Loitering Munition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

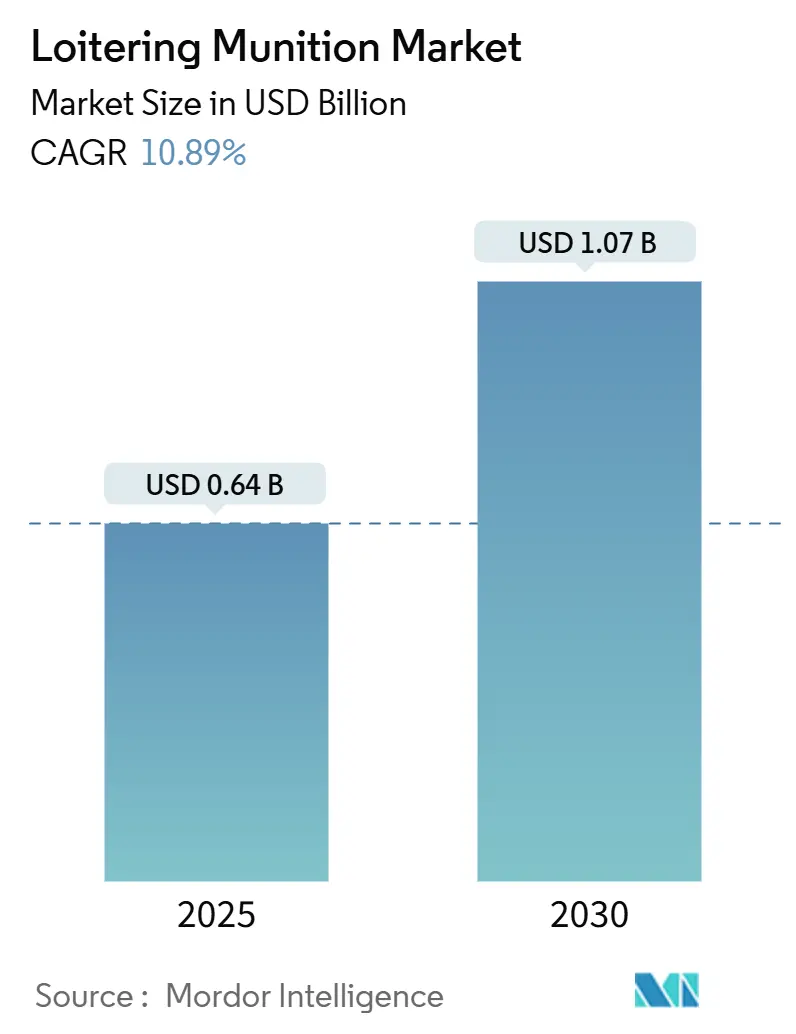

| Market Size (2025) | USD 0.64 Billion |

| Market Size (2030) | USD 1.07 Billion |

| Growth Rate (2025 - 2030) | 10.89% CAGR |

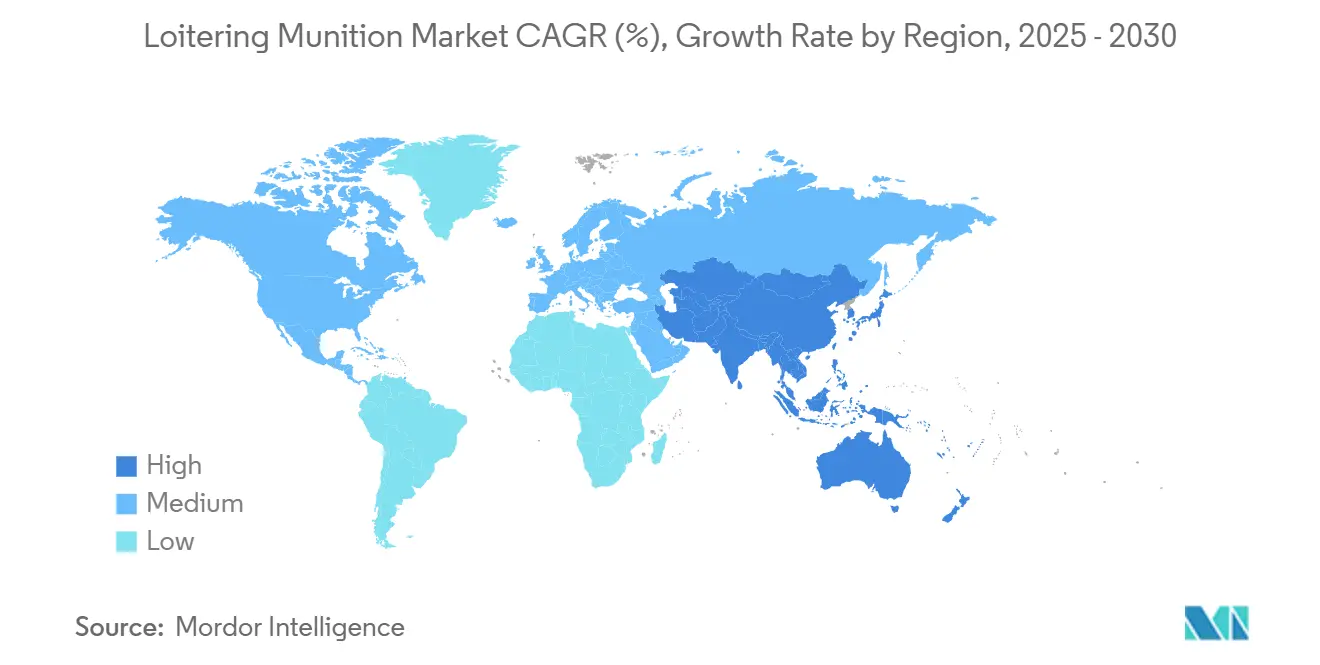

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Loitering Munition Market Analysis by Mordor Intelligence

The loitering munition market size reached USD 635.88 million in 2025 and is forecasted to climb to USD 1,066.43 million by 2030, advancing at a 10.89% CAGR. Sustained defense-modernization budgets, operational validation in Ukraine, and the need for precise, low-cost strike options continue to shift spending from conventional artillery toward intelligent, expendable systems. North America accounted for the largest loitering munition market share at 38.65% in 2024, supported by multi-year US procurement programs. Asia-Pacific is projected to register the fastest regional CAGR of 10.61% through 2030. Medium-range (50 to 100 km) designs dominate revenues, but long-range (greater than 100 km) variants are scaling quickly as standoff requirements grow. Naval forces are emerging as key adopters, experimenting with swarm concepts that extend coastal and littoral defense reach. On the industrial side, proven suppliers such as AeroVironment benefit from production scalability, yet new entrants offering AI-enabled swarm coordination are intensifying competition.

Key Report Takeaways

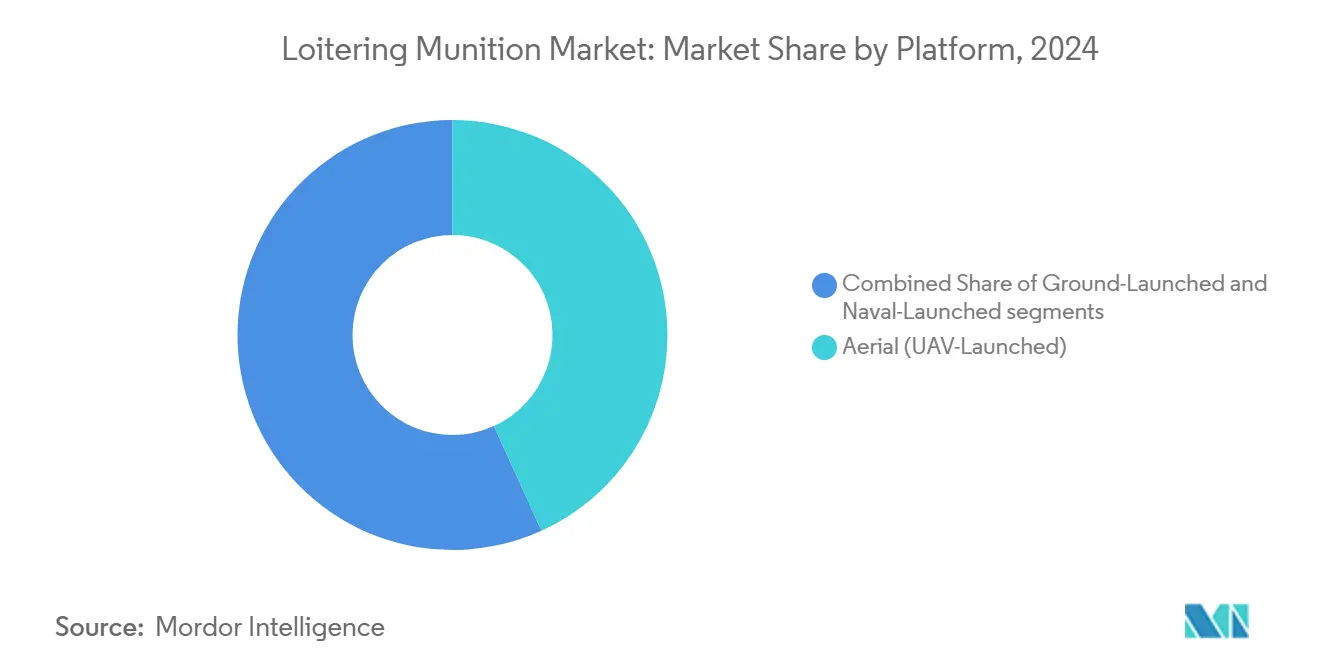

- By platform, aerial systems led with 43.21% revenue share in 2024; naval-launched systems are projected to expand at a 12.35% CAGR to 2030.

- By range, medium-range munitions commanded 47.34% of the loitering munition market size in 2024; long-range models are advancing at an 11.9% CAGR through 2030.

- By warhead type, fragmentation warheads held a 53.72% share in 2024; thermobaric options are forecasted to register a 9.65% CAGR to 2030.

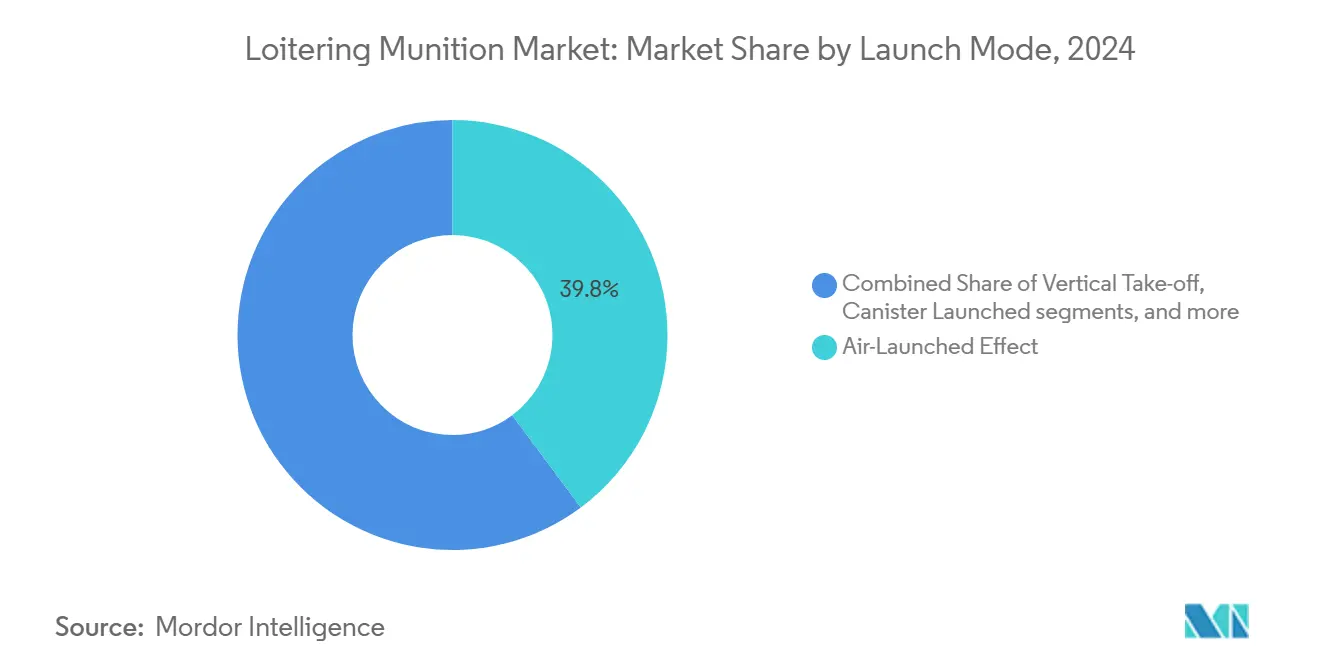

- By launch mode, air-launched effects captured a 39.82% share in 2024; canister-launched designs are growing at a 10.82% CAGR.

- By end user, air forces accounted for a 49.41% share in 2024; naval users are set to record a 12.46% CAGR by 2030.

- By geography, North America held a 38.65% market share in 2024; Asia-Pacific is expected to grow at a CAGR of 10.61% during the forecast period.

Global Loitering Munition Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of low-cost precision-guided munitions | + 2.10% | North America, Europe | Medium term (2-4 years) |

| Rising demand for man-in-the-loop strike options in contested A2/AD environments | + 2.80% | Asia-Pacific, Middle East and Africa | Long term (≥4 years) |

| Growing adoption for border security and counter-insurgency operations | + 1.90% | Middle East, South Asia | Short term (≤2 years) |

| Operational success in recent conflicts accelerating procurement | + 2.40% | Global | Short term (≤2 years) |

| Integration with AI-enabled autonomous target recognition | + 1.50% | North America, Europe | Long term (≥4 years) |

| Naval swarm concepts for coastal and littoral defense | + 1.20% | Asia-Pacific, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Low-Cost Precision-Guided Munitions

Affordable loitering munitions priced below USD 50,000 now give infantry-level units strike options once limited to high-value missiles. Ukraine ordered 4.5 million FPV drones for 2025, tripling 2024 volumes and illustrating mass-deployment economics.[1]“Ukraine Will Purchase 4.5 Million FPV Drones in 2025,” Anadolu Agency, AA.COM.TR Estonia’s EUR 400 million (USD 468.4 million), seven-year framework follows a similar path, signaling mid-tier nations’ intent to mainstream the capability. Manufacturing innovations in fast-curing composites and thermoplastics have raised throughput while cutting airframe costs. These economics reinforce tactical doctrines that favor saturation attacks over expensive single-shot missiles, accelerating adoption across NATO and allied forces.

Rising Demand for Man-in-the-Loop Strike Options in Contested A2/AD Environments

Modern anti-access defenses jam satellite navigation and datalinks, yet combatants still require human authorization before releasing lethal force. The US Defense Innovation Unit’s Project Artemis seeks long-range one-way drones that operate in GNSS-denied conditions but keep operators in control during the final attack.[2]DIU Awards Contracts for Long-Range One-Way Drones, Inside Defense, INSIDEDEFENSE.COM French developers demonstrated jam-resistant systems under Ukrainian electronic warfare (EW) pressure, and Chinese laboratories published swarm intelligence routines for satellite denied targeting. These programs balance ethical oversight with autonomy, aligning with international humanitarian-law requirements while meeting operational needs for deep-strike precision.

Growing Adoption for Border Security and Counter-Insurgency Operations

Mexico’s Secretaría de la Defensa Nacional has begun flight trials of man-portable loitering munitions along the Sonora–Arizona corridor, pairing them with fixed ground sensors to cut response times from minutes to seconds. Estonia’s EUR 400 million (USD 468.4 million) framework sets aside a battalion-level inventory, enabling round-the-clock border coverage that previously required helicopter patrols. Israel’s Police Border Guard plans to link its new “suicide-drone” fleet to a nationwide computer-aided dispatch network so commanders can task a munition directly from a patrol-car tablet. In South Asia, India’s Border Security Force integrates high-altitude units with satellite back-haul to maintain control links beyond 20 km, overcoming line-of-sight breaks in mountainous terrain. These deployments illustrate how loitering munitions are transitioning from special-forces assets to routine border-patrol tools, reinforcing demand across mid-sized defense budgets.

Operational Success in Recent Conflicts Accelerating Procurement

After the Switchblade 600’s publicized kill of a Russian SA-15, Ukrainian forces reported a 70% hit probability against moving armor when using coordinated two-drone tactics, doubling the confidence of prospective buyers. The US Marine Corps cited Ukraine data justifying its Organic Precision Fires–Light down-select, shortening milestone reviews by nine months. France’s Defense Procurement Agency fast-tracked Colibri prototypes into a six-month combat-evaluation window, bypassing the usual two-year qualification cycle. Germany’s Bundeswehr has earmarked EUR 1.2 billion (USD 1.41 billion) for immediate off-the-shelf purchases while domestic industry scales up HX-2 production, reflecting a new “buy-test-iterate” mindset. Such battlefield validations compress procurement timelines and ensure multi-year production visibility for manufacturers.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control tightening under MTCR Category-I interpretations | -1.80% | MTCR member states | Medium term (2-4 years) |

| EW countermeasures degrading mission effectiveness | -1.40% | Global conflict zones | Short term (≤2 years) |

| Public concerns over autonomous lethal weapons ethics | -1.10% | North America, Europe | Long term (≥4 years) |

| Supply-chain choke points in composite airframe components | -0.90% | Global supply hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Control Tightening Under MTCR Category-I Interpretations

The US Commerce Department added pulse-detonation engines and DMAZ propellant to its missile-technology control list in April 2025, sweeping up several long-range loitering-munition components. European Union states responded by harmonizing license-application questionnaires, increasing paperwork but reducing cross-border leakage of sensitive subsystems. Israel, a non-MTCR member, capitalized by signing rapid-delivery deals in the Caucasus and Central Asia, sidestepping Category-I ceilings while offering 250 km reach. The State Department’s end-use-monitoring clauses now require on-site inspections for exports over a 100 km range, raising compliance costs for US vendors. Collectively, these measures slow international sales of high-end models and shift demand toward locally produced or lower-spec variants.

Electronic Warfare Countermeasures Degrading Mission Effectiveness

Russian Krasukha-4 brigades in Donbas cut average GNSS availability for small drones to 18 seconds, forcing Ukrainian operators to rely on optic-flow navigation patches uploaded pre-flight. The US Joint Counter-UAS Office plans a 2026 field trial where blue-team loitering munitions must survive layered jamming, cyber spoofing, and laser dazzlers for eight minutes before strike approval. French developer Delair embedded a vision-based terrain-contour matcher in its OSKAR airframe, reducing positional drift to under 3 m in GNSS-denied zones at SOFINS 2025 demos. AeroVironment introduced a software update that swaps frequency bands mid-flight when signal-to-noise ratios degrade, but the added encryption pushes the unit cost 8% higher. Continual EW hardening raises R&D spending and underlines the technology-cost spiral facing suppliers and buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Aerial Dominance Drives Naval Innovation

Aerial systems captured 43.21% of the loitering munition market in 2024, reflecting seamless pairing with mature unmanned-aircraft command networks. The US Army’s USD 990 million Switchblade deal underscored operational confidence and ensured economies of scale. Ground-launched variants meet artillery-brigade needs for organic precision fires and border-security patrols, as shown by India’s order of 200 indigenous units for high-altitude engagements.

Naval-launched platforms are the fastest-growing segment at a 12.35% CAGR through 2030. Concepts such as LOCUST combine shipboard magazine depth with autonomous swarm tactics, opening a new theater for littoral warfare. European frigate programs now allocate deck space and power points for rapid-fire, canisterized loitering munition launchers, signaling design convergence between cruise-missile cells and smaller expendable systems.

By Range: Medium-Range Leadership Faces Long-Range Acceleration

Short-range (less than 50 km) units remain vital for urban and counter-insurgency missions where operators require visual confirmation before strike. Still, they capture under one-third of spending because limited reach exposes launch teams to return fire. Medium-range (50 to 100 km) weapons dominate with 47.34% of the loitering munition market size, thanks to standoff envelopes that stay under MTCR ceilings while still covering most brigade-level objectives; France’s Larinae is the exemplar at 50 km and sub-EUR 200,000 (USD 2,33,990) cost. Long-range classes (greater than 100 km) are scaling at an 11.9% CAGR as forces seek to suppress air-defense sites far beyond front lines; DIU’s Project Artemis calls for 300 km prototypes that edge close to cruise-missile performance. China’s public research on “super long-range” variants signals a tightening technology race that will pressure Western suppliers to extend range without triggering Category-I controls.

By Warhead Type: Fragmentation Prevalence Meets Thermobaric Innovation

Fragmentation warheads held a 53.72% share in 2024 because multi-effect charge liners can toggle between anti-personnel and light-vehicle modes, giving commanders flexible rules-of-engagement tools on a single airframe. Shaped-charge options retain a foothold for top-attack kills on main battle tanks. Still, increased active-protection systems nudge designers toward tandem-charge or precursor technologies to maintain lethality. Thermobaric loads—forecasted to grow 9.65% CAGR—produce prolonged overpressure ideal for clearing bunkers and subterranean complexes; South Korea added this selectable payload to its Warmate-3 buy, cutting the need for separate breach munitions. Vendors are now fielding clip-in payload modules so depot crews can re-role inventory within minutes, simplifying logistics for expeditionary forces.

By Launch Mode: Air-Launched Effects Lead Canister Innovation

Air-launched effects secured 39.82% of 2024 revenue because helicopters and fixed-wing assets can transport them deep into denied airspace, then release multiple rounds without exposing manned cockpits to short-range air defenses. South Korea’s plan to fire canisterized rounds from Light Armed Helicopters illustrates how legacy airframes gain instant stand-off punch without new hardpoints or software rewrites. Canister-launched models, growing at 10.82% CAGR, integrate with 155 mm artillery or vertical-launch cells so units can switch from ballistic to loitering modes on the same fire-control network; Australia’s OWL B catapult shows similar flexibility for dismounted troops. Vertical-takeoff and hand-thrown designs still serve special operations units that prioritize backpack portability. Still, future artillery-grade canisters with sealed batteries promise five-year shelf lives, reducing sustainment costs.

By End User: Air Force Leadership Yields to Navy Growth

Air forces owned a 49.41% share in 2024 because loitering munitions complement suppression-of-enemy-air-defense sorties and runway denial without risking billion-dollar jets. Army formations remain heavy buyers for organic precision fires. Yet, naval operators are now booking the fastest 12.46% CAGR as war-gaming proves that 30-drone swarms can saturate shipboard interceptors at a fraction of missile cost. The US Marine Corps intends to field three munition types across every infantry battalion by 2026, signaling how littoral forces will blur lines between land and sea employment. Border-security and special-operations agencies round out demand with lightweight variants that pack into patrol vehicles, expanding the customer base beyond traditional militaries.

Geography Analysis

North America maintained a 38.65% share in 2024 owing to deep US budgets and established manufacturing ecosystems. Congress appropriated USD 10.1 billion for uncrewed-vehicle programs in FY 2025, anchoring long-term demand. Large-volume Switchblade deliveries and the Marine Corps OPF-Light program ensure domestic plant utilization and export readiness.

Europe accelerated adoption via NATO capability targets and national rearmament. France is investing EUR 2 billion (USD 2.34 billion) to field 1,800 units under Colibri and Larinae. At the same time, Germany inserted loitering munitions into its EUR 100 billion (USD 117.07 billion) modernization fund following lessons from Ukraine. Estonia’s multi-year framework illustrates how smaller nations now embed these weapons in divisional structures, supported by EU defense-industrial policy harmonization.

Asia-Pacific is the fastest-growing region at a 10.61% CAGR. India signed INR 2 billion (USD 22.71 million) in local contracts covering altitude-capable systems, aligning with Make-in-India goals and contested-border needs. South Korea partnered with Israel Aerospace Industries to co-develop manned-unmanned-teaming solutions, enhancing regional self-sufficiency. Australia’s OWL B initiative underpins alliance interoperability while building a sovereign production base.

Competitive Landscape

Market concentration is moderate. AeroVironment secured a USD 990 million, five-year US Army contract that sustains high-rate production and solidifies its leadership. Yet agile firms such as XTEND Defense won Pentagon awards for indoor AI-centric systems, demonstrating room for disruptive entrants.[3]“XTEND Defense Smart Loitering-Munition Contract,” Joint-Forces, JOINT-FORCES.COM

Strategic partnerships characterize current dynamics: MBDA links with Novadem and Delair for rotary and fixed-wing platforms; Korea Aerospace Industries collaborates with Israel Aerospace Industries to pursue regional tenders.[4] “MBDA France Adds Two Loitering Munitions to Akeron Family,” EDR Magazine, EDRMAGAZINE.EU Electronic-warfare resilience, autonomous target recognition, and cost-efficient swarm launchers are primary differentiation vectors.

Domestic-production mandates in India, Estonia, and Australia create carve-outs for local firms, reshaping traditional supply chains. Counter-UAS technology progress also pressures incumbents to evolve, fuelling a race to embed hardened navigation, encrypted mesh networks, and multi-spectral seekers.

Loitering Munition Industry Leaders

AeroVironment, Inc.

Israel Aerospace Industries Ltd.

Elbit Systems Ltd.

UVision Group

Savunma Teknolojileri Mühendislik ve Ticaret A.Ş.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: KNDS France unveiled the MX-10 quadcopter loitering munition at IDEX 2025; 100 units have already reached Ukraine for field evaluation.

- December 2024: XTEND Defense received a USD 8.8 million DoD contract for AI-guided, indoor/outdoor tactical munitions.

- September 2024: Australia advanced the One-Way Loitering B program into manufacturing, testing, and evaluation under a government contract.

- August 2024: AeroVironment won a USD 990 million US Army deal for Switchblade systems with deliveries commencing within months.

Global Loitering Munition Market Report Scope

| Aerial (UAV-Launched) |

| Ground-Launched |

| Naval-Launched |

| Short Range (Less than 50 km) |

| Medium Range (50 to 100 km) |

| Long Range (Greater than 100 km) |

| Fragmentation |

| Shaped-charge |

| Thermobaric |

| Air-Launched Effect |

| Vertical Take-off |

| Canister Launched |

| Catapult Launched |

| Hand Launched |

| Army |

| Navy |

| Air Force |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Aerial (UAV-Launched) | ||

| Ground-Launched | |||

| Naval-Launched | |||

| By Range | Short Range (Less than 50 km) | ||

| Medium Range (50 to 100 km) | |||

| Long Range (Greater than 100 km) | |||

| By Warhead Type | Fragmentation | ||

| Shaped-charge | |||

| Thermobaric | |||

| By Launch mode | Air-Launched Effect | ||

| Vertical Take-off | |||

| Canister Launched | |||

| Catapult Launched | |||

| Hand Launched | |||

| By End User | Army | ||

| Navy | |||

| Air Force | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the loitering munition market in 2030?

The loitering munition market size was valued at USD 635.88 million in 2025 and is forecasted to reach USD 1,066.43 million by 2030 with a CAGR of 10.89%.

Which platform type currently generates the most revenue?

Aerial (UAV-launched) systems held 43.21% of 2024 revenue, reflecting mature integration with existing drone fleets.

Which region is growing the fastest?

Asia-Pacific is projected to expand at a 10.61% CAGR from 2025 to 2030, led by India, South Korea, and Australia.

What is the main regulatory hurdle for exporters?

Missile Technology Control Regime rules limit transfers of systems nearing 300 km range or 500 kg payload, tightening licensing for long-range models.

How are navies using loitering munitions?

Naval forces are testing swarm launchers that deploy dozens of expendable drones from shipboard canisters for littoral defense and distributed strike missions.

Which warhead type is gaining popularity in urban warfare?

Thermobaric warheads are growing at a 9.65% CAGR due to superior blast effects against fortified or enclosed positions.

Page last updated on: