Market Overview

| Study Period | 2020 - 2031 |

|---|---|

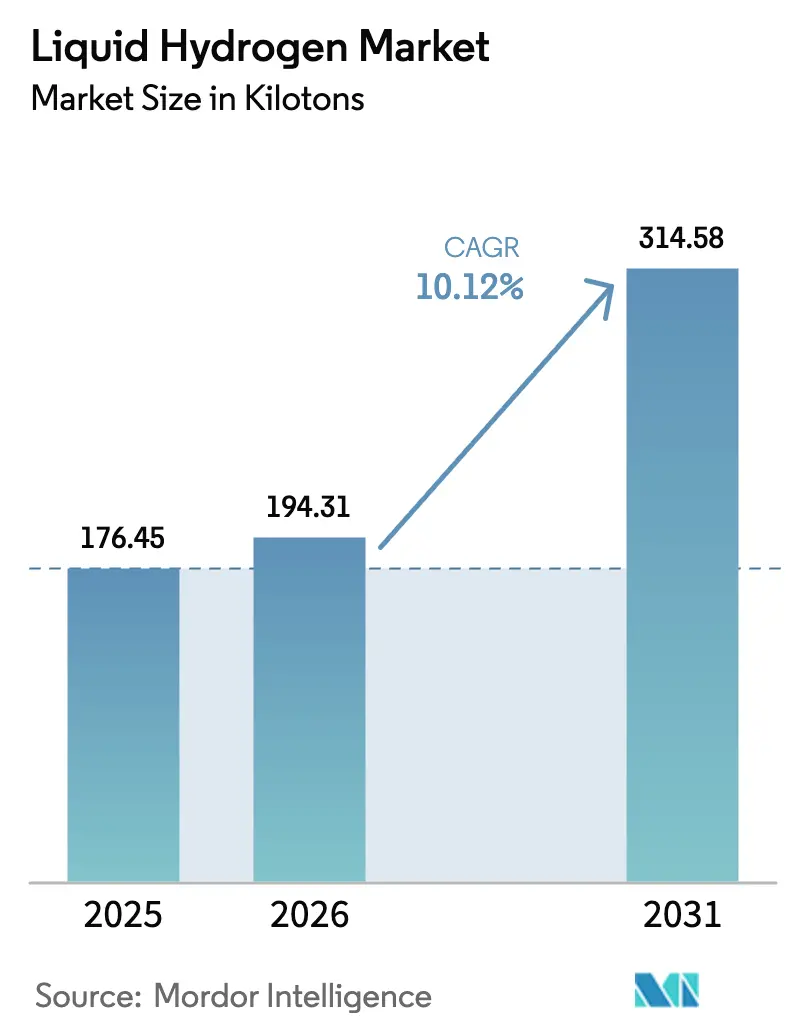

| Market Volume (2026) | 194.31 kilotons |

| Market Volume (2031) | 314.58 kilotons |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Hydrogen Market Analysis by Mordor Intelligence

The Liquid Hydrogen Market size was valued at 176.45 kilotons in 2025 and estimated to grow from 194.31 kilotons in 2026 to reach 314.58 kilotons by 2031, at a CAGR of 10.12% during the forecast period (2026-2031). A rising launch cadence linked to NASA’s Artemis program, accelerating heavy-duty fuel-cell truck deployments, and Asia-Pacific’s gigawatt-scale liquefaction projects are aligning to propel volume growth. Demand is further amplified by depot-scale refueling stations that enable 1,000 km FCEV range, while zero-boil-off storage advances cut operating losses to below 0.1% per day. Integrated value-chain strategies are becoming essential because production, liquefaction, and distribution assets must move in tandem with downstream mobility and aerospace requirements. However, the liquid hydrogen market faces headwinds from helium scarcity, electro-intensive liquefiers, and the economics of small-footprint stations, even as breakthroughs in ortho-para conversion and composite cryotanks promise step-change efficiency gains.

Key Report Takeaways

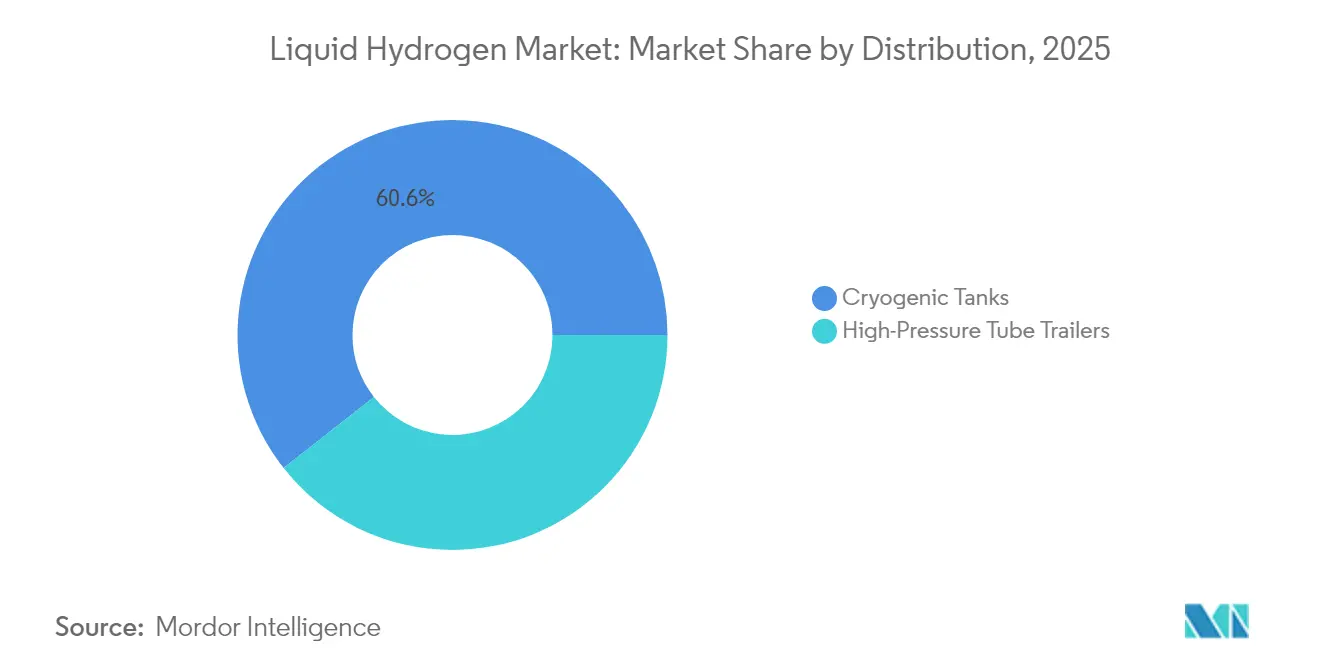

- By distribution, cryogenic tanks held 60.62% of the liquid hydrogen market share in 2025, while high-pressure tube trailers are projected to expand at an 11.05% CAGR through 2031.

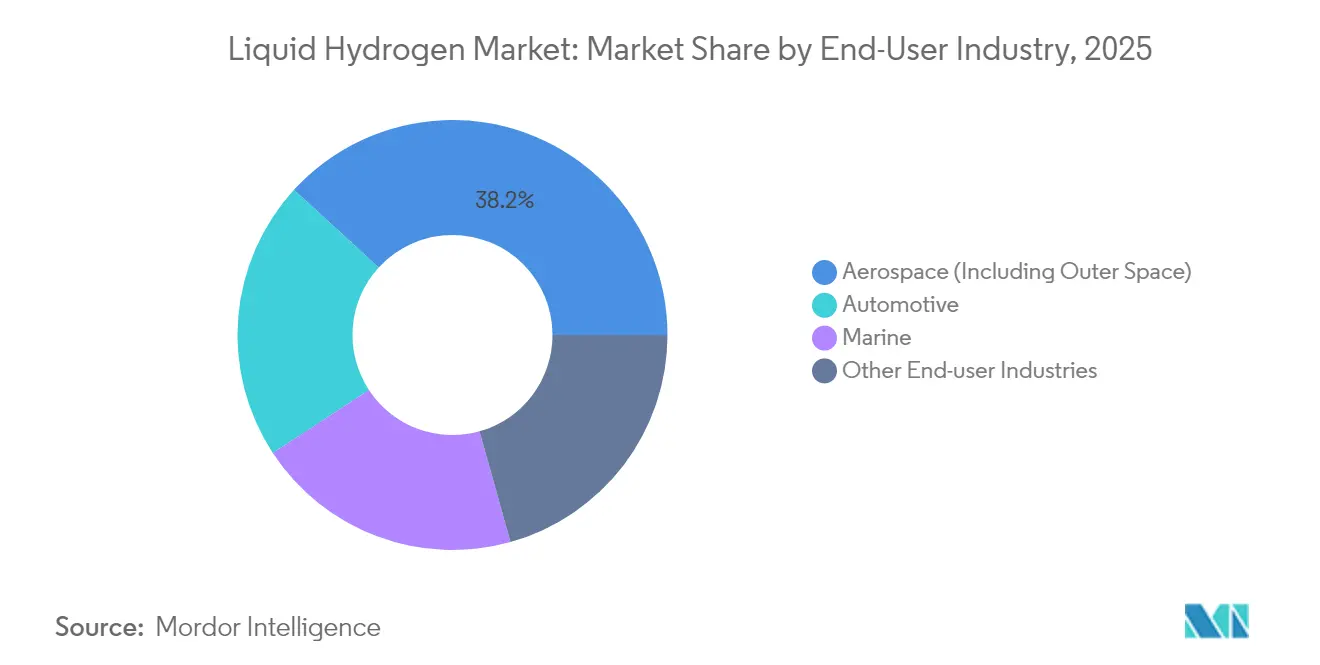

- By end-user industry, aerospace commanded 38.20% of the liquid hydrogen market size in 2025, whereas automotive is advancing at a 13.05% CAGR through 2031.

- By geography, North America accounted for 42.10% of the liquid hydrogen market share in 2025, while Asia-Pacific is forecast to post an 11.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Hydrogen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Launch Cadence and Lunar Mission Programs Post-Artemis | +2.8% | North America, with spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Commercial FCEV Truck Roll-Outs Needing Depot-Scale LH₂ Refuelling | +2.1% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Asia-Pacific Gigawatt-Scale Liquefiers Coming Online | +1.9% | APAC core, with spillover to global supply chains | Medium term (2-4 years) |

| Cost-Down in Ortho-Para Catalytic Conversion Packs | +1.4% | Global | Long term (≥ 4 years) |

| Cryogenic Carbon-Composite Tank Breakthroughs | +1.2% | Global, with early adoption in aerospace and automotive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Launch Cadence and Lunar Mission Programs Post-Artemis

NASA’s Artemis agenda has re-defined liquid propellant logistics by proving that zero-boil-off technology cuts propellant loss by 98% during multi-month storage in space. Aerospace primes now incorporate these findings into satellite-servicing architectures, creating a secondary pull for advanced liquid hydrogen systems. ESA aims to deploy a comparable zero-boil-off framework for its 2027 lunar gateway, broadening geographic demand. Private launch providers are co-locating liquefiers near pads to hedge supply risk, a move that accelerates regional capacity build-outs. Collectively, the surge in civil and commercial missions is anchoring long-term visibility for the liquid hydrogen market.

Commercial FCEV Truck Roll-Outs Needing Depot-Scale LH₂ Refueling

Mercedes-Benz GenH2 trials with Air Products validated liquid hydrogen’s superiority for Class 8 trucks by logging 1,000 km ranges and sub-15-minute refuels[1]Air Products, “Mercedes-Benz GenH2 Truck Trial Results,” airproducts.com . Fleet tenders in Europe now stipulate depot-scale liquid hydrogen capability, while TEAL Mobility plans 100 refueling stations by 2030, each designed for high-throughput loading. Heavy-duty corridor build-outs are cascading into demand for 20-40 ton-per-day liquefaction skids. As operators chase diesel parity, the liquid hydrogen market benefits from total-cost-of-ownership gains linked to higher gravimetric energy density.

Asia-Pacific Gigawatt-Scale Liquefiers Coming Online

China’s 23,000 ton-per-year Anyang plant signals the region’s shift from import dependence to export surplus. South Korea’s West Coast Hydrogen Belt adds a USD 7.8 billion integrated complex that spans electrolysis, liquefaction, and marine export terminals. Japan backs multiple projects scheduled for 2026-2028 start-ups to synchronize with its next wave of FCEV roll-outs. The clustering effect lowers delivered cost below USD 2.50/kg, undercutting compressed hydrogen alternatives and strengthening the liquid hydrogen market’s competitive stance.

Cost-Down in Ortho-Para Catalytic Conversion Packs

Next-generation Mn₃O₄ and CoO catalysts trim conversion energy by 15-20%, shaving as much as USD 0.50/kg off production cost at scale. Fe-Co bimetallic systems add thermal stability, expanding catalyst life and reducing downtime. Magnetocaloric refrigeration prototypes indicate 20-50% efficiency gains against helium-cycle baselines, with commercialization expected by 2028. These advances directly influence liquefier CAPEX and OPEX, reinforcing the liquid hydrogen industry’s push toward cost parity with incumbent fuels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Boil-Off Losses for Small-Footprint Stations | -1.8% | Global, particularly affecting distributed refueling networks | Short term (≤ 2 years) |

| Limited Global Helium Supply for LH₂ Pumps and Seals | -1.2% | Global, with acute impact in regions dependent on imported helium | Medium term (2-4 years) |

| Electro-Intensiveness of Liquefaction Inflates Green-H₂ LCOH | -0.9% | Global, with greater impact in regions with high electricity costs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Boil-Off Losses for Small-Footprint Stations

Throughputs below 200 kg/day typically suffer 2-3% daily boil-off, eroding unit economics[2]NASA, “Small-Scale LH₂ Station Challenges,” nasa.gov . While zero-boil-off architectures exist, the CAPEX premium is prohibitive for low-traffic stations. Toyota’s vapor-recycling system offers mitigation but adds operational complexity. As a result, developers favor hub-and-spoke models with centralized liquefaction, but that limits rural coverage and raises transport costs, muting near-term dispersion of the liquid hydrogen market.

Limited Global Helium Supply for LH₂ Pumps and Seals

Cryogenic pump makers rely on ultra-high-purity helium for seals operating at -256 °C, yet global shortages pushed prices up to 3 × normal levels between 2019-2023. Lead times for 600 kg/h pumps now run 6-12 months, stalling project timelines. Closed-loop helium recovery and nitrogen pre-cooling help, but they require incremental capital. Persistent helium volatility introduces a supply-chain risk premium that weighs on liquefier roll-outs within the liquid hydrogen market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Distribution: Cryogenic Tanks Consolidate Infrastructure Leadership

Cryogenic tanks dominated the liquid hydrogen market size with 60.62% of total volume in 2025, reflecting their legacy use in spaceflight and newly validated zero-boil-off performance benchmarks. The segment’s growth stems from multilayer insulation advances and composite shells that reduce weight by up to one-third while cutting permeation. Operators view stationary cryogenic depots as foundational assets because they scale efficiently with refueling demand spikes. Technological upgrades, including vacuum-jacketed lines and active thermal management, make cryogenic tanks the most cost-effective option for fleet hubs above 5 tons/day.

High-pressure tube trailers, though holding a smaller slice, are forecast to log an 11.05% CAGR through 2031. They attract early-stage corridors that lack the volumes needed for fixed tank farms, giving investors a lower entry cost and route flexibility. Verne’s cryo-compressed platform bridges the two modalities, offering 2× the volumetric density of standard 700 bar tubes and enabling back-to-back loading without time-consuming vent cycles. Regulatory harmonization on gross vehicle mass and ADR compliance in 2026-2027 will widen adoption across interstate freight networks, widening the addressable surface for the liquid hydrogen market.

By End-User Industry: Aerospace Holds Share, Automotive Accelerates

Aerospace retained 38.20% of 2025 demand, underpinned by Artemis, Starship, and ESA lunar gateway launch manifests. Long-duration storage specs for in-orbit depots are cascading into commercial satellite servicing, keeping aerospace the headline anchor of the liquid hydrogen market. Parallel investments in ground-based liquefier redundancy near launch pads further lock in volume offtake. Rocket propulsion’s absolute purity requirements also set the technical bar for upstream processing, indirectly lifting quality standards across other sectors.

Conversely, automotive is registering a 13.05% CAGR to 2031, driven by GenH2-class trucks, Hyundai’s Xcient portfolio, and Nikola-Bosch fuel-cell stacks. Depot operators report payload parity vis-à-vis diesel and sustained 1,000 km ranges, tilting TCO equations toward liquid hydrogen. By 2028, the liquid hydrogen market size attributed to heavy-duty trucking is projected to rival aerospace volumes in North America. SAE’s forthcoming J-2601-5 protocol for cryogenic heavy-duty refueling will set a global dispensing benchmark that could unlock multi-OEM interoperability and accelerate scale-up.

Geography Analysis

North America captured 42.10% of 2025 volume, reflecting NASA procurement cycles, California’s LCFS credits, and Department of Energy H2Hubs funding. Multi-gigawatt electrolyzer pipelines along the Gulf Coast are pairing with existing petrochemical infrastructure, offering salt-cavern storage options that complement above-ground cryogenic tanks. The liquid hydrogen market in the region is additionally buoyed by the July 2025 FMVSS safety standard that codified LH₂ vehicle regulations, de-risking OEM production planning.

Asia-Pacific is poised for the fastest compound lift at 11.12% CAGR to 2031, fueled by China’s Anyang megaproject and Korea’s USD 7.8 billion West Coast Hydrogen Belt. Large-scale carriers under development by HD KSOE and Kawasaki establish maritime export lanes to Japan and Singapore, creating a self-reinforcing ecosystem. Government-backed feed-in tariffs for renewable-powered electrolysis reduce delivered cost, while domestic truck OEMs plan 20,000 FCEV unit output by 2029, deepening offtake. These developments collectively re-balance global liquid hydrogen market capacity toward the East.

Europe’s build-out centers on Air Liquide’s EUR 110 million ENHANCE project and the IPCEI Hy2Infra pipeline plan that strings 2,700 km of hydrogen corridors by 2029. Policy levers such as RED III transport quotas and Fit-for-55 targets accelerate adoption across aviation, maritime, and steel decarbonization. Though the region trails in giga-scale liquefiers, a web of import terminals and ammonia-to-hydrogen cracking projects positions Europe as a high-demand sink for the liquid hydrogen industry. South America and the Middle East and Africa remain nascent but show promise, notably Oman-to-Europe export concepts backed by GasLog’s cryogenic shipping technology.

Competitive Landscape

The liquid hydrogen market is moderately consolidated, with Air Liquide, Linde, and Air Products leveraging end-to-end portfolios that span production to dispensing. Their entrenched cryogenic engineering know-how and patented liquefier cycles deliver scale economies that deter new entrants. Large players are regionalizing supply footprints—Air Liquide in Antwerp, Linde in Texas, Air Products in Rotterdam—to hedge logistics risk and meet local content mandates.

Specialty firms such as Kawasaki Heavy Industries, Hylium, and Verne are carving share by focusing on niche applications: Kawasaki on marine carriers, Hylium on aircraft ground support, and Verne on cryo-compressed distribution. Their agility enables faster prototyping cycles, but they often rely on contract manufacturing partnerships with incumbents for high-volume builds. Intellectual-property filings show a spike in magnetocaloric coolers and composite tank liners, signaling a pipeline of disruptive R&D that could reset cost curves for the liquid hydrogen industry.

Strategically, alliances are proliferating: TotalEnergies-Air Liquide’s TEAL Mobility targets 100 European stations, while Kawasaki-McDermott pair EPC heft with vessel know-how for integrated marine supply chains. M&A interest is rising around helium-recovery IP and low-OPEX liquefier skids, hinting at a consolidation wave aimed at de-risking technology gaps. Overall, top-five players command roughly 80% of installed liquefaction capacity, supporting a market concentration score of 8.

Liquid Hydrogen Industry Leaders

Air Liquide

Linde PLC

Iwatani Corporation

Air Products and Chemicals, Inc.

Messer SE and Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hidrogenii, a Plug Power and Olin Corporation joint venture, commissioned a 15-ton-per-day (TPD) hydrogen liquefaction plant in St. Gabriel, Louisiana. The project is a key part of Plug Power's strategy to build a national green hydrogen network and increases its total hydrogen production capacity to 40 TPD.

- December 2024: Air Liquide received a grant of 110 million euros from the European Innovation Fund for its ENHANCE project in the port of Antwerp-Bruges, Belgium, that aims to produce and distribute low-carbon and renewable hydrogen derived from ammonia. Replacing natural gas with ammonia to produce gaseous and liquid hydrogen would allow the project to reduce the CO₂ emissions by more than 300,000 tonnes per year.

Global Liquid Hydrogen Market Report Scope

The liquified form of hydrogen is clear, non-toxic, and has no color, odor, or taste. Under ambient conditions, the hydrogen molecule is extremely small (about 14 times lighter than air) and has a high diffusion rate and buoyancy.

The Liquid Hydrogen Market is Segmented By Distribution (Cryogenic Tank and High-Pressure Tube Trailers), End-user Industry (Automotive, Aerospace, Marine, and Other End-user Industries). The report also covers the market size and forecasts for the market in 11 countries across the globe. The report offers market size and forecasts for the liquid hydrogen market in volume (tons) for all the above segments.

By Distribution

| Cryogenic Tanks |

| High-Pressure Tube Trailers |

By End-User Industry

| Aerospace (Including Outer Space) |

| Automotive |

| Marine |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Distribution | Cryogenic Tanks | |

| High-Pressure Tube Trailers | ||

| By End-User Industry | Aerospace (Including Outer Space) | |

| Automotive | ||

| Marine | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the liquid hydrogen market in 2026?

The liquid hydrogen market size is 194.31 kilotons in 2026 and is projected to reach 314.58 kilotons by 2031.

Which distribution mode leads current volume?

Cryogenic tanks hold 60.62% of 2025 volume, reflecting their dominance in stationary storage and launch operations.

What is the fastest-growing end-user industry?

Automotive is advancing at a 13.05% CAGR through 2031, driven by heavy-duty fuel-cell truck roll-outs.

Which region is expanding quickest?

Asia-Pacific is forecast to grow at 11.12% CAGR thanks to giga-scale liquefiers in China and South Korea.

Page last updated on: