Locum Tenens Staffing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

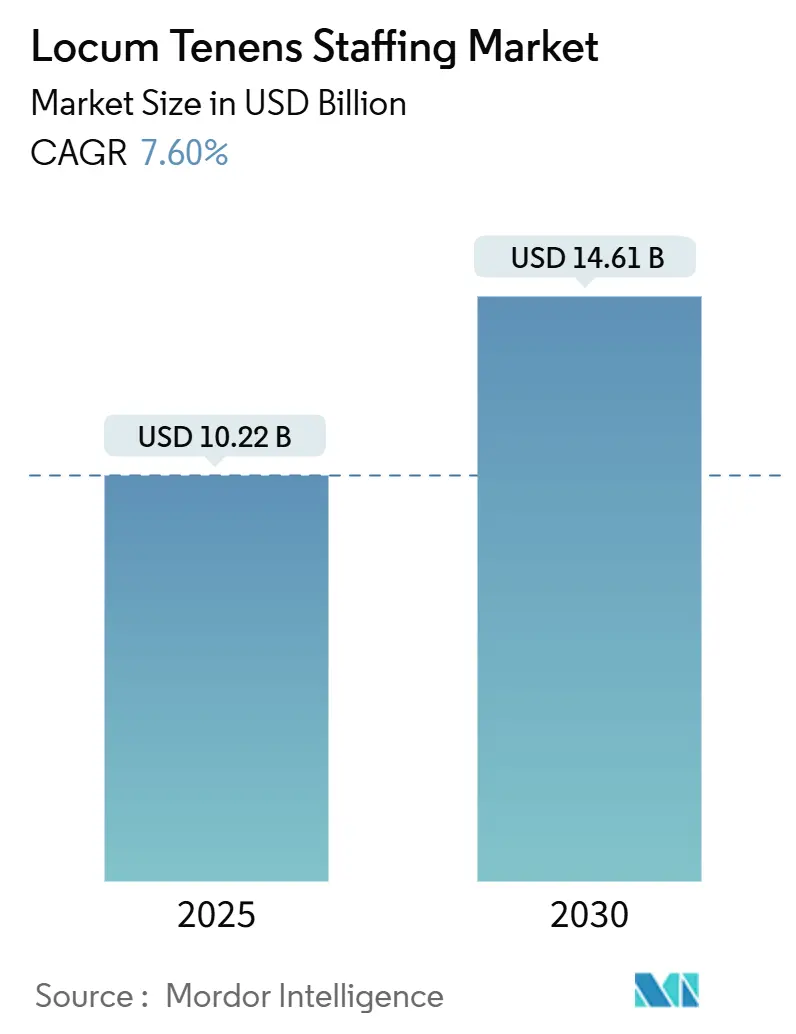

| Market Size (2025) | USD 10.22 Billion |

| Market Size (2030) | USD 14.61 Billion |

| Growth Rate (2025 - 2030) | 7.60% CAGR |

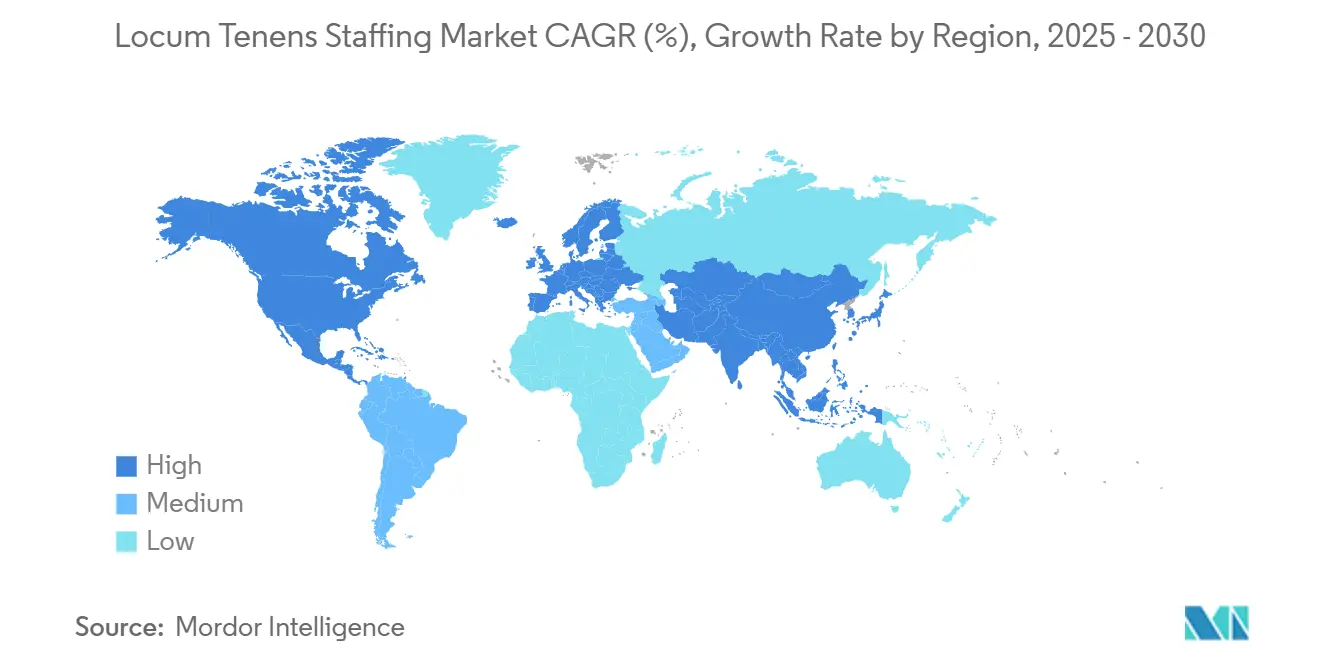

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Locum Tenens Staffing Market Analysis by Mordor Intelligence

The locum tenens staffing market size reached USD 10.22 billion in 2025 and is projected to advance to USD 14.61 billion by 2030, reflecting a 7.6% CAGR through the forecast period. Solid demand stems from widening physician shortages, rising chronic-care volumes, and the growing clinician preference for flexible work models. Elevated 2024 bill rates and double-digit volume gains carried into early 2025, setting the stage for a further 6% expansion in 2025 as hospitals rebalance post-pandemic staffing. Technology adoption is compressing credentialing cycles, allowing faster clinician deployment and supporting continued growth even as broader healthcare staffing normalizes. Consolidation among leading agencies, aggressive platform investment, and supportive multistate licensure reforms are reinforcing the momentum of the locum tenens staffing market across diverse care settings.

Key Report Takeaways

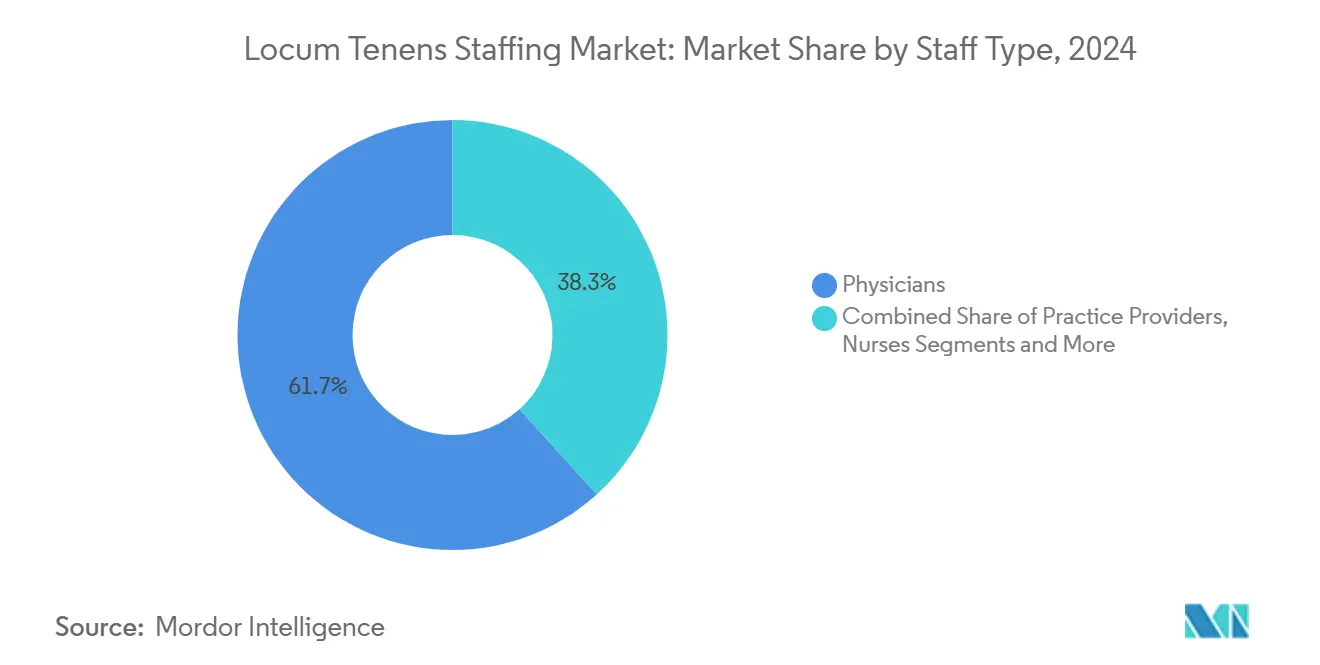

- By staff type, physicians led with 61.7% revenue share in 2024, while Advanced Practice Providers are projected to post the fastest expansion at a 10.8% CAGR through 2030.

- By medical specialty, family practice accounted for 15.2% of 2024 revenue, whereas psychiatry & behavioral health is set to grow the quickest at a 12.4% CAGR to 2030.

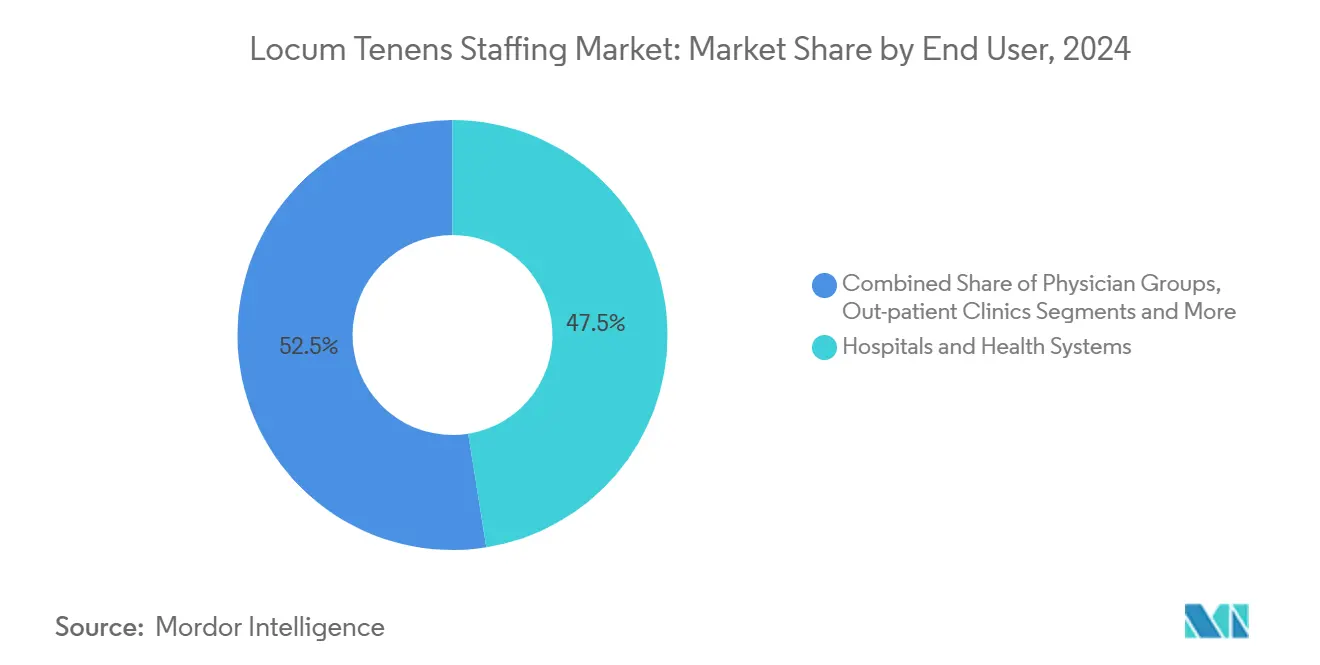

- By end user, hospitals & health systems held 47.5% of 2024 spending, while telehealth providers are advancing at an 11.9% CAGR over the forecast period.

- By contract duration, short-term engagements captured a 44.3% share in 2024 and represent the fastest-growing category with an 11.2% CAGR through 2030.

- By placement channel, traditional agencies maintained 63.1% of 2024 revenue, yet digital marketplaces are increasing fastest at a 13.5% CAGR to 2030.

- By geography, North America dominated with a 68.5% share in 2024, whereas Asia Pacific is on track for the strongest regional growth at a 9.5% CAGR through 2030.

Global Locum Tenens Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Global Clinician Shortages | +2.10% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Clinician Shift Toward Flexible Gig–Style Work | +1.80% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Aging-Driven Surge In Chronic-Care Visits | +1.50% | Global, pronounced in developed markets | Long term (≥ 4 years) |

| Cost Advantage Vs. Permanent Hires | +1.20% | Global, particularly rural and underserved areas | Short term (≤ 2 years) |

| AI-Driven Credentialing & Scheduling Adoption | +0.90% | North America & Europe early adoption | Medium term (2-4 years) |

| Value-Based Contracts Demand Coverage Continuity | +0.80% | North America, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Global Clinician Shortages

The Health Resources and Services Administration projects a deficit of up to 187,130 physicians by 2037, a gap compounded by roughly 10,000 annual physician retirements and slow medical-school pipeline growth.[1]Health Resources and Services Administration, “State of the Behavioral Health Workforce,” hrsa.gov Shortage pressure is acute in psychiatry, where more than 150 million Americans live in professional shortage areas, raising locum tenens utilization for behavioral health. Rural America bears a disproportionate burden, with 71% of locum doctors practicing in health professional shortage areas and serving around 75 million residents. Emergency departments, family medicine clinics, and hospitalist services are leaning on temporary coverage as permanent recruitment lags. Interstate Medical Licensure Compact provisions have cut average licensing times from months to about 7-10 days across 42 states, making rapid redeployment of scarce clinicians feasible.[2]American Medical Association, “Issue Brief: Interstate Medical Licensure Compact,” ama-assn.org Collectively, these dynamics keep the locum tenens staffing market on a strong demand trajectory.

Clinician Shift Toward Flexible Gig–Style Work

Survey data show 67% of U.S. physicians are familiar with locum work and 19% express strong assignment interest.[3]CHG Healthcare, “State of Locum Tenens: 2024 Report,” chghealthcare.com Motivations include autonomy, supplemental income, and better work-life balance, with younger doctors especially receptive to gig-style flexibility. Burnout hovering near 50% of permanent physicians accelerates temporary workforce expansion, while 79% of current locum physicians plan to continue such roles. Global gig-economy participation is projected to top 1.6 billion workers by 2025, and healthcare is emerging as a prime sector for flexible arrangements. Telehealth broadens the talent pool, as 59% of clinicians would accept virtual locum work, making geographic barriers less relevant. Together, these factors underpin sustained volume growth for the locum tenens staffing market.

Aging-Driven Surge in Chronic-Care Visits

The swelling senior population is swelling procedure counts and amplifying specialty shortages. Nearly half of U.S. counties lack a resident cardiologist, cementing demand for temporary coverage. Asia Pacific’s rapidly aging societies further amplify cross-border placement needs, positioning the region as the fastest-growing geography. Health systems deploying value-based care models need reliable coverage to safeguard quality metrics, pushing administrators toward locum contracts to avoid revenue penalties. As chronic-disease management intensifies, the locum tenens staffing market gains a durable structural driver.

Cost Advantage vs. Permanent Hires

Permanent primary-care recruitment averages 125 days, creating revenue voids that locum clinicians can immediately fill. While headline bill rates are high, temporary placement often remains cheaper than unfilled shifts when factoring in revenue preservation and avoided benefit costs. Rural facilities, half of which operate at a loss, rely on short-term locum coverage to maintain essential service lines without long-term salary liabilities. Consequently, the cost-flexibility calculus continues to favor the locum tenens staffing market in many scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Bill-Rates Strain Rural Hospital Budgets | -1.40% | Rural areas globally, acute in North America | Short term (≤ 2 years) |

| Multi-State Licensing & Onboarding Complexity | -0.80% | North America primarily, emerging in other regions | Medium term (2-4 years) |

| Telehealth Substitution For Select Specialties | -0.60% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Health-System-Owned Float Pools Reduce Demand | -0.50% | North America & Europe, hospital system dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Bill-Rates Strain Rural Hospital Budgets

Over 30% of U.S. rural hospitals face closure risk due to reimbursement gaps and fixed overhead pressures. Locum rates, while flexible, can exceed tight rural budgets, forcing administrators to ration coverage. Medicare wage-index disparities deepen funding mismatches, limiting spending power for premium temporary staffing. As a result, rural facilities must weigh immediate access against fiscal sustainability, tempering near-term growth for the locum tenens staffing market in these locations.

Multi-State Licensing & Onboarding Complexity

Despite Interstate Medical Licensure Compact gains, non-participating states maintain months-long licensing cycles that delay clinician deployment. Recently enacted agency-registration statutes in six U.S. states add paperwork and compliance costs. Facility-specific privileging still requires audits of malpractice coverage and orientation that can push onboarding beyond desired start dates. These frictions moderate growth, especially for urgent short-term placements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Staff Type: Physician Dominance Persists Amid APP Upswing

Physicians retained 61.7% revenue share in 2024, confirming their central role in complex decision-making and procedural medicine. Simultaneously, Advanced Practice Providers are growing at a 10.8% CAGR to 2030 as health systems broaden nurse practitioner and physician-assistant scope to counteract forecast deficits of up to 86,000 doctors by 2036. The locum tenens staffing market size for APP coverage is forecast to surpass USD 2.1 billion by 2030, underlining the segment’s momentum.

Broader clinician acceptance of team-based care supports this shift, particularly in primary care, emergency medicine, and behavioral health. Interstate licensing acceleration improves physician redeployment, yet APP supply expansion is proving faster, reinforcing their demand surge. As credentialing platforms integrate APP-specific privileging modules, placement friction declines, and hospitals lean on this cost-effective labor tier to maintain service lines without jeopardizing clinical quality.

By Medical Specialty: Primary Care Leads, Psychiatry Accelerates

Family practice captured 15.2% of 2024 revenue, reflecting its gateway role in healthcare and acute workforce shortages. The locum tenens staffing market share for psychiatry is expanding rapidly on the back of 12.4% CAGR expectations to 2030, driven by escalating mental-health utilization in all demographics.

Emergency medicine, hospitalist, and critical-care placements remain staples as 24/7 coverage mandates persist. Telepsychiatry widens market reach, letting providers cover multi-state patient panels, boosting placement volume despite fewer on-site days. Family practice, anesthesiology, gastroenterology, neurology, and cardiology round out the top ten in-demand specialties, ensuring a diversified revenue mix that anchors the locum tenens staffing market.

By End User: Hospitals Still Core While Telehealth Surges

Hospitals and integrated health systems held 47.5% of the locum tenens staffing market size in 2024, upheld by mandatory coverage obligations and high patient acuity. Their procurement sophistication drives complex multi-specialty engagements, sustaining volume notwithstanding tightening labor budgets.

Telehealth providers are pacing growth at 11.9% CAGR through 2030, aided by expanded Medicare codes and looser site-of-service rules. Ambulatory surgical centers, physician groups, government facilities, and long-term-care operators each cultivate niche demand, broadening end-user diversity and mitigating concentration risk for vendors.

By Contract Duration: Short-Term Engagements Take the Lead

Short assignments of 30 days or less amassed a 44.3% share in 2024 while posting an 11.2% CAGR outlook. Efficiency-minded administrators leverage these micro-contracts to bridge vacations, CME absences, and unplanned vacancies without long-term fiscal exposure.

Mid-term contracts fill maternity and sabbatical leaves, whereas long-term placements stabilize chronically underserved areas. Platform-enabled real-time availability visualization makes short stints practical, giving the locum tenens staffing market its most dynamic growth pocket.

By Placement Channel: Digital Marketplaces Gain Ground

Traditional agencies still hold 63.1% share thanks to deep client relationships and end-to-end credentialing services. Yet digital marketplaces are scaling fastest, with a 13.5% CAGR to 2030 and more than 20% of 2024 revenue. AI-powered matching slashes cycle times, and transparent fee structures attract both clinicians and facilities seeking cost savings.

Managed-service providers and hybrid models address enterprise needs by layering VMS tools atop agency networks, further modernizing the locum tenens staffing market’s ecosystem.

Geography Analysis

North America generated 68.5% of 2024 revenue, underpinned by the Interstate Medical Licensure Compact, advanced payer systems, and an acute shortage trajectory projecting a 13,500-86,000 physician gap by 2036. U.S. hospitals rely on locum physicians to avoid throughput bottlenecks, and Canada’s publicly funded system similarly taps temporary staff to guarantee coverage across remote provinces.

Asia Pacific is the fastest-growing region at a 9.5% CAGR through 2030, led by China and India. Demographic aging, investment in hospital infrastructure, and physician deficits mirroring developed nations drive demand. Regulatory modernization in Australia, Singapore, and Japan allows smoother foreign clinician entry, while telehealth adoption expands cross-border placement potential.

Europe maintains steady growth as EU free-movement directives support cross-member-state practice. Germany and the United Kingdom spearhead usage amid specialty shortages, although post-Brexit credentialing divergence creates new administrative hurdles. Middle East & Africa and South America represent smaller but rising markets, buoyed by medical-tourism initiatives and public-sector recruitment schemes for specialty coverage.

Competitive Landscape

Roughly 52,000 physicians—about 7% of the U.S. physician workforce—undertook locum assignments in 2024, evidencing a moderately fragmented supply base. Aya Healthcare’s USD 615 million purchase of Cross-Country Healthcare underscored consolidation pressures as leading agencies vie for technology scale. AMN Healthcare, Jackson Healthcare, CHG Healthcare, and LocumTenens.com retain sizeable footprints built on decades-long client networks and full-service offerings.

Digital upstarts like Clipboard Health, DirectShifts, and Nomad Health leverage AI to cut placement latency, winning share in less complex settings. Traditional players respond with hybrid offerings—AMN’s ShiftWise Flex VMS and CHG’s Modio credentialing suite—blending platform speed with human oversight.

The specialty focus remains a differentiator: Medicus Healthcare concentrates on the niches of psychiatry and emergency medicine, while OptumServe targets government contracts. Regulatory compliance capabilities, especially IMLC expertise, have become pivotal for win-rate differentiation. Scale, technology integration, and white-glove service together define competitive advantage as the locum tenens staffing market enters a digital-first era.

Locum Tenens Staffing Industry Leaders

AMN Healthcare Services Inc.

CHG Healthcare

Cross Country Healthcare Inc.

Jackson Healthcare

Barton Associates Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Aya Healthcare closed its USD 615 million acquisition of Cross Country Healthcare, broadening coverage across all 50 states.

- November 2024: CHG Healthcare’s State of Locum Tenens 2024 survey revealed 82% of facilities rely on locums during permanent-hire searches and 46% use them to avert revenue loss.

- 2024: CMS finalized 2025 Physician Fee Schedule updates with expanded telehealth codes, widening virtual locum opportunities.

Global Locum Tenens Staffing Market Report Scope

| Physicians |

| Advanced Practice Providers (NP & PA) |

| Nurses |

| Allied Health Professionals |

| Administrative & Other Personnel |

| Primary Care (Family/Internal Medicine) |

| Emergency Medicine |

| Psychiatry & Behavioral Health |

| Hospitalist & Critical Care |

| Anesthesiology |

| Radiology & Imaging |

| Surgical Specialties |

| Diagnostic & Laboratory (Pathology, etc.) |

| Hospitals & Health Systems |

| Ambulatory Surgical Centers |

| Physician Groups & Out-patient Clinics |

| Telehealth Providers |

| Government & Military Facilities |

| Long-term Care & Rehab Centers |

| Short-term (Less than 30 days) |

| Mid-term (31-180 days) |

| Long-term (More than 180 days) |

| Traditional Staffing Agencies |

| Digital Marketplaces & Online Platforms |

| MSP / VMS Solutions |

| Hybrid Models |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Staff Type | Physicians | |

| Advanced Practice Providers (NP & PA) | ||

| Nurses | ||

| Allied Health Professionals | ||

| Administrative & Other Personnel | ||

| By Medical Specialty | Primary Care (Family/Internal Medicine) | |

| Emergency Medicine | ||

| Psychiatry & Behavioral Health | ||

| Hospitalist & Critical Care | ||

| Anesthesiology | ||

| Radiology & Imaging | ||

| Surgical Specialties | ||

| Diagnostic & Laboratory (Pathology, etc.) | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory Surgical Centers | ||

| Physician Groups & Out-patient Clinics | ||

| Telehealth Providers | ||

| Government & Military Facilities | ||

| Long-term Care & Rehab Centers | ||

| By Contract Duration | Short-term (Less than 30 days) | |

| Mid-term (31-180 days) | ||

| Long-term (More than 180 days) | ||

| By Placement Channel | Traditional Staffing Agencies | |

| Digital Marketplaces & Online Platforms | ||

| MSP / VMS Solutions | ||

| Hybrid Models | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the locum tenens staffing market?

Revenue reached USD 10.22 billion in 2025 and is projected to climb to USD 14.61 billion by 2030, equal to a 7.6% CAGR.

Which staff types are expanding the fastest in temporary clinician placements?

Advanced Practice Providers are pacing growth at a 10.8% CAGR through 2030, outpacing the physician segments mature 61.7% share.

How are digital marketplaces reshaping locum tenens procurement?

Platforms already capture 20% of segment revenue and, helped by AI-driven matching, are growing at a 13.5% CAGR, cutting fill times from hours to minutes.

What role does the Interstate Medical Licensure Compact play in clinician deployment speed?

The IMLC now covers 42 states and reduces licensing approval from months to about 710 days, enabling faster multistate placements.

Why are hospitals still the largest buyers despite telehealth growth?

Continuous-coverage mandates keep hospitals at a 47.5% revenue share, while telehealth volumes rise at 11.9% CAGR to complement, not replace, on-site needs.

How concentrated is competition among service providers?

The top five vendors control roughly 32% of segment revenue, signaling moderate fragmentation and leaving room for both consolidators and digital entrants.

Page last updated on: