Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.04 Billion |

| Market Size (2026) | USD 4.19 Billion |

| Market Size (2031) | USD 5.07 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

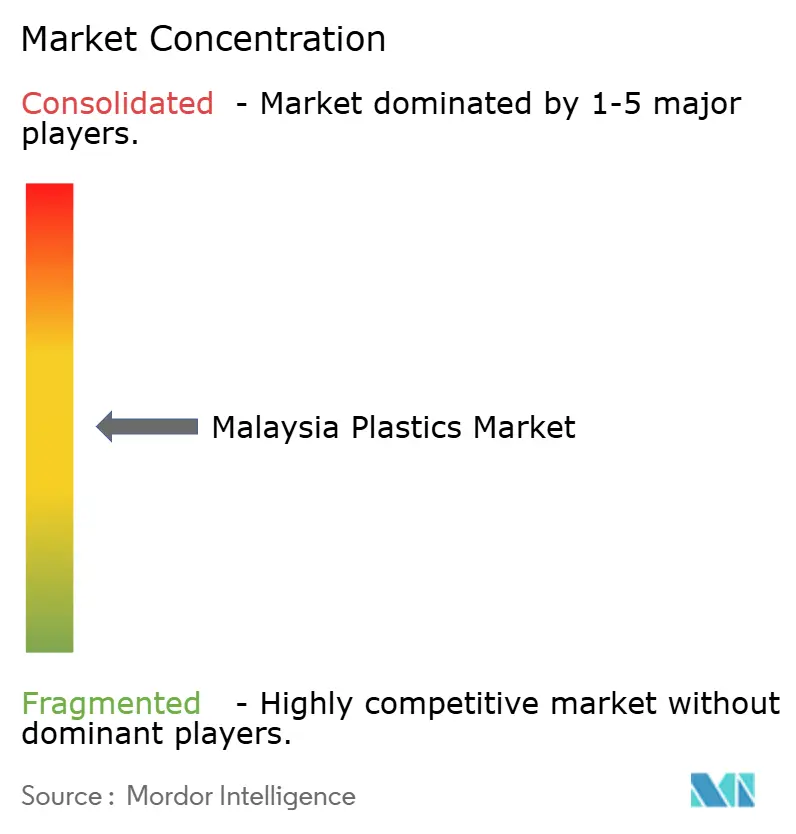

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Plastics Market Analysis by Mordor Intelligence

The Malaysia Plastics Market size in 2026 is estimated at USD 4.19 billion, growing from 2025 value of USD 4.04 billion with 2031 projections showing USD 5.07 billion, growing at 3.86% CAGR over 2026-2031. This steady expansion is anchored by Malaysia’s dual role as a regional petrochemical feedstock hub and a downstream manufacturing base that supplies the electronics, automotive, and packaging value chains across Southeast Asia. Stable feedstock from PETRONAS’s integrated complexes, export-oriented manufacturing clusters in Selangor, Johor, and Penang, and policy-driven incentives for downstream petro-chemicals together reinforce supply security and cost competitiveness. Momentum is further supported by global brands demanding recycled or bio-based content, Malaysia’s zero single-use plastics roadmap, and investments in automated processing that counter skills shortages. Meanwhile, environmental regulation and feedstock price volatility continue to temper margins but also catalyze upgrades into higher-value applications where specialty grades and precision molding command premium pricing.

Key Report Takeaways

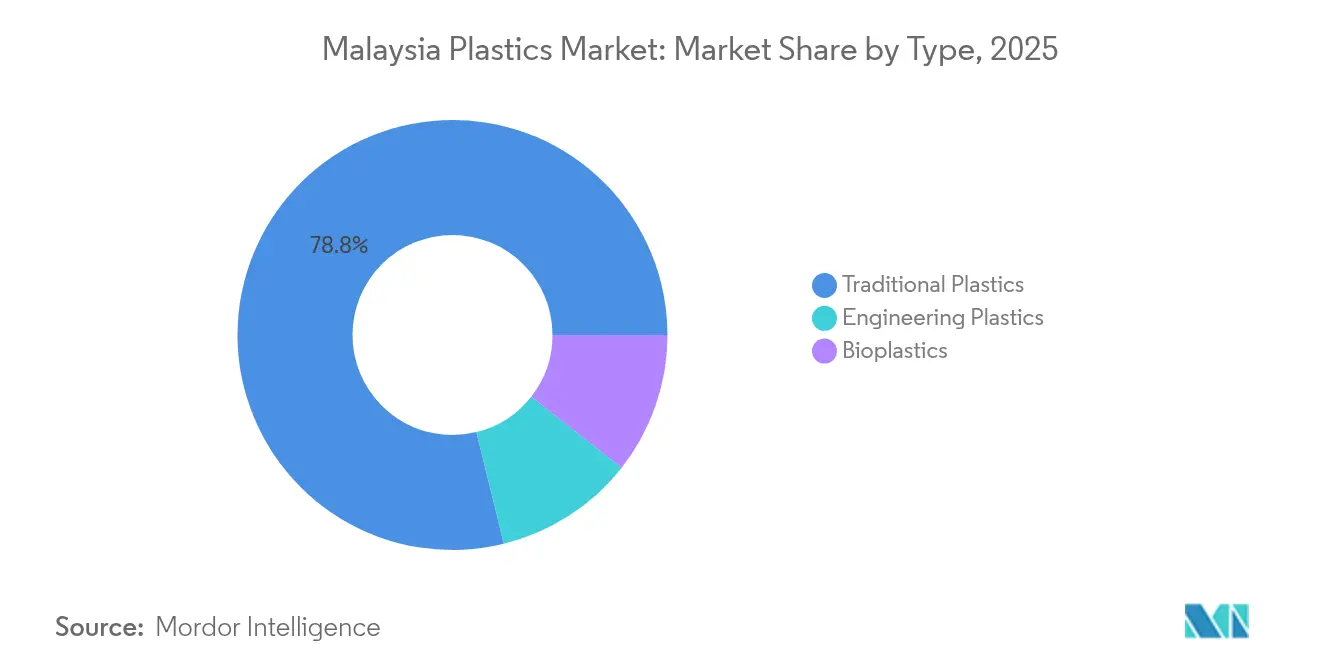

- By type, traditional plastics led with 78.84% Malaysia plastics market share in 2025; bioplastics are forecast to expand at a 4.86% CAGR through 2031.

- By technology, extrusion accounted for 49.96% of the Malaysia plastics market size in 2025, while blow molding is projected to advance at a 3.92% CAGR to 2031.

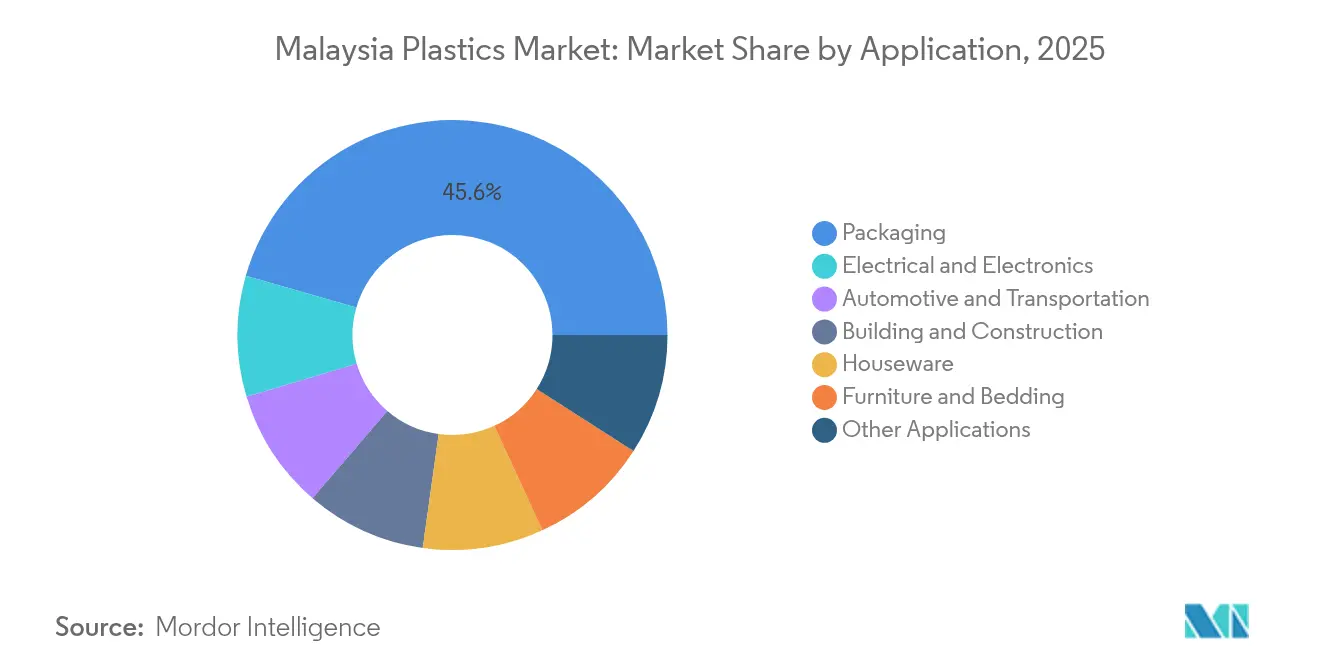

- By application, packaging captured 45.56% of the Malaysia plastics market share in 2025; electrical and electronics represent the fastest-growing application with a 3.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Plastics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from food and beverage packaging | +1.4% | National, with concentration in Selangor and Johor industrial zones | Medium term (2-4 years) |

| Growth of electronics manufacturing ecosystem | +1.2% | Penang, Selangor, Johor with spillover to Kedah and Melaka | Long term (≥ 4 years) |

| Government incentives for downstream petro-chemicals | +0.8% | National, focused on Johor (PIC), Terengganu, and Sarawak | Short term (≤ 2 years) |

| Circular-economy commitments by global brands | +0.6% | Export-oriented regions: Selangor, Johor, Penang | Medium term (2-4 years) |

| Expansion of medical-device clusters | +0.5% | Penang, Selangor with emerging presence in Johor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Food and Beverage Packaging

Food and beverage manufacturers rely on plastic barrier films and multilayer structures to meet higher food-safety standards in export markets. PETRONAS’s decision to embed a biorefinery inside the Pengerang Integrated Complex signals an upcoming local supply of bio-based packaging resins[1]Petroliam Nasional Berhad, “PETRONAS Strengthens Its Position for Future Growth Amid Global Energy Shifts,” petronas.com . Halal certification rules, prevalent in Malaysia’s export food trade, necessitate specialized packaging that maintains product integrity during long transit times. Rising urban income levels and a preference for ready-to-eat formats amplify the consumption of convenience packaging. As a result, converters supplying stand-up pouches, retort pouches, and PET beverage bottles are securing premium margins tied to performance and sustainability credentials.

Growth of Electronics Manufacturing Ecosystem

Malaysia’s National Semiconductor Strategy has attracted fresh investments from global players such as Infineon to expand back-end packaging, testing, and IC design activities. Semiconductor modules for 5G infrastructure and electric vehicles increasingly specify engineering plastics with high thermal stability and flame-retardant performance. Injection molding lines capable of micron-level tolerances are therefore proliferating within Penang’s Bayan Lepas and Kulim High-Tech parks. Automated vision inspection and closed-loop molding systems allow manufacturers to meet tight defect-rate requirements while offsetting the local skills gap in precision polymer processing.

Government Incentives for Downstream Petro-Chemicals

The Malaysian Investment Development Authority (MIDA) continues to provide tax holidays on value-added polymer production, while the 2025 federal budget allocated RM 200 million (USD 44.4 million) for reverse-vending machine deployment to improve plastics collection[2]Voloschuk C., “Malaysia to set stricter plastic import controls,” recyclingtoday.com. PETRONAS has earmarked USD 92.74 billion for clean-energy upgrades—including carbon capture and storage—that will progressively cut the emissions intensity of domestic resin output. The expansion of the Pengerang Integrated Complex into specialty chemicals provides local access to higher-margin polymers used in aerospace interiors and lightweight automotive components.

Circular-Economy Commitments by Global Brands

Multinationals such as ExxonMobil have begun piloting advanced recycling units in Malaysia to supply chemically recycled resins at a commercial scale. At the same time, the European Union’s Packaging and Packaging Waste Regulation is forcing Malaysian converters to certify recycled-content levels on export shipments. Dow’s success in launching glove packaging containing 60% post-consumer recycled material demonstrates that high-recycled-content films can pass stringent barrier and printability tests. These developments strengthen demand for consistent, locally sourced recycled pellets and drive investment into sophisticated washing, color-sorting, and de-inking systems close to major ports.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and single-use bans | -0.7% | National, with stricter enforcement in urban areas | Short term (≤ 2 years) |

| Feed-stock price volatility | -0.5% | National, affecting all polymer producers | Medium term (2-4 years) |

| Skills gap in advanced polymer processing | -0.3% | Industrial zones: Selangor, Johor, Penang with spillover to emerging centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Single-Use Bans

Malaysia’s 2025-2030 zero single-use plastics roadmap imposes phased restrictions on disposable bags, straws, and EPS foodware. Import controls on plastic scrap, tightened in July 2025, have removed low-cost feedstock streams but improved public perception of domestic waste handling. Converters that cannot pivot to recyclable or compostable formats face higher excise levies and tighter enforcement in Greater Kuala Lumpur, Johor Bahru, and George Town. Conversely, firms with compostable film lines and reusable food-service models are capturing the shift toward regulatory-compliant alternatives.

Feedstock Price Volatility

Global propylene and ethylene benchmarks routinely swing on refinery turnarounds and demand shifts in China, raising resin-price uncertainty for extruders and molders. While PETRONAS’s upstream capacity offers a partial hedge, export-oriented processors still purchase on international formulas that track crude-oil dynamics. Volatile natural-gas tariffs also feed directly into electricity-intensive operations such as twin-screw compounding. For smaller companies, these cost swings hinder long-term supply contracts and slow capital spending on new technology. Some players respond by integrating recycling lines to diversify raw-material sourcing and shield margins from virgin-resin price shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Traditional Dominance Faces Sustainability Pressure

Traditional polymers such as polyethylene and polypropylene retained 78.84% Malaysia plastics market share in 2025, buoyed by Pengerang’s integrated cracker and polymer lines that anchor low-cost output. Bioplastics, however, are forecast to grow fastest at a 4.86% CAGR, aided by brand targets for compostable packaging and the country’s single-use ban trajectory. Engineering resins addressing electrical insulation and under-hood automotive parts achieved mid-single-digit growth, supported by imported semifinished compounds rewired for localized finishing.

Producers associated with the Malaysia plastics market leverage existing cracker-to-film logistics to supply high-volume FMCG applications, yet face mounting EPR levies that narrow margins. The upcoming biorefinery within Johor’s complex will enable drop-in replacements for fossil-based PET and PE, positioning local converters to claim advanced recycling credit in export tenders. Specialty compounders catering to the Malaysia plastics industry gain premium prices by offering flame-retardant, glass-fiber, and halogen-free grades, particularly for smart-device connectors. A widening skills gap in materials science underscores the value of technical service teams able to qualify new bio-based grades for food-contact and electronic-component certification.

By Technology: Automation Drives Processing Innovation

Extrusion continues to dominate with 49.96% of the Malaysia plastics market size in 2025, servicing film, sheet, and pipe production across food packaging and infrastructure segments. Blow molding is projected to outpace at a 3.92% CAGR owing to rising demand for pharmaceutical bottles and personal-care containers that require multilayer oxygen barriers. Injection molding lines equipped with servo-hydraulic systems registered capital-spending gains in Penang’s EMS corridor, where precision tolerances are critical to semiconductor packaging.

Co-extruders add gravimetric dosing and inline barrier-layer control to reduce scrap and energy use. Blow-molders installing all-electric machines report 20% lower power consumption, aligning with corporate net-zero mandates. Molders serving medical-device OEMs equip ISO-class clean rooms and SCADA-enabled traceability to meet U.S. FDA and EU MDR export approvals. This technology race differentiates firms that can accommodate bioplastic rheology shifts and recycled-pellet variability without yield loss.

By Application: Electronics Sector Drives Premium Growth

Packaging retained a 45.56% share of the Malaysia plastics market size in 2025, capitalizing on halal-certified food exports to the Middle East and ready-to-drink beverages across ASEAN. Yet electrical and electronics components will post the fastest 3.96% CAGR through 2031, fueled by chiplet-level encapsulation, EMI shielding films, and high-temperature sockets for SiC power modules. Building and construction, while a smaller consumption base, benefits from PVC pipe replacement cycles and urban railway projects.

Malaysia’s semiconductor ascendancy allows precision-molders to insert engineered resins into LED optics, smartphone camera spacers, and ADAS sensor housings. Packaging converters diversify into mono-material laminates to comply with Europe’s 95% recyclability threshold. Automotive OEMs sourcing from Pekan and Kulim demand lightweight PP/ABS interior trim to lower overall vehicle mass, opening supply windows for compounding houses that pre-color and pre-foam resins. Across these verticals, the Malaysia plastics market aligns growth toward performance-critical niches that justify higher per-kilogram value over commodity grades.

Geography Analysis

The Malaysia plastics market draws on a tri-cluster axis: Johor for feedstock, Selangor for processing scale, and Penang for high-precision electronics applications. Johor’s Pengerang Integrated Complex ensures steady ethylene and propylene supply, thus insulating converters from regional import parity swings. Selangor hosts the widest converter base, served by Port Klang’s global shipping routes and proximity to Kuala Lumpur’s consumer hub.

Emerging east-coast investments in Terengganu and Sarawak leverage PETRONAS upstream discoveries to anchor new plastics clusters aligned with petrochemical derivative diversification. Logistics upgrades, including sections of the East Coast Rail Link set to open in 2027, promise to shorten resin transit from Johor to northeastern states, reducing delivered costs for rural packaging plants. Kedah and Melaka absorb spillover from Penang’s semiconductor parks, with land banks geared toward medium-volume OEMs producing EV battery components and automotive connectors. Malaysia’s port network, ASEAN tariff privileges, and bilingual workforce together give processors fast-cycle access to clients across Indonesia, Thailand, and the Philippines. Halal packaging certification serves as a market-entry passport into GCC economies, prompting Selangor-based film plants to dedicate lines to Sharia-compliant resins.

Value Chain Analysis

Malaysia's plastics value chain is anchored upstream by integrated petrochemical feedstock from PETRONAS-linked complexes and local resin production led by PETRONAS Chemicals Group and LOTTE Chemical Titan, with major downstream conversion concentrated in Selangor (scale converters and FMCG packaging) and Penang (precision molding for electronics). Imports complement domestic supply for specialty monomers, additives, and engineering polymers, while export-oriented converters route finished films, molded parts, and compounded materials through hubs such as Port Klang and Johor ports to serve ASEAN and global customers.

Key value-chain pinch points increasingly sit between resin supply, compounding, and high-spec conversion. In 2026, industry and media reports highlighted tightened resin availability tied to maintenance-related disruptions at major producers and broader supply constraints connected to West Asia-related shocks to refinery and aromatics output, raising working-capital pressure for processors reliant on spot purchases. Downstream players are responding with closer supplier tie-ups, higher recycled-pellet integration where specifications allow, and energy and automation upgrades across plants to stabilize conversion yields and reduce unit costs.

Competitive Landscape

The Malaysian plastics market is moderately fragmented. Scientex Berhad commands leading flexible-film capacity integrated from blown-film extrusion to lamination, while LOTTE Chemical Titan leverages upstream cracker connectivity for cost leadership in PE and PP. Competitive strategy emphasizes vertical integration and sustainability positioning. Multinationals like ExxonMobil and Dow collaborate with local recyclers to lock in PCR supply partnerships, thus raising the barrier for traditional converters that lack traceability. Overall, firms that marry feedstock security with low-carbon credentials and process automation are best positioned to outpace peers through 2030.

Malaysia Plastics Industry Leaders

BP Plastics Holding Bhd

LOTTE CHEMICAL TITAN HOLDING BERHAD.

Polyplastics Co., Ltd.

Scientex Berhad

SLP RESOURCES BERHAD

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led circularity is opening measurable whitespace across collection, sorting, and recycled-resin upgrading needed by brand owners and exporters. The National Circular Economy Council approved in principle an EPR policy framework in 2025, with a voluntary phase beginning in 2026 and mandatory status by 2030, and from January 1, 2026, shopping complexes must provide recycling facilities or drive-through recycling centers as part of local-authority premises licensing. These policy steps strengthen demand for traceable PCR resins, food-grade and high-clarity recycled pellets, and converter capabilities such as mono-material redesign, de-inking, odor removal, and quality-assurance systems that support export documentation.

Feedstock resilience and higher-value materials represent another opportunity set as Malaysia balances its role as a petrochemical hub with export manufacturing requirements. PETRONAS's move in May 2026 to acquire Saudi Aramco's stake in PRefChem and assume full ownership of the Pengerang-based integrated refining and petrochemical complex underscores ongoing consolidation and operational flexibility at a critical national feedstock node. At the same time, electronics and medical supply chains are pulling more demand for engineering plastics, precision molding, and compounds (including recycled-content grades), creating room for local compounders, tooling ecosystems, and specialty processors located near Penang, Selangor, and Johor clusters.

Recent Industry Developments

- July 2026: Malaysia's National Economic Action Council (NEAC) reviewed proposals submitted by the Malaysian Plastics Manufacturers Association (MPMA) as the industry flagged cost and competitiveness pressure amid global supply disruption. The engagement elevated raw-material availability, logistics, and structural cost issues into the national policy agenda, supporting industry push for measures that stabilize resin supply and improve downstream competitiveness.

- July 2025: Malaysia enacted a nationwide ban on plastic-scrap imports, aligning domestic rules with Basel Convention-related controls on plastic scrap movements. The change reduced access to low-cost imported scrap and shifted the recycling value chain toward domestic collection, sorting, and higher-quality processing capacity.

- June 2024: Malaysia continued implementation of the Malaysia Plastics Sustainability Roadmap 2021-2030, which frames national actions on recycling rates, design for recyclability, and circular-economy infrastructure. The roadmap has supported converter and recycler investments in traceability, upgraded washing and sorting, and recycled-content formulations that meet both domestic sustainability programs and export customer requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market size covers plastics produced and consumed in Malaysia, measured as revenue from polymer resins and plastic materials supplied into local converting and end use demand, with imports and exports reflected in the balance.

Scope exclusions: It does not count recycled plastic scrap trading as a standalone market, and it excludes finished non-plastic goods where plastic is only a minor component.

Segmentation Overview

- By Type

- Traditional Plastics

- Engineering Plastics

- Bioplastics

- By Technology

- Blow Molding

- Extrusion

- Injection Molding

- Other Technologies

- By Application

- Packaging

- Electrical and Electronics

- Building and Construction

- Automotive and Transportation

- Houseware

- Furniture and Bedding

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the factual backbone for the Malaysia plastics model, especially around resin supply, downstream manufacturing, and trade flows. The work typically starts with public statistics such as Malaysia DOSM manufacturing data, UN Comtrade and Malaysia customs trade tables for polymers and plastic products, and Bank Negara Malaysia macro indicators that help explain demand cycles.

To keep the market tied to industry realities, we also review sources such as Malaysian Plastics Manufacturers Association publications, energy and feedstock commentary from official portals, and peer reviewed journals that track polymer demand and recycling policy impacts. Company annual reports, investor presentations, and credible press coverage are then used to confirm capacity moves, plant utilization commentary, and product mix shifts. In a few cases, paid subscriptions are used for company financials and intelligence, shipment level trade tracking, and patent databases to support trend validation. The sources listed here are illustrative only, and many other references are consulted to collect, cross check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions that cannot be fully read from public documents, such as near-term resin price pass through, importer behavior, and how demand is shifting across packaging, construction, and electrical and electronics. Interviews are conducted with a mix of resin suppliers, converters, distributors, and large end users across Malaysia, and we then mirror-check key inputs with regional trade participants where cross-border flows influence pricing and availability. What we hear is used to refine conversion ratios, typical contract terms, and timing of capacity ramps, before final numbers are signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 58% | Functional/Unit leaders: 41% | |

| Smaller Players: 14% | Managers: 45% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where national demand is reconstructed from resin and plastic material supply patterns, trade balances, and end use pull from manufacturing activity in Malaysia. The top-down side leans on production and trade data to map the available polymer pool, then allocates it across key application demand centers based on conversion intensity and observed shifts in sector output.

To keep totals realistic, the results are corroborated with selective bottom-up checks such as sampled price per ton ranges by polymer family, converter throughput discussions, and importer and distributor channel checks. These checks are used to adjust totals when gaps show up. Key inputs that influence the model include polymer and naphtha linked price direction, import penetration for major resins, construction and infrastructure activity, electrical and electronics export momentum, and packaging consumption indicators tied to domestic spending and food and beverage output.

For forecasting, scenario analysis is used because the market is sensitive to feedstock prices, export demand, and policy pressure on single-use plastics, and these drivers do not move in a straight line every year. Assumptions are carried forward only after they are stress tested with interview feedback. Where data is missing for a sub area, proxy indicators like trade volume trends and manufacturing PMI direction are applied with conservative bounds.

Data Validation & Update Cycle

Outputs are cross checked through triangulation across supply side signals, demand indicators, and trade movement, then reviewed for year over year jumps that do not match known events. When a variance looks abnormal, the underlying drivers are reworked, and where needed, follow up calls are made to confirm whether pricing, utilization, or mix changes explain the swing.

Before publication, the full model and assumptions go through a multi step analyst review so that scope, units, and currency handling stay consistent across the time series. The report is refreshed annually, and interim updates are made when material changes occur, such as a major capacity start up, policy change, or sharp feedstock shift. Right before delivery, a final pass is completed so clients receive the most current view based on the latest available public releases and field notes.

Mordor Intelligence's Malaysia Plastics Market Sizing Compared With Other Published Estimates

It is normal to see different market size values for Malaysia plastics, even when the topic name looks the same, because the scope boundary and the measurement point in the value chain can shift. Some studies track resin only, some include conversion services, and some mix value and volume without clearly stating the pricing basis.

By tracking resin supply and trade balances and then refreshing price per ton assumptions with converter feedback, Mordor Intelligence keeps the Malaysia plastics total tied to a consistent value definition before the forecast is extended using application level demand signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.04 B (2025) | |

| Global Consultancy A | USD 3.73 B (2024) | Uses an earlier base year and a narrower timing window, and the pricing basis is not clearly aligned to the same average resin and converted product mix used in the baseline. |

| Industry Publisher B | USD 2.30 B (2025) | Tracks plastic resin revenue only, which leaves out downstream conversion value and reduces totals in a country where converting activity is a large part of the plastics economy. |

The spread across the table mainly comes from what each source counts, whether it is resins only or the broader plastics value flowing into converting and end use demand, and how the base year pricing is handled. When scope is held steady and key assumptions are rechecked against trade, production, and interview signals, the final estimate becomes easier to replicate and easier to update as new industry data is released.

Key Questions Answered in the Report

What is the current value of the Malaysia plastics market?

The Malaysia plastics market size stands at USD 4.19 billion in 2026.

How fast is the market expected to grow through 2031?

The market is forecast to expand at a 3.86% CAGR, reaching USD 5.07 billion by 2031.

Which application segment is growing the fastest?

Electrical and electronics plastics demand is projected to rise at a 3.96% CAGR, driven by semiconductor packaging expansions.

Why are bioplastics gaining attention in Malaysia?

Bioplastics benefit from the zero single-use plastics roadmap and PETRONAS's upcoming biorefinery, enabling local supply of bio-based resins for export packaging.

How are companies addressing environmental regulations?

Leading converters invest in advanced recycling, compostable materials, and automation to meet EPR requirements and cut operational emissions.

Where are Malaysia's main plastics manufacturing hubs?

Johor provides feedstock from Pengerang, Selangor hosts large-scale processors near Port Klang, and Penang specializes in precision molding for electronics.

Page last updated on: