Measured Volume Burette Set Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 563.23 Million |

| Market Size (2030) | USD 758.94 Million |

| Growth Rate (2025 - 2030) | 6.15% CAGR |

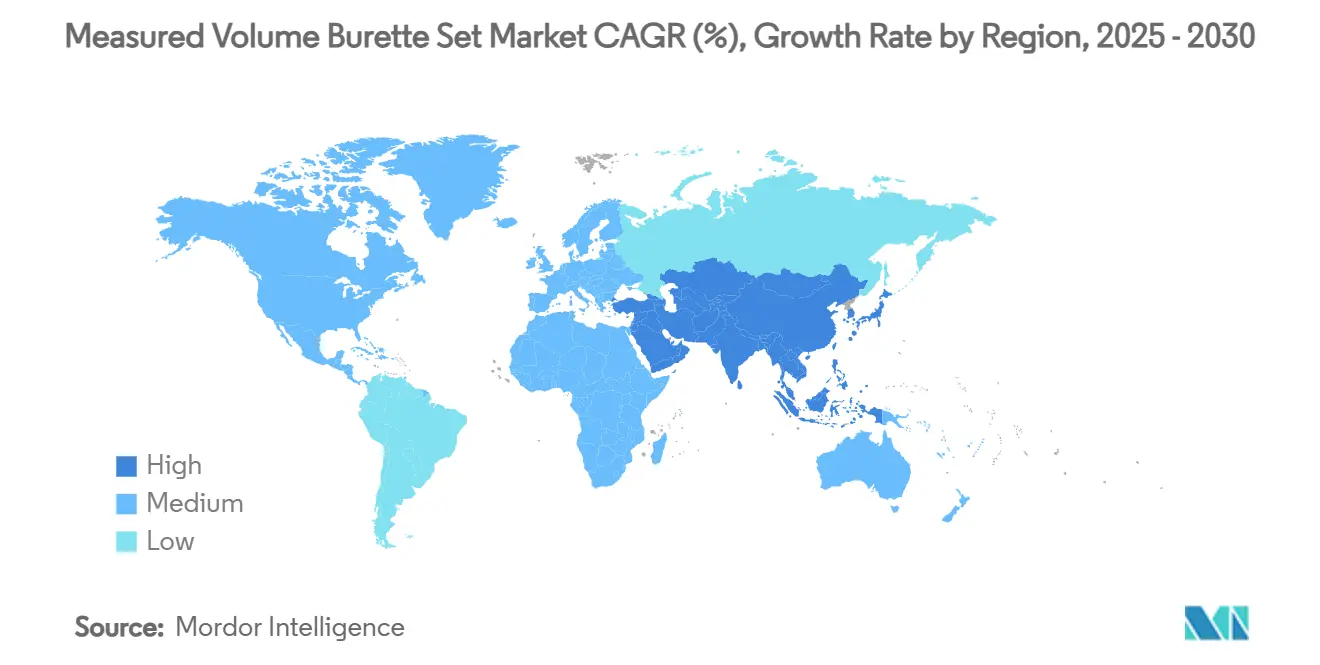

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

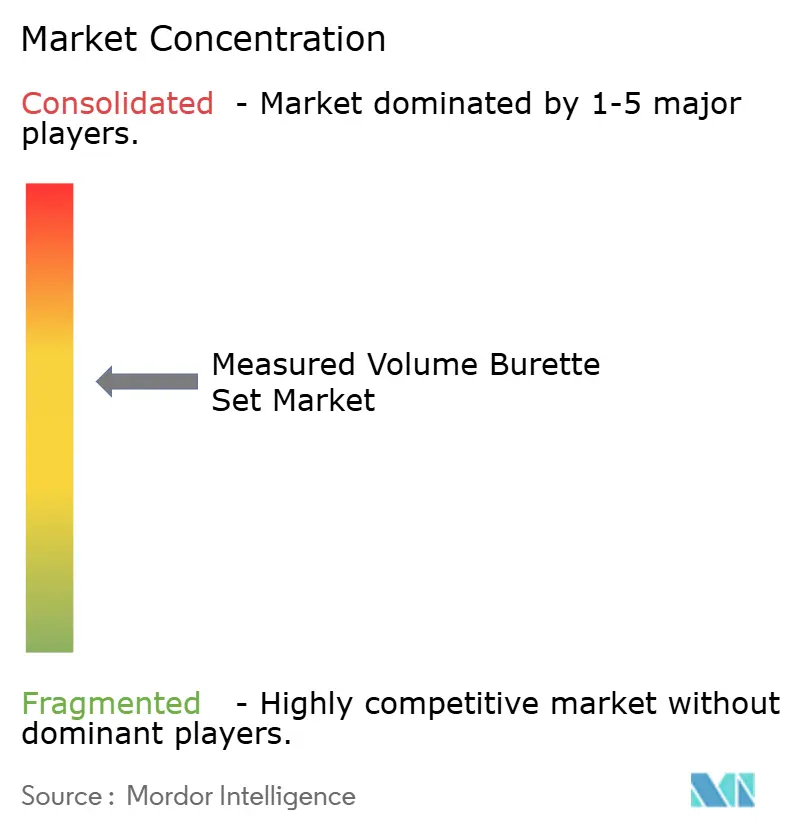

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Measured Volume Burette Set Market Analysis by Mordor Intelligence

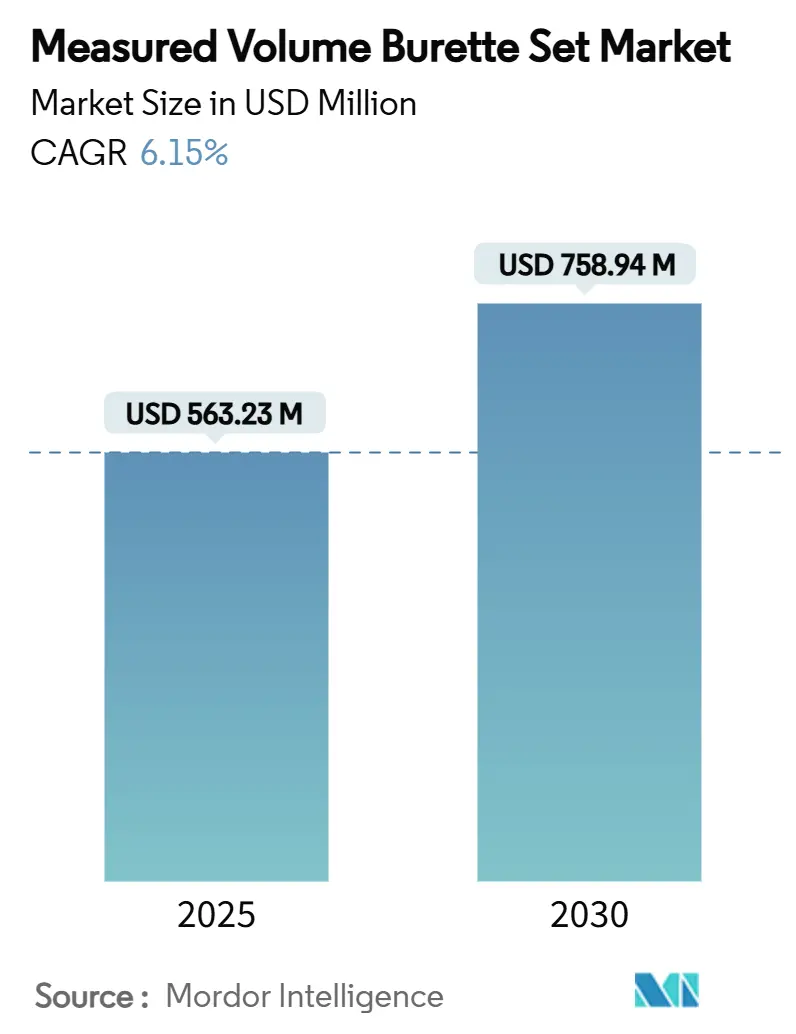

The Measured Volume Burette Set market stood at USD 563.23 million in 2025 and is forecast to reach USD 758.94 million by 2030, reflecting a 6.15% CAGR across the period and underscoring steady expansion despite lingering supply-chain pressures. During 2025, North America retained leadership on the back of hospital consolidation, while Asia-Pacific rose fastest, buoyed by pediatric procedure growth, capacity additions and rising regulatory alignment. Demand is reinforced by mandates that phase out DEHP, prompting accelerated investment in compliant materials, as well as by smart-pump connectivity that helps providers cut medication-error rates. Incremental opportunities emerge from day-surgery growth, home-infusion expansion and bundled public-hospital tenders that reward scale and price transparency. At the same time, margins remain sensitive to PVC‐resin volatility and to the nascent shift toward needle-free closed systems, which compels continuous product redesign.

Key Report Takeaways

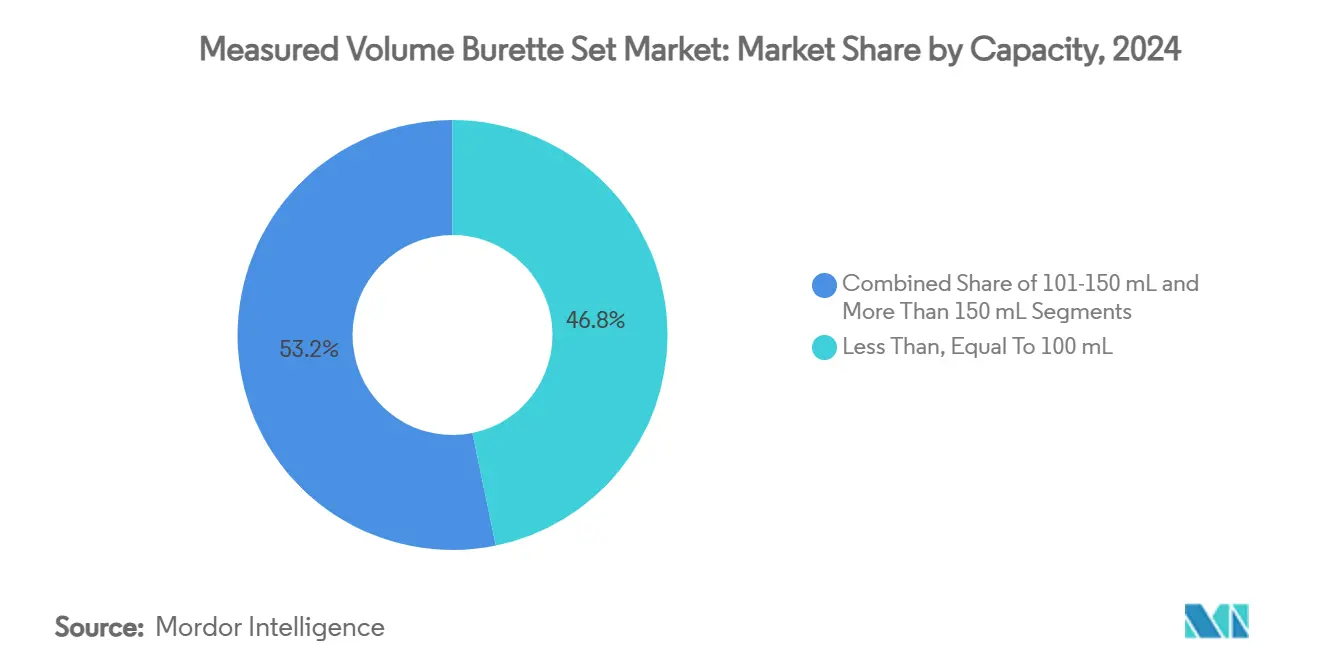

- By capacity, devices ≤100 mL led with 46.78% of Measured Volume Burette Set market share in 2024; units >150 mL are projected to expand at a 9.45% CAGR through 2030.

- By material, standard PVC dominated with 63.46% share in 2024; DEHP-free PVC variants are advancing at a 10.42% CAGR to 2030.

- By end-user, hospitals accounted for 69.28% revenue in 2024; ambulatory surgical centers are set to grow at a 9.23% CAGR through 2030.

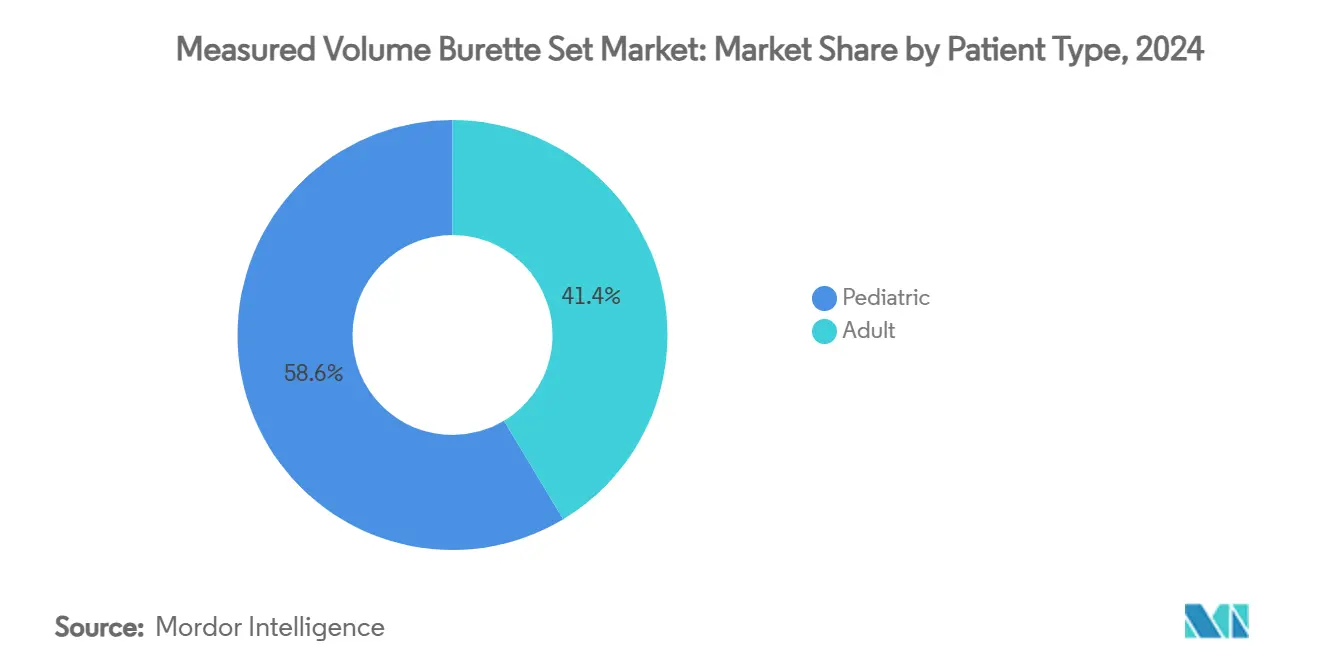

- By patient type, pediatric applications captured 58.61% share in 2024; the same segment also records the fastest 8.77% CAGR to 2030.

- By distribution channel, hospital tenders and group purchasing organizations secured 68.36% share in 2024; online and retail pharmacies are climbing at a 9.78% CAGR through 2030.

- By geography, North America held 33.55% of 2024 revenue; Asia-Pacific is forecast to expand at an 8.04% CAGR to 2030.

Global Measured Volume Burette Set Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pediatric IV therapy volumes in emerging Asia | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Shift toward DEHP-free PVC alternatives in EU and U.S. | +0.8% | North America & EU | Long term (≥ 4 years) |

| Bundled tender contracts in public hospitals | +0.6% | Global | Short term (≤ 2 years) |

| Integration with smart pumps enabling dose tracking | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| COVID-19 driven inventory replenishment cycles | +0.4% | Global | Short term (≤ 2 years) |

| Surging day-care surgeries fueling short-term infusions | +0.7% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pediatric IV Therapy Volumes in Emerging Asia

Rapid demographic growth and expanding insurance coverage in India, Southeast Asia and China are enlarging the pediatric patient pool that requires precise dosing. Regulatory clearance of pediatric-specific lipid emulsions and evidence that neonates experience 3.25% IV infiltration incidence intensify focus on calibrated burette sets with advanced safety sensors.[1]Matheus F.P.T. van Rens, “Peripheral Intravenous Therapy Infiltration/Extravasation (PIVIE) Risks and the Potential for Earlier Notification of Events Using a Novel Sensor Technology in a Neonatal Population,” Journal of Vascular Access, journals.sagepub.com Hospital procurement teams therefore prioritize ≤100 mL calibrated chambers, while device makers integrate computer-controlled delivery modules to shorten time to steady-state infusion. The trend positions APAC as a core driver of incremental Measured Volume Burette Set market demand over the medium term.

Shift Toward DEHP-Free PVC Alternatives in EU and U.S.

California’s AB 2300 law and the EU’s planned DEHP ban by 2026 compel manufacturers to replace legacy plasticizers with compounds such as DEHT and TOTM. B. Braun’s early adoption of DEHP-free formulations and its USD 1 billion Solutions for Life program highlight first-mover advantage. While production changeovers create near-term supply constraints, early-adopter brands gain pricing power and preferred-supplier status in public tenders. Over the long term, material compliance will define baseline eligibility for hospital contracts, bolstering the Measured Volume Burette Set market outlook.

Bundled Tender Contracts in Public Hospitals

National and provincial buying consortia are aggregating demand to secure volume discounts. China’s Volume-Based Procurement model trimmed hip-implant inpatient costs by 50.10% and is expanding to consumables.[2]Yongyong Fan, Qiang Xu, Gang Jin, Lingjun Jiang, and Chenglong Wang, “The Cost of Total Hip Arthroplasty: Compare the Hospitalization Costs of National Centralized Procurement and National Volume-Based Procurement,” Frontiers in Public Health, frontiersin.org Similar frameworks in Western Europe and parts of Latin America incentivize scale and standardized specifications. Large burette-set suppliers capable of offering DEHP-free variants, delivery-bag compatibility and pump integration in one proposal win multi-year contracts, fortifying their recurring revenue base while pressuring smaller competitors.

Integration With Smart Pumps Enabling Dose Tracking

Closed-loop systems such as Baxter’s Novum IQ enable libraries, wireless updates and EMR interfacing that cut medication errors by up to 90.5%.[3]Benjamin Borrelli, Roxana Lucaci, Nathan Wilson, Rashi Taneja, Elizabeth Weiss, and James Beer, “Evaluating the Impact of Smart Infusion Pump Interoperability on Medication Administration Errors,” Medical Devices: Evidence and Research, dovepress.comProcurement teams increasingly bundle administration sets with pump platforms, making connectivity an essential selection criterion. As smart-pump penetration deepens, demand for bar-coded burette sets with dedicated compatibility coding accelerates, widening the technology gap between leaders and late adopters within the Measured Volume Burette Set market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in PVC resin prices | -0.8% | Global | Short term (≤ 2 years) |

| Hospital shift to needle-free closed systems | -0.6% | North America & EU | Medium term (2-4 years) |

| Global syringed micro-infusion adoption (NICU) | -0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Strict single-use plastics bans in Western Europe | -0.5% | EU, expanding to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in PVC Resin Prices

Geopolitical tensions, energy-price swings and environmental curbs on chlor-alkali production have widened PVC-resin price ranges, squeezing gross margins. Manufacturers respond by digitizing supply chains and partnering with converters for capacity pooling, yet contract negotiations with group purchasing organizations remain tense as resin costs can swing up to 20% of finished-good value. Smaller firms lacking hedging capabilities risk losing bids, tempering Measured Volume Burette Set market growth in the near term.

Hospital Shift to Needle-Free Closed Systems

Devices such as BD’s PIVO™ Pro allow blood draws through existing IV lines, reducing needlestick injuries and needle-phobia anxiety, particularly among pediatrics. Early adopters in the U.S. and Western Europe are redesigning infusion workflows around closed systems, dampening demand for traditional burette-needle configurations. Producers are forced to develop hybrid connectors, lifting R&D spending and certification costs that weigh on profitability through 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Precision Dosing Shapes Size Preferences

Smaller chambers ≤100 mL held 46.78% of 2024 revenue in the Measured Volume Burette Set market, reflecting pediatric wards’ zero-tolerance toward dosage miscalculations. Flow-regulated valves, integrated air-elimination filters and bar-coded identification are increasingly standard. In contrast, >150 mL chambers posted the briskest 9.45% CAGR, riding day-surgery and adult oncology demand. Vendors incorporate microchannel flow regulators and heat-responsive catheter tips that soften once inserted to improve patient comfort. The intermediate 101–150 mL band caters to general wards and post-acute care, giving suppliers a balanced volume base. Over the forecast period, the segment mix will gradually tilt toward larger chambers as ambulatory settings proliferate, yet pediatric volumes lock in the core foundation for the Measured Volume Burette Set market size.

Developments in temperature-responsive materials from KAIST and adjustable passive flow regulators enable tighter rate control across all capacities, helping providers meet Joint Commission infusion-therapy targets. As these designs move from prototypes to commercial scale, differentiation will hinge on device memory chips that log infusion history to simplify audits and reimbursement documentation. Suppliers aligning capacity choice with procedure type and smart-pump interoperability are positioned to outpace overall Measured Volume Burette Set market growth.

By Material: Compliance Drives the DEHP-Free Shift

Standard PVC accounted for 63.46% of 2024 sales, supported by entrenched production lines and lower per-unit cost. Yet DEHP-free PVC’s 10.42% CAGR underscores healthcare systems’ rising risk aversion. B. Braun’s CARESAFE administration sets, fully free from DEHP and PVC, illustrate premium-tier adoption in safety-sensitive oncology and neonatal units. Hospitals facing AB 2300 targets are fast-tracking conversion plans, and public tenders increasingly specify DEHP-free options as mandatory. Polyethylene and niche polymers gain share where chemical compatibility or recyclability is paramount, though lack of drop-in manufacturing substitution limits scale for now.

The Measured Volume Burette Set market size linked to DEHP-free categories will exceed USD 300 million by 2030, assuming suppliers can secure medical-grade alternative plasticizer capacity and obtain bio-compatibility clearances. Parallel alignment of the U.S. FDA QMSR with ISO 13485 requirements from 2026 raises documentation demands but harmonizes global filings, easing cross-regional launches. Vendors that standardize common molds for both PVC and non-PVC lines gain tooling leverage while meeting diverging customer needs.

By End-user: Hospitals Dominate but Outpatient Momentum Builds

Hospitals delivered 69.28% of 2024 revenue, relying on continuous infusion for critical and post-operative care. Consolidation among U.S. and European hospital systems intensifies bargaining power, nudging manufacturers toward value-based contracts that bundle pumps, sets and analytics platforms. Ambulatory surgical centers posted the fastest 9.23% CAGR thanks to policy incentives favoring same-day discharge and non-opioid pain-management reimbursement. Specialty clinics maintain a niche anchored in oncology and nephrology, whereas home-care settings open white-space pathways for lightweight, patient-operated kits.

Through 2030, outpatient channels will absorb a larger slice of Measured Volume Burette Set market demand as insurers push procedures outside high-cost acute settings. Success hinges on user-friendly interfaces, compact packaging and rapid telehealth troubleshooting. Manufacturers who pair consumables with digital tracking apps can cement stickier recurring revenue streams among ambulatory and home-care accounts.

By Patient Type: Pediatric Safety Stays Paramount

Pediatrics captured 58.61% of 2024 sales and continues at 8.77% CAGR, reflecting both demographic trends in high-growth Asia and uncompromising safety standards. Evidence showing elevated infiltration risk among neonates has popularized integrated air-bubble detectors and safety clamps. Adult segments, driven by oncology infusions and chronic disease management, complement baseline demand.

Because pediatric regimens often require dosages ≤0.1 mL increments, burette sets must exhibit low dead-space volumes and tight calibration tolerances to minimize cumulative error. Vendors achieving hospital-validated first-attempt success rates through closed-catheter systems build brand equity. Over the forecast horizon, advanced drug libraries in pediatric EMR modules will strengthen demand for burette sets that support data-rich interoperability, reinforcing the Measured Volume Burette Set market’s pediatric-centric profile.

By Distribution Channel: Digital Platforms Erode Procurement Orthodoxy

Hospital tenders and group purchasing organizations owned 68.36% of 2024 revenues, underpinned by standardized contracting cycles and volume-discount thresholds. Yet online and retail pharmacies are expanding at 9.78% CAGR as home-infusion usage broadens and patients source replacement sets directly. Direct sales to private facilities hold steady where procurement autonomy outweighs central mandates.

E-procurement pilots such as the NHS “Tech Devices – Link 4” framework illustrate how cloud storefronts reduce administrative overhead and widen supplier reach. Parallel volume-based purchasing in China cut implant prices by over 90% of total cost savings, pressuring distributors to slash mark-ups. For suppliers, multichannel presence that blends tender compliance with e-commerce agility will be essential to safeguard Measured Volume Burette Set market share in a fragmenting demand landscape.

Geography Analysis

North America retained 33.55% of 2024 revenue, riding group-purchasing leverage and smart-pump ecosystem rollouts that reduce infusion errors by up to 90.5%. Hurricane Helene revealed supply-chain fragility when Baxter’s North Cove site, which produced 25% of its IV solutions, paused operations, prompting buyers to diversify sourcing. Stringent DEHP legislation positions California as a bellwether, accelerating demand for compliant burette sets and influencing nationwide protocols. Payer moves such as the CMS NOPAIN Act encourage non-opioid infusion modalities, adding volume to ambulatory channels and reinforcing regional Measured Volume Burette Set market expansion.

Asia-Pacific leads on growth at 8.04% CAGR, underpinned by rising surgical volumes, public-sector capacity build-outs and strong domestic innovation. China filed 138,000 medical-equipment patents in 2023, equal to 67% of global filings, and now produces over 40% of its high-end devices domestically. Local champions capitalize on government incentives that limit refurbished imports, as seen in India’s medtech policy, broadening the supplier base. Multinationals respond by forming joint ventures and technology-transfer agreements, ensuring regulatory alignment and local sourcing that cut lead times and tariffs.

Europe remains sizable but slower-growing, with impending single-use-plastic restrictions and DEHP bans creating compliance hurdles that raise cost and complexity. Producers explore circular-economy designs, recyclable polymers and life-cycle assessments to secure tender eligibility. Middle East-Africa and South America trail in absolute volume yet post above-global-average growth where public-health budgets expand and private insurers offer advanced infusion benefits. Nevertheless, currency volatility and uneven logistics infrastructure temper immediate scale, keeping these regions in a portfolio-growth role rather than a core revenue pillar for the Measured Volume Burette Set market.

Competitive Landscape

Market concentration is moderate as B. Braun, Baxter and ICU Medical leverage integrated portfolios covering pumps, administration sets and consumables. B. Braun’s four-decade DEHP-free track record and USD 1 billion Solutions for Life investment underpin its U.S. leadership. Baxter’s Novum IQ platform, launched in 2024 with wireless updates and drug libraries, positions the company at the forefront of closed-loop medication management. ICU Medical focuses on oncology-grade leak-proof connectors that align with increasing needle-free adoption.

Consolidation accelerates capabilities: BD’s USD 4.2 billion purchase of Edwards’ Critical Care division deepens monitoring expertise, Nordson’s Atrion acquisition widens fluid-delivery know-how and Teleflex’s EUR 760 million BIOTRONIK deal enhances coronary-portfolio depth. Strategic moves provide end-to-end solutions that help hospitals rationalize vendor lists while enabling data aggregation across infusion touchpoints.

Adjacent players seek white space through AI-driven flow prediction, 3D-printed custom chambers and cloud analytics that predict tubing replacement cycles. Domestic suppliers in China and India capture public-hospital tenders via tariff advantages and local-content quotas, but scale production for DEHP-free lines remains a hurdle. Over the forecast period, competition will revolve around material compliance, connectivity, and service-level agreements rather than price alone, shaping the trajectory of the Measured Volume Burette Set market.

Measured Volume Burette Set Industry Leaders

B. Braun Melsungen AG

Baxter International Inc.

ICU Medical

Fresenius Kabi AG

Vygon SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed the EUR 760 million acquisition of BIOTRONIK’s Vascular Intervention business, broadening its coronary and peripheral vascular lineup.

- April 2025: B. Braun secured FDA approval for Piperacillin-Tazobactam in its PVC- and DEHP-free DUPLEX container, reducing dose-prep time by nearly 4 minutes

Global Measured Volume Burette Set Market Report Scope

| Less Than, Equal To 100 mL |

| 101-150 mL |

| More Than 150 mL |

| PVC (Standard) |

| PVC (DEHP-free) |

| Polyethylene/Other Plastics |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Pediatric |

| Adult |

| Direct Sales to Private Facilities |

| Online & Retail Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Capacity | Less Than, Equal To 100 mL | |

| 101-150 mL | ||

| More Than 150 mL | ||

| By Material | PVC (Standard) | |

| PVC (DEHP-free) | ||

| Polyethylene/Other Plastics | ||

| By End-user | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| By Patient Type | Pediatric | |

| Adult | ||

| By Distribution Channel | Direct Sales to Private Facilities | |

| Online & Retail Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will the Measured Volume Burette Set market grow through 2030?

The sector is projected to advance at a 6.15% CAGR, taking revenue from USD 563.23 million in 2025 to USD 758.94 million by 2030.

Which capacity range shows the highest growth?

Devices larger than 150 mL lead with a 9.45% CAGR as day-surgery demand rises.

Why is DEHP-free material adoption accelerating?

California’s AB 2300 law and an impending EU ban require elimination of DEHP, pushing hospitals toward compliant sets and boosting DEHP-free PVC sales at 10.42% CAGR.

What is driving Asia-Pacific’s surge in demand?

Expanding pediatric populations, domestic manufacturing incentives and increasing patent activity propel regional growth at an 8.04% CAGR.

How are smart pumps affecting product design?

Interoperable pumps like Novum IQ cut infusion errors by up to 90.5%, creating demand for burette sets with embedded connectivity codes and bar-coding that sync with EMRs.

Which distribution channels are expanding fastest?

Online and retail pharmacies are rising at 9.78% CAGR as home-infusion therapy and direct-to-consumer purchasing gain traction.

Page last updated on: