Market Overview

| Study Period | 2019 - 2030 |

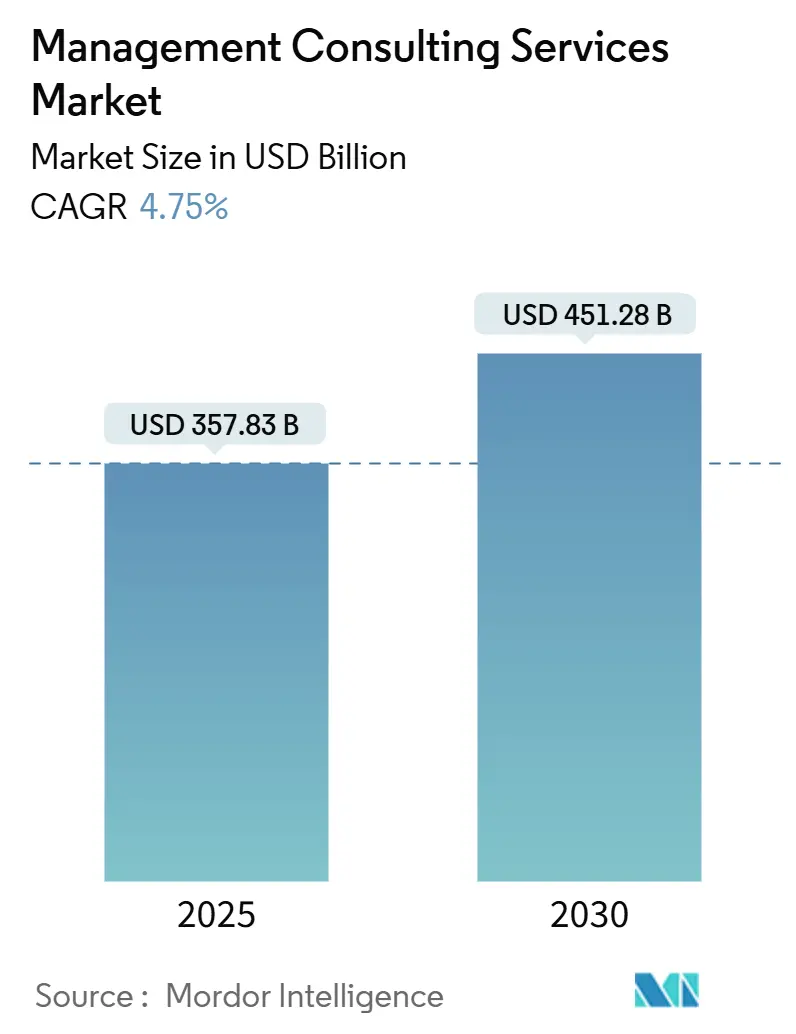

| Market Size (2025) | USD 357.83 Billion |

| Market Size (2030) | USD 451.28 Billion |

| Growth Rate (2025 - 2030) | 4.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Management Consulting Services Market Analysis by Mordor Intelligence

The management consulting services market generated USD 357.85 billion in 2025 and is forecast to reach USD 451.28 billion in 2030, advancing at a 4.75% CAGR. Solid demand for external expertise in digital transformation, risk management, and operational excellence underpins this steady growth path. Enterprises worldwide keep expanding AI, cloud, and sustainability programs, and they rely on consultants to close capability gaps, standardize best practices, and speed execution. Ongoing regulatory shifts, especially around ESG rules, add further impetus as companies seek guidance to comply without stalling innovation. A parallel rise in remote-first delivery models lowers engagement costs while enlarging addressable client pools, strengthening market resilience even during macroeconomic uncertainty.

Key Report Takeaways

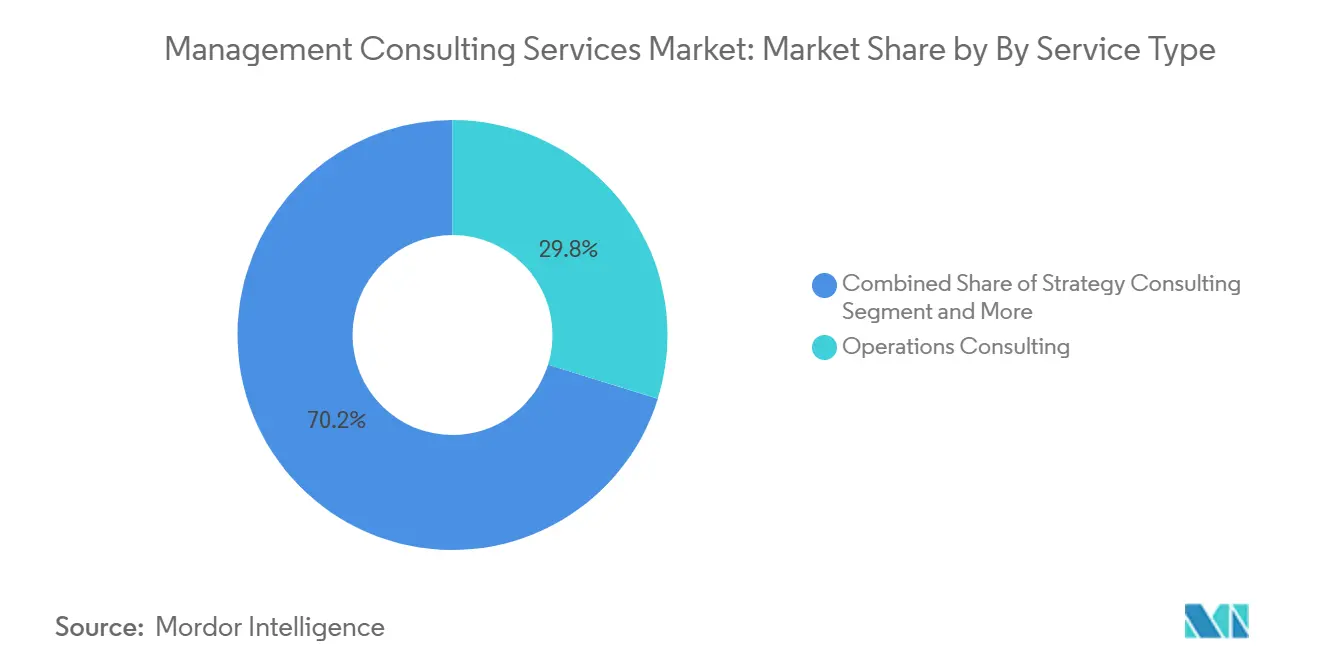

- By service type, Operations Consulting led with 29.80% revenue share in 2024; Digital Transformation Consulting is projected to expand at a 13.40% CAGR through 2030.

- By end-user industry, Financial Services commanded 24.30% of the market in 2024, whereas Healthcare and Life Sciences is poised to grow at an 11.80% CAGR to 2030.

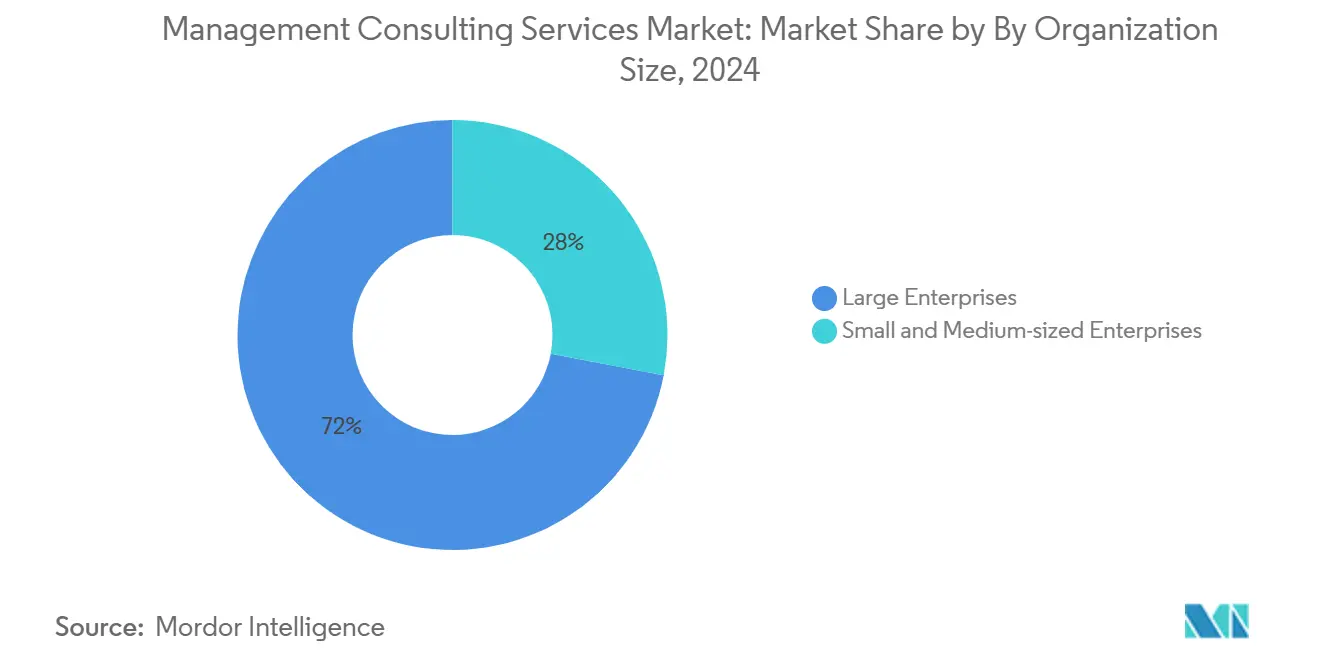

- By organization size, Large Enterprises held 72.00% of demand in 2024, while Small and Medium-sized Enterprises are expected to post a 9.90% CAGR to 2030.

- By delivery model, On-site Consulting accounted for 61.50% of the market in 2024; Remote and Virtual Consulting is on track for a 14.60% CAGR through 2030.

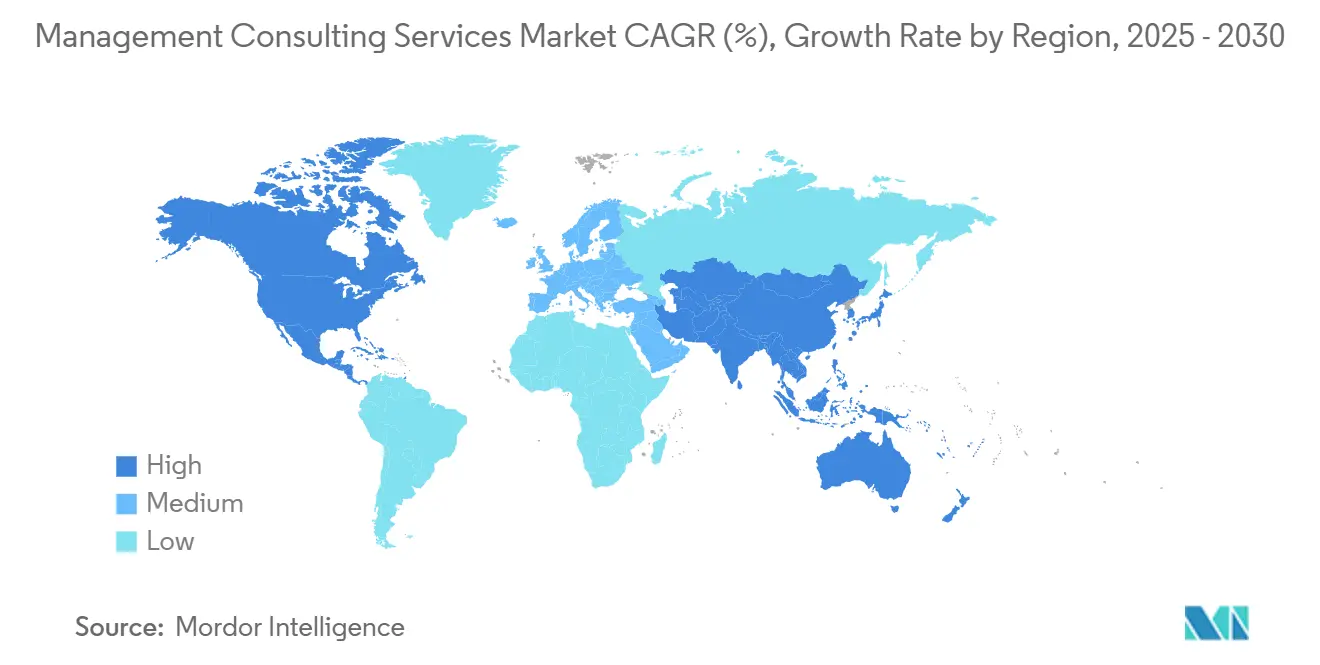

- By geography, North America led with 37.90% market share in 2024, and Asia-Pacific is forecast to be the fastest-growing region at a 10.70% CAGR to 2030.

Global Management Consulting Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first transformation demand | +1.2% | Global, especially North America and Asia-Pacific | Medium term (2-4 years) |

| Regulatory and risk-management complexity | +0.8% | Global, notably EU and North America | Long term (≥ 4 years) |

| Outsourcing of strategy and operations expertise | +0.6% | Global, emerging-market focus | Medium term (2-4 years) |

| Emerging-market enterprise growth | +0.9% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| ESG-linked consulting mandates | +0.7% | Global, EU leading adoption | Medium term (2-4 years) |

| AI “consulting-as-a-service” models | +0.5% | North America and EU early adoption | Short term (≤ 2 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Digital-first transformation demand

Organizations allocate record budgets to AI integration, cloud migration, and data-centric architectures. Technology consulting spending is set to exceed USD 400 billion in 2025, and 87% of enterprises that embarked on digital overhauls now rely on external advisors[1]Datacentre Solutions Staff, “Global Enterprises Accelerate Digital Transformation Spend,” datacentresolutions.com. Generative AI projects already represent up to 40% of new engagements among leading firms, pushing consultants to deliver intertwined technology roadmaps, change-management programs, and workforce reskilling packages in multi-year deals. Financial services and healthcare are focal points because regulatory scrutiny magnifies implementation complexity. The outcome is a sustained pipeline that balances near-term efficiency with long-term modernization goals.

Regulatory and risk-management complexity

Expanding ESG and data-privacy rules amplify demand for compliance advisory. The EU Corporate Sustainability Reporting Directive alone fuels an estimated USD 2 billion annual consulting opportunity. Banks and insurers face layered capital, conduct, and cyber-resilience standards that require risk assessment frameworks and reporting automation. Energy and healthcare operators confront parallel mandates tied to safety and environmental disclosures. Consultants supply audit-ready methodologies, RegTech integration skills, and cross-border policy insight, turning compliance from a cost center into a driver of structured transformation spending.

Outsourcing of strategy and operations expertise

Executives increasingly contract out complex planning, process redesign, and cost-optimization tasks to tap objective, industry-specific know-how. Outcome-based engagements now stipulate measurable performance gains that justify fees, aligning consultant incentives with client value. Demand is acute in emerging markets where local firms seek the best global practices to scale. Providers respond by codifying playbooks for supply-chain resilience, digital marketing, and sustainability, enhancing repeatability and profit margins. The shift also broadens the management consulting services market as standardized offerings attract mid-tier clients.

Emerging-market enterprise growth

Rapid economic expansion in Asia-Pacific, Latin America, and parts of the Middle East brings new entrants to the consulting buyer pool. Digital infrastructure buildouts and government modernization programs spur large public-sector engagements, while regional tech champions require market-entry and operational-scaling support. For example, Southeast Asian fintech firms regularly engage consultants for regulatory navigation and product localization. This wave of regional demand offsets slower growth in certain mature markets and lifts global revenue prospects through 2030.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage and high attrition | -0.9% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Rise of low-cost freelance platforms | -0.6% | Global, mid-market focus | Medium term (2-4 years) |

| Outcome-based fee pressure | -0.4% | Global, led by mature markets | Medium term (2-4 years) |

| Data-sovereignty delivery limits | -0.3% | EU and Asia-Pacific regulatory environments | Long term (≥ 4 years) |

Source: Mordor Intelligence

Talent shortage and high attrition

Consulting firms report attrition rates near 15-20%, while professional-services utilization has dipped as staffing gaps widen. Specialists in AI and advanced analytics command premium salaries, compressing margins. Firms invest in accelerated promotion tracks, flexible work arrangements, and alumni boomerang programs, yet chronic shortages persist. Selective project bidding and tighter resource allocation mitigate the immediate capacity squeeze but may constrain overall market expansion until talent pipelines mature.

Rise of low-cost freelance platforms

Digital marketplaces now match enterprises with seasoned strategists and technologists at rates below traditional firm fee structures. Platforms such as Upwork enable modular project sourcing, a model that gains traction as remote delivery proves credible[3]Upwork Research, “Distributed Consulting Talent Report 2025,” upwork.com. The commoditization of discrete tasks—competitive benchmarking, data visualization, code prototyping—intensifies price pressure on mid-tier consultancies. To defend premium positioning, established firms emphasize integrated end-to-end solutions, proprietary data assets, and risk-sharing contract terms that freelancers cannot easily replicate.

Segment Analysis

By Service Type: Operational Excellence Sustains Leadership

Operations Consulting captured 29.80% of the management consulting services market in 2024, reflecting persistent client focus on cost control and process rigor. The segment’s depth in lean methodologies, supply-chain diagnostics, and performance benchmarking secures recurring engagements. Digital Transformation Consulting, propelled by accelerated AI and cloud adoption, is forecast to advance at a 13.40% CAGR to 2030, making it the primary growth engine. Together, these segments form complementary value propositions as clients merge technology upgrades with workflow redesign. Strategy Consulting maintains relevance for market expansion and portfolio recalibration, while HR and Financial Advisory Consulting benefit from workforce realignment and ESG-linked reporting needs.

The convergence of operational and digital mandates spawns hybrid offerings where consultants embed AI-enabled analytics into process-improvement roadmaps. For instance, industrial clients now expect predictive maintenance models alongside classical throughput analysis, enabling double-digit efficiency gains. Such cross-disciplinary approaches allow firms to command higher fees and protect client relationships from specialist insurgents. As a result, revenue mix continues to shift toward technology-infused services, reinforcing the long-term position of providers that scale digital talent pools early.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Financial Services Anchor Demand

Financial Services accounted for 24.30% of the management consulting services market in 2024, driven by digital banking, capital-efficiency programs, and compliance transformations. The vertical relies on consultants to orchestrate core-system modernization, risk-model validation, and fintech partnership strategies. Healthcare and Life Sciences is projected to expand at an 11.80% CAGR through 2030, spurred by digital health adoption and stricter regulatory oversight. Manufacturing clients seek Industry 4.0 roadmaps, while Energy players turn to advisors for grid modernization and sustainability metrics.

Cross-industry themes such as cybersecurity, data governance, and ESG reporting integrate with sector-specific challenges, intensifying the need for specialized, multidisciplinary teams. In practice, financial institutions now procure bundled offerings spanning AI fraud detection, climate-risk modeling, and customer-experience redesign. Consultants that assemble domain experts with technology architects thus secure multi-year mandates, locking in revenue visibility and raising switching costs for clients.

By Organization Size: SME Uptake Accelerates

Large Enterprises held 72.00% of spending in 2024 thanks to complex global footprints and sizable transformation budgets. Yet SME adoption is on a 9.90% CAGR trajectory, sustained by affordable, modular service packages delivered remotely. AI-powered diagnostics and templated playbooks lower entry barriers, allowing smaller firms to contract outcome-oriented advisory without heavy upfront fees. This democratization broadens the management consulting services market size and diversifies revenue streams for providers that can balance volume with customization.

Enterprise clients increasingly stipulate performance-linked fees, reinforcing demand for data-driven engagement governance. In response, consulting firms deploy dashboards that track KPIs in real time, enhancing transparency and trust. SMEs, conversely, often prioritize rapid implementation and cash-flow discipline, pushing consultants to shorten project cycles and adopt subscription models. The dual-track evolution of client expectations compels firms to refine segmentation strategies and resource allocation to safeguard profitability.

By Delivery Model: Remote Engagement Gains Scale

On-site Consulting preserved 61.50% share in 2024 as many complex programs still benefit from in-person workshops and stakeholder alignment sessions. Remote and Virtual Consulting, however, is set to climb at a 14.60% CAGR through 2030 as cloud collaboration tools mature and clients normalize distributed work. Hybrid models blend virtual sprints with milestone on-site visits, offering cost-efficient access to global experts without sacrificing relationship depth.

Digital whiteboarding, secure data-rooms, and AI-assisted document drafting cut cycle times while facilitating 24/7 availability across time zones. Consultants pass efficiency gains to clients through slimmer travel budgets and faster deliverables, reinforcing perceived value. Competition intensifies as specialist boutiques leverage virtual reach to contest engagements historically reserved for large incumbents. The resulting pressure accelerates investment in proprietary platforms that differentiate through speed, analytics breadth, and implementation linkage.

Geography Analysis

North America retained 37.90% of the management consulting services market share in 2024 on the back of robust enterprise technology spending and a dense regulatory environment across banking, healthcare, and energy. Generative AI project demand now constitutes up to 40% of new contracts, lifting revenue per consultant as high-value advisory replaces commodity deliverables. Federal agencies also ramp up digital-services procurement, while private-sector clients intensify ESG and cyber-resilience initiatives. The region’s shift to hybrid engagement models enables firms to serve global subsidiaries without eroding margins, preserving leadership status through the forecast period.

Asia-Pacific is the fastest-growing territory with a 10.70% CAGR outlook to 2030, propelled by rapid digitalization, infrastructure rollout, and multinational regional investment. Consulting spend concentrates on financial services modernization, healthcare digitization, and manufacturing productivity. Governments across India and Southeast Asia commission smart-city blueprints and public-sector modernization studies, expanding addressable demand. Local consultancy challengers capitalize on cultural fluency and lower cost bases, but global firms maintain an edge in complex cross-border transactions and deep technical skills.

Europe posts steady expansion anchored in ESG compliance mandates and advanced data-privacy rules. The EU Corporate Sustainability Reporting Directive drives firm pipelines in sustainability reporting, while energy transition policies spark grid-modernization advisory across Germany, France, and the Nordics. Financial institutions prioritize digital core upgrades to meet open-banking norms. Data-sovereignty concerns encourage clients to engage advisors with regional hosting partners and specialized governance frameworks, reinforcing demand for niche regulatory expertise.

Competitive Landscape

The management consulting services market is moderately fragmented, with the Big Four audit-linked groups and top strategy houses still dominating large, multi-country transformations. Their combined scale supports heavy investment in generative AI toolkits that automate knowledge retrieval, code generation, and slide production, lifting consultant productivity while safeguarding premium pricing. McKinsey’s “Lilli” platform now underpins 70% of proposal drafting and presentation workflows, showcasing early first-mover benefits.

Mid-tier and boutique firms counter by specializing in high-growth niches such as cloud FinOps, industrial IoT, and Scope 3 carbon accounting. MandA remains a favored path to bolt on scarce capabilities; A.T. Kearney’s purchase of Project Partners Management GmbH broadened SAP S/4HANA capacity in the DACH region[2]Bird & Bird M&A Updates, “Kearney Acquires Project Partners Management GmbH,” birdandbird.com. Freelance talent networks increase competitive pressure at the bottom end of the market by offering modular expertise at lower cost, forcing incumbents to highlight integrated delivery scale and risk-sharing commercial models.

Technology vendors also encroach via consulting arms that couple software licenses with strategic advisory. Cognizant’s USD 5.1 billion Q1 2025 revenue illustrates how tech-services lineage can translate into full-stack transformation engagements. As service lines converge, competitive advantage rests on cross-disciplinary teams, proprietary data assets, and proven outcome-based contracts.

Management Consulting Services Industry Leaders

-

McKinsey & Company

-

Boston Consulting Group

-

Deloitte Touche Tohmatsu Limited

-

Accenture plc

-

PricewaterhouseCoopers LLP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: McKinsey and Company broadened its AI platform Lilli, automating proposal and presentation creation for more than 70% of consultants .

- May 2025: Huron Consulting Group reported Q1 2025 revenue of USD 395.7 million, up 11.2% year over year.

- April 2025: Cognizant Technology Solutions posted Q1 2025 revenue of USD 5.1 billion, a 7.5% rise, and announced major wins with Boehringer Ingelheim and Citizens Financial Group.

- April 2025: Boston Consulting Group disclosed record 2023 revenue of USD 12.3 billion with a workforce of 32,000 consultants.

Global Management Consulting Services Market Report Scope

Management consulting offers services to businesses to enhance their performance or achieve organizational goals. Management consulting firms examine operations and determine organizational inefficiencies, from high raw material costs to HR policies. They then employ their knowledge to devise a strategy for resolving all difficulties most effectively.

The management consulting services market is segmented by type (HR consulting, strategy consulting, operations consulting), end-user industry (IT & telecommunication, healthcare, hotel & hospitality, media & entertainment, real estate), and geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa). The market sizes and forecasts are provided in terms of value in USD for all the segments.

| By Service Type | Strategy Consulting | |||

| Operations Consulting | ||||

| HR Consulting | ||||

| Financial Advisory Consulting | ||||

| Digital Transformation Consulting | ||||

| Risk and Compliance Consulting | ||||

| Other Service Types | ||||

| By End-user Industry | IT and Telecommunications | |||

| Healthcare and Life Sciences | ||||

| Financial Services (BFSI) | ||||

| Manufacturing and Industrial | ||||

| Energy and Utilities | ||||

| Government and Public Sector | ||||

| Real Estate and Construction | ||||

| Retail and Consumer Goods | ||||

| Media, Entertainment and Sports | ||||

| Hospitality and Travel | ||||

| Other Industries | ||||

| By Organization Size | Large Enterprises | |||

| Small and Medium-sized Enterprises | ||||

| By Delivery Model | On-site Consulting | |||

| Remote / Virtual Consulting | ||||

| Hybrid Consulting | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Nordics | ||||

| Rest of Europe | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Egypt | ||||

| Nigeria | ||||

| Rest of Africa | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| ASEAN | ||||

| Australia | ||||

| New Zealand | ||||

| Rest of Asia-Pacific | ||||

By Service Type

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Service Types |

By End-user Industry

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

By Organization Size

| Large Enterprises |

| Small and Medium-sized Enterprises |

By Delivery Model

| On-site Consulting |

| Remote / Virtual Consulting |

| Hybrid Consulting |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the management consulting services market?

The market generated USD 357.85 billion in 2025 and is projected to reach USD 451.28 billion by 2030.

Which service segment is growing the fastest?

Digital Transformation Consulting is expected to register a 13.40% CAGR through 2030, driven by AI and cloud adoption.

Which region offers the strongest growth opportunities for consulting firms?

Asia-Pacific is forecast to expand at a 10.70% CAGR as rapid digitalization and infrastructure spending fuel demand.

How are delivery models changing in the industry?

Remote and Virtual Consulting is advancing at a 14.60% CAGR, supported by collaboration platforms that lower project costs.

What is the biggest challenge facing consulting providers today?

A global talent shortage, with attrition rates near 15-20%, pressures margins and delivery capacity.

Page last updated on: July 3, 2025