Local Anesthesia Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.44 Billion |

| Market Size (2031) | USD 6.43 Billion |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

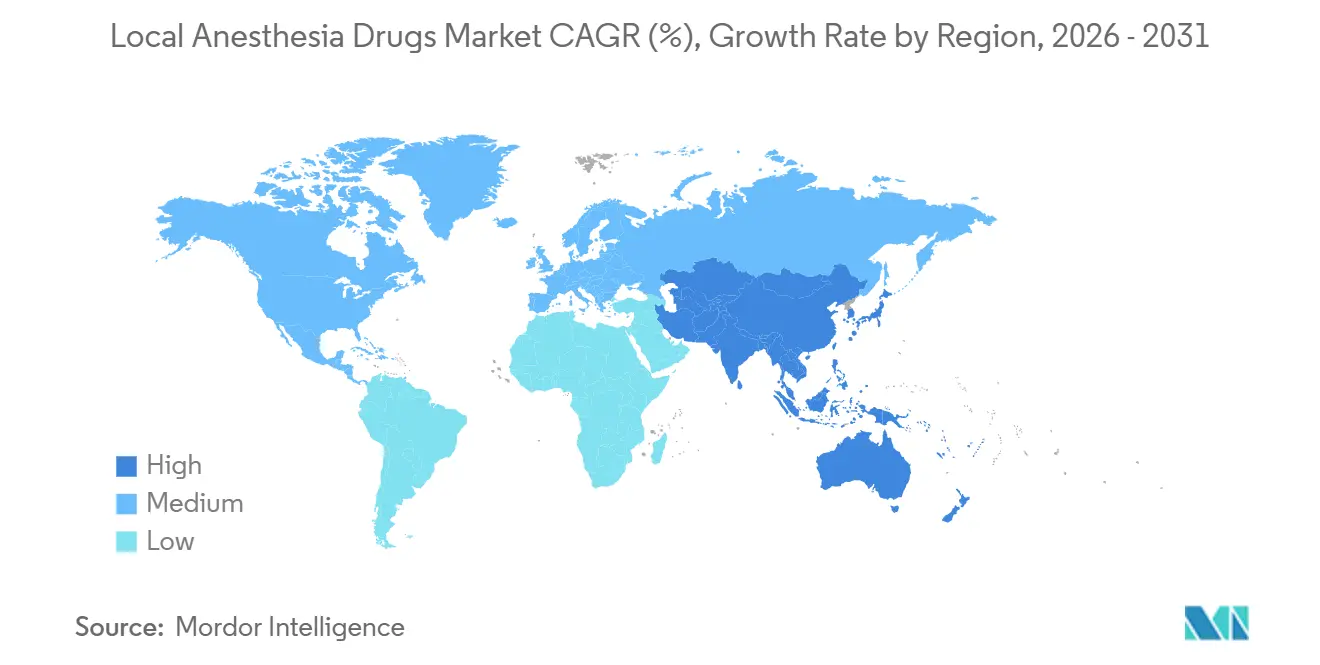

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Local Anesthesia Drugs Market Analysis by Mordor Intelligence

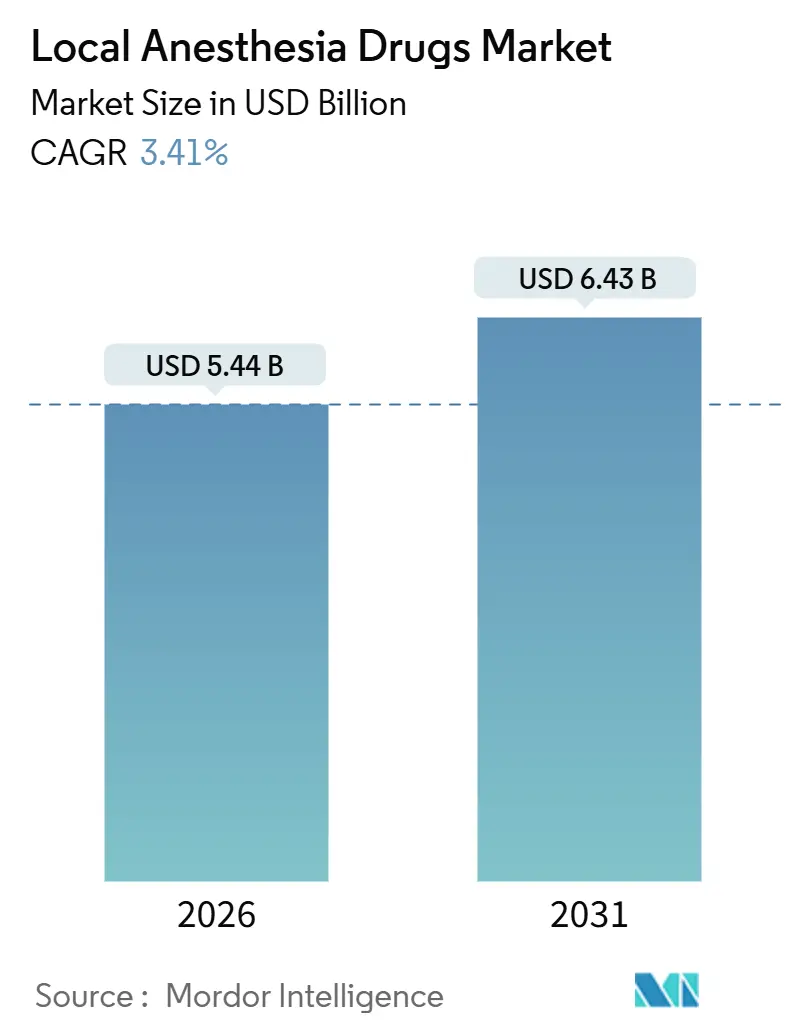

The Local Anesthesia Drugs Market size is estimated at USD 5.44 billion in 2026, and is expected to reach USD 6.43 billion by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

Uptake is reinforced by reimbursement reforms that reward non-opioid analgesia, ultrasound-guided regional blocks that optimize per-procedure dosing, and long-acting liposomal platforms that condense multi-dose courses into a single injection. Separate payment pathways for non-opioid pain control under the 2025 NOPAIN Act have tipped formularies toward local options, while a steady stream of polymer-based launches provides competitive alternatives to opioids in same-day settings. Injectable formats remain dominant; however, topical creams and patches, driven by home-health adoption, are expanding faster than the overall market. Clinician preference for ropivacaine in obstetric and pediatric nerve blocks, combined with hospital dual-sourcing strategies that hedge against sterile injectable shortages, is reshaping supplier dynamics. Generic approvals of complex liposomal bupivacaine and ready-to-use ropivacaine have added price pressure but also validated extended-release technologies, encouraging broader formulary coverage.

Key Report Takeaways

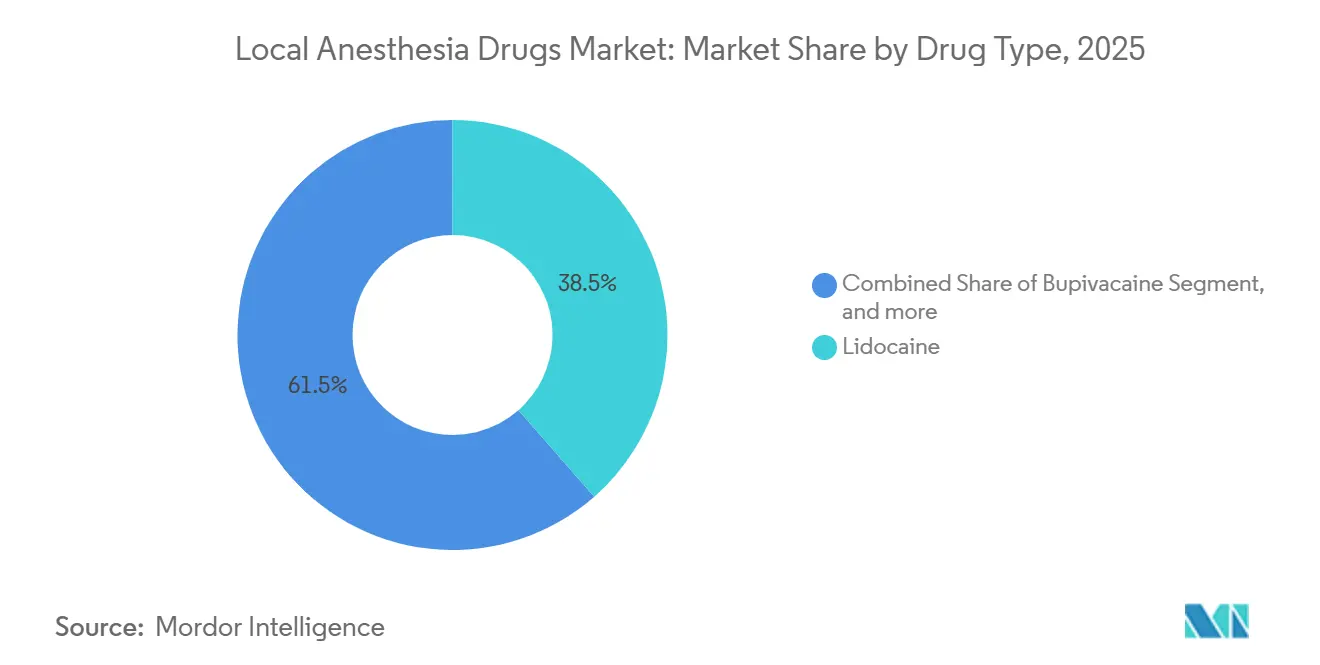

- By drug type, lidocaine commanded 38.54% of 2025 revenue, whereas ropivacaine is forecast to post a 5.67% CAGR to 2031, the highest within the class.

- By mode of administration, injectables held 71.43% local anesthesia drugs market share in 2025, while surface anesthetics are set to expand at a 5.87% CAGR through 2031.

- By application, surgical anesthesia contributed 55.67% of the 2025 revenue, but dental anesthesia is projected to grow the fastest, at 6.87%, through 2031.

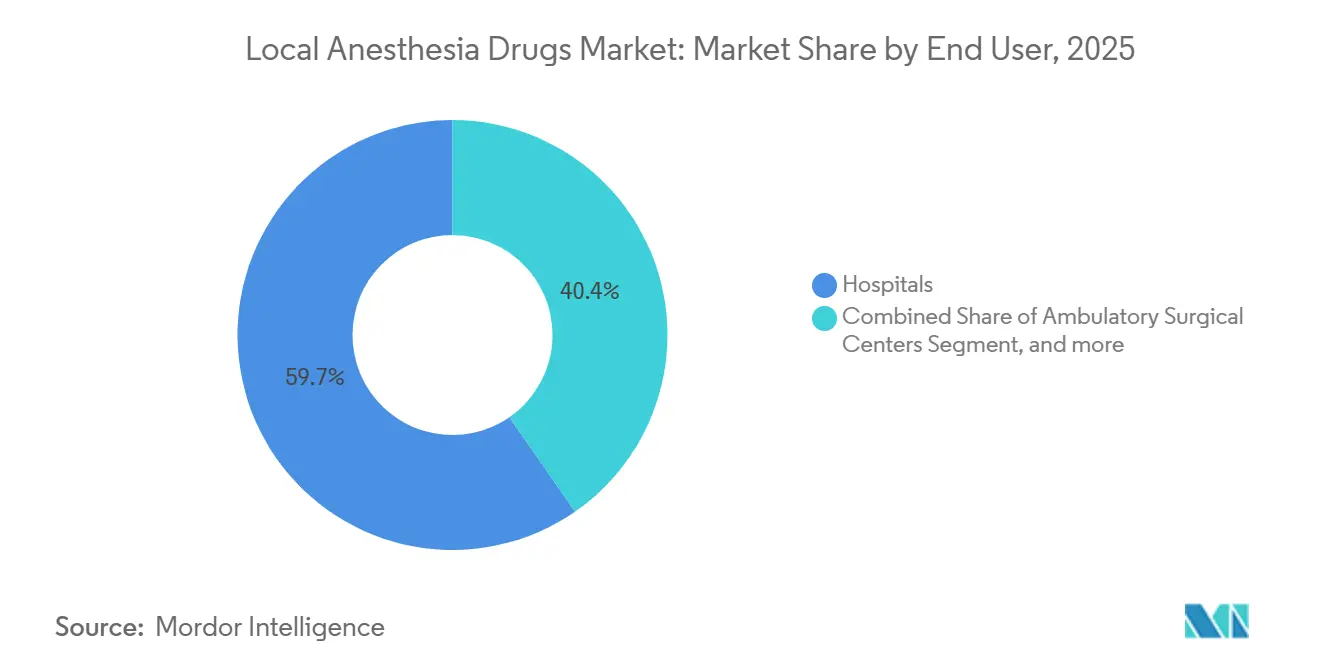

- By end user, hospitals generated 59.65% of the 2025 demand; however, ambulatory surgical centers are expected to rise at a 6.32% CAGR across the forecast period.

- By distribution channel, direct institutional tenders accounted for 58.54% of sales in 2025, while online pharmacies are projected to achieve a 6.54% CAGR from 2025 to 2031.

- By geography, North America accounted for 42.56% of sales in 2025, while the Asia-Pacific region is projected to achieve a 4.56% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Local Anesthesia Drugs Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volume globally | +0.9% | Global, led by North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing approvals of novel formulations | +0.7% | North America and Europe with Asia-Pacific spillover | Short term (≤ 2 years) |

| Adoption in ambulatory and day-care surgery | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Ultrasound-guided regional blocks | +0.6% | North America, Europe, select Asia-Pacific centers | Long term (≥ 4 years) |

| Long-acting liposomal and polymer matrices | +0.5% | North America, Western Europe | Long term (≥ 4 years) |

| Expanding dental tourism | +0.3% | Asia-Pacific, Latin America, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volume Globally

Elective backlogs in OECD economies are expected to be cleared by late 2025, and hip and knee replacements continue climbing at 4-5% per year, both heavy users of peripheral nerve blocks that drive local anesthesia drug market growth[1]Organisation for Economic Co-operation and Development, “Health at a Glance 2024,” oecd.org. China’s hospital-bed target of 7.5 per 1,000 population by 2025 and India’s Ayushman Bharat upgrades are lifting amide anesthetic consumption for infiltration and neuraxial techniques. Medicare beneficiaries underwent 222.1 ASC procedures per 1,000 enrollees in 2023, underscoring the shift of intermediate cases to venues that rely on regional blocks. Enhanced Recovery After Surgery protocols from the World Bank standardize single-shot blocks in colorectal and orthopedic cases, cementing predictable drug demand. Collectively, these volume gains contribute a measurable uplift to the CAGR of the local anesthesia drugs market.

Increasing Approvals and Launches of Novel Local Anesthetics

The 2024 U.S. approval of ZYNRELEF, a bupivacaine–meloxicam polymer, delivers 72-hour pain control and directly competes with opioid tablets[2]U.S. Food and Drug Administration, “NDA Approval Letter for ZYNRELEF,” fda.gov. Jiangsu Hengrui received a green light for its generic liposomal bupivacaine in July 2024, erasing a single-supplier bottleneck and validating biosimilar pathways for complex injectables. Baxter’s ready-to-use ropivacaine eliminates the need for on-site compounding, a proposition valued by hospitals facing contamination alerts. Pacira BioSciences responded with new process patents for EXPAREL in December 2024, extending exclusivity and prompting rivals to seek alternative carriers. Accelerated pipelines shorten adoption lags, lifting product refresh rates across the local anesthesia drugs market.

Growing Adoption in Ambulatory & Day-Care Surgeries

Payment parity under the 2025 NOPAIN Act removes financial penalties for non-opioid analgesics in ASCs and hospital outpatient departments, increasing formulary ordering of long-acting local anesthetics. MedPAC data show that ASC rates rose faster than outpatient department rates in 2024, incentivizing the migration of orthopedic and ophthalmology procedures that favor nerve blocks over general anesthesia. Updated ASA guidelines recommend rapid-onset chloroprocaine for cesarean delivery in low-resource facilities, expanding rural demand. Dental service organizations leverage volume contracts for articaine and lidocaine cartridges, standardizing usage patterns in over 15% of U.S. practices. Together, these shifts deepen penetration of the local anesthesia drugs market in same-day care.

Shift Toward Ultrasound-Guided Regional Anesthesia

Visualization reduces the risk of systemic toxicity and improves block success, encouraging investments in portable ultrasound systems and training. ASRA’s practice advisory mandates lipid-emulsion rescue kits, which raises hospital preparedness costs but reassures clinicians. Ropivacaine-based transversus abdominis plane blocks lower postoperative opioid use by up to 40%, aligning with federal opioid-reduction targets. B. Braun’s USD 1 billion North American expansion underscores confidence in growing demand for needles and catheters. Although lower volumes per block trim per-case usage, the higher number of procedures lifts aggregate volumes across the local anesthesia drugs market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Systemic toxicity and adverse events | -0.4% | Global, higher in low-resource centers | Short term (≤ 2 years) |

| Stringent regulatory requirements for new molecules | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Supply shortages of key active pharmaceutical ingredients | -0.5% | Global, acute in North America | Short term (≤ 2 years) |

| Rising use of non-pharmacological analgesia | -0.2% | North America, Europe, urban Asia-Pac | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Systemic Toxicity and Adverse Events Associated with Amide Anesthetics

Local anesthetic systemic toxicity, though rare, carries high mortality without immediate lipid-emulsion rescue, obligating each operating suite to stock 20% Intralipid and train staff, adding direct costs. FDA labeling emphasizes incremental dosing and maximum limits, yet case reports continue, often linked to inadvertent intravascular injections. Benzocaine spray warnings about methemoglobinemia have pushed ENT specialists toward lidocaine viscous alternatives, reshuffling topical shares. Ropivacaine offers a safer cardiac profile but costs 20-30% more than bupivacaine, limiting access in price-sensitive regions. Portable ultrasound can reduce the incidence of toxicity. Yet, units cost USD 10,000–30,000 and require training, creating a hurdle for smaller ambulatory centers that would otherwise expand the local anesthesia drugs market.

Stringent Regulatory Requirements for New Anesthetic Molecules

Bringing a novel agent to market requires non-inferiority trials versus entrenched comparators, multi-ethnic pharmacokinetics, and long-term safety surveillance, which can consume up to 12 years and nearly USD 1 billion in R&D. The EMA demands separate release-kinetic assessments for combination products, thereby prolonging approvals. Liposomal generics must replicate release curves without infringing process patents, a technical barrier that delayed Hengrui’s bupivacaine approval despite demonstrated equivalence. Manufacturing quality lapses trigger FDA warning letters and temporary shutdowns, as seen in sterile injectable plants in 2024, discouraging smaller entrants and slowing innovation within the local anesthetic drugs market.

Segment Analysis

By Drug Type: Ropivacaine Gains on Safety Profile

In 2025, lidocaine accounted for 38.54% of revenue, maintaining its position in rapid-onset dental and minor surgical blocks. Ropivacaine is forecast to expand at 5.67% annually, the fastest among its peers, as obstetric and pediatric units prioritize its lower cardiotoxicity[3]American College of Obstetricians and Gynecologists, “Practice Bulletin 209 Update,” acog.org. Bupivacaine, though still favored for lengthy spine and joint procedures, faces usage caps in settings without advanced resuscitation capabilities. Benzocaine’s decline follows FDA methemoglobinemia warnings, steering demand toward safer amide alternatives.

Liposome-encapsulated bupivacaine straddles categories by delivering 72-hour coverage, attracting centers seeking opioid-free discharges. Chloroprocaine’s rapid offset makes it ideal for cesarean spinal blocks, as per ASA’s 2024 guidance, thereby widening its rural penetration. These shifts diversify the local anesthesia drugs market, with safety and duration rather than cost becoming decisive purchasing criteria.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Administration: Surface Anesthetics Ride Home-Health Wave

Injectables accounted for 71.43% of 2025 revenue, as surgery, obstetrics, and dentistry rely on precise dosing. Surface formats are projected to grow at a rate of 5.87% to 2031, driven by the increasing adoption of lidocaine patches for neuralgia among the elderly and dermatology’s preference for EMLA cream during minimally invasive aesthetic procedures. Over-the-counter sales of ≤4% lidocaine products expand retail access, while prescription-strength patches remain reimbursable in many markets, thereby increasing volumes.

Ready-to-use ropivacaine injectables mitigate compounding risks, justifying premium prices in hospitals that have battled contamination alerts. Topicals maintain a more diverse supplier base, insulating the channel from the shortages plaguing sterile injectables. This resilience supports consistent expansion of the local anesthesia drugs market size within consumer and outpatient settings.

By Application: Dental Anesthesia Accelerates on DSO Consolidation

Surgical anesthesia accounted for 55.67% of 2025 revenue, yet dental applications are poised for a 6.87% CAGR, the fastest growth rate across categories. Group purchasing by dental service organizations secures discounts on articaine cartridges, raising throughput in consolidated clinics. Cross-border dental tourism funnels foreign patients to ASEAN and Latin American hubs, where demand for lidocaine and articaine is bundled into procedural packages.

Post-operative pain control is shifting to single-shot liposomal injections that extend relief beyond discharge, cutting opioid tablets and nursing callbacks. Obstetric neuraxial blocks remain entrenched, with over 60% of U.S. singleton births using epidural or spinal anesthesia, sustaining bupivacaine and ropivacaine volumes. Broad application diversity stabilizes revenue streams across the local anesthesia drugs market.

By End User: ASCs Gain on Payment Parity

Hospitals captured 59.65% of the 2025 demand as primary sites for complex interventions and trauma care. Ambulatory surgical centers are expected to post a 6.32% CAGR, buoyed by NOPAIN Act parity and surgeon preference for efficient workflows. Specialty pain clinics and dermatology offices are expanding their use of injections for musculoskeletal pain and cosmetic procedures, thereby diversifying their end-user revenue.

Dental clinics benefit from higher elective-procedure volumes and DSO-driven cartridge standardization. Home-health services represent an emerging niche where caregivers apply topical anesthetics for wound care and cannulation, enlarging the addressable population. Together, these channels reinforce stability and growth across the local anesthesia drugs market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Exploit E-Prescribing

Direct institutional tenders commanded 58.54% of 2025 sales, leveraging volume contracts and supply guarantees. Online pharmacies are forecast to grow at 6.54%, assisted by e-prescribing rules for non-controlled anesthetics and consumer preference for home delivery. Retail chains face reimbursement squeezes and rising mail-order competition, which is accelerating their shift to online operations.

Group purchasing organizations aggregate demand across multiple hospital systems, intensifying price negotiations and favoring suppliers with broad portfolios and just-in-time delivery options. Online platforms dynamically source from multiple wholesalers, which can cushion shortages but also challenge brand loyalty. This evolving mix distributes risk and opportunity across the local anesthesia drugs market.

Geography Analysis

North America generated 42.56% of 2025 revenue, propelled by the highest surgical incidence worldwide, early adoption of liposomal bupivacaine and polymer combinations, and reimbursement structures that reward non-opioid analgesia. The GAO confirmed that 71 of 102 active U.S. shortages involve sterile injectables, leading hospitals to dual-source lidocaine and bupivacaine, sometimes at premium prices. Canada’s publicly funded system supports broad access, while Mexico’s medical tourism corridor boosts private-sector demand.

The Asia-Pacific region is projected to achieve a 4.56% CAGR from 2021 to 2031, driven by the expansion of hospital beds in China and India, as well as government support for rural surgery. China’s 7.5-beds-per-1,000 target elevates procedural throughput, directly increasing amide anesthetic consumption. India’s Ayushman Bharat upgrades secure operating rooms equipped for regional blocks, lowering dependency on anesthesiologists and broadening patient reach.

Europe offers stable, low-growth prospects due to rigorous EMA reviews and tender-driven pricing. The United Kingdom’s NRFit connector mandate accelerates product refreshes and favors suppliers certified to ISO standards. Urban centers in the Middle East and Africa are adopting ultrasound-guided techniques, while Latin America is leveraging dental tourism and expanding middle-class spending. Currency swings in South America, however, translate into revenue-recognition volatility for global manufacturers active in the local anesthesia drugs market.

Competitive Landscape

The local anesthesia drugs market is moderately fragmented. Pacira BioSciences leads the premium segment, with EXPAREL surpassing USD 500 million in sales in 2024 and fresh patents that extend exclusivity. FDA approval of Hengrui’s generic liposomal bupivacaine breaks Pacira’s monopoly, slicing institutional prices and prompting polymer-based alternatives. Hikma’s USD 135 million acquisition of Xellia’s U.S. injectables portfolio widens capacity, positioning the firm to capture share during supply disruptions.

B. Braun’s billion-dollar North American build-out guarantees domestic syringe and catheter output, appealing to hospitals that prioritize secure supply chains. Regional players, such as Cristália, Tonghua Dongbao, and Septodont, exploit local networks to offer cost-competitive amide generics, further fragmenting the market shares. ASHP-documented shortages elevate the strategic value of redundancy, leading pharmacy directors to award contracts based on reliability as well as price.

Local Anesthesia Drugs Industry Leaders

Fresenius SE & Co. KGaA

Pacira Pharmaceuticals, Inc.

Pfizer Inc.

Septodont

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Glenmark Pharma launched a generic Ropivacaine Hydrochloride injection for local anesthesia in the United States. This move aims to expand Glenmark’s presence in the American pharmaceutical market.

- August 2025: Avenacy introduced its first Lidocaine Hydrochloride Injection, USP in the United States. The product, a generic version of XYLOCAINE, is approved by the FDA for local anesthesia. It comes in 50 mL vials with 500 mg of lidocaine and is sold in cartons of 25 vials.

- August 2024: Amneal Pharmaceuticals, Inc. received Abbreviated New Drug Application (“ANDA”) approval from the U.S. Food and Drug Administration (FDA) for Propofol Injectable Emulsion USP, 200 mg/20 mL (10 mg/mL), 500 mg/50 mL (10 mg/mL), and 1,000 mg/100 mL (10 mg/mL), Single-Dose Vials. Propofol is an intravenous drug commonly used in hospitals for the induction and maintenance of anesthesia and sedation.

Global Local Anesthesia Drugs Market Report Scope

According to the report's scope, local anesthesia drugs are medications used to numb a specific area of the body, thereby preventing pain during medical procedures. They work by blocking nerve signals in the targeted region. These drugs provide pain relief while keeping the patient awake and aware.

The Local Anesthesia Drugs Market is Segmented by Drug Type (Bupivacaine, Lidocaine, Benzocaine, Ropivacaine, Prilocaine, Chloroprocaine, and Other Drug Types), Mode of Administration (Injectable and Surface Anesthetic), Application (Surgical Anesthesia, Post-Operative Pain Management, Dental Anesthesia, Labor & Delivery Analgesia, and Chronic Pain Management), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Dental Clinics, and Home Healthcare Settings), Distribution Channel (Institutional Sales, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Bupivacaine |

| Lidocaine |

| Benzocaine |

| Ropivacaine |

| Prilocaine |

| Chloroprocaine |

| Other Drug Types |

| Injectable |

| Surface Anesthetic |

| Surgical Anesthesia |

| Post-Operative Pain Management |

| Dental Anesthesia |

| Labor & Delivery Analgesia |

| Chronic Pain Management |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Dental Clinics |

| Home Healthcare Settings |

| Institutional (Direct/Tender) Sales |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Type | Bupivacaine | |

| Lidocaine | ||

| Benzocaine | ||

| Ropivacaine | ||

| Prilocaine | ||

| Chloroprocaine | ||

| Other Drug Types | ||

| By Mode of Administration | Injectable | |

| Surface Anesthetic | ||

| By Application | Surgical Anesthesia | |

| Post-Operative Pain Management | ||

| Dental Anesthesia | ||

| Labor & Delivery Analgesia | ||

| Chronic Pain Management | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Dental Clinics | ||

| Home Healthcare Settings | ||

| By Distribution Channel | Institutional (Direct/Tender) Sales | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected value of the local anesthesia drugs market in 2031?

The local anesthesia drugs market is forecast to reach USD 6.43 billion by 2031.

Which drug type is expected to grow the fastest through 2031?

Ropivacaine is projected to expand at a 5.67% CAGR, the quickest among major agents.

How will ambulatory surgical centers influence demand?

Payment parity under the NOPAIN Act supports a 6.32% CAGR in ASC purchases, lifting overall market volumes.

Why are surface anesthetics gaining popularity?

Expanded home-health use of lidocaine patches and OTC creams drives a 5.87% CAGR for surface formats.

Which region offers the strongest growth outlook?

Asia-Pacific is set for a 4.56% CAGR, supported by hospital-bed expansion and rising medical tourism.

How are supply shortages affecting hospital procurement?

Facilities now dual-source injectables and value suppliers with domestic capacity, raising resilience but also acquisition costs.