Malaysia Box Truck Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

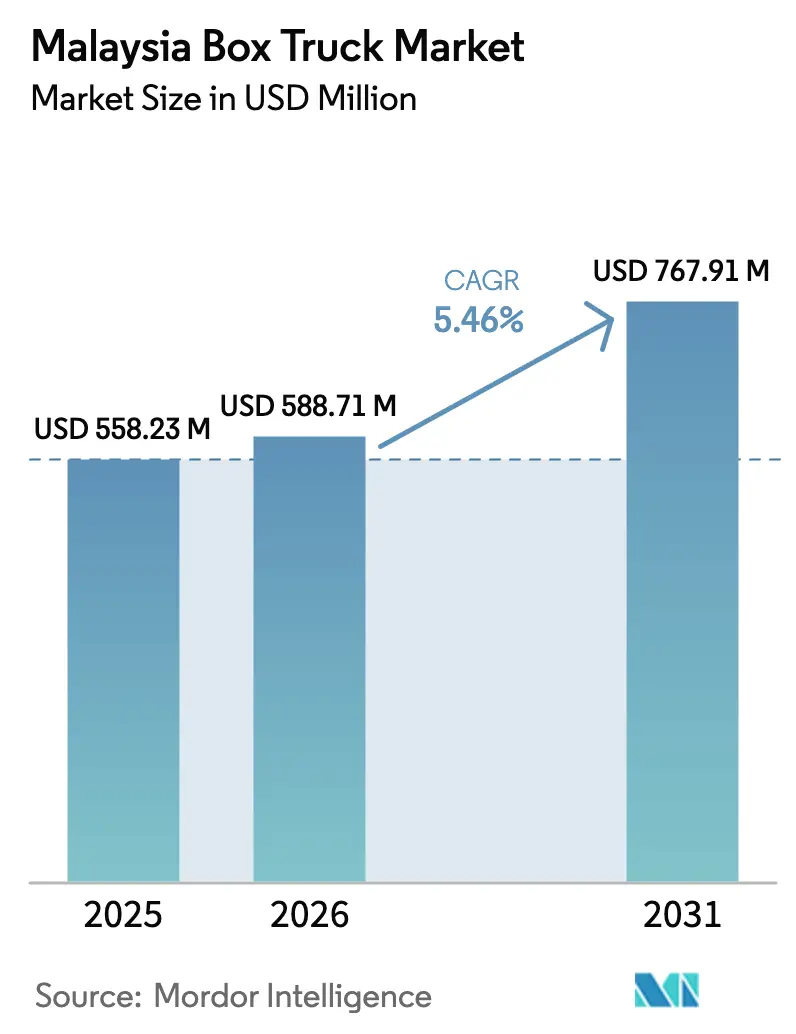

| Base Year Market Size (2025) | USD 558.23 Million |

| Market Size (2026) | USD 588.71 Million |

| Market Size (2031) | USD 767.91 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Box Truck Market Analysis by Mordor Intelligence

Malaysia box truck market size in 2026 is estimated at USD 588.71 million, growing from 2025 value of USD 558.23 million with 2031 projections showing USD 767.91 million, growing at 5.46% CAGR over 2026-2031. Resilient demand stems from e-commerce growth, infrastructure upgrades, and stricter emissions regulations, which collectively offset near-term headwinds from the removal of diesel subsidies, higher financing costs, and foreign exchange volatility. Light-duty vehicles designed for last-mile delivery are driving new registrations, while refrigerated bodies are gaining traction as cold-chain standards become increasingly stringent. Fleet operators are also refreshing assets to meet Euro VI timelines and to hedge against volatile diesel prices by piloting electric variants. At the same time, the market benefits from federal grants that subsidize automation and telematics, allowing logistics firms to enhance route planning and improve fuel efficiency.

Key Report Takeaways

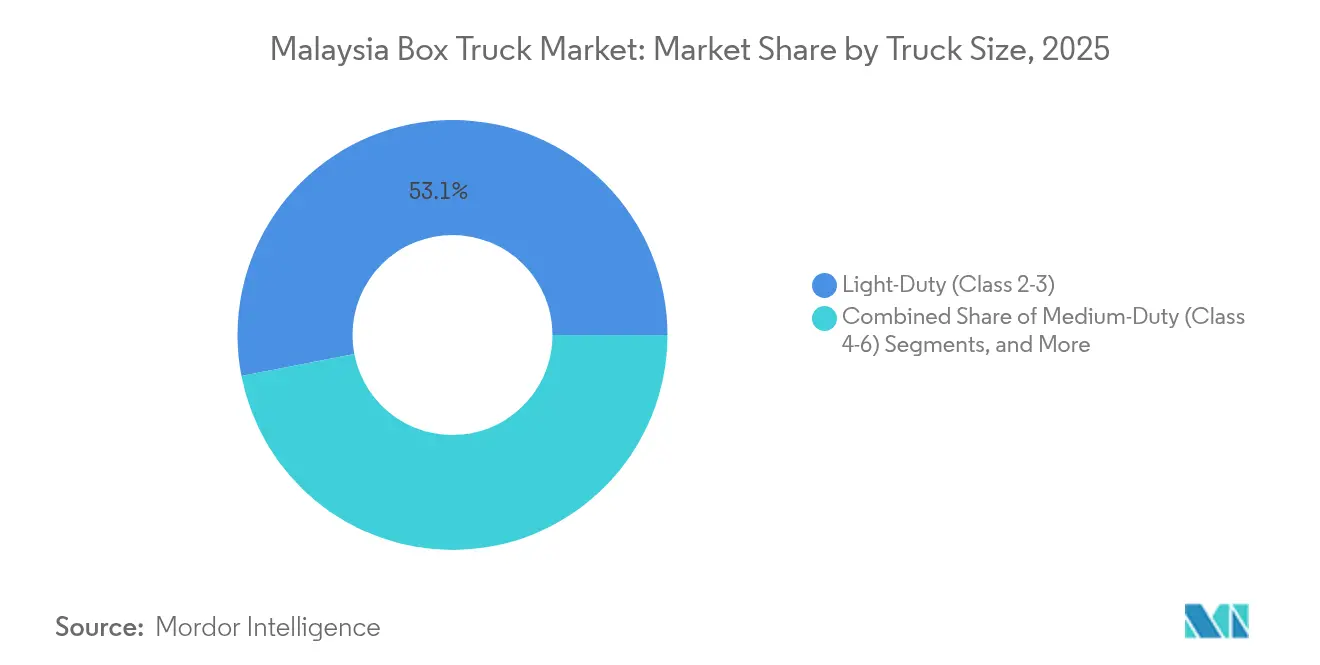

- By truck size, light-duty units captured 53.05% of Malaysia's box truck market share in 2025 and posted the fastest growth, at a 5.78% CAGR, through 2031.

- By fuel type, diesel accounted for 85.62% of Malaysia's box truck market share in 2025, while electric variants led expansion at a 6.04% CAGR through 2031.

- By body type, dry freight boxes held a 58.55% of Malaysia's box truck market share in 2025, and refrigerated boxes are expected to advance at a 5.59% CAGR through 2031.

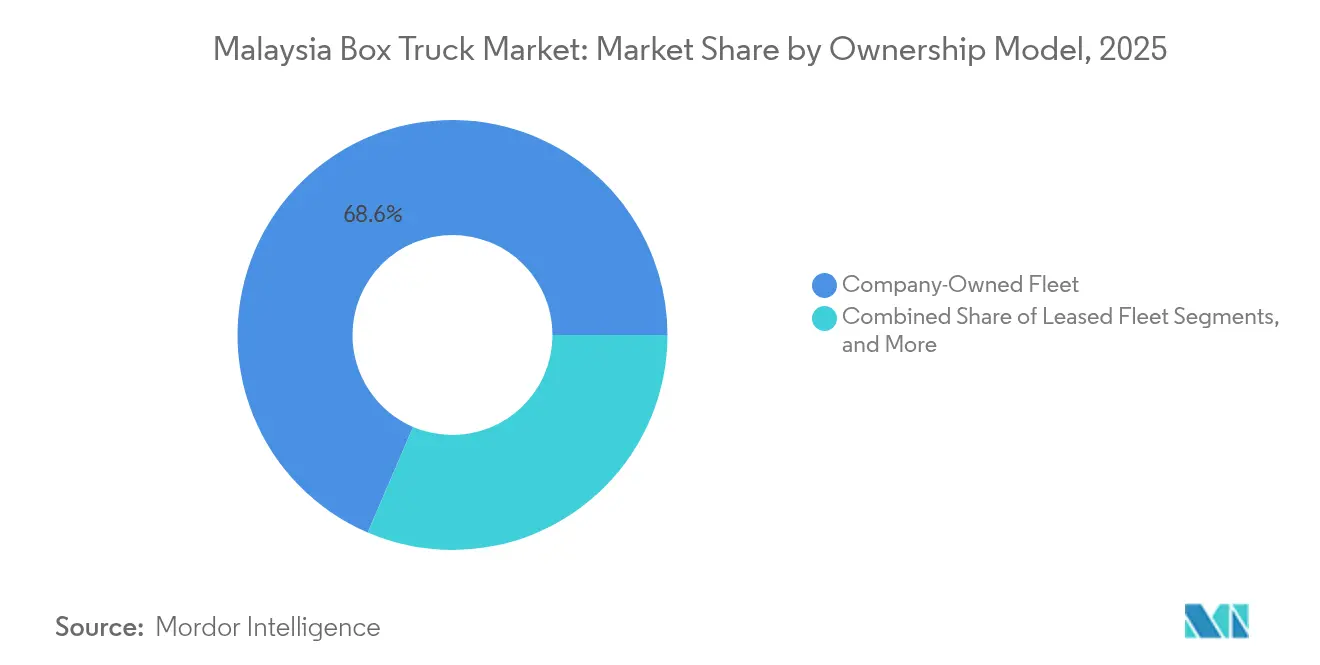

- By ownership model, company fleets controlled 68.55% of Malaysia's box truck market share in 2025, whereas rental fleets are expected to show the highest 5.31% CAGR through 2031.

- By end user, transportation companies led with a 37.85% of Malaysia's box truck market share in 2025, while courier & parcel services drove growth at a 5.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Box Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-Mile Delivery Surge | +1.2% | Global, concentrated in Klang Valley, Penang, Johor | Short term (≤ 2 years) |

| Road Infra Upgrades | +0.9% | National, with early gains in Peninsular Malaysia, Sabah, Sarawak | Medium term (2-4 years) |

| Cold-Chain Expansion | +0.8% | Global, spill-over to regional hubs | Medium term (2-4 years) |

| Fleet Renewal via Euro VI | +0.7% | National compliance requirement | Short term (≤ 2 years) |

| Halal Logistics Drive Box Trucks | +0.4% | Global, with concentration in Muslim-majority regions | Long term (≥ 4 years) |

| Weight-Efficient Designs Favored | +0.3% | National, phased implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom and Last-Mile Delivery Surge

The Malaysia box truck market continues to benefit from a sharp rise in online retail volumes that require frequent, small-parcel dispatches. Investments such as DHL’s RM300 million Kuala Lumpur Gateway facility and the introduction of automated sortation hubs around Klang Valley confirm sustained parcel throughput growth [1]“Kuala Lumpur Gateway Expansion Press Release,”, DHL Express Malaysia, dhl.com. Urban consolidation centers favor light-duty box trucks able to navigate narrow streets and execute multiple daily stops with minimal dwell time. Telematics platforms, including 5G-enabled solutions offered by Yes Fleet, now deliver real-time diagnostics and route optimization that lower monthly fuel use by more than 4,000 liters for high-utilization vehicles. Cross-border parcels flowing under the ASEAN Customs Transit System’s 24-hour clearance window boost demand for sealed, customs-compliant bodies. Collectively, these shifts embed e-commerce logistics as a structural, not cyclical, catalyst for additional vehicle purchases and fleet digitalization.

Government-Led Road Infrastructure Upgrades

Ongoing highway widening and new corridor projects shorten intra-Malaysia transit times, reduce vehicle wear and tear, and spur incremental freight demand. Key initiatives include the Johor–Singapore Causeway overhaul, KL–Karak capacity expansion, and the Pan Borneo Highway rollout, each of which involves adding lanes, reinforcing pavements, and introducing weigh-in-motion enforcement [2]“Highway Development Plan 2025,”, Malaysian Public Works Department, jkr.gov.my. Improved road quality reduces maintenance downtimes, which raises asset utilization and encourages medium-duty fleet additions that can now complete longer hauls in a single shift. Real-time traffic platforms linked to smart sensors also enable carriers to trim fuel costs by rerouting around congestion.

Cold-Chain Expansion for Perishables and Pharma

Malaysia’s ambition to serve as a regional pharmaceutical and halal-food logistics hub is accelerating demand for temperature-controlled transport. Refrigerated box trucks compliant with Good Distribution Practice and Medical Device Authority standards now form a critical link in supply chains that move vaccines, biologics, and fresh produce [3]“Good Distribution Practice Guidelines,”, Ministry of Health Malaysia, pharmacy.gov.my. DHL and DKSH have expanded their pharma-grade storage, which requires precise last-mile temperature integrity, while local agribusinesses, such as FGV, invest in multi-zone reefers for fresh produce distribution. IoT sensors that monitor temperature, humidity, and shock are becoming a standard fitment, and redundant power units mitigate spoilage risk during grid or vehicle outages. Consequently, refrigerated bodies show the strongest incremental unit growth within the Malaysia box truck market.

Corporate Fleet Renewal Driven by Euro VI Standards

Stricter emission norms are shortening replacement cycles as operators retire Euro II and Euro III assets. The Road Transport Department enforces enhanced smoke-opacity checks, and non-compliant vehicles face immediate grounding[4]“Vehicle Emission Standards Circular,”, Road Transport Department Malaysia, jpj.gov.my. Isuzu, Hino, and Mitsubishi Fuso have launched Euro IV-ready chassis ahead of the Euro VI transition. Fleet owners who adopt compliant trucks benefit from lower road tax brackets and improved fuel economy, which partially offset the higher capital outlays. This regulatory push is therefore a demand accelerator for modern, cleaner vehicles across all weight classes in Malaysia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV Truck Costs | -0.8% | National, with urban concentration | Short term (≤ 2 years) |

| Diesel Price Volatility | -0.6% | National impact on diesel fleet operations | Short term (≤ 2 years) |

| Limited EV Charging for Industry | -0.5% | National, with rural gaps more pronounced | Medium term (2-4 years) |

| Axle Rules Cut Payloads | -0.3% | National enforcement with highway focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Electric Box Trucks

Battery-electric models carry price tags 70% higher than comparable diesel units, even after import-duty exemptions, which constrains adoption among small carriers. Finance houses also discount residual values due to technological uncertainty, pushing monthly installments higher than those for diesel alternatives. Depot charging requires electrical upgrades that cost up to RM100,000 per site. Meanwhile, the charging network density outside major corridors remains sparse, with fewer than 1,000 operational points nationwide. Although the total cost of ownership becomes favorable after five years under high mileage, cash-flow constraints deter many operators from early transition, tempering the short-term lift that electrification could otherwise provide to the market.

Volatile Diesel Prices Compressing Freight Margins

The June 2024 elimination of blanket diesel subsidies resulted in a 56% overnight increase in pump prices, eroding operating margins for carriers locked into annual freight contracts. While some shippers accepted spot-rate surcharges, smaller hauliers lacked the bargaining power to do so and deferred truck purchases. The planned RON95 subsidy rationalization in mid-2025 reinforces investor caution across the Malaysia box truck industry. Operators are countering cost volatility via telematics-driven driver training, aerodynamic retrofits, and route optimization, but these measures offset only a portion of fuel inflation. Persistent uncertainty, therefore, weighs on near-term replacement intentions, while simultaneously nudging fleet managers toward lighter chassis and alternative fuels, thereby reshaping long-run demand patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Truck Size/Class: Light-Duty Vehicles Anchor Urban Growth

Light-duty vehicles hold 53.05% of Malaysia's box truck market share in 2025, representing a 5.78% CAGR outlook through 2031. These compact trucks maneuver through congested lanes, reach residential doorsteps, and minimize driver license requirements, making them the default choice of courier and retail distributors as urban warehousing adopts hub-and-spoke designs. As trip frequency rises, demand for nimble chassis with walk-through cabs and tail-lift options also increases.

Medium-duty trucks service inter-city cold-chain and construction supply runs that require greater payload but not the full capacity of heavy rigs. Meanwhile, heavy-duty classes cater to high-volume corridors linking Port Klang, Penang Port, and Johor Port, but they face payload caps under stricter axle-weight enforcement. Technology features such as advanced driver assistance systems, collision avoidance, and real-time load monitoring are spreading from heavy to lighter segments, creating cross-segment convergence that lifts average selling prices and deepens aftermarket demand within the Malaysia box truck market.

By Fuel Type: Diesel Dominates as Electric Scales Gradually

Diesel engines powered 85.62% of Malaysia's box truck market share in 2025. The segment benefits from established refueling infrastructure, attractive torque curves, and robust residual values. Nonetheless, subsidy removal magnifies operating-cost exposure and accelerates interest in efficiency upgrades, such as start-stop systems, low-rolling-resistance tires, and high-pressure fuel injection.

Electric box trucks, supported by duty exemptions and a 38% national EV penetration target by 2040, are projected to grow at the fastest rate, with a 6.04% CAGR through 2031. Fleet pilots led by swift-parcel and food-delivery operators demonstrate that depot-return schedules match battery ranges of 200-300 kilometers. Hybrid and CNG/LPG platforms fill transitional niches but lack the policy impetus offered to zero-emission drivetrains. Long-term, declining battery costs and federal tax credits are forecast to lift the electric share above 10.00% by 2031, thereby diversifying energy exposure for the Malaysian box truck market.

By Body Type: Dry Freight Prevails, Refrigerated Bodies Outpace

Dry freight boxes accounted for 58.55% of Malaysia's box truck market share in 2025, serving as the primary mode of transportation for general cargo, e-commerce parcels, and light construction materials. Their standardized dimensions ease dock integration and maximize cubic utilization, traits critical in high-turn warehouses. The Malaysia box truck market share of refrigerated boxes stands lower today, but its 5.59% CAGR underscores how temperature accountability reshapes logistics requirements.

Pharmaceutical companies, fresh produce exporters, and halal food distributors specify multi-zone reefers fitted with IoT sensors that transmit temperature and humidity data to cloud-based dashboards. Curtain-side variants remain popular among building materials suppliers for the side loading of irregular pallets, while tail-lift boxes gain ground for last-mile furniture and appliance delivery. Demand for specialized interiors, such as antimicrobial linings and aluminum flooring, further segments the market and boosts value-added fabrication activity within local body-builder clusters.

By Ownership Model: Capital-Light Demand Lifts Rentals

Company-owned vehicles still dominate at 68.55% of Malaysia's box truck market share in 2025 because large 3PLs and retailers place a premium on in-house control, brand graphics, and predictable total cost of ownership. They also leverage in-house workshops that minimize downtime and stretch asset life. Yet the rental fleet’s 5.31% CAGR through 2031 signals a shift toward capital agility, particularly among SMEs that confront margin compression from fuel volatility and interest-rate hikes.

Full-service leasing packages bundle insurance, maintenance, and telematics into a single monthly fee, freeing up cash for core business expansion. Subscription models introduced by major conglomerates allow term flexibility as short as three months, appealing to businesses with seasonal peaks such as electronics launches and harvest periods. Electrification accelerates this pivot because rental providers absorb battery risk and invest in shared charging depots. Consequently, the rental channel adds resilience to overall vehicle demand and broadens participation in the Malaysia box truck market.

By End User: Transportation Companies Lead, Couriers Accelerate

Transportation companies accounted for 37.85% of Malaysia's box truck market share in 2025, leveraging economies of scale to serve a diverse range of sectors, including FMCG and industrial inputs. Their fleet renewal cycles track regulatory mandates and client service-level agreements, undergirding baseline demand for newer trucks with advanced safety tech.

Courier and parcel operators, propelled by double-digit e-commerce parcel volumes, register a 5.71% CAGR to 2031. They specify tight wheelbases, sliding doors, and telematics that integrate with customer apps. Retailers and wholesalers continue to right-size their private fleets, favoring medium-duty units equipped with tail lifts for store-direct deliveries. Construction companies increase orders when infrastructure capital expenditures rise, while public agencies maintain modest replacement of utility and emergency support vehicles. The Malaysia box truck market thus mirrors the structural interplay between consumer behavior, manufacturing shifts, and public-sector budgets.

Geography Analysis

Peninsular Malaysia contributes a significant share of current revenue due to its dense highway grid, proximity to major seaports, and cross-border trade with Singapore. The Klang Valley alone houses fulfillment centers that dispatch more than 1 million parcels daily, underpinning continuous demand for light-duty trucks with rapid-loading configurations. Johor’s Iskandar region benefits from causeway upgrades that cut clearance times, drawing electronics assemblers that depend on time-critical trucking links. Penang’s industrial cluster similarly sustains medium-duty refrigerated flows for medical devices and semiconductor supply chains.

East Malaysia, historically hindered by fragmented road networks, now represents the fastest-growing regional node within the Malaysian box truck market. The Pan Borneo Highway reduces Kuching-Kota Kinabalu transit by six hours, enabling same-day freight that previously required overnight stops. Agribusiness exporters in Sabah deploy heavy-duty rigs outfitted with lighter chassis to comply with stricter axle weight rules while maximizing palm oil and seafood payloads. Sarawak’s resource projects, encompassing timber and gas, require specialized body orders that can withstand rugged terrain and high humidity.

Cross-border dynamics extend market reach beyond national boundaries. The ASEAN Customs Transit System enables 24-hour through-runs at Bukit Kayu Hitam and Johor Bahru, stimulating demand for trucks equipped with electronic cargo sealing and satellite tracking that meet the Singapore Land Transport Authority's requirements. Proposed Malaysia-Singapore Special Economic Zone incentives could increase point-to-point vehicle movements by up to 15% by 2030, potentially driving sustained chassis demand for operators serving integrated supply chains. Collectively, regional investments ensure that the Malaysia box truck market delivers balanced growth across mature and emerging corridors.

Competitive Landscape

Japanese OEMs maintain their primacy through localized assembly, extensive dealer networks, and proven durability in tropical climates. Isuzu’s ten-year reign reflects a consistent lead-time advantage for chassis, spares, and after-sales support. Hino and Mitsubishi Fuso follow with complementary product ladders that span light to heavy segments. The trio leverages Euro-IV readiness to secure fleet conversions ahead of looming Euro-VI cut-offs, thereby reinforcing brand loyalty among institutional buyers.

Strategic collaborations intensify. DRB-HICOM’s end-to-end ecosystem covers CKD assembly, parts distribution, and fleet management services, delivering bundled offers that lower lifecycle cost for fleet operators. Global forwarders, such as GEODIS, procure Mercedes-Benz Actros tractors equipped with geofencing and driver-fatigue sensors, signaling technology-led differentiation. Domestic bodybuilders step up by integrating composite panels and refrigerated liners that meet GDP and halal standards, capturing margins beyond the bare chassis value and anchoring local supply chains for the Malaysian box truck market.

Electric entrants spur fresh competition. Chinese OEMs JAC and BAIC have secured CKD agreements that circumvent import duties and commit to localizing battery assembly, a prerequisite for tender participation by government entities aiming for zero-emission fleets. Meanwhile, telematics vendors partner with insurers to launch pay-how-you-drive premiums that reward safer behavior, carving out ancillary revenue streams. Altogether, the competitive field balances entrenched scale advantages with innovation-driven disruption, maintaining moderate rivalry that favors customers through wider choice and faster technology diffusion.

Malaysia Box Truck Industry Leaders

Isuzu Motors Limited

Hino Motors Sales (Malaysia) Sdn Bhd

Mitsubishi Fuso Truck and Bus Corporation

Tata Motors Limited

Scania (Malaysia) Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: At the Hino Total Support Customer Centre (HTSCC) in Sendayan, Hino Motors Sales (Malaysia) Sdn. Bhd. (HMSM) rolled out its latest Hino 300 Series Euro 5 Light Commercial Vehicles (LCVs). The event spotlighted the debut of two enhanced models: the 4-Wheeler and 6-Wheeler, under the banner “Strong, Smart & Smooth.”

- July 2025: UD Trucks, alongside its exclusive Malaysian distributor, Tan Chong Industrial Equipment Sdn Bhd (TCIE), unveiled the New Kuzer SKE 155. This light-duty truck is designed to meet the growing demands of businesses across Southeast Asia.

Malaysia Box Truck Market Report Scope

The Malaysia Box Truck Market Report is Segmented by Truck Size/Class (Light-Duty Class 2-3, Medium-Duty Class 4-6, and Heavy-Duty Class 7-8), Fuel Type (Diesel, Gasoline, Electric, Hybrid, and CNG/LPG), Body Type (Dry Freight Box, Refrigerated Box, Curtain Side Box, and Tail-Lift Box), Ownership Model (Company-Owned Fleet, Leased Fleet, and Rental Fleet), End User (Transportation Companies, Retailers and Wholesalers, Courier and Parcel Services, and Construction Firms, Government Agencies). The Market Forecasts are Provided in Terms of Value (USD).

| Light-Duty (Class 2-3) |

| Medium-Duty (Class 4-6) |

| Heavy-Duty (Class 7-8) |

| Diesel |

| Gasoline |

| Electric |

| Hybrid |

| CNG/LPG |

| Dry Freight Box |

| Refrigerated Box |

| Curtain Side Box |

| Tail-Lift Box |

| Company-Owned Fleet |

| Leased Fleet |

| Rental Fleet |

| Transportation Companies |

| Retailers and Wholesalers |

| Courier and Parcel Services |

| Construction Firms |

| Government Agencies |

| By Truck Size/Class | Light-Duty (Class 2-3) |

| Medium-Duty (Class 4-6) | |

| Heavy-Duty (Class 7-8) | |

| By Fuel Type | Diesel |

| Gasoline | |

| Electric | |

| Hybrid | |

| CNG/LPG | |

| By Body Type | Dry Freight Box |

| Refrigerated Box | |

| Curtain Side Box | |

| Tail-Lift Box | |

| By Ownership Model | Company-Owned Fleet |

| Leased Fleet | |

| Rental Fleet | |

| By End User | Transportation Companies |

| Retailers and Wholesalers | |

| Courier and Parcel Services | |

| Construction Firms | |

| Government Agencies |

Key Questions Answered in the Report

What is the current value of the Malaysia box truck market?

The Malaysia box truck market size stood at USD 588.71 million in 2026 and is projected to reach USD 767.91 million by 2031.

Which truck class is growing fastest in Malaysia?

Light-duty units used for last-mile delivery are expected to post the highest 5.78% CAGR through 2031.

How big is diesel’s share in Malaysian box trucks?

Diesel engines powered 85.62% of units sold in 2025, although that share will gradually decline as electric adoption increases.

How is infrastructure spending affecting demand?

Highway upgrades such as the Pan Borneo project shorten transit times, which lifts truck utilization and supports new vehicle purchases across regions.

Page last updated on: