Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.36 Billion |

| Market Size (2031) | USD 10.78 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

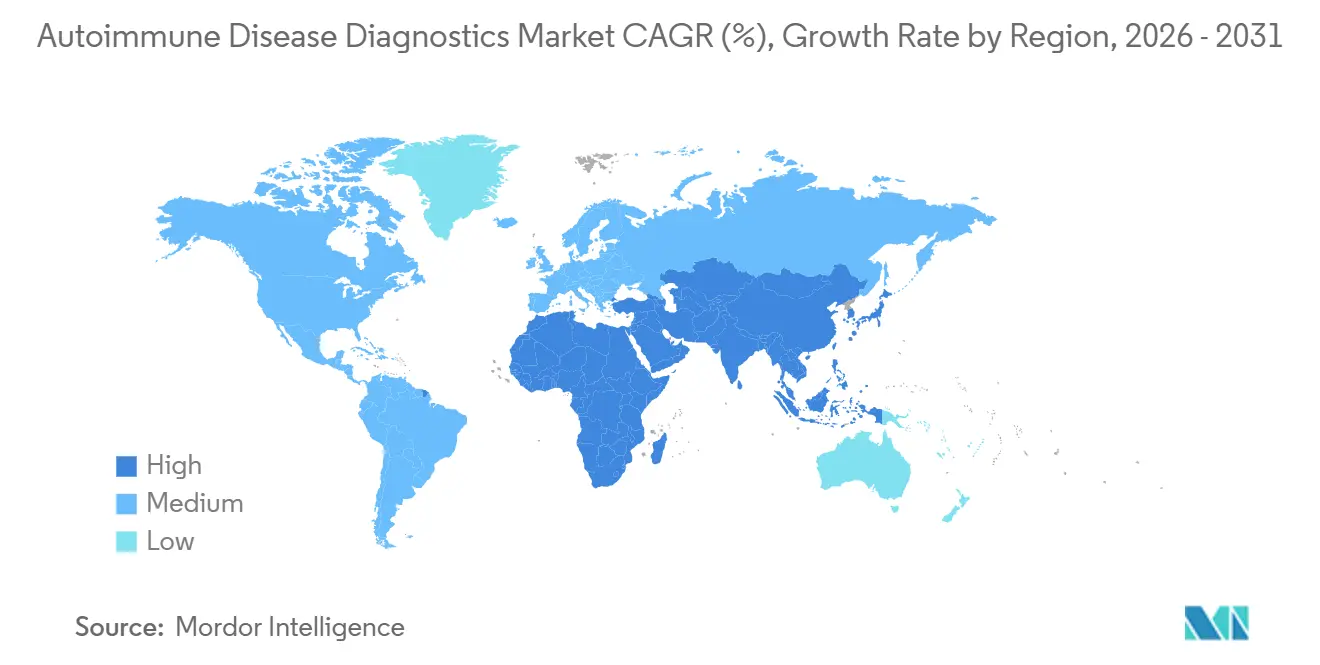

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autoimmune Disease Diagnostics Market Analysis by Mordor Intelligence

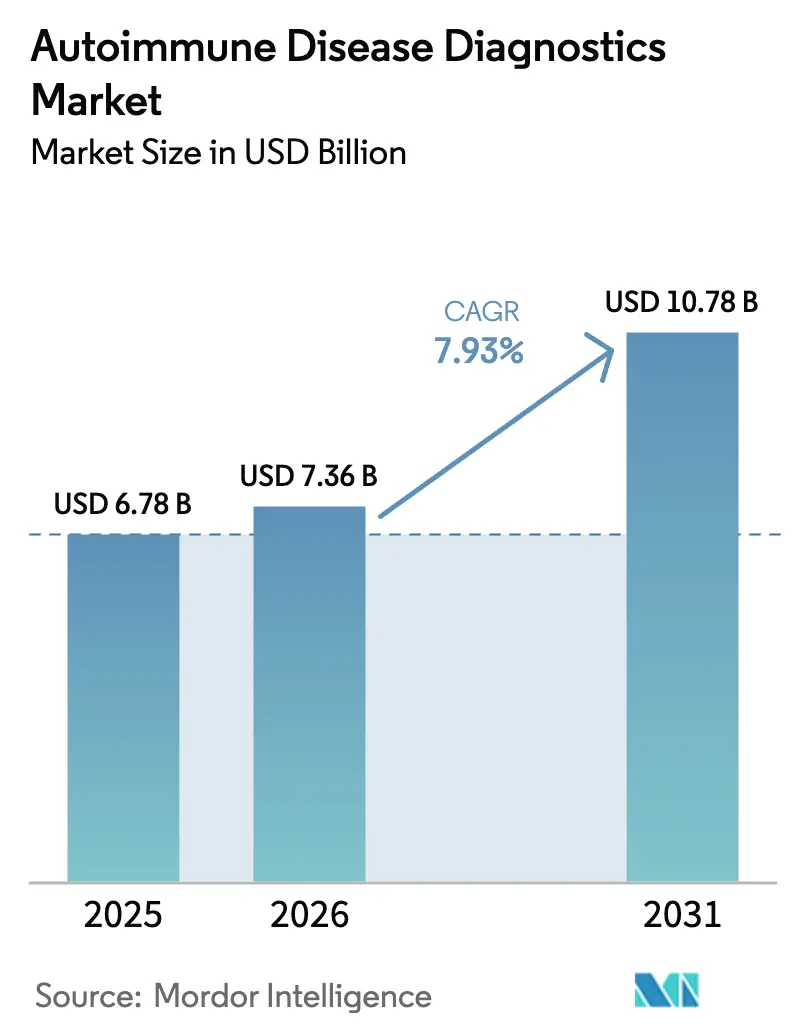

The Autoimmune Disease Diagnostics Market size is expected to grow from USD 6.78 billion in 2025 to USD 7.36 billion in 2026 and is forecast to reach USD 10.78 billion by 2031 at 7.93% CAGR over 2026-2031.

The market’s current expansion is anchored in the widening prevalence of systemic and localized conditions, payer support for multiplex platforms, and AI-enabled pattern recognition that halves turnaround time in reference laboratories. Demand is further reinforced by government-backed screening mandates in the Asia-Pacific region, reimbursement of multi-analyte panels in Japan and South Korea, and Germany’s January 2025 coverage decision for multiplex rheumatoid arthritis testing. Laboratories are therefore shifting their capital budgets toward automated systems that process 20 or more autoantibody targets per sample, replacing single-plex workflows and driving a 30% increase in instrument installations across Europe.

Key Report Takeaways

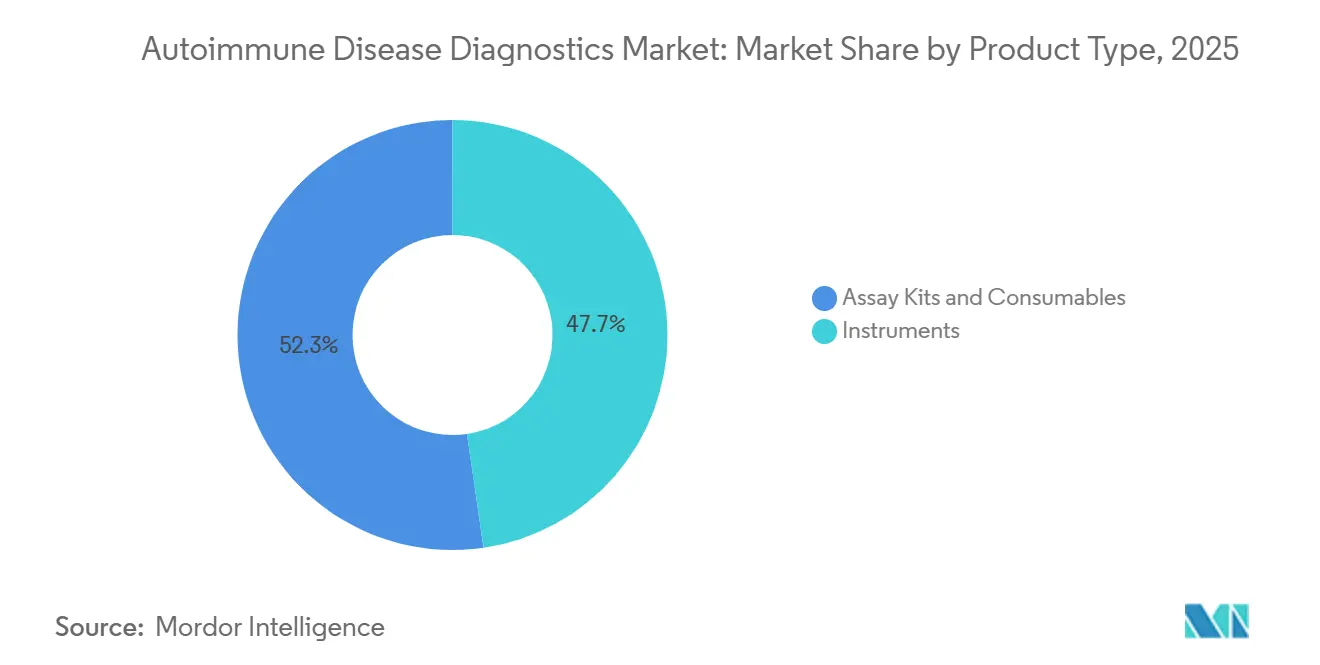

- By product type, assay kits and consumables led with 52.31% revenue share in 2025; instruments are projected to grow at a 10.06% CAGR to 2031.

- By disease type, systemic autoimmune diseases held 66.73% of the autoimmune disease diagnostics market share in 2025, while localized autoimmune diseases are forecast to expand at a 10.72% CAGR through 2031.

- By technology, immunoassays captured 31.48% share of the autoimmune disease diagnostics market size in 2025, and point-of-care testing is advancing at an 8.79% CAGR through 2031.

- By end user, hospitals and clinics accounted for 44.46% of the autoimmune disease diagnostics market in 2025, and clinical laboratories are projected to grow at a 12.69% CAGR through 2031.

- By geography, North America dominated with a 39.26% share in 2025; the Asia-Pacific region is forecast to grow at an 11.53% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autoimmune Disease Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of autoimmune diseases | +1.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Advances in immunoassay & molecular diagnostics | +1.5% | Global, led by North America, Europe, developed APAC | Medium term (2–4 years) |

| Growing awareness & early-detection initiatives | +1.2% | Core APAC, spill-over to Latin America | Medium term (2–4 years) |

| Expansion of automated multiplex testing platforms | +1.4% | North America, Europe, urban APAC hubs | Short term (≤ 2 years) |

| AI-enabled pattern recognition reducing turnaround | +0.9% | North America, Western Europe, select APAC labs | Short term (≤ 2 years) |

| Commutable reference materials speeding approvals | +0.6% | Global, early adoption in EU and Japan | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Autoimmune Diseases

Global incidence continues to climb, with rheumatoid arthritis affecting 18 million adults in 2025, up from 16 million in 2020.[1]World Health Organization, “Global Autoimmune Disease Burden,” who.int Systemic lupus erythematosus prevalence climbed 12% over the same span, mainly among women of childbearing age, while Type 1 diabetes diagnoses in children under 15 increased 3% annually across OECD nations. Environmental factors such as urbanization and dietary change now feature prominently in multi-year cohort studies across Southeast Asia. Payers are expanding coverage for autoantibody panels, citing evidence that early diagnosis can delay biologic therapy by up to 3 years.

Advances in Immunoassay & Molecular Diagnostics

Chemiluminescent immunoassays now achieve greater than 95% sensitivity for anti-CCP antibodies, surpassing the sensitivity of first-generation ELISAs.[2]Clinical Chemistry, “Advances in Chemiluminescent Immunoassays,” clinical-chemistry.org Next-generation sequencing of T-cell receptor repertoires reveals clonal expansions in inflammatory bowel disease up to six months before lesion appearance. Siemens Healthineers’ Atellica IM, cleared in March 2025, merges immunoassay and molecular modules, reducing sample handling and cutting per-test labor costs by 25%.[3]Siemens Healthineers, “Atellica IM Analyzer,” siemens-healthineers.com

Growing Awareness & Early-Detection Initiatives

China mandated thyroid autoantibody screening for all pregnant women in January 2025, resulting in an additional 15 million annual tests. India is piloting adolescent Type 1 diabetes screening across five states, while South Korea’s national checkup program now includes anti-nuclear antibody testing for 25 million adults. These policies convert latent need into laboratory orders, especially where previous out-of-pocket costs suppressed asymptomatic testing.

Expansion of Automated Multiplex Testing Platforms

Bio-Rad’s BioPlex 2200, CE-marked in June 2025, runs 200 samples per shift with limited operator input. Abbott’s upgraded Alinity i, launched September 2025, integrates a 15-autoantibody panel, barcode tracking, and auto-dilution to decrease pre-analytical errors by 40%. Laboratories deploying these systems report a 30% faster turnaround and a 20% reduction in repeat tests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced diagnostics in LMICs | −1.1% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Lack of standardized criteria / false positives | −0.8% | Global, acute in primary care | Medium term (2–4 years) |

| Specialty reagent supply-chain vulnerabilities | −0.6% | Regions dependent on single-source suppliers | Short term (≤ 2 years) |

| Heightened regulatory scrutiny of multiplex assays | −0.7% | North America, Europe, developed APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Diagnostics in LMICs

Multiplex panels priced at USD 150–300 remain out of reach in many low-income markets where per-capita health spending averages USD 50. Public laboratories rely on donated single-plex assays, which extends the median time-to-treatment by 18 months compared to high-income countries. Pooled procurement pilots in East Africa negotiate 40% discounts yet still cover less than 10% of regional need.

Lack of Standardized Criteria / False Positives

ANA positivity in healthy individuals reaches 15%, causing diagnostic ambiguity. Updated 2024 classification criteria attempt to curb false positives, but 35% of ANA results in U.S. primary care yield no definitive diagnosis after one year. Insurers now restrict reimbursement to cases meeting defined clinical thresholds, which risks underdiagnosing atypical presentations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instruments Gain as Labs Consolidate

In 2025, assay kits and consumables captured 52.31% of the autoimmune disease diagnostics market share, benefiting from recurring demand for reagents. Instruments are, however, expanding at a 10.06% CAGR, as reference laboratories replace manual microscopes with fully automated systems that run 500 samples per day. Beckman Coulter’s DxI 9000 Access, launched August 2025, merges chemiluminescent and immunofluorescence workflows on one platform.

Consumables account for a larger share of revenue, with each installed instrument generating USD 200,000–400,000 in yearly reagent sales. Yet payer-driven consolidation favors labs that invest in closed-ecosystem analyzers, locking in multi-year service contracts. Smaller hospital laboratories continue to rely on open-platform reagent purchases, but their 6.5% growth lags the overall autoimmune disease diagnostics market.

By Disease Type: Localized Conditions Outpace Systemic

Systemic diseases held a 66.73% share in 2025, but localized autoimmune disorders are predicted to drive a 10.72% CAGR on the strength of mandated thyroid and Type 1 diabetes screening. China’s policy alone accounts for an additional 15 million thyroid tests per year. The localized segment’s contribution to the autoimmune disease diagnostics market size will therefore accelerate faster than systemic testing, especially as U.S. NIH-funded pilots screen 500,000 high-risk children by 2027.

Inflammatory bowel disease panels that differentiate between Crohn’s disease and ulcerative colitis with 80% accuracy support treatment stratification. Thyroid autoantibody testing volumes in the Asia-Pacific region are rising at a 15% annual rate, cementing localized conditions as the fastest-growing area within the autoimmune disease diagnostics market.

By Technology: Point-of-Care Testing Disrupts Centralized Models

Immunoassays led with a 31.48% share in 2025, anchored in hospital workflows. Point-of-care (POC) devices are, however, expected to advance at a rate of 8.79% through 2031, fueled by the approval of Roche’s Elecsys Anti-CCP POC test in April 2025. India’s June 2025 rollout of thyroid POC testing across 5,000 primary-health centers highlights the appeal of decentralized diagnostics.

Indirect immunofluorescence remains the reference standard but scales poorly. Multiplex assays that simultaneously quantify ≥20 autoantibodies reduce turnaround time by 40% and are gaining market share in the autoimmune disease diagnostics market. Molecular diagnostics represent <5% of commercial testing, hampered by cost and reimbursement gaps.

By End User: Clinical Laboratories Surge on Payer Mandates

Hospitals and clinics commanded a 44.46% share in 2025. Yet clinical laboratories, buoyed by payer preference for high-throughput sites, are poised for a 12.69% CAGR. Quest Diagnostics logged a 25% increase in autoimmune testing volumes in 2025, following the requirement by insurers for prior authorization for hospital testing. Medicare’s July 2025 rule, which reimburses multiplex panels only in CLIA-certified reference labs, accelerates outsourcing.

Academic institutes, though representing just 12% of revenue, often pay premium prices for research-use-only reagents, acting as early adopters of novel markers. Physician-office labs and retail clinics remain underutilized, with less than 10% adoption, due to complexity and regulatory barriers.

Geography Analysis

North America retained a 39.26% share in 2025, with the United States accounting for 85% of regional revenue, primarily due to reimbursement rates exceeding USD 200 per panel. Canada broadened rheumatoid arthritis test coverage, and Mexico initiated lupus screening pilots in high-prevalence states. FDA clearance of 12 autoimmune assays in 2025 underscores sustained innovation, but also highlights longer approval times for multiplex platforms.

Germany’s January 2025 reimbursement for multiplex rheumatoid arthritis panels drove a 30% rise in volumes by mid-year. The United Kingdom boosted capacity by 15% through private-lab contracts, while Spain and Italy piloted POC testing to shorten diagnostic delays. EMA’s 2025 adoption of commutable reference materials streamlines multi-country approvals.

The Asia-Pacific region is the fastest-growing, with an 11.53% CAGR from 2026 to 2031. China’s thyroid screening mandate, India’s adolescent Type 1 diabetes pilot, and Japan’s approval of eight new assays in 2025 collectively expand the size of the autoimmune disease diagnostics market across the region. Australia reduced the POC regulatory timelines from 18 to 10 months to address the needs of remote areas. South Korea added ANA testing for 25 million adults in April 2025.

The Middle East & Africa and South America are smaller but evolving. GCC investments target tertiary centers, while South Africa’s public labs expanded capacity by 10% in 2025. Brazil approved five new assays in 2025, aiming to address the needs of underserved Amazon regions.

Regulatory Landscape

Regulation is tightening around multiplex and software-enabled autoimmune assays as authorities narrow historical flexibilities for laboratory-developed tests (LDTs) and raise documentation expectations for analytical validation. In the United States, the FDA finalized a four-year phaseout of enforcement discretion for LDTs in May 2024, which shifts many high-complexity autoimmune workflows toward medical-device-style controls (including complaint handling and reporting obligations). The phaseout timeline includes Stage 1 beginning May 6, 2025 and Stage 2 beginning May 6, 2026, expanding expectations for areas such as registration and listing, labeling, and investigational use requirements for affected tests.

In Europe, the In Vitro Diagnostic Regulation (IVDR 2017/746) continues to shape market access, particularly for Class C tests that cover a large share of autoimmune serology menus. Under the IVDR transition provisions, Class C IVDs face key 2026 milestones, including application submission by May 2026 and signed Notified Body agreements by September 26, 2026, which becomes a practical gating factor for portfolio continuity. Separately, global method validation expectations are also converging via ICH updates, with ICH Q2(R2) taking effect on June 14, 2024, influencing validation packages used in registration applications and supporting comparability for multi-analyte assays.

Competitive Landscape

The autoimmune disease diagnostics market remains moderately consolidated. Roche, Abbott, Siemens Healthineers, Danaher, and Thermo Fisher together hold a significant share, mainly through reagent annuities tied to closed-system analyzers. Roche’s cobas platform generated USD 1.2 billion in 2025, with 70% of the revenue coming from reagents. Abbott advanced multiplex capability via the Alinity i upgrade, bolstering adoption in Europe.

Specialists such as Exagen and Inova Diagnostics exploit proprietary biomarkers. Exagen’s AVISE Lupus test utilizes cell-bound complement activation products for earlier detection of lupus, differentiating it from generic panels. Bio-Rad secured three 2025 U.S. patents covering AI-based immunofluorescence analysis, signaling a shift toward software differentiation.

Strategic moves center on expanding point-of-care services and incorporating AI modules. Quest Diagnostics and LabCorp broadened esoteric menus, adding rare autoantibodies for academic centers. DiaSorin and Werfen leverage robust regulatory teams to navigate FDA scrutiny, often winning clearances three to six months ahead of smaller rivals. ISO 15189 accreditation trends in Asia-Pacific raise the bar for new entrants lacking quality infrastructure.

Autoimmune Disease Diagnostics Industry Leaders

F. Hoffmann-La Roche AG

Abbott Laboratories

Siemens Healthineers

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multiplexing and automation create near-term whitespace where screening mandates and payer policies are converting latent demand into routine testing volumes, but laboratories need higher throughput and tighter quality control to stay within coverage criteria. China has mandated thyroid autoantibody screening for all pregnant women since January 2025 (an additional 15 million annual tests), and South Korea has added ANA testing for 25 million adults. Germany's January 2025 coverage decision for multiplex rheumatoid arthritis testing has already been associated with higher multiplex volumes. These policy-driven volumes reward platforms that consolidate multiple autoantibodies into a single run (for example, CE-marked multiplex systems and upgraded immunoassay analyzers). They also expand opportunities for regional reference labs to build standardized, high-capacity workflows that meet payer requirements for validated panels.

A second opportunity is deeper immunophenotyping and specialty testing that goes beyond first-line ANA and single-marker confirmation, particularly where new lab capabilities are being installed closer to the patient. In November 2025, Dr. Lal PathLabs launched a specialized complement testing laboratory in India (including assays such as C1q, C5, and Factor H antibody), showing demand for more granular immune-pathway readouts in large, cost-sensitive markets. At the same time, the compliance bar is acting as a market filter: the U.S. transition from LDT discretion to device-like requirements and the IVDR execution timelines, including 2026 milestones for Class C devices, increase the value of manufacturers that can bundle instruments, standardized reagent menus, and quality-system documentation that supports multi-site deployments and reimbursement-aligned testing algorithms.

Recent Industry Developments

- May 2026: Roche announced a definitive merger agreement to acquire PathAI, adding digital pathology and AI capabilities intended to be integrated into its Diagnostics business. The company expects this to support algorithmic interpretation and workflow software alongside immunology testing, as labs shift toward automated, multiplex-heavy menus.

- November 2025: Thermo Fisher Scientific received FDA 510(k) clearance for the EXENT Analyser and Immunoglobulin Isotypes (GAM) Assay, an automated mass spectrometry system to aid in the diagnosis of multiple myeloma. The clearance expands automated, high-complexity protein analysis options within diagnostic laboratories, complementing immunoassay-based portfolios used in immune-mediated disease workups.

- October 2024: Pathkind Diagnostics expanded its autoimmunity testing capabilities by adopting Sebia's Alegria Monotest technology. The deployment reflects continued investment by laboratory networks in specialized immunoassay automation to increase menu breadth and throughput for autoimmune testing services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of in-vitro diagnostics used to identify autoimmune disorders from patient samples, including reagents, assay kits, instruments, and related software that support testing in lab settings.

Scope exclusions: We exclude allergy-related diagnostics and assays used only for drug-therapy titration or treatment monitoring without a diagnostic decision.

Segmentation Overview

- By Product Type

- Instruments

- Assay Kits & Consumables

- By Disease Type

- Systemic Autoimmune Diseases

- Rheumatoid Arthritis

- Systemic Lupus Erythematosus

- Scleroderma

- Vasculitis

- Inflammatory Bowel Disease

- Others

- Localized Autoimmune Diseases

- Type 1 Diabetes

- Autoimmune Thyroid Diseases

- Systemic Autoimmune Diseases

- By Technology

- Immunoassays

- Indirect Immunofluorescence

- Multiplex Assays

- Molecular Diagnostics

- Point-of-Care Testing

- Others

- By End User

- Hospitals & Clinics

- Clinical Laboratories

- Academic & Research Institutes

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a fact base on autoimmune disease burden, testing patterns, and laboratory capacity, then mapping how those signals translate into diagnostic demand. Public sources used include the World Health Organization, the US CDC, the European Centre for Disease Prevention and Control, OECD health statistics, and National Institutes of Health publications, which help anchor prevalence context and health system scale.

We also review peer-reviewed journals on autoantibody testing and assay adoption, along with professional association materials and clinical guideline summaries that indicate when tests like ANA and related panels are typically ordered. Company filings, investor presentations, and reliable press coverage are used to understand product positioning and pricing direction, and then a paid subscription covering company financials and intelligence is used selectively to confirm revenue splits and business exposure. The desk sources listed here are illustrative only, and many other references are used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk model and close gaps that public sources cannot fully answer, especially around test mix, average selling price movement, and the share of testing done in hospitals versus independent and reference labs. We speak with lab managers, hospital diagnostics teams, distributors, and product specialists across the Americas, EMEA, and APAC, then we re-check assumptions when responses show a clear regional pattern (for example, different adoption timing for immunoassay and IFA workflows).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 20% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where diagnosed autoimmune demand and routine testing behavior are reconstructed by region, then converted into market value using realistic test mix and pricing. In practice, the model uses a demand pool built from autoimmune prevalence signals, suspected case workups, and care-access indicators, and then it is adjusted using lab utilization context.

To keep the totals practical, we corroborate the output with selective bottom-up approximations, such as sampled ASP times volume checks for key assays and supplier and channel sense-checks on reagent and kit intensity per test. Market fingerprints that help stabilize the math include ANA and autoantibody panel ordering rates, the split between ELISA, CLIA, and IFA workflows, reagent and kit price movement, instrument placement cycles in clinical labs, and regional differences in reimbursement and guideline-driven testing. When granular data is missing for smaller countries, gaps are handled through proxy ratios from comparable health systems, followed by expert review to avoid over-extending any single assumption.

Forecasts are developed using scenario analysis, where volume growth and pricing are projected separately and then combined, and where primary feedback is used to set realistic adoption slopes for higher-throughput platforms. Final outputs are checked for year-to-year continuity so the growth path fits the underlying disease and testing signals.

Data Validation & Update Cycle

Validation is done through several layers so that unusual outputs are caught early and corrected with evidence. We compare modeled results against independent signals such as diagnostic industry revenue direction, lab testing activity trends, and the expected split between high-volume screening tests and confirmatory panels, then we investigate variances before sign-off.

If an input change creates a sharp step-up or step-down in a region, the assumption is revisited and, when needed, experts are re-contacted to confirm whether the shift is real or model-driven. The report is refreshed annually, with interim updates when material events occur that can affect test volumes or pricing, and before delivery an analyst performs a final pass so clients receive the most current view.

Mordor Intelligence's Global Autoimmune Disease Diagnostics Market Size Versus Other Published Estimates

Published market sizes for autoimmune disease diagnostics can differ even when they appear to cover the same space, because firms often pick different test inclusions, time windows, and pricing assumptions. The table below helps show how those choices can move the number up or down for the same year.

Key gap drivers usually come from what is counted as diagnostics versus broader immunology testing, how instruments and software are treated versus consumables only, and whether confirmatory panels are bundled into wider autoimmune testing pools. Currency timing and the assumed pace of ASP changes also matter, and estimates can drift when models are not re-checked against lab workflow shifts or guideline updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.78 B (2025) | |

| Global Consultancy A | USD 6.07 B (2025) | Uses a narrower value pool that appears more weighted to consumables and core assay revenue, with less explicit treatment of supporting software and instrument value capture across lab settings. |

| Industry Research Group B | USD 5.72 B (2024) | Uses an earlier base year and a broader label around disease diagnosis, which can mix screening and routine lab work with autoimmune-specific panels, and the currency-year basis can shift the stated USD total. |

The table shows a spread that is mainly explained by scope boundaries and base-year choices. In Mordor Intelligence's model, the total reflects in-vitro autoimmune diagnostic reagents, assay kits, instruments, and supporting software, while excluding allergy-related diagnostics and assays used only for therapy titration. With those inclusions and exclusions stated up front, the sizing steps stay easy to follow and can be repeated as new testing and pricing signals emerge.

Key Questions Answered in the Report

What is the projected value of autoimmune disease diagnostics by 2031?

The autoimmune disease diagnostics market size is forecast to reach USD 10.78 billion by 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to expand at an 11.53% CAGR, the highest among all regions.

Which segment is the largest by product type?

Assay kits and consumables led with 52.31% revenue share in 2025, reflecting recurring reagent demand.

How are AI tools impacting laboratory turnaround time?

AI-enabled pattern recognition now classifies ANA patterns with 98% concordance, reducing slide review time to 90 seconds and halving the overall turnaround in reference labs.

What factor is propelling growth in localized autoimmune testing?

Population-wide screening mandates for thyroid and Type 1 diabetes autoantibodies are driving localized testing volumes, especially in China and India.

Page last updated on: