Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

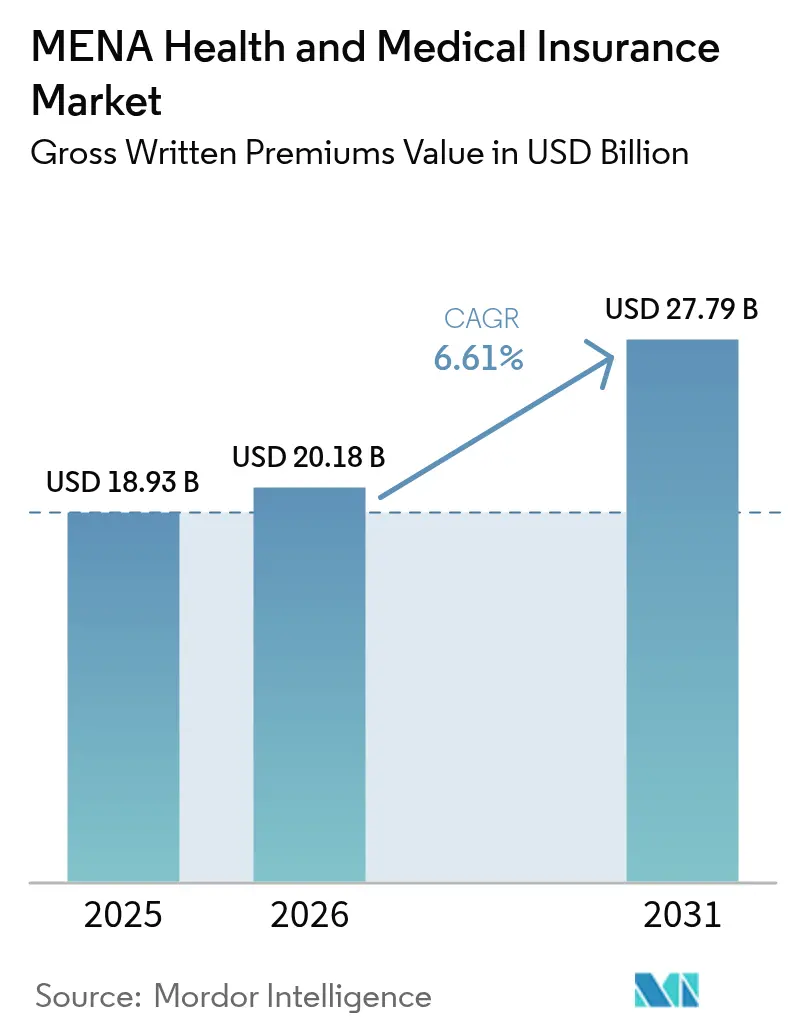

| Base Year Market Size (2025) | USD 18.93 Billion |

| Market Size (2026) | USD 20.18 Billion |

| Market Size (2031) | USD 27.79 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

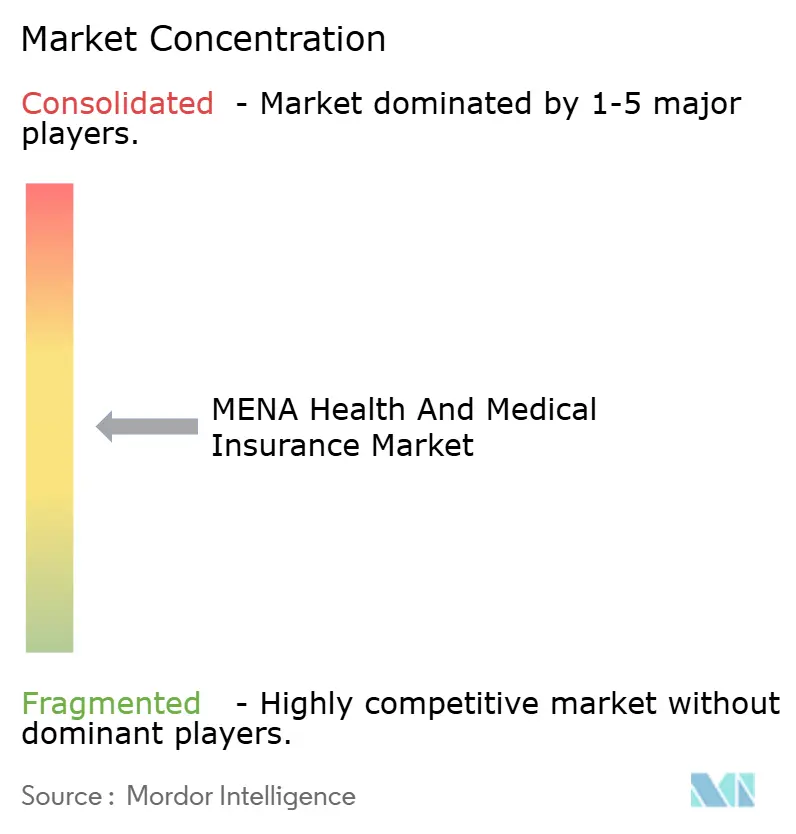

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Health And Medical Insurance Market Analysis by Mordor Intelligence

The MENA health & medical insurance market size is expected to grow from USD 18.93 billion in 2025 to USD 20.18 billion in 2026 and is forecast to reach USD 27.79 billion by 2031 at 6.61% CAGR over 2026-2031. Strong premium momentum stems from sweeping mandatory-insurance laws across Gulf states, heightened private-sector investment under Vision 2030 agendas, and rapid adoption of digital health solutions. Expanding expatriate populations in the Gulf Cooperation Council (GCC) underpin steady demand, while governments shift fiscal pressure from public budgets toward mixed public-private financing models that improve system sustainability. AI-driven underwriting, embedded distribution through super-apps, and medical-tourism-oriented plans widen revenue pools and diversify product portfolios. Persistent medical-cost inflation and fragmented regulation temper growth, yet targeted cost-containment tools and gradual alignment of solvency standards mitigate downside risks for carriers.

Key Report Takeaways

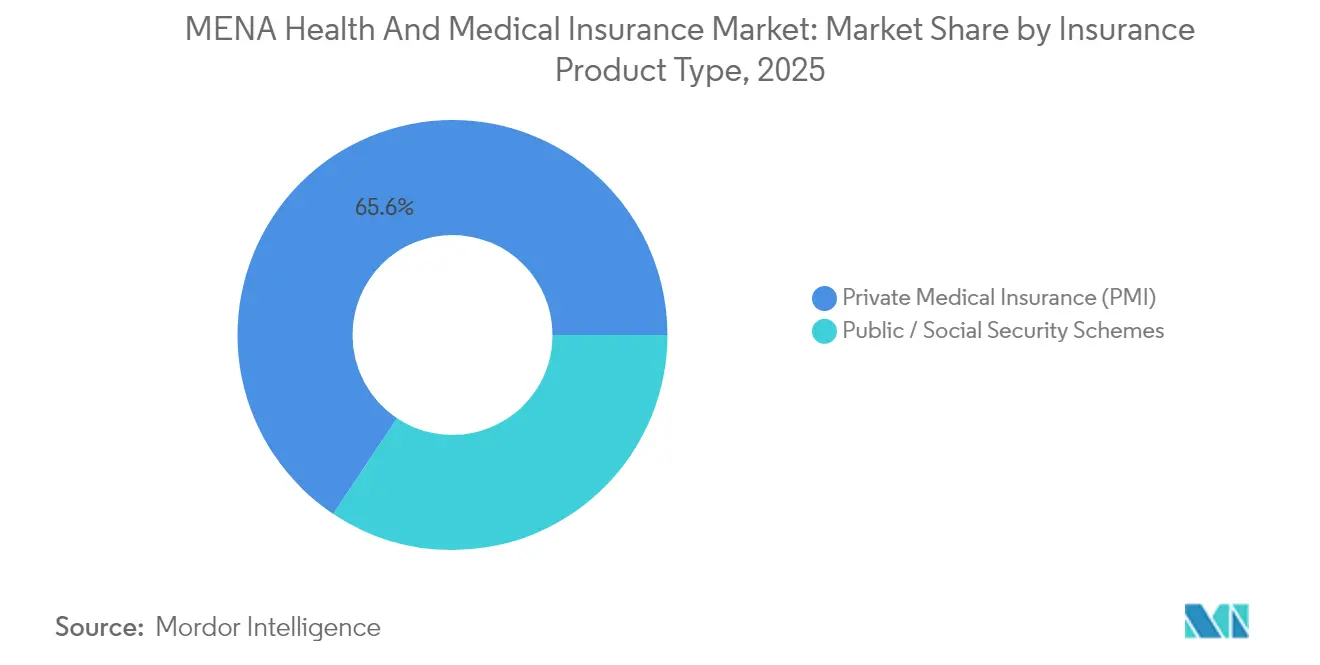

- By insurance product type, private medical insurance led with 65.64% of MENA health & medical insurance market share in 2025; public and social-security schemes are expanding fastest at a 7.53% CAGR through 2031.

- By term of coverage, long-term policies captured 84.02% of the MENA health & medical insurance market size in 2025 and are advancing at a 8.72% CAGR to 2031.

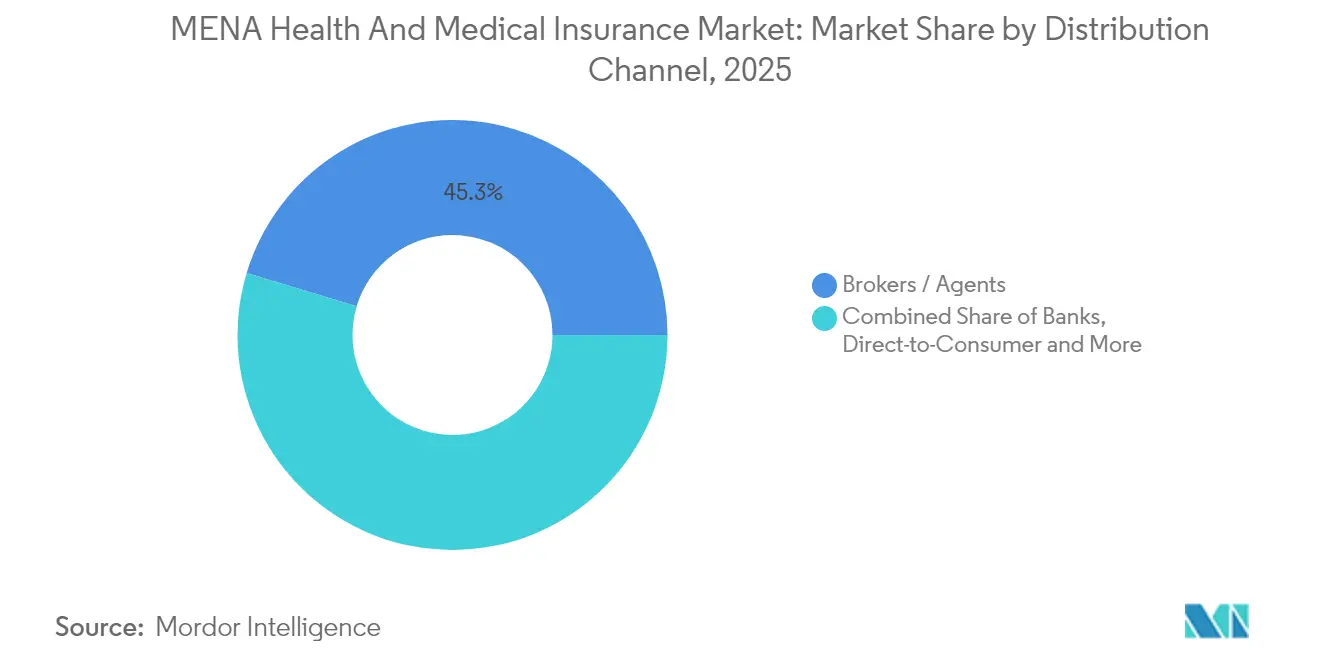

- By distribution channel, brokers and agents held a 45.34% revenue share in 2025, while direct-to-consumer sales recorded the highest projected CAGR at 7.58% through 2031.

- By end-user, large corporates accounted for 58.23% of 2025 demand, whereas SMEs exhibit the strongest growth trajectory at an 7.71% CAGR to 2031.

- By geography, the GCC controlled 70.31% of premiums in 2025; Levant & Emerging markets post the quickest climb at an 8.48% CAGR despite geopolitical headwinds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MENA Health And Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of mandatory health-insurance schemes | +1.8% | GCC core, spill-over to North Africa | Medium term (2-4 years) |

| Rising NCD-linked medical inflation | +1.2% | Global | Short term (≤ 2 years) |

| Privatization & PPPs in regional healthcare | +1.0% | GCC, notably the UAE and Saudi Arabia | Long term (≥ 4 years) |

| Cross-border insured medical-tourism boom | +0.8% | GCC hub, flows to Egypt and Jordan | Medium term (2-4 years) |

| Embedded coverage via super-apps & gig-platforms | +0.6% | Urban GCC and North Africa | Short term (≤ 2 years) |

| AI-driven risk scoring, unlocking new micro-plans | +0.4% | GCC core, gradual Levant uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Mandatory Health-Insurance Schemes

Federal and provincial mandates create the strongest tailwind for the MENA health & medical insurance market. The UAE’s Federal Decree-Law No. 48/2023 requires every resident to carry out a health policy from January 2025, adding about 3.7 million new lives to insurer pools.[1]International Trade Administration, “United Arab Emirates – Healthcare Overview,” trade.gov. Oman adopted a co-insurance framework in December 2024 that lets Category A and Category B carriers share risk, broadening capacity and lowering entry barriers. Saudi Arabia’s rule extending coverage to 3.7 million domestic workers from July 2024 demonstrates how regulators target groups previously outside formal employment. Progressive solvency rules across GCC jurisdictions raise capital standards yet reassure providers, improving claim settlement reliability. Together, these measures stimulate premium inflow, cut hospital bad-debt exposure, and anchor long-run actuarial predictability.

Rising NCD-Linked Medical Inflation

Non-communicable diseases such as diabetes affect over 20% of GCC adults and drive utilization of high-cost interventions. New oncology biologics, continuous glucose monitors, and advanced cardiac procedures lift per-capita spending far above consumer price trends. Governments pilot value-based payment, Saudi Arabia’s AR-DRG model, and Dubai’s eClaimLink, yet specialty pharmaceutical outlays still increase at double-digit rates. Insurers counter through tiered formularies, prior authorization, and tighter preferred-provider agreements. Public-health campaigns under Vision 2030 pivot toward preventive care, but their fiscal savings materialize gradually, keeping margin pressure intense in the near term.

Privatization & PPPs in Regional Healthcare

Sovereign stakeholders reposition from direct provisioning to partnership models that leverage private capital. Saudi Arabia’s Health Holding Company will oversee 290 hospitals and 2,300 primary centers by 2030, prompting insurers to craft bundled service contracts that spread risk across entire episodes of care. Dubai Healthcare City’s 300-provider free-zone ecosystem demonstrates how regulatory leniency attracts multinational carriers and facilitates medical-tourism billing. Egypt’s Universal Health Insurance Authority separates financing from service delivery, letting insurers bid for government contracts while marketing supplemental plans. Such PPPs reallocate risk, reward operational efficiency, and invite specialized actuarial talent into the public domain.

Cross-Border Insured Medical-Tourism Boom

Dubai ranks first in the Arabic Medical Tourism Index and funnels patients seeking oncology, cardiology, and fertility treatments from across MENA. Insurers design region-wide policies that bundle procedure costs, travel, and post-operative accommodation, responding to demand for seamless cross-border care. Abu Dhabi’s flagship carrier collaborates with hospitals to offer flight-plus-treatment packages, strengthening revenue diversification. Simplified visa processes and international accreditation standards expand direct-billing networks. High-occupancy Doha-to-Damascus routes reflect the latent need for evacuation and repatriation coverage in fragile states.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-digit medical-cost inflation | -1.4% | Global | Short term (≤ 2 years) |

| Regulatory fragmentation across MENA | -0.9% | Regional, with a concentration in the Levant markets | Medium term (2-4 years) |

| Chronic clinical-talent shortages | -0.7% | GCC core, acute in Saudi Arabia and the UAE | Long term (≥ 4 years) |

| Geopolitical conflict-zone risk pools | -0.5% | Levant & Emerging, spillover effects to North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Double-Digit Medical-Cost Inflation

Escalating procedure and drug prices erode affordability, prompting carriers to lift premiums and trim benefits. Specialty medicines for oncology and immunology can surpass USD 100,000 per patient-year, straining reserves and raising reinsurance thresholds. Hospital consolidation across major metros concentrates bargaining power, discouraging aggressive tariff discounts. Imported equipment becomes pricier in markets coping with local-currency depreciation, intensifying cost pressures. Carriers pilot value-based contracts and bundled payments, but fragmented provider IT systems limit the rapid scalability of such models across the region.

Regulatory Fragmentation Across MENA

Twenty-two jurisdictions impose divergent capital, solvency, and product-approval requirements that complicate regional scaling strategies. Minimum paid-up capital ranges from USD 10 million in some North-African states to USD 50 million in key Gulf markets, forcing multinationals to lock liquidity in multiple silos. Risk-based capital systems coexist with fixed-ratio regimes, inflating compliance costs and muddying group-wide solvency optimization. Several countries prohibit reimbursement for treatment abroad, constraining cross-border medical-tourism plans. Harmonization talks within the Arab Monetary Fund’s insurance committee are ongoing but remain slow, so insurers must navigate country-by-country filings for each new product.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Product Type: Public Schemes Accelerate Amid PMI Dominance

Private medical insurance retained a 65.64% leadership position in 2025, illustrating entrenched employer-sponsored benefits and individual demand among affluent expatriates. Public and social-security schemes, however, post the most rapid 7.53% trajectory, signaling government commitment to universal coverage. The UAE’s AED 320 (USD 87.1) annual premium mandate expands pooled lives and bolsters underwriting depth. Saudi Arabia’s planned National Health Insurance Centre will further tilt volumes toward public programs by 2026. Insurers pivot from premium-centric competition to administrative-service contracting, requiring advanced population-health analytics. Group coverage inside PMI leverages scale efficiencies, while retail PMI targets middle-class families seeking enhanced maternity and dental benefits. Yet as mandatory frameworks broaden, supplemental riders present lucrative cross-sell avenues for carriers.

Regulatory designs encourage duality: public baselines deliver essential benefits, and private top-ups fill gaps such as elective surgery or international treatment. Egypt’s phased rollout brings 12.8 million more citizens under the umbrella, boosting risk diversification. Morocco’s AMO extension to self-employed workers broadens contributory tax bases. This twin-track architecture supports actuarial stability, though it challenges legacy PMI players accustomed to high-margin expatriate products within the MENA health & medical insurance market.

By Term of Coverage: Long-Term Policies Provide Stability

Annual and multi-year contracts command 84.02% of premiums and log a 8.72% climb, showing participant preference for uninterrupted access and insurer appetite for predictable cash flow. Gulf expatriate visas typically span two to three years, dovetailing with policy durations and lowering churn. Short-term covers cater to medical tourists, seasonal labor, and humanitarian missions but remain a modest slice of overall volume. Oman’s co-insurance scheme rewards carriers that keep clients enrolled across consecutive years, reinforcing long-term dominance.

Extended terms also dovetail with chronic-care management programs: continuous glucose monitoring, oncology case management, and wellness coaching demand year-round engagement to achieve cost savings. As wearable-driven data flows mature, insurers will refine renewal pricing based on longitudinal health metrics rather than broad socio-demographic proxies, sharpening risk segmentation within the MENA health & medical insurance market.

By Distribution Channel: Digital Acceleration Erodes Broker Exclusivity

Traditional brokers and agents still write 45.34% of 2025 premiums, leveraging regulatory fluency and human advisory value in complex group negotiations. Yet direct-to-consumer (D2C) channels expand 7.58% per year, energized by high smartphone penetration and fintech integration. Real-time payment rails let carriers issue micro-policies in minutes, shrinking onboarding costs. Bancassurance remains resilient because consumers view banks as trusted custodians for sizable family health budgets. Affinity programs pair tailored benefits with professional guilds, sports clubs, and alumni networks, deepening niche penetration.

Super-apps drive D2C momentum, embedding coverage within ride-hailing, food-delivery, and gig-work ecosystems. Embedded checkout flows route premiums instantly to insurers, improving cash management. The UAE’s insurance authority now grants digital-broker licenses that cap commission ceilings, further aligning incentives toward transparent pricing. Consequently, carriers invest in customer-experience platforms, chatbots, AI symptom triage, and telemedicine to retain digitally savvy policyholders inside the MENA health & medical insurance market.

By End-User: SME Momentum Challenges Corporate Supremacy

Large corporates consumed 58.23% of 2025 demand due to statutory obligations and bargaining clout that secure broad benefit packages at negotiated rates. SMEs, however, record an 7.71% expansion as governments revoke exemptions and mandate employee coverage regardless of firm size. Cloud-based enrollment portals and simplified group underwriting trim administrative overhead, enabling profitable service of smaller payrolls.

Domestic-worker mandates multiply policy counts among households that must evidence coverage for residency visas. Kuwait’s public-sector budget squeeze illustrates how state employers periodically reevaluate insurer panels, injecting competitive dynamism. Freelancers and solo entrepreneurs increasingly purchase retail plans or join trade association pools, enlarging the addressable market for modular products in the MENA health & medical insurance market.

Geography Analysis

The GCC captured 70.31% of premium in 2025, reflecting oil-funded health infrastructure, strict mandatory-coverage statutes, and sizable expatriate communities. Saudi Arabia’s Vision 2030 reforms place 290 hospitals under the Health Holding Company, enhancing procurement leverage and creating partnership opportunities for insurers on integrated-care pilots. Federal law in the UAE obliges all residents to maintain coverage, and Dubai tops the Arabic Medical Tourism Index, drawing inbound patients who favor seamless cross-border billing. Qatar’s insurance mandate kicked in during 2022, and Oman’s Category A/B licensing model revolutionizes local competition while keeping solvency high. Bahrain incrementally raises employer contribution rates, collectively fortifying premium pools that underpin the MENA health & medical insurance market.

North Africa advances under Egypt’s Universal Health Insurance Authority, which targets 12.8 million additional enrollees in its second phase. Morocco broadens its Assurance Maladie Obligatoire to the self-employed, and its 152 hospitals along the Atlantic corridor combine with 2,000 primary centers to support insurer networks. Regional consolidation appeared when Wafa Assurance moved to acquire Egypt’s Delta Insurance in June 2025, boosting cross-border operational efficiency. Algeria and Tunisia benefit from middle-class growth and established public-health infrastructures, sustaining steady uptake of supplemental private covers.

Levant & Emerging markets clock the swiftest 8.48% ascent despite volatility. Jordan’s resilient system lures patients from conflict-affected neighbors, necessitating medical-tourism add-ons. Iraq plans a collaborative public-private model, and early regulatory drafts envision pooled funds that purchase services competitively. Syria’s reopened air links create demand for evacuation and political-risk riders, evidenced by full capacity on Doha–Damascus flights. Lebanon’s fragile finances spur reliance on international reinsurers for high-severity claims. Amid adversity, insurers that master agile risk assessment and political-violence clauses unlock profitable growth in these frontier territories of the MENA health & medical insurance market.

Competitive Landscape

Market concentration remains moderate. Bupa Arabia’s launch of a “No Pre-Approvals Network” in March 2025 reconfigures claims flows by allowing direct provider adjudication, eliminating processing latency for members, and reducing administrative spend. Large incumbents also expand into neighboring markets via green-field licenses or minority stakes, capitalizing on brand trust and actuarial depth.

Digitalization redraws the competitive map. Arabian Falcon Insurance’s AI-enabled underwriting partnership with eData elevates risk selection accuracy and slashes quote turnaround times from days to minutes. Insurtech entrants leverage cloud-native architectures that integrate seamlessly with SaaS back-offices, chasing white-space segments such as gig-worker micro-covers and cross-border medical-travel bundles. Strategic alliances with super-apps unlock captive audiences at marginal acquisition cost, intensifying pressure on brokers to justify commissions inside the MENA health & medical insurance market.

Regulation still shapes competitive parameters. GCC solvency frameworks favor well-capitalized groups, raising hurdles for pure-play startups. However, sandbox programs in the UAE and Bahrain invite controlled testing of pay-as-you-go products, potentially leveling the field. As governments harmonize data-protection and e-health standards, interoperable claims rails promote portability and increase the addressable market for cross-jurisdictional players. Consequently, competitive advantage now pivots on a triad: digital distribution mastery, advanced analytics, and ability to navigate multi-country regulatory mosaics.

MENA Health And Medical Insurance Industry Leaders

Bupa Arabia

Tawuniya

Daman (NHIC)

GIG Gulf (incl. Orient/Sukoon)

MedGulf

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wafa Assurance agreed to acquire Egypt’s Delta Insurance, strengthening North-African footprint and unlocking cross-border cost collaborations.

- May 2025: GIG Gulf received Category A health-insurance approval from Oman’s Financial Services Authority, enabling co-insurance participation under the new framework.

- March 2025: Bupa Arabia introduced the region’s first “No Pre-Approvals Network,” granting members instant provider access without prior authorization and reducing administrative burden.

- February 2025: Tawuniya clinched the comprehensive health insurance contract for Saudi airline employees and their families, bolstering group coverage in the aviation sector via competitive bidding.

MENA Health And Medical Insurance Market Report Scope

Health insurance covers a range of medical treatments, including surgical expenses.

The MENA health and medical insurance market is segmented by insurance providers, demographics, distribution channels, coverage, and country. By insurance providers, the market is segmented into public sector insurers, private sector insurers, and standalone health insurance companies. By demographics, the market is segmented into adults, minors, and senior citizens. By distribution channel, the market is segmented into direct sales, agents, online, bancassurance, and other distribution channels. By coverage, the market is segmented into individuals and families or groups. By country, the market is segmented into Saudi Arabia, United Arab Emirates, Egypt, Kuwait, Qatar, and Rest of Middle East and North Africa. The report offers market size and forecasts in value (USD) for all the above segments.

By Insurance Product Type

| Private Medical Insurance (PMI) | Individual Policy Coverage |

| Group Policy Coverage | |

| Public / Social Security Schemes |

By Term of Coverage

| Short-term (< 12 months) |

| Long-term (≥ 12 months) |

By Distribution Channel

| Brokers / Agents |

| Banks (Bancassurance) |

| Direct-to-Consumer (Online / Phone) |

| Employer-Sponsored (Companies) |

| Other Channels (Affinity, Associations) |

By End-user Segment

| Individuals |

| SMEs |

| Large Corporates |

By Geography

| Gulf Cooperation Council (KSA, UAE, Qatar, Kuwait, Bahrain, Oman) |

| North Africa (Egypt, Morocco, Algeria, Tunisia) |

| Levant & Emerging (Jordan, Lebanon, Palestine, Iraq) |

| By Insurance Product Type | Private Medical Insurance (PMI) | Individual Policy Coverage |

| Group Policy Coverage | ||

| Public / Social Security Schemes | ||

| By Term of Coverage | Short-term (< 12 months) | |

| Long-term (≥ 12 months) | ||

| By Distribution Channel | Brokers / Agents | |

| Banks (Bancassurance) | ||

| Direct-to-Consumer (Online / Phone) | ||

| Employer-Sponsored (Companies) | ||

| Other Channels (Affinity, Associations) | ||

| By End-user Segment | Individuals | |

| SMEs | ||

| Large Corporates | ||

| By Geography | Gulf Cooperation Council (KSA, UAE, Qatar, Kuwait, Bahrain, Oman) | |

| North Africa (Egypt, Morocco, Algeria, Tunisia) | ||

| Levant & Emerging (Jordan, Lebanon, Palestine, Iraq) |

Key Questions Answered in the Report

What is the forecast value of the MENA health & medical insurance market by 2031?

The market is expected to reach USD 27.79 billion by 2031 based on a 6.61% CAGR projection.

Which product segment is growing fastest within MENA health & medical insurance?

Public and social-security schemes show the highest growth at a 7.53% CAGR as governments expand mandatory coverage.

Why are SMEs important for future premium growth?

Regulatory mandates now require even small employers to insure staff, pushing SME-segment premiums to grow 7.71% annually.

How does digital distribution affect traditional brokers?

Direct-to-consumer channels embedded in super-apps lower acquisition costs and are growing 7.58% each year, gradually eroding broker dominance.

Which region contributes the largest share of premiums?

The GCC region holds 70.31% of total premiums due to comprehensive mandatory insurance laws and high expatriate populations.

What major technological trend is reshaping underwriting?

AI-driven risk scoring improves pricing precision and supports micro-insurance, giving carriers real-time insights from wearable and clinical data streams.

Page last updated on: