Medium Voltage Transformer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.58 Billion |

| Market Size (2031) | USD 31.63 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

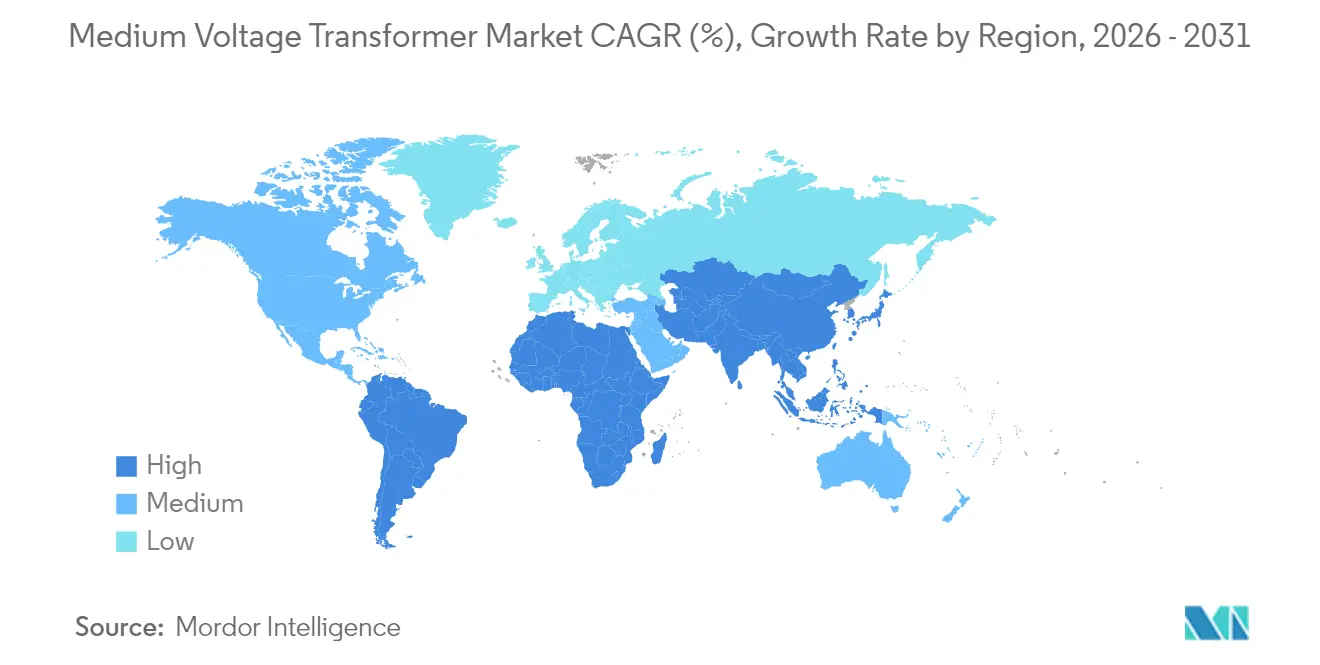

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medium Voltage Transformer Market Analysis by Mordor Intelligence

Medium Voltage Transformer market size in 2026 is estimated at USD 22.58 billion, growing from 2025 value of USD 21.11 billion with 2031 projections showing USD 31.63 billion, growing at 6.97% CAGR over 2026-2031.

The expansion reflects simultaneous grid modernization mandates, large-scale renewable integration, and the electrification of industrial loads, all of which require robust medium-voltage infrastructure. Utilities are replacing aging assets—about 70% of installed transformers in the United States are over 25 years old—while Asia–Pacific and the Middle East commission new capacity at an unprecedented pace. Supply constraints have lengthened delivery lead times to more than two years, prompting buyers to adopt early procurement frameworks and multi-vendor strategies. Meanwhile, commercial users, such as hyperscale data centers, are shifting their design specifications toward fire-safe, cyber-resilient, and eco-friendly units that command premium pricing.

Key Report Takeaways

- By cooling type, oil-cooled units held 61.70% of the medium voltage transformer market share in 2025, while air-cooled models are growing at the fastest rate, with a 7.75% CAGR through 2031.

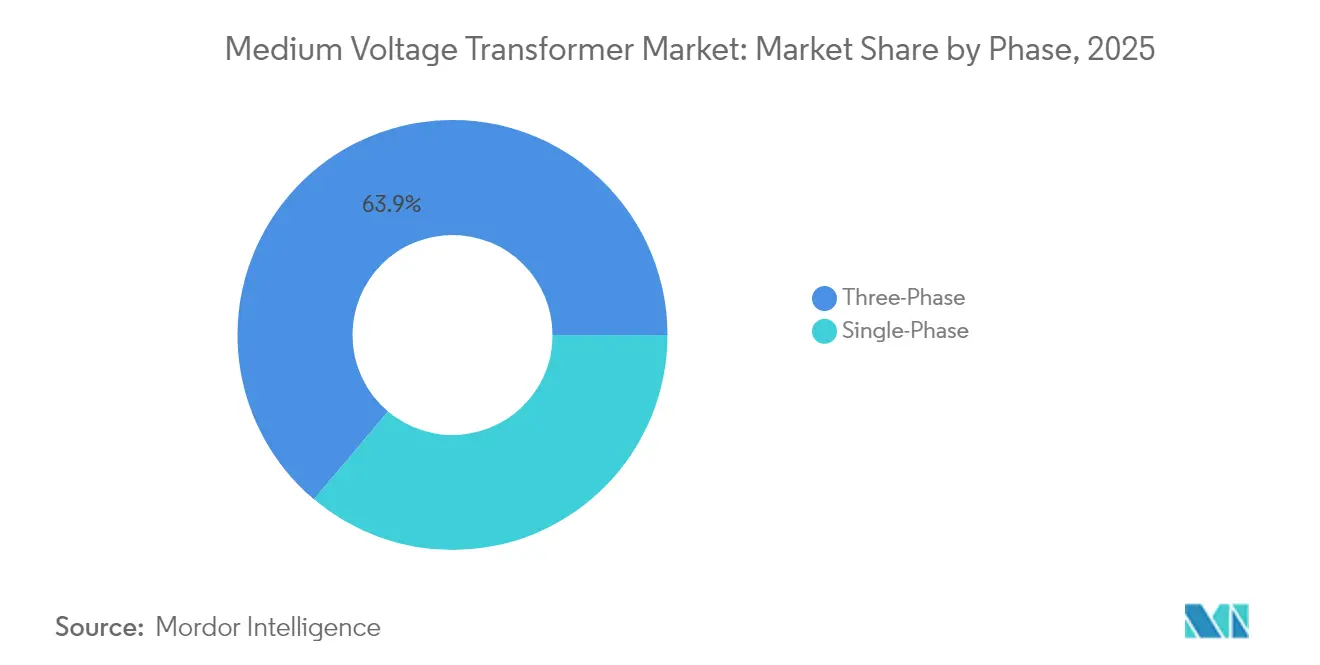

- By phase, three-phase products led with 63.85% revenue share in 2025; single-phase alternatives are expected to progress at 7.21% CAGR to 2031.

- By transformer type, distribution units accounted for 60.20% of the medium voltage transformer market size in 2025, whereas power units are expected to advance at a 7.78% CAGR during 2026-2031.

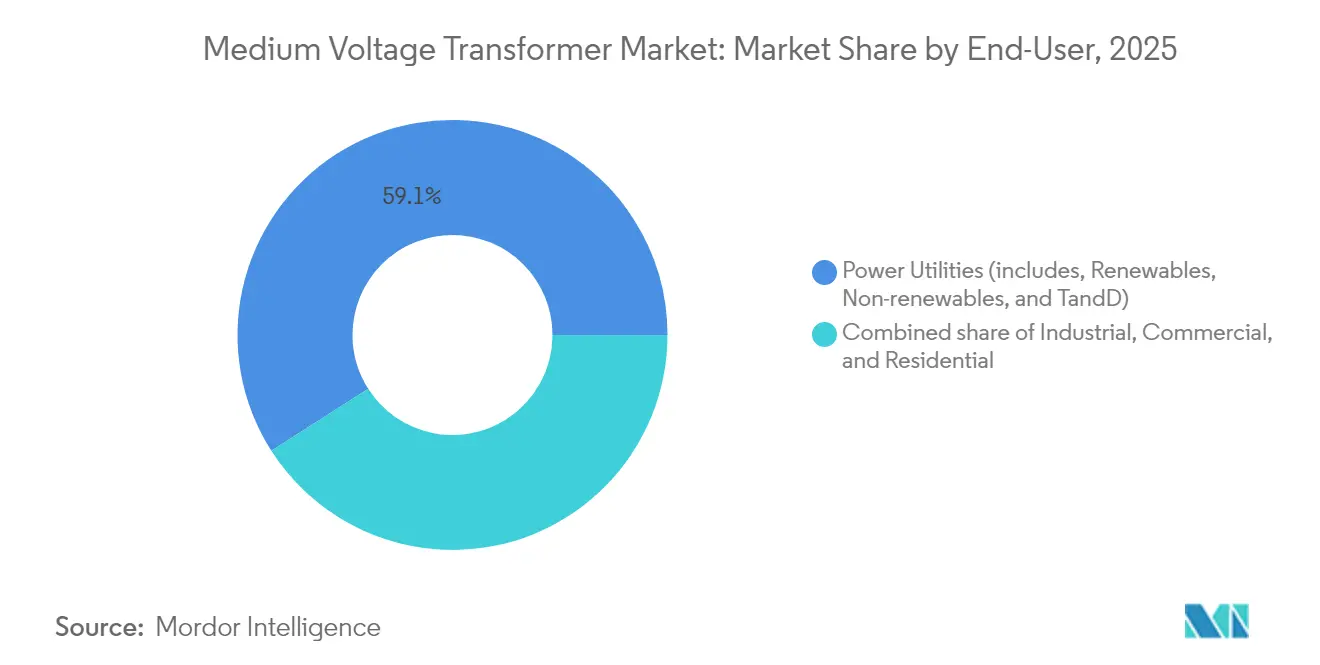

- By end-user, power utilities commanded a 59.05% share in 2025; the commercial segment is projected to record the fastest CAGR at 8.12% through 2031.

- By geography, the Asia-Pacific region captured 48.90% of 2025 revenues and is forecast to expand at a 7.63% CAGR through 2031.

- Hitachi Energy, Siemens Energy, and Schneider Electric together controlled just under 35% of global shipments in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medium Voltage Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization & aging-asset replacement | +2.1% | North America, Europe, global spillover | Medium term (2-4 years) |

| Renewable-integration push (utility & C&I) | +1.8% | Asia–Pacific core, Middle East & Africa spill-over | Long term (≥ 4 years) |

| Urban/industrial electricity-demand growth | +1.4% | Asia–Pacific, Middle East, North America | Medium term (2-4 years) |

| Data-center microgrid build-out | +0.9% | North America, Europe, advanced APAC markets | Short term (≤ 2 years) |

| Electrolyzer-grade hydrogen projects | +0.6% | Middle East, Europe, selective APAC | Long term (≥ 4 years) |

| Cyber-resilient hardened MV units | +0.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization & Aging-Asset Replacement

More than two-thirds of U.S. medium-voltage transformers were installed before 2000, with a similar pattern emerging in Western Europe. As utilities face an equipment obsolescence cliff, they bundle replacement orders with digital monitoring, eco-design compliance, and cyber-resilience features that raise the bill of materials. The European Union’s Regulation 548/2014 already enforces published loss parameters with zero upward tolerance, steering buyers toward higher-efficiency cores and natural-ester insulation. This replacement super-cycle tightens global supply, enabling manufacturers to operate plants at near-full capacity and secure multi-year order books.(1)Bruno Melles, “Hitachi Energy Successfully Tests Groundbreaking 765 kV Transformer,” Hitachi Energy, hitachienergy.com

Renewable-Integration Push (Utility & C&I)

Utility-scale solar and wind farms now exceed 2 GW per site in several Asian and Middle Eastern markets, each requiring dozens of step-up transformers, as well as collection substations. Bidirectional power flow, variable voltage support, and rapid islanding are standard specification points as hybrid plants pair battery storage with intermittent generation. Corporate power-purchase agreements drive similar needs behind the meter, where distributed rooftop arrays or on-site turbines connect to private medium-voltage networks. The result is a sustained demand for intelligent transformers equipped with digital tap changers and edge analytics.

Urban/Industrial Electricity-Demand Growth

Industrial electrification—ranging from steel arc furnaces to green-hydrogen electrolyzers—concentrates multi-megawatt loads inside single campuses. Cities add strain as electric vehicle charging plazas and rail transit systems draw on the same feeders. Medium-voltage substations must therefore handle higher fault currents while fitting into space-restricted footprints. Operators are increasingly specifying dry-type or natural-ester units, which reduce fire risk and simplify permitting. Over the medium term, these dense load pockets keep pressure on both distribution and power-class transformer demand curves.

Data-Center Microgrid Build-Out

Hyperscale sites in the United States and Northern Europe now budget 130 kW per rack, adopting 800 V HVDC backbones for efficiency. Owners deploy on-site gas turbines or fuel cells in microgrid layouts that require bidirectional, low-loss medium-voltage conversion. Transformer manufacturers respond with hermetically sealed windings, forced-air cooling, and embedded fiber sensors that monitor hotspot temperatures in real-time. Availability contracts often impose penalties for annual downtime exceeding 1 hour, so buyers prefer suppliers with demonstrated reliability records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper & steel price volatility | -1.2% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| High cap-ex & supply-chain delays | -0.8% | North America, Europe | Medium term (2-4 years) |

| Wildfire-risk insurance premiums | -0.3% | North America, Australia, Southern Europe | Medium term (2-4 years) |

| PCB-legacy liability on refurbishments | -0.2% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper & Steel Price Volatility

Copper constitutes roughly one-quarter of a medium-voltage transformer’s cost stack, so tariff announcements or mining disruptions quickly inflate bid prices. Electrical-steel grades—particularly grain-oriented sheets—face similar challenges due to the limited number of mills worldwide that produce high-permeability material. Volatility forces suppliers to shorten quotation validity from 90 days to 30 days, and encourages formula-based adjustment clauses, which complicates buyer budgeting.

High Cap-ex & Supply-Chain Delays

Current order backlogs extend up to 130 weeks for conventional units and exceed 200 weeks for extra-high-capacity models. Even though manufacturers have announced USD 1.8 billion of new North American capacity since 2023, factory lead times remain elevated due to tooling, workforce training, and certification cycles. Financing costs rise when projects must fund multi-year inventory buffers, which dampens near-term installation schedules despite long-term demand strength.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Type: Environmental Safety Drives Air-Cooled Adoption

Oil-immersed designs held 61.70% of the medium voltage transformer market in 2025, yet the air-cooled segment is pacing ahead at a 7.75% CAGR through 2031. Utilities in wildfire-prone regions prefer dry-type or natural-ester units that mitigate fire and spill risks. Hitachi Energy’s successful 765 kV ester-filled prototype demonstrates that fire-safe fluids can now address very high-voltage applications without thermal penalties. Air-cooled products eliminate oil containment pits and reduce maintenance, appealing to data centers and metro rail projects where floor space commands a premium. Efficiency advances—such as vacuum-cast coils, amorphous-metal cores, and active fan modules—help narrow the historical losses of oil-filled counterparts. As insurers attach higher premiums to mineral-oil equipment, the trend toward dry-type units is expected to hold.

Air-cooled transformers also avoid lengthy environmental permitting processes, which accelerates site schedules for commercial developers. The cumulative effect positions the segment to capture a steadily rising share even though oil-cooled models continue to dominate large-capacity substation builds. Utilities looking to modernize legacy sites often blend both cooling types, using ester or dry technology inside city centers while deploying conventional oil units on the transmission perimeter. This hybrid approach generates steady, recurring demand for suppliers that maintain diversified product portfolios within the medium-voltage transformer market.

By Phase: Three-Phase Dominance Reflects Grid Architecture

Three-phase equipment accounted for 63.85% revenue in 2025 and is expected to grow at a 7.18% CAGR, mirroring the prevalence of three-wire distribution grids worldwide. Balanced loading reduces conductor mass and neutral currents, giving three-phase designs natural cost and efficiency advantages for high-density feeders. Applications such as data centers, electrolyzers, and rail traction systems require a three-phase supply for stable power quality. Single-phase units remain essential for rural step-down or single-wire-earth-return schemes; however, their growth tracks broader grid extension pacing rather than demand spikes.

Digital monitoring further tilts the field toward three-phase designs because sensor data can be leveraged for phase-imbalance analytics and dynamic capacity forecasting. Vendors bundle harmonic-filtering capability to address rising inverter-based generation, reinforcing the three-phase proposition. Consequently, network planners expect the three-phase share to stay above 60% of the medium voltage transformer market size through 2031.

By Transformer Type: Power Units Accelerate with Renewables

Distribution transformers represented 60.20% of installations in 2025; however, power-class units are advancing at a faster rate, with a 7.78% CAGR. Massive solar and wind complexes in Saudi Arabia, India, and Australia require multiple high-MVA step-up transformers to tie generation to transmission backbones. Grid interconnection codes also promote low-loss cores and online dissolved-gas analysis, adding extra value to each purchase.

Despite the faster expansion of power units, replacement cycles in suburban feeders keep distribution volumes high. Smart-grid mandates now include sensors, LTE modems, and arc-fault interruption, which lifts average selling prices and allows suppliers to defend margins even in commoditized rural segments. Together, these trends sustain balanced growth across both transformer classes within the medium voltage transformer market.

By End-User: Commercial Demand Surges on Data & EV Infrastructure

Power utilities retained a 59.05% share in 2025, but the commercial category—data centers, campuses, shopping complexes—leads with an 8.12% CAGR outlook. AI training clusters routinely exceed 80 MW per building and require N-1 redundancy at the substation level, resulting in twin or triple 50/70 MVA medium-voltage transformers per site. Similarly, urban EV charging depots incorporate megawatt chargers that need dedicated 13.2 kV feeders.

Industrial users, particularly those in the metals and chemicals sectors, maintain a steady baseline due to decarbonization retrofits. Residential volume growth primarily occurs in Asia and Africa through rural electrification, while rooftop solar and efficient appliances mitigate per-household demand. Overall, non-utility segments collectively generate the fastest incremental revenue within the medium voltage transformer market.

Geography Analysis

Asia–Pacific commanded 48.90% of global revenue in 2025 and is forecast to post a 7.63% CAGR through 2031. China replaces end-of-life 110 kV assets while installing new 220 kV corridors to evacuate renewables from inland provinces. India’s Production-Linked Incentive scheme accelerates domestic manufacturing, ensuring shorter lead times for local state utilities. Southeast Asian nations roll out electrification and metro rail programs that further amplify regional demand. Japan and South Korea contribute technology-intensive orders, particularly for solid-state prototypes and ester-filled units.

North America ranks second by revenue, driven by aging fleets and federal stimulus for grid resilience. The United States faces a 30% shortfall in power-class units by 2025, and imports still satisfy roughly half of distribution-class demand. New factories in Texas, Alabama, and Ontario aim to cut lead times, yet most will only reach scale after 2026. Cybersecurity directives and wildfire risk are pushing buyers toward dry-type or ester-filled designs, lifting average selling prices across the medium-voltage transformer market.

Europe sustains steady demand through renewable build-outs and cross-border interconnectors. The Continent enforces EcoDesign Tier 2 efficiency from July 2025, compelling utilities to adopt ultra-low-loss cores. Offshore wind hubs in the North Sea and Baltic require 66 kV collection networks, opening fresh opportunities for medium-voltage step-up units. Eastern Europe focuses on grid reliability upgrades supported by EU cohesion funds, while Southern Europe channels investment into wildfire mitigation, favoring dry-type products.

South America and the Middle East & Africa together comprise a fast-growing but smaller base. Brazil’s distributed generation boom and Chile’s copper mining electrification continue to drive demand for pad-mounted distribution units. The Middle East channels USD 9.5 billion into solar-plus-storage complexes and green-hydrogen projects, each employing custom medium-voltage step-ups. In Africa, donor-funded rural electrification underpins volume, albeit with extended payment terms that pose challenges to vendor liquidity.

Competitive Landscape

The medium voltage transformer market remains moderately consolidated, with the top five vendors controlling roughly 55% of global shipments in 2024. Hitachi Energy strengthens its lead with a USD 250 million multi-site expansion focused on natural-ester and digital-ready units. Siemens Energy co-locates winding and core fabrication in its Virginia plant to cut logistics time, while Schneider Electric deploys predictive-maintenance software that locks customers into recurring analytics contracts.

New entrants target niches such as silicon-carbide-based solid-state transformers or modular skid solutions for data centers. Barriers to entry rise, however, because buyers demand proven long-term reliability and IEEE/IEC certification. Existing players, therefore, allocate 4-5% of their revenue to R&D, far above the historical average, to maintain a competitive edge. Supply-chain localization is another battleground; vendors positioning copper and steel stockpiles near final assembly sites gain bidding advantages amid raw-material volatility.

Strategic alliances also surface. Samsung C&T partners with Hitachi Energy to pursue undersea HVDC links, while Mitsubishi Electric transfers its legacy transformer lines into a focused subsidiary, enabling it to invest more heavily in high-speed rail traction converters. These moves signal that scale alone is insufficient; technology specialization and regional proximity are increasingly defining the competitive edge within the medium voltage transformer market.(4)Sang Hoon Sung and Jin-Won Kim, “HD Hyundai Electric to Invest $274 mn in Transformer Output Ramp-Ups,” KED Global, kedglobal.com

Medium Voltage Transformer Industry Leaders

Schneider Electric SE

General Electric Company

Eaton Corporation PLC

Siemens AG

Hitachi Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyosung announces plans to double its U.S. transformer output to ease supply shortages and capitalize on infrastructure stimulus spending.

- January 2025: HD Hyundai Electric commits USD 274 million to expand capacities in Alabama and Ulsan by 30%.

- January 2025: Virginia Transformer confirms exploration of a potential USD 6 billion sale to support growth financing.

- December 2024: Samsung C&T and Hitachi Energy sign an MOU for a USD 2.4 billion HVDC subsea project in the UAE.

Global Medium Voltage Transformer Market Report Scope

The medium voltage transformer market report include:

| Air-cooled |

| Oil-cooled |

| Single-Phase |

| Three-Phase |

| Power |

| Distribution |

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Cooling Type | Air-cooled | |

| Oil-cooled | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Transformer Type | Power | |

| Distribution | ||

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the medium voltage transformer market in 2031?

The market is forecast to reach USD 31.63 billion by 2031, growing at a 6.97% CAGR.

Which region leads current demand for medium-voltage transformers?

Asia-Pacific holds the top position with 48.90% revenue share in 2025 and the fastest 7.63% CAGR outlook.

Why are air-cooled transformers gaining traction?

They reduce fire risk, simplify permitting, and comply with stricter environmental standards, leading to a 7.75% CAGR through 2031.

What is driving commercial-segment growth?

Hyperscale data centers and EV charging depots create high-density load centers, boosting commercial demand at an 8.12% CAGR.

How long are transformer delivery lead times today?

Standard medium-voltage units can require 115-130 weeks for delivery, with larger ratings extending beyond 200 weeks.

Which companies are expanding capacity in North America?

Hitachi Energy, HD Hyundai Electric, and Siemens Energy have each announced major investments to shorten regional lead times.

Page last updated on: