Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

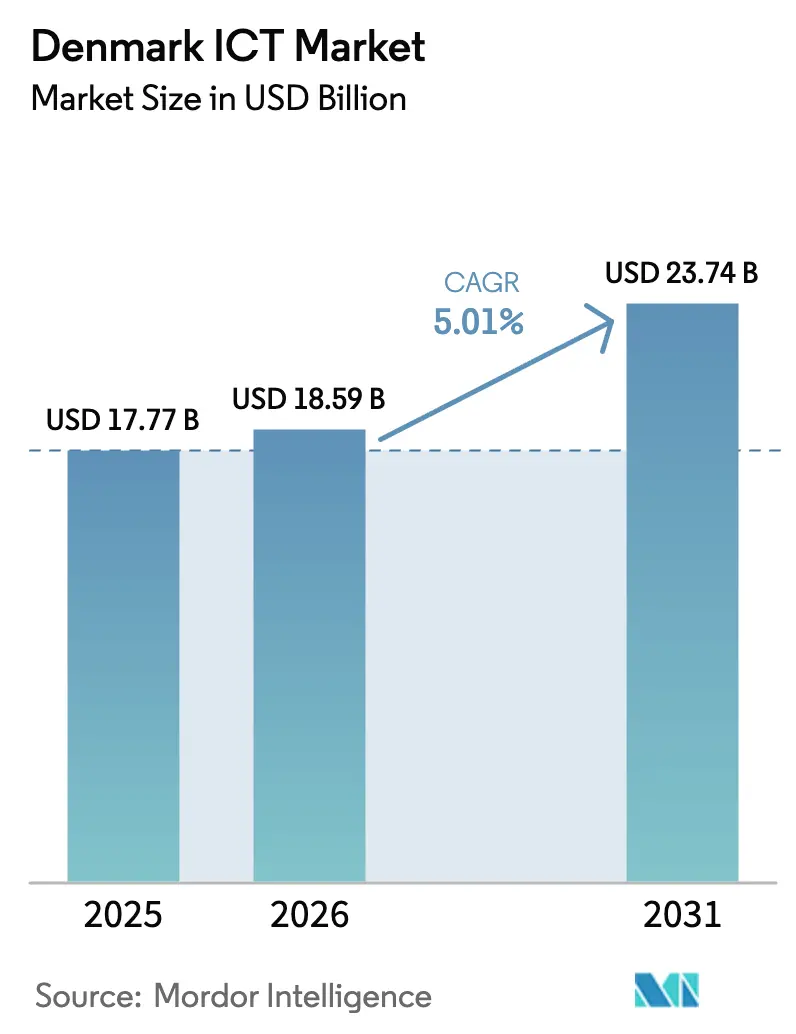

| Base Year Market Size (2025) | USD 17.77 Billion |

| Market Size (2026) | USD 18.59 Billion |

| Market Size (2031) | USD 23.74 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark ICT Market Analysis by Mordor Intelligence

The Denmark ICT market size is expected to grow from USD 17.77 billion in 2025 to USD 18.59 billion in 2026 and is forecast to reach USD 23.74 billion by 2031 at 5.01% CAGR over 2026-2031. A mature digital economy limits headline expansion, yet steady gains emerge from software-as-a-service substitution, cloud workload migration, and data-driven automation. Capital outlays by central and municipal agencies under the National Strategy for Digitalization continue to stabilize demand, while private enterprises divert budgets toward artificial intelligence pilots that shorten time-to-insight. Sub-sea cable upgrades improve latency and spur edge analytics in maritime logistics and renewable-energy grid balancing, reinforcing Denmark’s role as a Nordic data-transit hub. Tight labor supply and energy-price volatility temper margins, compelling providers to emphasize vertical expertise, sustainability credentials, and sovereign-cloud offerings.

Key Report Takeaways

- By product type, IT Services led with 34.48% revenue share in 2025, while IT Security and Cybersecurity is forecast to expand at a 6.43% CAGR through 2031.

- By enterprise size, the large enterprises segment held 54.82% of the Denmark ICT market share in 2025, whereas small and medium-sized enterprises are advancing at a 6.83% CAGR to 2031.

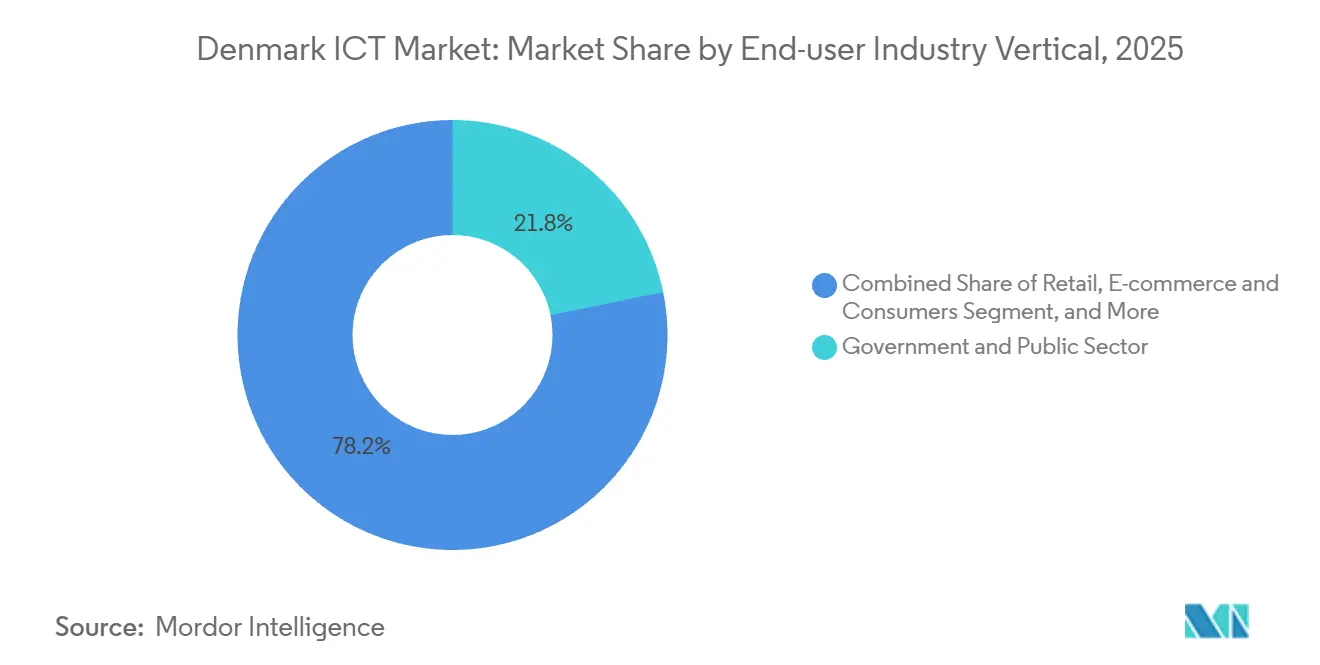

- By end-user vertical, Government and Public Sector accounted for 21.81% of the Denmark ICT market size in 2025, while Retail, E-commerce and Consumers is progressing at a 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Public-Sector Digitalization Targets | +1.2% | National focus on Copenhagen, Aarhus, Odense | Medium term (2-4 years) |

| Rising Adoption of Cloud-Native Architectures by SMEs | +1.0% | Nationwide with Greenland and Faroe Islands spillover | Short term (≤ 2 years) |

| Consistent Digital Transformation Initiatives | +0.9% | Countrywide | Long term (≥ 4 years) |

| Robust Telecommunication Infrastructure | +0.7% | Nationwide, early benefits in West Denmark | Medium term (2-4 years) |

| Growing VC Funding In Danish Deep-Tech Start-Ups | +0.5% | Greater Copenhagen hubs | Long term (≥ 4 years) |

| Sub-Sea Data-Cable Upgrades Enabling Low-Latency Services | +0.4% | National, Arctic links to Greenland and Faroe Islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Public-Sector Digitalization Targets

Government outlays of DKK 2 billion (USD 300 million) over 2022-2026 anchor the Denmark ICT market by funding interoperable platforms that streamline citizen services. The MitID authentication rollout exceeded 5.5 million users in 2025, replacing NemID and unifying access to e-Boks and borger.dk. Procurement frameworks increasingly reward Danish integrators with strong compliance records; Atea’s DKK 4.1 billion (USD 615 million) sole-supplier award covering 103 municipalities underscores the scale advantages. NNIT’s placement on the national health-data hub highlights interoperability mandates such as HL7 FHIR. Multi-year partnerships generate annuity revenue but also heighten vendor lock-in, raising the innovation bar for contract renewals.

Rising Adoption of Cloud-Native Architectures by SMEs

Cloud adoption reached 75% of Danish enterprises in 2023, well above the EU average, and the composition is tilting toward platform-as-a-service and SaaS layers.[1]Eurostat, “Cloud Computing Adoption in European Enterprises 2023,” ec.europa.eu SMEs, which comprise 99% of businesses, are driving hybrid-cloud growth by combining public elasticity with on-premises data residency to meet GDPR Article 32 requirements. AI experimentation, already at a 15% adoption rate, depends on container-based environments that automate DevOps workflows. [2]Danish Business Authority, “AI Adoption Survey 2024,” erhvervsstyrelsen.dk Kubernetes penetration is deepest in manufacturing and logistics, where seasonal peaks can quadruple compute demand. Until Microsoft’s December 2025 domestic region, many latency-sensitive workloads transited Stockholm or Frankfurt, adding round-trip delays that hindered real-time analytics.

Consistent Digital Transformation Initiatives

Although 69% of residents possessed basic digital skills in 2024, only 5.7% filled ICT specialist roles, creating a skills mismatch. Enterprises address gaps with low-code platforms that enable business analysts to automate workflows. MobilePay’s user base grew to over 4 million, underscoring the platform's migration from P2P payments to merchant integration. Retailers merge online and physical stores on omnichannel stacks, needing real-time inventory views. Integration with legacy ERP and CRM consumes up to 60% of large-enterprise IT budgets, sustaining demand for system integrators skilled in API gateways and data migration.

Robust Telecommunication Infrastructure

TDC NET achieved 99.7% 5G coverage and linked 820,000 homes via fiber by end-2024. [3]TDC NET, “Annual Report 2024,” tdcnet.dk Its 5G Standalone network enables slicing, reserving bandwidth for mission-critical use cases. Microsoft’s three planned data centers in Varde and Esbjerg will cut domestic round-trip latency below 5 milliseconds. The DKK 3 billion (USD 450 million) Greenland-Faroe-Denmark cable, due 2027, will shrink Arctic latency from satellite-scale 100 milliseconds to sub-20 milliseconds. Rural fiber economics remain challenging despite a EUR 110 million (USD 121 million) Nordic Investment Bank loan, creating reliance on fixed wireless and satellite backhaul.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Denmark’s Tight Tech-Talent Labor Pool | -0.8% | Copenhagen and Aarhus hotspots | Short term (≤ 2 years) |

| Price Pressures from Near-Shore EU Service Providers | -0.6% | Nationwide, affects IT services | Medium term (2-4 years) |

| Cybersecurity Skills Gap in Critical Infrastructure | -0.3% | Energy, healthcare, finance segments | Medium term (2-4 years) |

| Energy-Price Volatility Impacting Data-Center OPEX | -0.2% | West Denmark clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Denmark’s Tight Tech-Talent Labor Pool

ICT specialists formed only 5.7% of employment in 2024, far below the EU 2030 goal of 10%. Universities graduate roughly 3,000 computer science majors each year, yet multinational R&D hubs absorb talent rapidly, forcing SMEs to outsource or offshore. Fast-track work permits shorten visa cycles to 30 days, but Copenhagen’s high living costs deter recruits from emerging markets. Reliance on staff augmentation from Poland and Romania adds coordination overhead and intellectual property risks. Cybersecurity roles remain underfilled, even as ransomware events against critical infrastructure rose 40% in 2024.

Price Pressures from Near-Shore EU Service Providers

Polish, Romanian, and Baltic vendors undercut Danish labor rates by up to 50%, commoditizing application maintenance and helpdesk contracts. Domestic integrators pivot toward high-value consulting in regulated verticals, narrowing addressable demand. Netcompany pursued geographic diversification, landing a GBP 135 million (USD 169 million) HMRC deal in 2024. Cross-border delivery introduces currency and compliance risk, while global capability centers internalize work that once went to third parties, shrinking the outsourcing pool by as much as 25% according to industry surveys.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: IT Services Sustain Leadership Amid Security Boom

IT Services captured 34.48% of 2025 revenue after headline wins such as the DKK 3 billion Ministry of Taxation framework and Tryg’s seven-year digital overhaul. The Denmark ICT market size within IT Services reflects entrenched vendor relationships that bundle application development, integration, and managed operations into multi-year cycles. Clients prioritize outcome-based pricing, cloud orchestration, and AI-enabled automation, leaving commoditized break-fix contracts to smaller outfits. In parallel, heightened NIS2 obligations push security outlays beyond patch management toward managed detection and response, threat hunting, and zero-trust network design.

IT Security and Cybersecurity is the fastest-growing slice, expanding at a 6.43% CAGR through 2031. Providers differentiate through 24 × 7 SOC coverage, sovereign data-storage options, and playbooks mapped to EU directives. Meanwhile, hardware distributors see margin squeeze as public cloud discourages on-premise refreshes and as distributors consolidate to chase scale, evidenced by Atea’s buyout of KMD’s supply unit. SaaS adoption keeps software revenue recurring; SimCorp’s private-equity-backed subscription pivot underscores this migration.

By Enterprise Size: SME Cloud Momentum Counters Large-Enterprise Dominance

Large Enterprises still generated 54.82% of 2025 spending, largely because heavyweights such as Novo Nordisk and Maersk run hybrid estates that demand big-ticket ERP, cybersecurity, and private-cloud capacity. These firms underpin the Denmark ICT market share for bespoke consulting and colocation contracts. SMEs, however, post a 6.83% CAGR, closing capability gaps via turnkey SaaS and platform services.

Subsidized vouchers under the SMV: Digital program, worth DKK 185 million (USD 27 million), cut migration costs and spur take-up of e-commerce engines, CRM, and bookkeeping SaaS. The December 2025 Azure region announcement further lowers latency and sovereignty concerns, letting SMEs deploy customer-facing workloads domestically while tapping global hyperscale features.

By End-User Industry Vertical: Government Spend Stays Predominant as Retail Surges

Government and Public Sector commanded 21.81% of 2025 demand, cementing its role as anchor client for large integrators. Framework agreements guarantee steady inflows for modernization of tax, welfare, and identity platforms. The Denmark ICT market size within public services benefits from mandatory compliance timelines, creating long queues of change orders and extension scopes.

Retail, E-commerce and Consumers, by contrast, tops the growth table at 6.57% CAGR as merchants roll out unified-commerce suites, AI-driven personalization, and warehouse robots to serve Denmark’s near-universal internet audience. Banks and insurers remain steady investors, funneling core-system migrations and open-banking APIs, while manufacturers digitize assembly lines to offset high labor costs.

Geography Analysis

Greater Copenhagen accounts for roughly 40% of Denmark ICT market spending, buoyed by headquarters, ministries, and universities. Aarhus and Odense form secondary clusters centered on manufacturing and regional healthcare, while the Faroe Islands and Greenland gain relevance through new fiber links that cut latency from triple-digit satellite ranges to under 20 milliseconds.

West Denmark emerges as a sovereign-cloud zone after Microsoft’s data-center commitment, drawing oil-and-gas and logistics workloads that require proximity compute. Denmark leverages renewable energy and cool temperatures to compete with Iceland and Norway for hyperscale colocation. Rural municipalities below 500 inhabitants per square kilometer remain dependent on 5G fixed wireless, constraining IoT penetration in agriculture.

Alignment with GDPR, NIS2, and the forthcoming AI Act eases cross-border data flow inside the EEA but hikes compliance costs for SMEs lacking legal staff. The Danish Centre for Cybersecurity mandated 24-hour incident reporting following a surge in ransomware in 2024. Proximity to Germany and Sweden fosters joint innovation corridors yet exposes domestic providers to larger rivals.

Competitive Landscape

Global hyperscalers compete with Danish integrators in a fragmented arena. Microsoft, Amazon Web Services, and Google Cloud invest over USD 1 billion in local capacity, wagering on latency, data residency, and green power. Netcompany, KMD, NNIT, and Atea anchor domestic contracts worth billions of Danish kroner during 2024-2025. Atea’s DKK 4.1 billion (USD 615 million) municipality frame agreement illustrates winner-take-most dynamics in public procurement.

Strategies emphasize regulated-sector specialization; NNIT dominates life sciences, Netcompany leads government digitalization, and KMD retains municipal tax and welfare software. White-space opportunities arise in edge computing for offshore wind farms and AI-driven automation for SMEs. Deep-tech start-ups funded with EUR 300 million (USD 330 million) in new capital are developing quantum and photonic processors. Nearshore competitors compress commodity-service margins, forcing Danish players toward value-added consulting.

Firms mastering Kubernetes orchestration, zero-trust networking, and AI model governance gain pricing power, while those reliant on legacy infrastructure see erosion. Mergers and cross-border contracts, such as Netcompany’s HMRC deal and Deutsche Börse’s EUR 3.9 billion (USD 4.29 billion) SimCorp acquisition, signal consolidation and geographic diversification. Additionally, the growing emphasis on ESG compliance is reshaping investment strategies across industries.

Denmark ICT Industry Leaders

Oracle

Microsoft Corporation

Google LLC

International Business Machines Corporation

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft outlined three new data centers in Varde and Esbjerg, designed for 100% renewable energy.

- December 2025: NNIT signed a four-year framework with the Agency for IT and Learning to provide AI-driven digital-learning platforms.

- December 2025: NNIT and Edora were chosen to build the national health-data hub compliant with HL7 FHIR standards.

- November 2025: Netcompany secured a nationwide digital infrastructure contract with the Scottish government.

Denmark ICT Market Report Scope

Information and communications technology (ICT) is an extended term for information technology (IT) that encompasses a wide range of hardware, software, internet- and telecommunications-based services, social networking, media applications, and so on. The technology allows users to access, retrieve, store, send, and manipulate information in digital form. ICT has become more popular as the need for more advanced solutions like IoT, cloud computing, big data, content management, and so on has grown.

The Denmark ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, and Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), End-user Industry Vertical (BFSI, Government and Public Sector, Oil and Gas, IT and Telecom, Retail E-commerce and Consumers, Manufacturing and Industrial, Energy and Utilities, Healthcare, Other End-user Industry Verticals). The Market Forecasts are Provided in Terms of Value USD.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | Application Security |

| Cloud Security | |

| Data Security | |

| Network Security | |

| Endpoint Security | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Identity and Access Management (IAM) | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| BFSI |

| Government and Public Sector |

| Oil and Gas |

| IT and Telecom |

| Retail, E-commerce and Consumers |

| Manufacturing and Industrial |

| Energy and Utilities |

| Healthcare |

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | Application Security | |

| Cloud Security | ||

| Data Security | ||

| Network Security | ||

| Endpoint Security | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Identity and Access Management (IAM) | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | BFSI | |

| Government and Public Sector | ||

| Oil and Gas | ||

| IT and Telecom | ||

| Retail, E-commerce and Consumers | ||

| Manufacturing and Industrial | ||

| Energy and Utilities | ||

| Healthcare | ||

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) | ||

Key Questions Answered in the Report

How large is the Denmark ICT market in 2026?

It reached USD 18.59 billion in 2026 and is set to climb toward USD 23.74 billion by 2031 at a 5.01% CAGR.

Which product segment grows the fastest through 2031?

IT Security and Cybersecurity expands at a 6.43% CAGR, outpacing all other offerings driven by NIS2 compliance needs.

Why are SMEs adopting cloud so quickly in Denmark?

Pay-as-you-go pricing, government SMV: Digital vouchers, and the new in-country Azure region lower both cost and data-sovereignty hurdles.

What restrains Denmark ICT spending despite strong demand?

A tight tech-talent pool and volatile electricity prices raise delivery and operating costs, tempering the overall growth rate.

Which geography outside Copenhagen is becoming a datacenter hub?

Esbjerg and Varde in West Denmark gain prominence thanks to renewable energy abundance and new subsea cable landings.

Page last updated on: