vendors toward randomized-controlled trials. Insurers echo this evidence requirement when they negotiate per-member-per-month rates with platforms such as Talkspace, which lists Aetna and Cigna as partners in its SEC filings.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambiguous regulatory classification and evidence requirements | -2.6% | Global; sharper in North America and Europe | Medium term (2-4 years) |

| Data-privacy and cybersecurity concerns | -2.3% | Global; highest in Europe due to GDPR | Short term (≤ 2 years) |

| Market saturation with low-quality apps | -1.9% | Global; strongest in mature markets | Medium term (2-4 years) |

| Low engagement and high dropout rates | -2.1% | Global, with similar impact across regions | Short term (≤ 2 yrs) |

Source: Mordor Intelligence

Ambiguous Regulatory Classification & Evidence Requirements Across Regions

Regulators are still deciding when a mental health app crosses the line from wellness aid to medical device. The United States Food and Drug Administration has issued draft guidance on software as a medical device that references artificial-intelligence updates, yet many predictive mood tools remain in a gray zone. Europe moves more cautiously; the United Kingdom’s Medicines and Healthcare Products Regulatory Agency and the National Institute for Health and Care Excellence released a joint framework in 2024 that sets out stepped evidence tiers for digital mental health technologies, increasing compliance costs for start-ups. Unclear pathways slow time to market and raise investor risk premiums.

Data-Privacy and Cybersecurity Concerns Undermining User Trust

Mental health records are among the most sensitive personal data. A 5.3 TB breach at Confidant Health in December 2024 exposed therapy notes across five US states, reinforcing fears about cloud misconfiguration in the sector. Earlier that year, the Federal Trade Commission fined Cerebral USD 7.8 million for undisclosed data-sharing with social media networks, establishing a precedent for robust enforcement. Users react swiftly; download churn spikes whenever privacy scandals surface, compelling vendors to spend heavily on encryption, credential management, and third-party audits.

Segment Analysis

By Platform Type: Android’s Expansion Narrows iOS Lead

The mental health apps market size for platforms shows iOS controlling 49.12% revenue in 2024, aided by Apple’s privacy messaging and seamless integration with the HealthKit framework. Android, however, demonstrates faster uptake in Latin America, India, and Southeast Asia and is forecast to rise at an 18.94% CAGR. Google’s lower entry barrier for developers spurs a proliferation of vernacular-language apps that target first-time help seekers. Developers increasingly employ cross-platform tools that allow parallel deployment, gradually reducing the historic performance advantage of native builds. Wearable-first experiences remain niche but gain traction for continuous heart-rate monitoring that can cue real-time breathing exercises. Voice-only interfaces open new possibilities for users with visual impairments or screen fatigue, though clinical validation remains thin.

The competitive equation is shifting as platform owners vie to lock in health datasets. Apple’s iOS 18 privacy rubric positions on-device processing for sentiment analysis, while Google’s Health Connect unifies data permissions across Android partners. These native capabilities influence acquisition targets; smaller app publishers that harmonize well with platform health stacks attract premium valuations. Enterprise buyers weigh operating-system compatibility when negotiating bulk licenses, making cross-platform stability a procurement necessity. As device ecosystems blend with wearables and smart speakers, platform fragmentation risk recedes, but data-governance alignment takes center stage.

Note: Segment shares of all individual segments available upon report purchase

By Application: Targeted Modules Outpace General Wellness

Depression and anxiety modules hold 30.78% of 2024 revenue because these conditions account for the largest share of diagnosed cases and carry a strong evidence base for digital cognitive therapy. Stress-management tools are forecast to log the highest growth at 18.53% CAGR as employers fund burnout reduction programs. Meditation and mindfulness suites retain cultural resonance yet face competition from specialized sleep aid apps that couple blue-light reduction coaching with behavioral activation tasks. Substance-use disorder modules remain a smaller slice but carry high societal value, prompting insurers to reimburse contingency-management protocols delivered over secure channels.

Artificial-intelligence personalization is accelerating segmentation. In January 2025, Amia launched an adaptive companion that analyses language patterns to flag escalating distress, demonstrating how large language models can customize care journeys without human intermediaries. Developers also embed smart triage prompts that guide users to licensed therapists or crisis lines when risk scores cross thresholds. These clinical safeguards answer payer and regulator calls for stepped-care pathways, positioning evidence-oriented vendors for broader distribution.

By End User: Corporate Wellness Spurs B2B Shift

Home-care settings continue to dominate with 62.86% share in 2024 as consumers download apps directly from marketplaces for self-paced use. The corporate channel is projected to grow at 17.68% CAGR, propelled by return-on-investment analyses that link psychological safety to lower turnover. Employers increasingly demand analytics dashboards that aggregate anonymized utilization metrics, enabling program managers to align interventions with absentee trends. Mental hospitals and outpatient clinics embed app prescriptions into discharge plans, improving continuity between in-person and virtual care. Universities expand licenses for student populations facing unprecedented stress loads, integrating app usage data into early-alert systems.

The mental health apps market share within enterprises is tilting toward platforms offering multi-modal support—chat-based coaching, synchronous therapy, and self-help content—under a single contract. Vendors leverage this bundling to secure three-year deals with headcount-based pricing, ensuring predictable recurring revenue. In North America, where corporate wellness spending is expected to exceed USD 94.6 billion by 2026, procurement teams now treat mental wellbeing solutions as critical infrastructure rather than perk-like line items.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Youth Engagement Drives Design Evolution

Adults aged 18-64 contribute 67.11% of 2024 spending thanks to disposable income and direct influence over health decisions. Children and adolescents are the fastest-growing cohort at 17.88% CAGR as schools deploy district-wide licenses and parents seek early-stage interventions. A mixed-methods study found that 61.1% of surveyed teens would download a mental health app if they encountered psychological distress. Youth-oriented designs incorporate gamified challenges and peer-support loops that align with digital habits, yet still require parental controls and clinician-approved content.

State-level investments accelerate adoption; California committed USD 4.7 billion to youth mental health programs that include free app access for high-school students. Developers refine inclusivity features such as language localization, culturally relevant avatars, and LGBTQ+ resource sections to close representation gaps identified in recent app audits. For older adults, simpler interfaces, larger fonts, and caregiver dashboards tackle digital-literacy barriers, yet the segment remains under-served, signaling white-space potential.

Geography Analysis

North America commands 37.65% of 2024 revenue, supported by high smartphone penetration and an insurance system that increasingly reimburses tele-psychiatry. Canada’s “Not Myself Today” managerial e-learning series illustrates how workplace programs amplify app uptake by embedding mental health literacy into leadership training. U.S. venture capital maintains a steady flow into start-ups that combine measurement-based care with clinician networks, while policy initiatives such as the 2024 enforcement of mental-health parity rules sustain reimbursement momentum. Regional adoption is further catalyzed by the dense presence of digital-health accelerators that pair seed funding with clinical trial mentorship.

Asia-Pacific records the fastest expansion at 18.15% CAGR through 2030 because of surging smartphone affordability, public health campaigns, and employer interest in well-being. India launched a rigorous mental health app quality review in 2024, raising visibility for vetted products and prompting developers to strengthen evidence bases. China’s urban centers endorse digital stress-management courses as part of community wellness drives, and Japanese telecom firms trial mood-tracking wearables that link lonely seniors to group mindfulness sessions. OECD/WHO analyses reveal that depressive and anxiety disorders comprise one-quarter of non-fatal disease burden across the region, a statistic that underlines large latent demand.

Europe remains a significant market shaped by stringent privacy standards. The 2024 collaboration between the Medicines and Healthcare Products Regulatory Agency and the National Institute for Health and Care Excellence yielded a classification framework that clarifies evidence thresholds, encouraging investors to back scale-ups confident in their regulatory pathway. Germany’s DiGA model continues to reimburse certified digital therapeutics, nudging other member states toward similar coverage. At the same time, the new EU–US Data Privacy Framework raises compliance obligations for trans-Atlantic vendors.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

Competitive rivalry is brisk but not yet consolidated. Headspace is one of the key players yet face pressure from AI-first challengers that tailor interventions through language models trained on clinical corpora. BetterHelp extends reach via podcast sponsorships and insurance partnerships that position the brand within employer networks. Talkspace leverages its payor integrations with Aetna and Cigna to deepen reimbursement channels while refining asynchronous messaging formats that reduce clinician idle time.

Strategic alliances between mental-health platforms and electronic health record vendors aim to embed digital therapies into clinician workflows. Such integrations shorten referral loops and create data pipelines that feed outcome dashboards, positioning app providers as clinical partners rather than consumer-only brands. An interesting by-product is that interoperability standards now influence acquisition valuations more than user-base size.

White-space remains in culturally specific content, geriatric cognitive support, and multimorbidity management that links mental health with chronic-disease coaching. Intellectual-property fences are low; few patents cover core therapeutic techniques, so brand equity and evidence depth serve as primary moats. Vendor evaluation criteria now weigh cybersecurity certifications alongside clinical outcomes, reflecting heightened purchaser sophistication.

Mental Health Apps Industry Leaders

-

Sanvello Health, Inc.

-

Talkspace Inc.

-

BetterHelp (Teladoc Health)

-

Wysa Ltd.

-

Headspace Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SonderMind expanded its hybrid mental health network to all 50 US states, opening access for virtual and in-person counseling.

- April 2025: Psych Hub received the 2025 Health Techworld Award for innovations in digital mental health education.

- November 2024: Oxfordshire authorities announced the rollout of Tellmi, a moderated peer-support app for youth, reflecting local commitment to preventive mental health

- October 2024: Northern Ireland launched a national campaign promoting digital mental health services to broaden early intervention access.

Global Mental Health Apps Market Report Scope

As per the scope of the report, mental health apps are designed to provide mental healthcare assistance to the patient population and can be accessed through mobile applications. These applications help track the mental health of individuals and invest in self-care. The mental health apps market is segmented by platform type, application, end users, and geography. The platform type segment is divided into Android, iOS, and other platforms. Other platform types include web-based and hybrid multi-platform. The application segment is divided into depression and anxiety management, stress management, meditation management, and other applications. The other applications include sleep aid and crisis support. The end user segment is bifurcated into homecare settings, mental hospitals, and other end users. The other end users include corporations and educational institutes. The geography is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market sizing and forecasts are done based on value (USD).

| By Platform Type | iOS | ||

| Android | |||

| Web/Progressive Web Apps | |||

| Others (Wearable-first, Voice-only) | |||

| By Application | Depression and Anxiety Management | ||

| Stress Management | |||

| Meditation and Mindfulness | |||

| Sleep and Wellness Improvement | |||

| Substance-Use Disorder Support | |||

| Other Applications | |||

| By End User | Home-care Settings | ||

| Employers and Corporate Wellness Programs | |||

| Mental Hospitals and Clinics | |||

| Schools and Universities | |||

| Other End Users | |||

| By Age Group | Children and Adolescents (≤17 yrs) | ||

| Adults (18-64 yrs) | |||

| Geriatric (65+ yrs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| iOS |

| Android |

| Web/Progressive Web Apps |

| Others (Wearable-first, Voice-only) |

| Depression and Anxiety Management |

| Stress Management |

| Meditation and Mindfulness |

| Sleep and Wellness Improvement |

| Substance-Use Disorder Support |

| Other Applications |

| Home-care Settings |

| Employers and Corporate Wellness Programs |

| Mental Hospitals and Clinics |

| Schools and Universities |

| Other End Users |

| Children and Adolescents (≤17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (65+ yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

Why are employers increasingly funding mental health apps for staff?

Firms see measurable links between app-based stress-reduction programs and lower absenteeism, improved retention, and stronger engagement scores, making digital mental-health support a core productivity lever rather than a discretionary perk.

How is artificial intelligence shaping next-generation mental health apps?

AI now drives real-time mood detection, adaptive content sequencing, and automated triage to human therapists, allowing apps to personalize care paths while easing clinician workload.

What privacy features are users demanding from mental health apps?

Encrypted data storage, on-device processing of sensitive information, and transparent consent dashboards have become baseline expectations as high-profile breaches heighten consumer scrutiny.

What differentiates leading mental health apps from lower-quality alternatives?

Top performers back their interventions with peer-reviewed studies, integrate seamlessly with wearable data, and offer stepped-care pathways that escalate users to licensed professionals when risk thresholds are reached.

How are regulators influencing product development in this market?

Merging frameworks that classify certain apps as software medical devices are pushing vendors to embed clinical evidence and risk-management protocols early in the development cycle.

Page last updated on: June 11, 2025