Low Voltage Motor Control Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

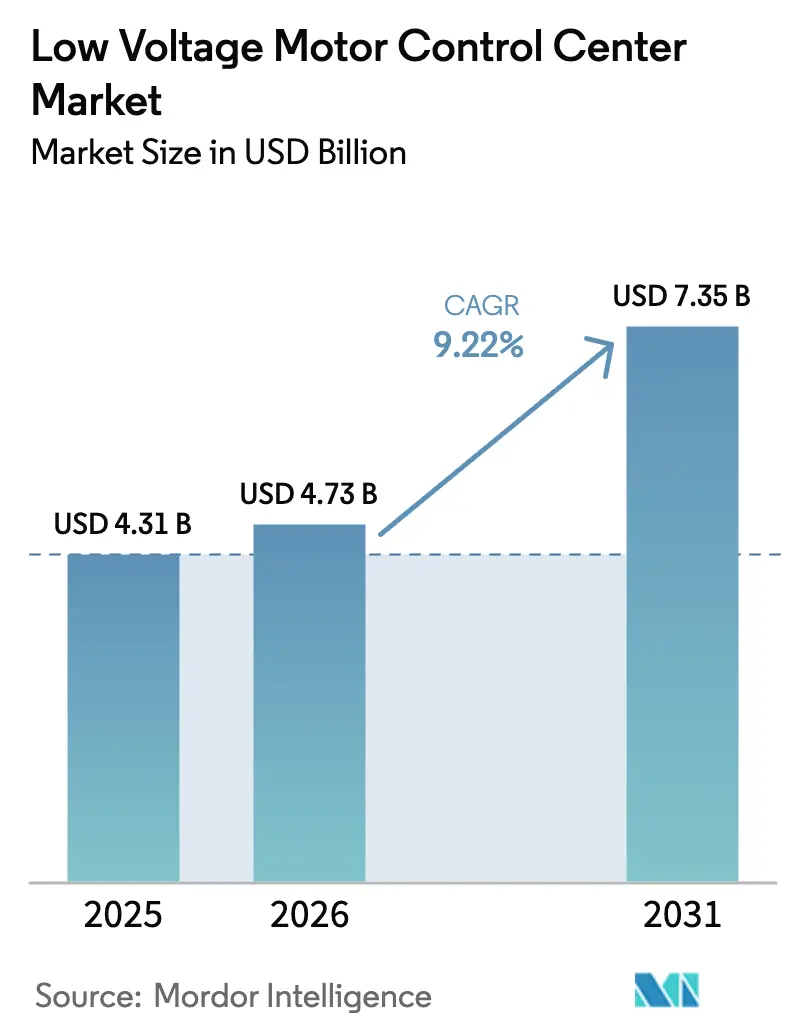

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 7.35 Billion |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

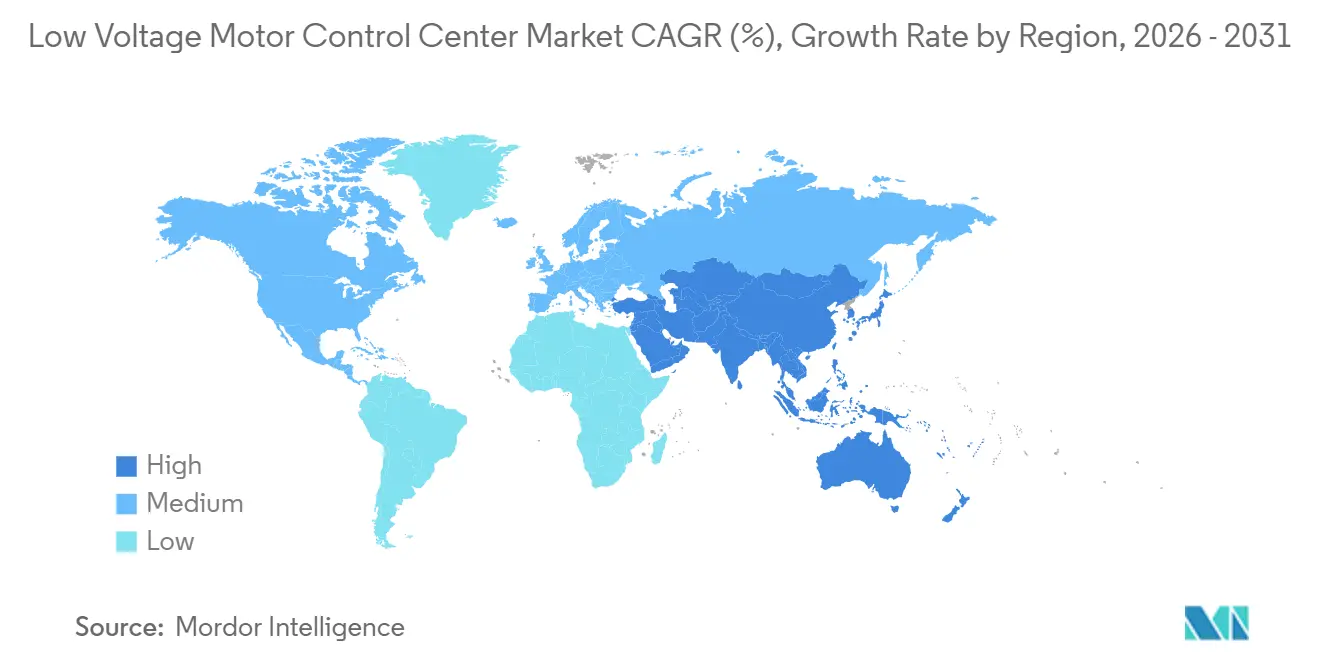

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Voltage Motor Control Center Market Analysis by Mordor Intelligence

The low voltage motor control center market is valued at USD 4.73 billion in 2026 and is projected to reach USD 7.35 billion by 2031, advancing at a 9.22% CAGR. The convergence of factory digitalization, demand for energy-efficient motor operations, and large-scale infrastructure programs is accelerating the procurement of intelligent switchgear that embeds IoT sensors, edge analytics, and cybersecurity safeguards. Variable-speed drives (VSDs) built on wide-bandgap semiconductors are reducing energy use by as much as 50% in pumping and HVAC duty cycles, resulting in measurable cost savings for users. The Asia-Pacific region remains the largest revenue contributor, driven by the integration of renewable energy sources in China and India. In contrast, North America and Europe are prioritizing retrofits that extend asset life without lengthy outages. Strategic moves by global suppliers, such as embedding predictive-maintenance algorithms trained on 10 million operating hours, are tilting revenue mix toward software and services. Meanwhile, cybersecurity frameworks under IEC 62443 and United States binding directives are tightening procurement specifications, effectively elevating intelligent variants from nice-to-have to non-negotiable.

Key Report Takeaways

- By type, conventional motor control centers held 74% of revenue in 2025; intelligent variants are forecast to expand at a 9.87% CAGR through 2031.

- By component, busbars led with 58% of revenue in 2025, whereas variable speed drives are expected to grow at a 10.12% CAGR to 2031.

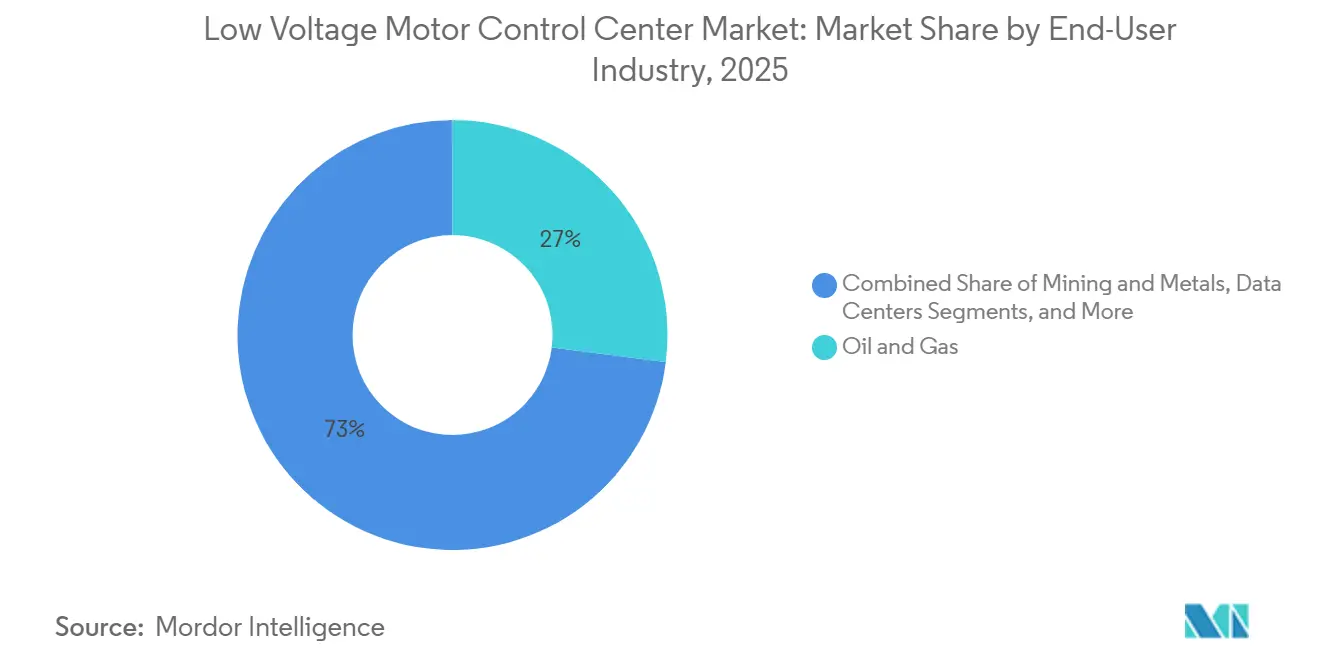

- By end-user industry, the oil and gas sector commanded a 27% share in 2025, while data centers posted the fastest growth outlook at a 10.95% CAGR through 2031.

- By installation, new installations captured 60% of 2025 shipments, yet retrofit activity is advancing at a 9.62% CAGR to 2031.

- By geography, the Asia-Pacific region accounted for 40% of global revenue in 2025 and is projected to grow at a 10.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Voltage Motor Control Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial Automation and Industry 4.0 Adoption | +2.3% | Germany, Japan, South Korea, United States | Medium term (2-4 years) |

| Demand for Energy-Efficient Motor Operations and Regulatory Standards | +2.1% | European Union, North America | Long term (≥ 4 years) |

| Expansion of Infrastructure Projects in Emerging Economies | +1.9% | Asia-Pacific core, Middle East and Africa | Medium term (2-4 years) |

| Rapid Shift Toward Intelligent Motor Control Centers with IoT Integration | +1.6% | North America, Europe, advanced Asia-Pacific | Short term (≤ 2 years) |

| Integration of Wide-Bandgap Power Semiconductors | +0.8% | Global, for early adopters | Medium term (2-4 years) |

| Growing Adoption of Modular Skid-Mounted MCCs | +0.5% | Remote mining sites and renewable projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Industrial Automation and Industry 4.0 Adoption

Factories are collapsing control silos by directly tying low voltage motor control centers into Ethernet-based plant networks, which unify programmable logic controllers, manufacturing execution systems, and cloud dashboards. The approach enables real-time load balancing, predictive diagnostics, and automated spare parts ordering, resulting in a 22% reduction in unplanned downtime across 140 plants in 2025.[2]Siemens AG, “Annual Report 2025,” siemens.com Public subsidies such as Germany’s EUR 500 million (USD 565 million) Industry 4.0 fund are offsetting capital costs for small manufacturers. South Korea’s mandate for IoT-enabled MCCs in any new facility above 10 MW by 2027 is creating a locked-in replacement cycle. These benefits come with heightened cyber-risk, so buyers are bundling IEC 62443-compliant firewalls that add 8-12% to project budgets but are now prerequisites for insurance coverage in critical infrastructure sectors.

Demand for Energy-Efficient Motor Operations and Regulatory Standards

Electric motors draw 45% of global electricity consumption, making them central to decarbonization policy. The European Union’s 2024 Ecodesign update moves the minimum efficiency bar to IE4 by 2027 and IE5 by 2030, which effectively forces pairing of premium-efficiency motors with VSDs inside low voltage motor control centers. In municipal water systems, swapping fixed-speed pumps for VSD-enabled units trimmed energy use by 42% and delivered a payback in under three years. China’s Top Runner tax rebates covering 20% of VSD investments lifted intelligent MCC installations 14% year-on-year during 2025. North American utilities now pay industrial customers up to USD 120 per MWh for demand-response load shedding, which is impossible without intelligent centers that can modulate torque on command.

Expansion of Infrastructure Projects In Emerging Economies

India’s National Infrastructure Pipeline earmarks USD 1.4 trillion through 2030, with one-third of the commitment allocated to electrical distribution, which includes motor control centers for metro rail, pumping, and wastewater plants. Saudi Arabia’s USD 320 billion NEOM and Red Sea megaprojects rely on modular, pre-commissioned MCC skids to maintain aggressive schedules in remote areas. Indonesia’s 18 GW coal-to-gas program requires intelligent centers with cloud monitoring to satisfy multilateral lenders. These large orders favor factory-tested assemblies, which compress onsite commissioning from 12 weeks to 3 weeks, addressing labor shortages while reducing field errors by 40%. However, currency swings such as the Turkish lira’s 28% slide in 2024 have nudged suppliers toward cost-plus contracts that trade margin certainty for risk mitigation.

Rapid Shift Toward Intelligent Motor Control Centers with IoT Integration

Ethernet switches, edge gateways, and secure cloud links embedded in low voltage motor control centers are extending motor lifetimes by 15-25% through condition-based maintenance. ABB’s Ability platform spots bearing degradation up to eight weeks ahead of failure by analyzing vibration envelopes, allowing intervention during routine shutdowns. Rockwell’s FactoryTalk funnels telemetry straight into enterprise resource planning modules, automating parts procurement once thresholds are crossed. Compliance pressure is accelerating adoption: United States DHS directive BOD 23-01 obligates critical infrastructure sites to segment OT networks and deploy deep-packet inspection on all connected MCCs, with non-compliance exposing owners to liability in the event of a breach. Even so, the added security stack inflates upfront costs by USD 80,000-USD 250,000 per facility, a hurdle offset by avoided downtime and lower insurance premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Investment and Total Cost of Ownership | -1.4% | Global, price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled Personnel for Installation and Maintenance | -0.9% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity Liabilities from Increased Connectivity | -0.6% | North America, European Union | Medium term (2-4 years) |

| Grid Harmonic Compliance Constraints | -0.5% | Weak-grid regions, island utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment and Total Cost of Ownership

Intelligent low voltage motor control centers, equipped with IoT sensors, edge analytics, and security hardening, cost 35-55% more than relay-based assemblies, resulting in a 4-7 year payback that strains budgets in cyclical industries. Sixty-two percent of plant managers surveyed by IEEE in 2025 cited upfront costs as their primary barrier to upgrade, even where lifetime savings exceed USD 500,000. Ongoing costs, such as software licenses and cloud storage, add USD 15,000-USD 40,000 per year, while currency hedging can increase the cost of imported hardware by 12%. Financing remains scarce for small enterprises in developing economies, delaying modernizations until catastrophic failure forces emergency spending.

Shortage of Skilled Personnel for Installation and Maintenance

Retirement of experienced electricians is outpacing new entrants; 38% of licensed professionals in North America and Europe are set to retire by 2030. Intelligent centers require commissioning specialists who can tune power electronics, harden networks, and fine-tune cybersecurity rules, skills that remain scarce even in developed markets. Schneider Electric reported that labor shortages stretched project timelines an extra 14 weeks in 2025, triggering penalty clauses in turnkey contracts. Technical colleges and utilities are launching MCC-specific apprenticeships, but graduation rates trail demand. Augmented-reality field support offers a stopgap yet adds USD 20,000-USD 50,000 in hardware and licensing per site.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Conventional Stronghold Faces Digital Momentum

Conventional assemblies claimed 74% of 2025 sales, anchored by decades-old design familiarity, abundant spare parts, and technicians skilled in relay logic. Yet intelligent variants are projected to climb at a 9.87% rate, boosted by integration into supervisory control systems that facilitate predictive maintenance and utility demand-response payments. Rockwell Automation demonstrates that digital diagnostics can slash mean time to repair by 35%, critical on offshore rigs where every technician mobilization costs more than USD 10,000. The low voltage motor control center market size for intelligent units is expected to widen its footprint as utilities roll out time-of-use tariffs that penalize inflexible loads. Retrofit kits, such as ABB’s Ability modules, allow operators to digitize existing boards for only 20-30% of full replacement cost, which accelerates adoption when capital budgets are tight.

While conventional gear remains attractive in cost-sensitive tenders, its inability to interface with cybersecure Ethernet networks or participate in automated load shedding is steadily eroding its competitive edge. A high-profile ransomware event at a European chemical plant in 2025 forced insurers to require IEC 62443 certification for coverage renewals, effectively making connectivity with security a procurement prerequisite. The low voltage motor control center market is therefore tipping toward intelligent offerings, especially in regions where utilities remunerate flexibility or where regulators tighten energy-efficiency benchmarks.

By Component: VSDs Take Center Stage As Efficiency Mandates Tighten

Busbars held 58% of 2025 component revenue due to their critical role in distributing high current across starters, breakers, and overload relays. Oil and gas, mining, and heavy-duty sectors still favor copper-intensive busbars designed for high inrush currents. However, variable speed drives are projected to post a 10.12% growth rate through 2031, responding to IEC 60034-30-1 requirements for higher motor efficiency classes. The low voltage motor control center market size for VSD-embedded boards is expected to expand as wide-bandgap semiconductors deliver 98% inverter efficiency and 30% smaller footprints, allowing higher density in data centers.

SiC-based inverters accounted for 18% of Mitsubishi Electric’s industrial drive shipments in 2025, up from 9% in 2023. These gains underscore how component mix is tilting away from passive copper toward active power electronics. Meanwhile, soft starters are losing relative share as VSD price premiums contract to 10-15%. Margin pressures on commoditized elements such as surge arresters and fuses are steering vendors toward value-added analytics that create subscription revenue in the low voltage motor control center market.

By End-User Industry: Data Centers Lead Growth Curve

Oil and gas logged 27% of 2025 demand but faces share erosion as greenfield drilling budgets migrate toward carbon-capture retrofits that require explosion-proof digital boards. Data centers are projected to expand at 10.95% through 2031, reflecting hyperscale operators’ preference for modular, pre-commissioned skids that can shave six to nine months from construction schedules. Amazon reported 60% onsite labor savings after adopting the approach in 22 data halls, which directly influences the low-voltage motor control center market share held by data centers.

Mining, metals, and chemicals represent mature verticals where replacement cycles drive steady but slower growth. Water utilities in California, piloting demand-response programs, earned USD 50-USD 120 per MWh in incentive payments by modulating pump loads through intelligent motor control centers. Pharmaceutical and automotive factories are implementing clean-power conditioning within MCCs to meet stringent quality regulations, indicating that regulatory compliance continues to steer procurement across multiple verticals.

By Installation Type: Retrofit Wave Gathers Pace

New installations accounted for 60% of 2025 shipments, driven by megaprojects in Asia-Pacific and the Middle East. Yet retrofits are advancing at a 9.62% CAGR, energized by aging fleets in North America and Europe, where 40-50% of installed boards have exceeded 25-year lifespans. The low-voltage motor control center market size for retrofit projects is further buoyed by insurance mandates after a USD 180 million arc-flash incident in Texas underscored the risk of legacy gear.

Modular retrofit designs retain existing enclosures and busbars while replacing contactors and relays with digital-native components, saving 30-40% compared with a full replacement. Greenfield sites, especially in data centers and renewable generation, increasingly specify intelligent boards from day one, embedding telemetry into building-management systems that optimize energy use in real time. European Union energy-efficiency rules requiring annual audits and upgrades of 3% of public buildings are creating a predictable pipeline of retrofits, even though permitting hurdles can extend project timelines by more than a year.

Geography Analysis

Asia-Pacific generated 40% of 2025 revenue and is forecast to advance at 10.86% through 2031. China’s CNY 2.3 trillion (USD 320 billion) grid-modernization budget is channeling demand for intelligent centers with remote diagnostics, while India’s incentives for domestic production reduce import reliance and compress lead times. ASEAN economies court supply-chain relocation from China, opening markets for quick-deploy MCCs in electronics clusters. Mature Japanese and South Korean plants are retrofitting to meet tighter efficiency rules, while Australia trials microgrids that pair MCCs with solar and battery storage in remote mines.

North America and Europe contributed 45% of 2025 sales but face slower unit growth due to saturated installed bases. The United States Infrastructure Investment and Jobs Act dedicates USD 65 billion to grid upgrades, yet labor shortages and permitting delays extend build times. Germany’s rule compelling facilities above 10 MW to install demand-response-capable MCCs by 2028 establishes a captive retrofit cycle, whereas the United Kingdom is piloting sub-second frequency-response schemes that rely on Ethernet-based MCCs.

Middle East and Africa and South America register faster expansion on the back of megaprojects and resource extraction. Saudi Arabia’s USD 320 billion NEOM and Red Sea builds require explosion-proof, skid-mounted solutions in remote deserts. The United Arab Emirates tendered 12 GW of solar and nuclear capacity that mandates remote monitoring to meet International Atomic Energy Agency standards. Brazil’s USD 2.8 billion offshore electrification program and South Africa’s coal-retrofit initiatives financed by the World Bank are adding to order books in the low voltage motor control center market.

Competitive Landscape

Five global vendors, ABB, Schneider Electric, Siemens, Eaton, and Rockwell Automation, control an estimated 55-60% of global shipments, but regional specialists and EPC contractors claim the balance. Leading suppliers pivot toward software and services; Schneider Electric attributed 28% of its 2025 low voltage revenue to analytics subscriptions, up from 19% in 2022. Patent activity for SiC-based inverters and machine-learning diagnostics increased by 18% in 2025, indicating that innovation is shifting from mechanical protection to power electronics and software.

Midsized firms, such as Powell Industries and Technical Control Systems, specialize in hazardous-area certifications and modular skid assemblies that can shorten site work by up to 70 days. White-space opportunities include arc-flash mitigation, active harmonic filters, and edge platforms that integrate MCC data with enterprise planning software. Cybersecurity liabilities emerged after a ransomware attack on a European chemical plant prompted insurers to mandate IEC 62443 compliance and third-party penetration testing, highlighting the delicate balance between digital service revenue and risk exposure.

Strategic moves illustrate market dynamism. Eaton’s 2025 acquisition of Jiangsu Linyang Energy gives it an 18% slice of China’s fragmented market and a local supply chain. Siemens’ partnership with Microsoft integrates Azure edge analytics into Sirius boards, enabling pharmaceutical and food processors to meet FDA electronic record requirements. Mitsubishi Electric opened a SiC-drive line that achieves 98.5% inverter efficiency and 30% footprint reduction, supporting higher rack density in data centers.[3]World Bank, “South Africa Eskom Support Project,” worldbank.org

Low Voltage Motor Control Center Industry Leaders

Schneider Electric SE

Siemens AG

ABB Ltd.

Eaton Corporation PLC

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Schneider Electric committed EUR 180 million (USD 203 million) to expand its Bangalore, India MCC factory, adding 120,000 square meters of automated capacity.

- November 2025: ABB won a USD 95 million contract to deliver intelligent MCCs for Saudi Aramco’s Jafurah unconventional gas project.

- October 2025: Siemens partnered with Microsoft to embed Azure IoT edge analytics into its Sirius line, targeting FDA-regulated sectors.

- September 2025: Eaton closed its USD 420 million purchase of Jiangsu Linyang Energy, securing 18% local market share in China.

Global Low Voltage Motor Control Center Market Report Scope

Low Voltage Motor Control Centers (LVMCC) are a component of all electrical distribution systems and consist of one or more enclosed sections having a common power bus and motor control units. These provide the most suitable and secure method for grouping electrical motor control, automation, and power distribution in a compact and economic package. They are employed in residential, industrial, and commercial including buildings, oil and gas, and automotive manufacturing.

The Low Voltage Motor Control Center Market is Segmented by Type (Conventional Motor Control Centers, Intelligent Motor Control Centers), Component (Busbars, Circuit Breakers, Overload Relays, and More), End-User (Oil and Gas, Mining, Chemicals, Power, Food, Water, Buildings, Data Centers), Installation (New Installations, Retrofit and Upgrades), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Conventional Motor Control Centers |

| Intelligent Motor Control Centers |

| Busbars |

| Circuit Breakers and Fuses |

| Overload Relays |

| Variable Speed Drives |

| Soft Starters |

| Other Components |

| Oil and Gas |

| Mining and Metals |

| Chemicals and Petrochemicals |

| Power Generation and Utilities |

| Food and Beverage |

| Water and Wastewater Treatment |

| Commercial Buildings |

| Data Centers |

| Other End-User Industries |

| New Installations |

| Retrofit and Upgrades |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Type | Conventional Motor Control Centers | |

| Intelligent Motor Control Centers | ||

| By Component | Busbars | |

| Circuit Breakers and Fuses | ||

| Overload Relays | ||

| Variable Speed Drives | ||

| Soft Starters | ||

| Other Components | ||

| By End-User Industry | Oil and Gas | |

| Mining and Metals | ||

| Chemicals and Petrochemicals | ||

| Power Generation and Utilities | ||

| Food and Beverage | ||

| Water and Wastewater Treatment | ||

| Commercial Buildings | ||

| Data Centers | ||

| Other End-User Industries | ||

| By Installation Type | New Installations | |

| Retrofit and Upgrades | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the low voltage motor control centers market in 2026?

The market stands at USD 4.73 billion in 2026 and is projected to grow to USD 7.35 billion by 2031, reflecting a 9.22% CAGR.

Which component inside motor control centers is growing fastest?

Variable speed drives are expanding at 10.12% per year as efficiency mandates push users to replace fixed-speed starters with inverter-based systems.

Why are data centers important buyers of motor control centers?

Hyperscale operators favor modular, pre-commissioned MCC skids that cut onsite construction by up to nine months and support high-density electrical loads.

What regions offer the strongest growth opportunities?

Asia-Pacific leads with a 10.86% CAGR through 2031, driven by China's grid upgrades and India's renewable capacity build-out.

How does cybersecurity affect MCC procurement?

Insurers now require IEC 62443 compliance after ransomware incidents, making network-secure intelligent MCCs a default specification for critical facilities.

Are retrofits a larger opportunity than new installations?

New builds still account for 60% of shipments, but retrofits are growing quicker at 9.62% because half of legacy boards in North America and Europe exceed 25-year design lives.

Page last updated on: