Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.73 Billion |

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

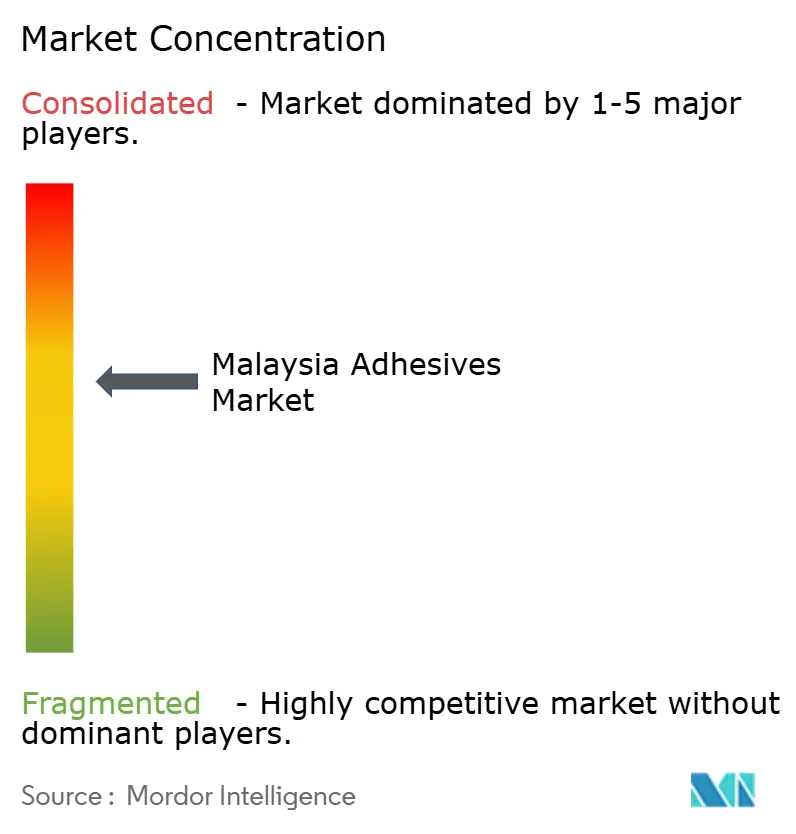

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Adhesives Market Analysis by Mordor Intelligence

The Malaysia Adhesives market size is expected to grow from USD 0.73 billion in 2025 to USD 0.77 billion in 2026 and is forecast to reach USD 1.02 billion by 2031 at 5.88% CAGR over 2026-2031. Rising infrastructure spending, accelerated electric-vehicle (EV) assembly, and stringent low-VOC rules keep demand for advanced bonding technologies on an upward track. The National Construction Policy 2030 channels government tenders toward certified, BIM-specified products, a shift already pulling higher-performance, fast-curing adhesives into prefabrication lines. Penang’s battery-separator hub strengthens local sourcing of specialty chemistries for cell assembly, while bonded-warehouse e-commerce hubs in Klang Valley and Johor lift volumes for carton-sealing and label adhesives. Raw-material tariffs and skilled-labor shortages remain headwinds, yet recent multinationals’ investments in regional technical centers shorten lead times, deepen local formulation support, and help the Malaysia Adhesives market absorb supply shocks.

Key Report Takeaways

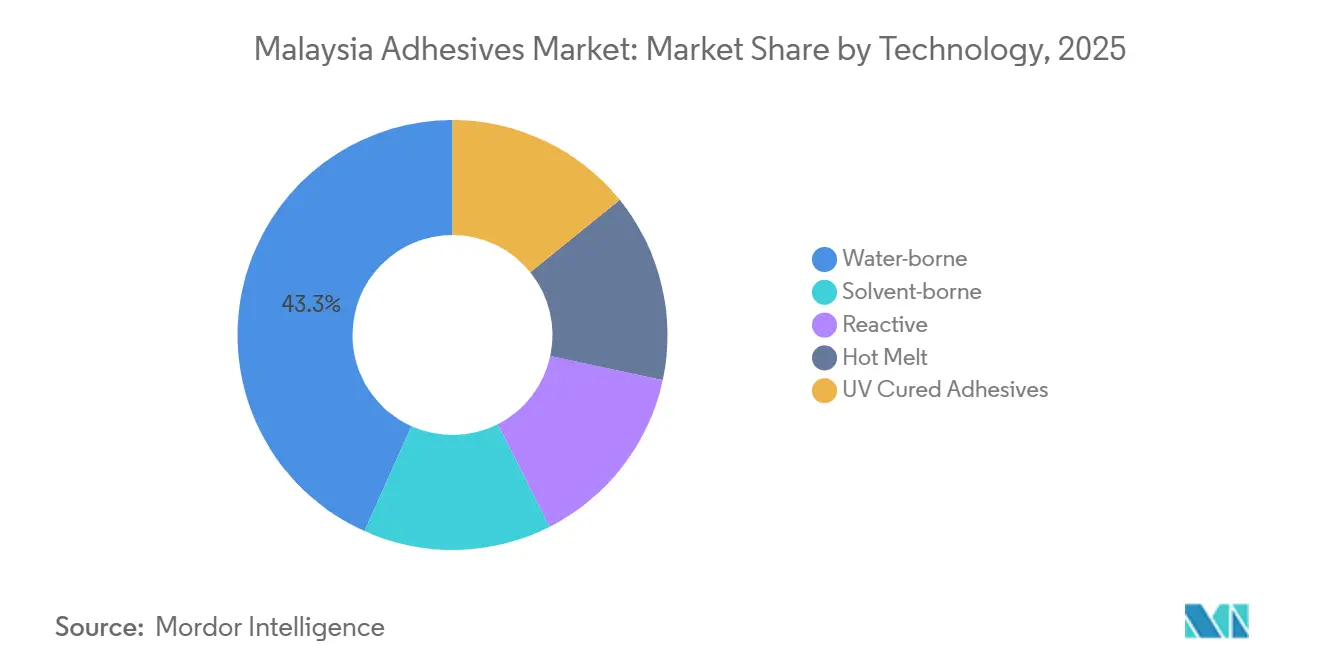

- By technology, water-borne held the largest market share of 43.28% in 2025, and the demand for hot-melt-based ones is expected to grow with a CAGR of 6.34% during the forecast period (2026-2031).

- By resin, acrylic had the largest share of 31.46% in 2025, and VAE/EVA's demand is expected to grow at a CAGR of 6.27% during the forecast period (2026-2031).

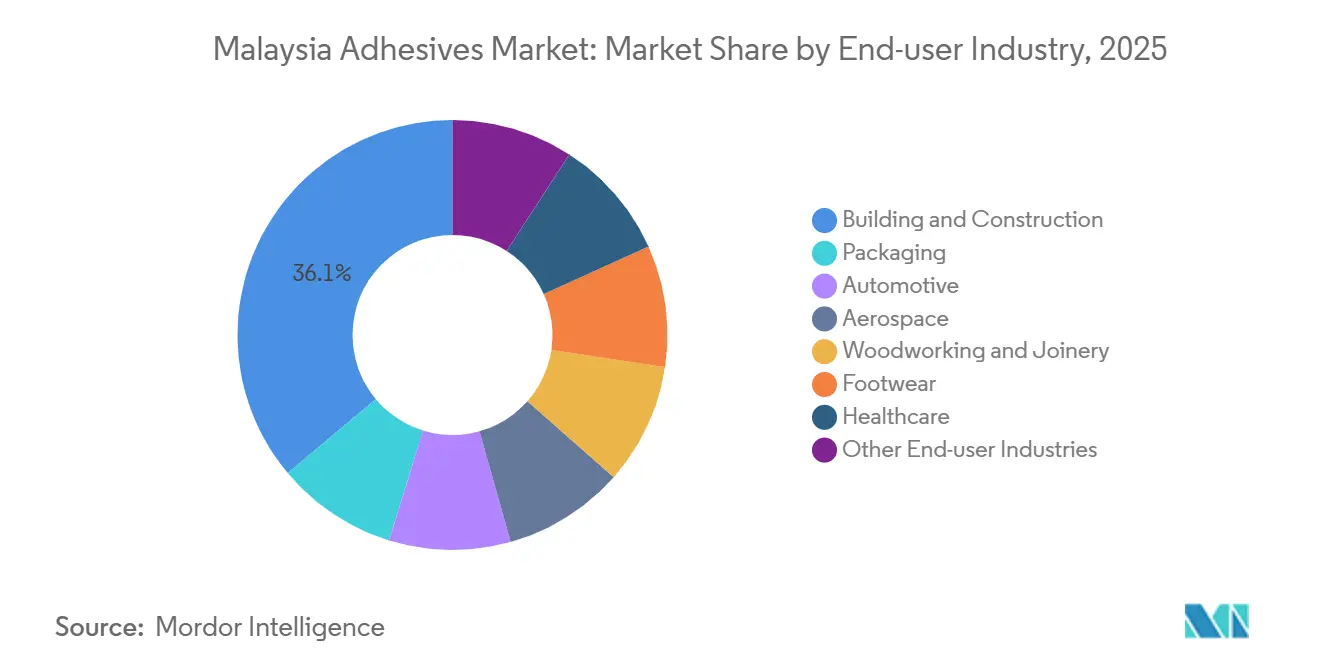

- By end-user industry, building and construction had a market share of 36.11% in 2025, and the automotive industry's share is expected to increase at a CAGR of 6.31% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Malaysia's National Construction Policy 2030 boosts demand | +1.2% | National, with concentration in Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Growing EV-battery assembly operations in Penang | +0.8% | Penang Technology Park, spillover to Selangor and Johor automotive clusters | Medium term (2-4 years) |

| Bonded-warehouse e-commerce boom increases packaging adhesives | +0.6% | National, with logistics hubs in Klang Valley, Johor (Port of Tanjung Pelepas proximity) | Short term (≤ 2 years) |

| Halal-certified bio-adhesives gaining export premiums | +0.3% | National production, export-oriented to Middle East, ASEAN Muslim-majority markets | Long term (≥ 4 years) |

| Local content rules in public housing spur wood-based panels | +0.5% | National, early adoption in Selangor, Johor public housing projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Construction Policy 2030 Accelerates Prefabrication and Infrastructure Maintenance Demand

Malaysia’s National Construction Policy 2030 mandates at least 50% digitalization of project lifecycles and compulsory BIM adoption for public works, creating detailed adhesive specifications for factory-controlled prefabrication lines[1]Construction Industry Development Board Malaysia, “National Construction Policy 2030,” cidb.gov.my. Greater traceability under QLASSIC and SHASSIC ratings rewards suppliers holding low-VOC or MyHIJAU labels. Repair and maintenance budgets, set to comprise up to 50% of future infrastructure outlays, add recurring demand for façade and bridge-repair bonding agents. The policy’s balance-of-payments clause encourages local sourcing, giving domestic producers a pricing advantage over imports. Collectively, these elements add an estimated 1.2 percentage-points to long-term growth potential in the Malaysia Adhesives market.

Penang’s Battery-Separator Hub Unlocks Specialty Opportunities

INV New Material’s USD 750 million separator plant, operational since June 2025 at 1.3 billion m² annual capacity, anchors Southeast Asia’s largest separator supply and requires heat-resistant, electrochemically stable adhesives for pouch cell assembly. Phase-two expansion in 2027 lifts capacity to 2 billion m², tying suppliers into a high-growth EV chain expected to support 15% of global separator demand. Multinationals such as Henkel have responded by upgrading regional labs to provide PFAS-alternative benchmarking and thermal-interface material development[2]Henkel AG, “Henkel Opens Electronics Adhesive Hub,” henkel.com. Close collaboration with Universiti Sains Malaysia on joint research and development further embeds a science-driven ecosystem that will sustain 0.8 percentage-points of incremental CAGR for the Malaysia Adhesives market.

E-Commerce Logistics Expansion Drives Packaging Adhesive Volumes

Bonded warehouses clustered near Kuala Lumpur International Airport and Port of Tanjung Pelepas process rising cross-border parcels, pushing hot-melt and pressure-sensitive adhesive volumes for corrugated cartons and labels. A new coating line coming online at UPM’s Johor factory mid-2026 will add filmic label capacity aimed at durable electronics shipped through these nodes. Retailers focused on sustainable packaging shift specifications toward water-based formulas that slash VOCs by as much as 60% relative to solvent systems. The immediate, shipment-driven nature of e-commerce lends short-term momentum worth roughly 0.6 percentage-points to market CAGR.

Halal Certification Creates Premium Channels for Bio-Based Adhesives

Demand from Middle East and ASEAN Muslim-majority importers lifts premiums for adhesives verified under JAKIM or equivalent halal standards. Nitto’s dual-sided tapes combine solvent-free acrylic chemistry with dermatological safety, illustrating how religious compliance dovetails with sustainability. University research using lignin-fortified natural rubber latex has surpassed ASTM fiberboard strength minimums, indicating technical readiness for commercial scale. As more producers pursue halal certification, the Malaysia Adhesives industry captures long-run export upside estimated at 0.3 percentage-points of additional CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortage in woodworking and furniture clusters | -0.7% | Johor (Muar, Segamat), Negeri Sembilan (Gemas), Perak, Sarawak | Short term (≤ 2 years) |

| Slow ASTM/ISO harmonisation delays aerospace uptake | -0.3% | Penang electronics clusters, proximity to Singapore aerospace hub | Long term (≥ 4 years) |

| Import duties on specialty isocyanates | -0.4% | National, affecting polyurethane formulators and automotive/construction end-users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Woodworking Labor Scarcity Constrains Volumes

Furniture exporters in Muar and Gemas report order cancellations as lead times doubled to 120 days by late 2024, curbing adhesive offtake for panel lamination and edge-banding. Automation retrofits partially offset manpower gaps, yet small and medium enterprises struggle with capital costs, shaving 0.7 percentage-points from potential CAGR growth in the Malaysia Adhesives market.

Aerospace Adhesive Uptake Hindered by Certification Lags

Despite SIRIM’s accredited composite labs, a lack of locally aligned ASTM and ISO pathways extends qualification cycles for aerospace-grade structural films and sealants. Multinationals continue to import pre-certified stock, limiting knowledge transfer and trimming 0.3 percentage-points from long-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance, Hot-Melt Momentum

Water-borne systems accounted for 43.28% of Malaysia Adhesives market share in 2025, driven by stricter indoor-air regulations and easier equipment cleanup. Investments in low-VOC vinyl-acetate-ethylene (VAE) dispersions and acrylic emulsions support continued leadership. Hot-melt lines, fueled by hygiene-product assembly and high-speed packaging, are slated to record a 6.34% CAGR to 2031, gradually raising their slice of the Malaysia Adhesives market. Formulators such as AICA Adtek and Wilron commission new extrusion capacity that can deliver stick or pillow formats optimized for automated dispensing.

Fast-tack performance, zero solvent emissions, and immediate handling strength make hot-melt chemistries attractive for EV battery-pack side-seam sealing and e-commerce carton closure. Yet capital requirements for melt tanks and temperature-controlled lines still limit adoption among smaller woodworking firms that default to water-borne PVAs. Regional subsidies for energy-efficient packaging equipment could hasten technology displacement and reshape Malaysia Adhesives market dynamics.

By Resin: Acrylic Versatility, VAE/EVA Upswing

Acrylic emulsions held 31.46% of Malaysia Adhesives market share in 2025. Their balanced tack-to-peel profile suits paper laminates, pressure-sensitive labels, and tropical-climate construction joints. Copolymers of vinyl acetate and ethylene (VAE/EVA) are forecast to outpace at 6.27% CAGR during the forecast period (2026-2031), leveraging superior waterproofing and flexibility needed for façade insulation systems in humid zones.

Price volatility in vinyl-acetate monomer still affects resin economics, but expanded regional cracker capacity in Indonesia may ease future supply. Polyurethane and epoxy resins remain indispensable in structural automotive and electronics encapsulation niches, yet their combined volume trails acrylics by more than half. Active research and development into lignin-modified acrylic backbones promises to add bio-content without sacrificing performance, a differentiator for halal-certified offerings.

By End-user Industry: Construction Leads, Automotive Electrifies Growth

Building and construction absorbed 36.11% of Malaysia Adhesives market size in 2025, reflecting robust pipeline repair, data-center fit-outs, and public housing. Fire-rated sealants, tile mortars, and waterproof membranes dominate volumes. Automotive demand is projected to climb fastest at 6.31% CAGR during the forecast period (2026-2031), tied to Proton and Perodua EV rollouts and UMW Toyota’s hybrid-battery assembly. Each vehicle integrates up to 15 kg of structural adhesives, from battery pack sealing to mixed-material body-in-white joints.

Packaging ranks third, buoyed by e-commerce logistics, while woodworking growth is capped by raw-material and labor constraints. Aerospace and medical devices remain niche but offer margin-rich pockets once local qualification frameworks mature.

Geography Analysis

Greater Kuala Lumpur and Selangor form the epicenter of Malaysia Adhesives market demand thanks to data-center builds, MRT expansions, and dense manufacturing estates. Johor contributes sizable volumes via furniture exports and e-commerce warehouse hubs linked to Singapore’s port corridors. Penang’s electronics and battery-separator complexes elevate specialty adhesive usage for die-attach, underfill, and thermal-interface applications.

Sabah and Sarawak trail in share yet present untapped upside as industrial-forest projects push panel production closer to timber sources, cutting logistics costs for bulky urea-formaldehyde resins. Government incentives under the New Industrial Master Plan 2030 nudge formulators toward satellite facilities in these eastern states, aiming to shorten supply chains and localize compliance testing.

Overall, peninsular Malaysia commands the majority of current volumes, but East-Malaysia’s share could increase by 2031 if infrastructure corridors and downstream timber processing reach the planned scale. Such redistribution would diversify the Malaysia Adhesives market and heighten requirements for multi-site technical-service coverage.

Competitive Landscape

The Malaysia Adhesives market is moderately consolidated. White-space opportunities cluster around halal-certified bio-adhesives, battery-pack thermal adhesives and aerospace-grade structural films. Market entrants must navigate stringent standards committees where incumbents often hold voting seats, yet collaboration with local universities offers a viable path to validation and niche positioning within the Malaysia Adhesives market.

Malaysia Adhesives Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

Mohm Chemical Sdn. Bhd.

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kumpulan Jetson Bhd revealed its intention to sell its complete equity stake in GRP Sdn Bhd, a subsidiary it wholly owns indirectly. GRP specializes in producing and selling adhesives and sealants.

- May 2025: DIC Malaysia introduced the DUALAM solvent-free adhesive technology to partners, customers, and industry peers from Malaysia, Indonesia, and Vietnam.

Malaysia Adhesives Market Report Scope

Adhesives, including glue and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The Malaysia Adhesives Market is segmented by technology, resin, and end-user industry. By Technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By Resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By End-user Industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-user Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms